First-Time Seller Faces a $10K Appraisal Gap, Now the Entire Deal is Hanging by a Thread

We all know that moment when a seemingly done deal suddenly falls apart. For one first-time home seller, a smooth real estate transaction quickly turned into a stressful nightmare after a surprising home appraisal. They listed their property, found a willing buyer, and even agreed to cover some closing costs to sweeten the deal.

But when the bank stepped in, the valuation fell short by ten thousand dollars. Suddenly, the real estate agent was asking the seller to absorb the loss, sparking immediate confusion and frustration. Was this just standard protocol, or was someone trying to pull a fast one? Curious how this high-stakes negotiation unfolded? The full story is right below.

The initial shock of the real estate process was setting in, turning what should have been a straightforward transaction into a confusing financial hurdle.

Reality clashed with expectations, leaving the seller desperately seeking guidance before making a costly final decision.

This seller’s confusion over a $10,000 difference is a remarkably common hurdle in fluctuating housing markets. When a low home appraisal comes in under the agreed-upon purchase price, the shock can paralyze both sides of the transaction, forcing buyers and sellers to return to the negotiating table.

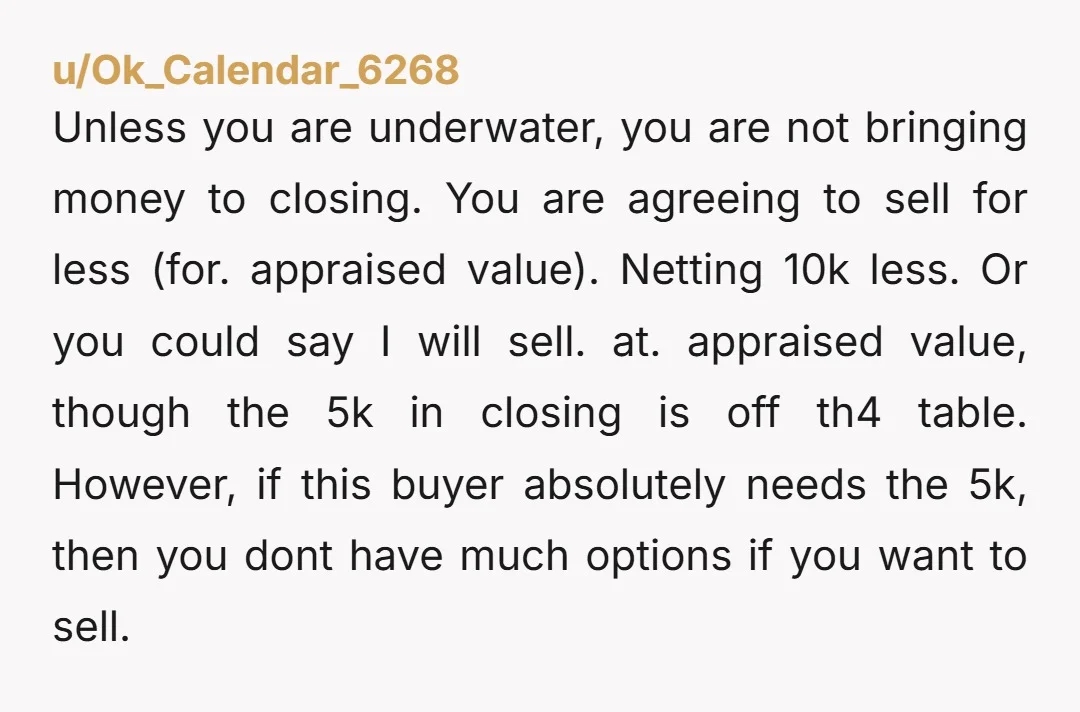

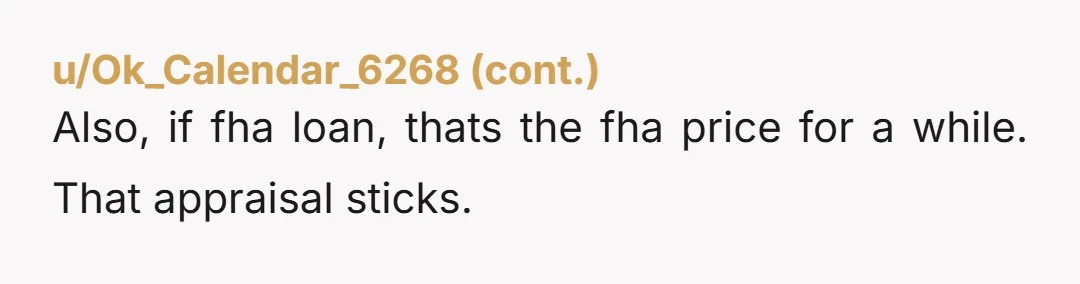

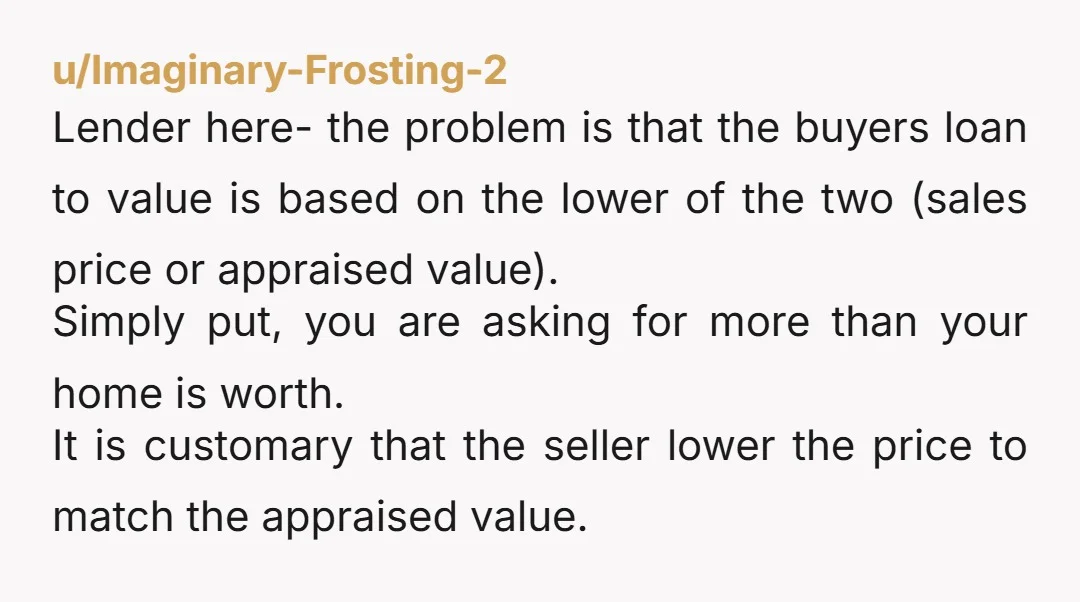

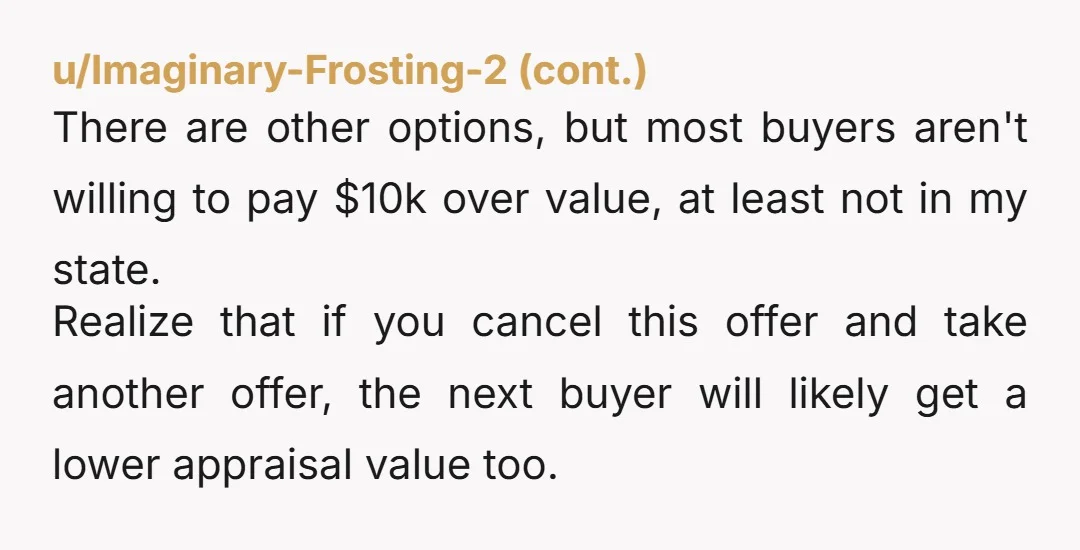

Practically speaking, a seller in this position has three distinct choices: lower the asking price to match the bank’s valuation, negotiate a compromise where the buyer brings extra cash to closing, or terminate the contract entirely. Financial professionals and real estate brokers broadly agree that a lender will simply not finance a mortgage beyond the home’s appraised value.

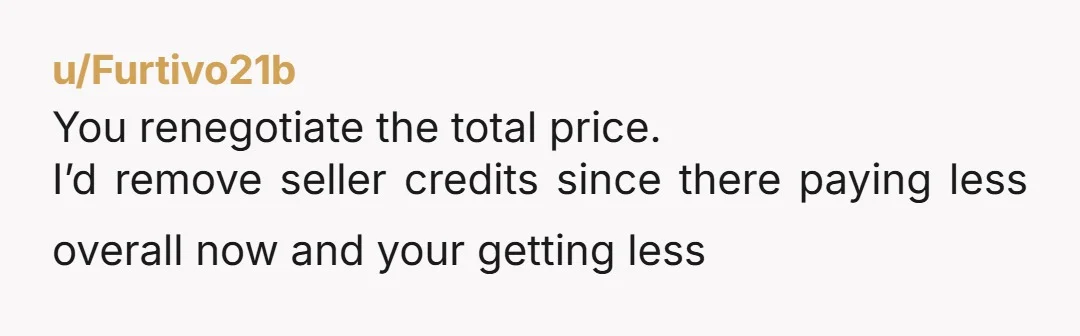

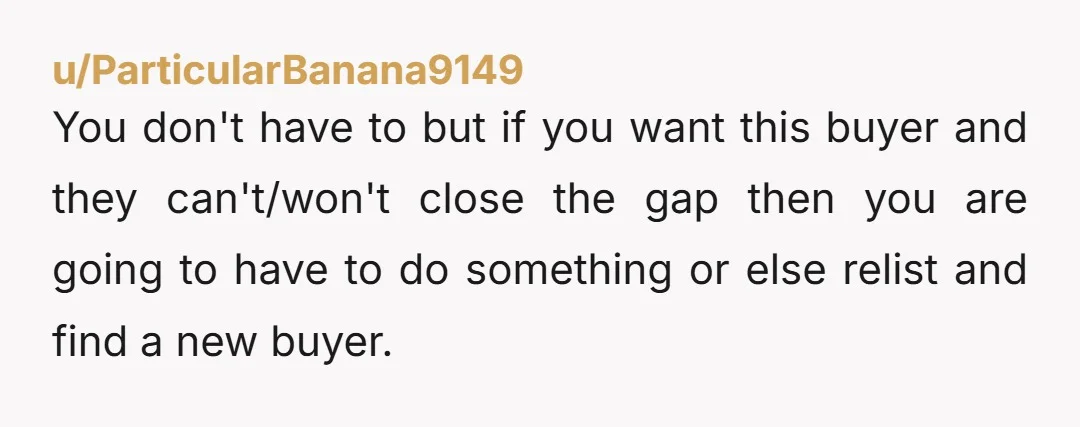

If the seller refuses to budge and the buyer lacks the liquid cash to cover the difference, the deal will likely collapse. To protect their bottom line, the seller might consider restructuring the deal by revoking the initial seller credit to offset the newly reduced price. To learn more about navigating these tricky waters, check out our real estate negotiation guides. The most crucial step is maintaining clear communication with your agent and remaining completely flexible as options are weighed.

Real estate transactions rarely go exactly as planned, and navigating an unexpected appraisal gap requires patience and strategic thinking. Both buyers and sellers have to weigh their financial boundaries against their desire to successfully close the deal.

Do you think the seller should absorb the $10,000 difference to save the sale, or should the buyer be responsible for covering the appraisal gap? And how would you handle a real estate agent asking you to take the financial hit? Share your thoughts below!

Community Opinions

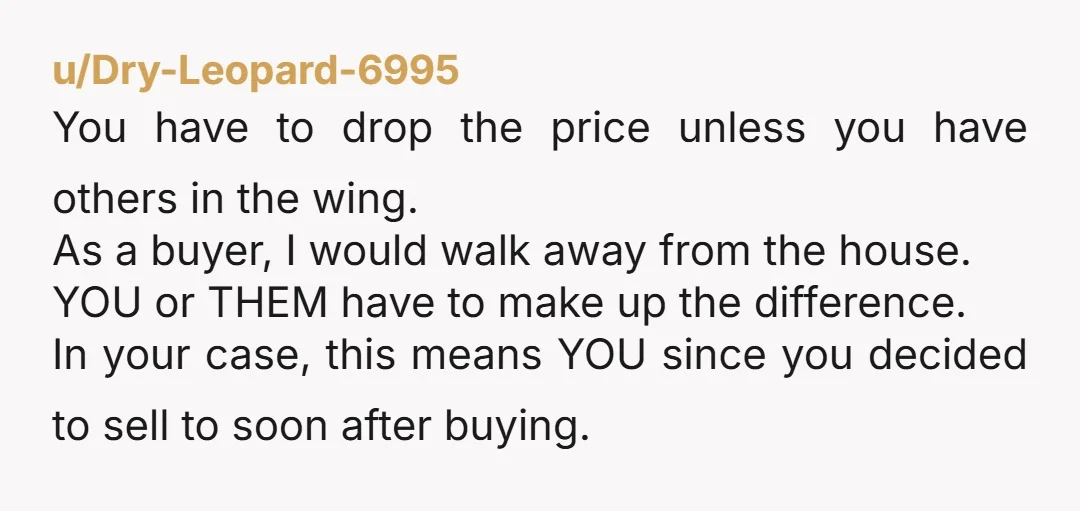

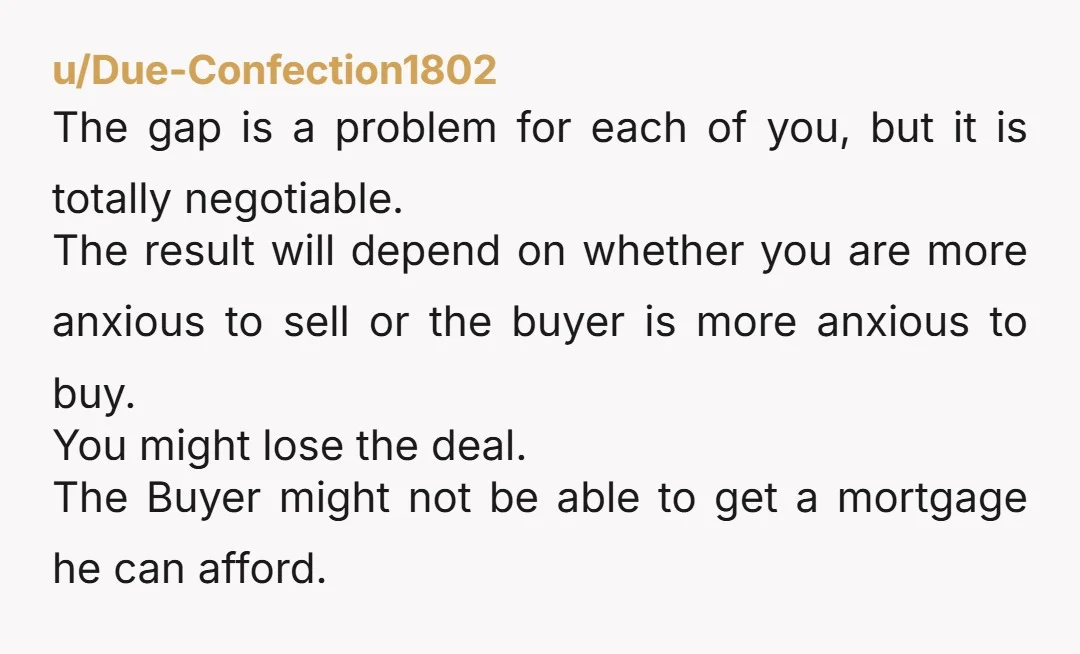

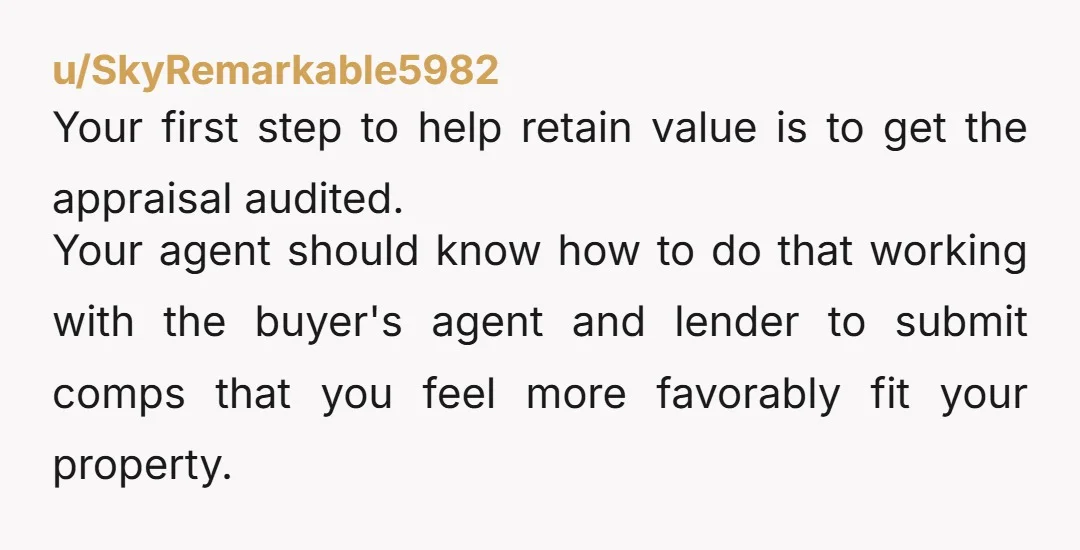

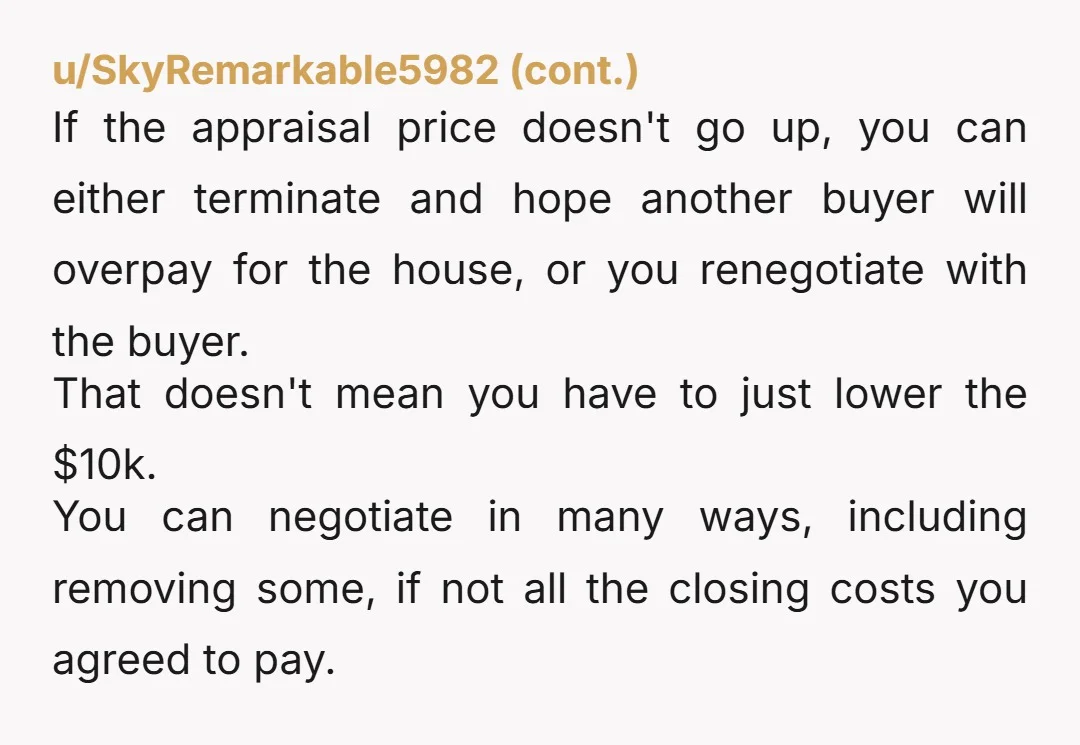

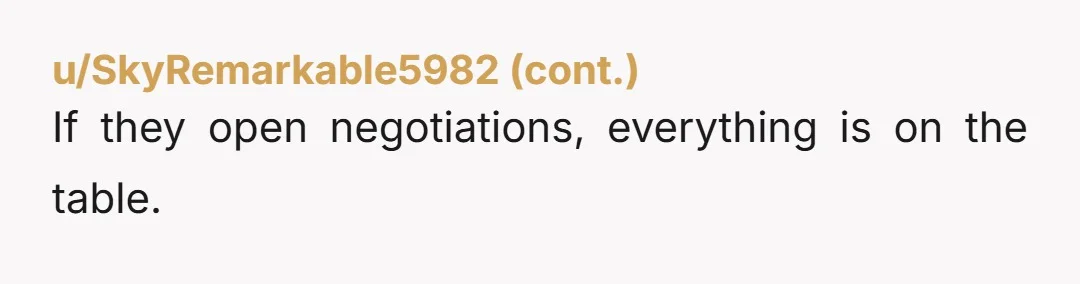

Most commenters sided firmly with financial reality, urging the seller to recognize that an overpriced house requires a price drop.

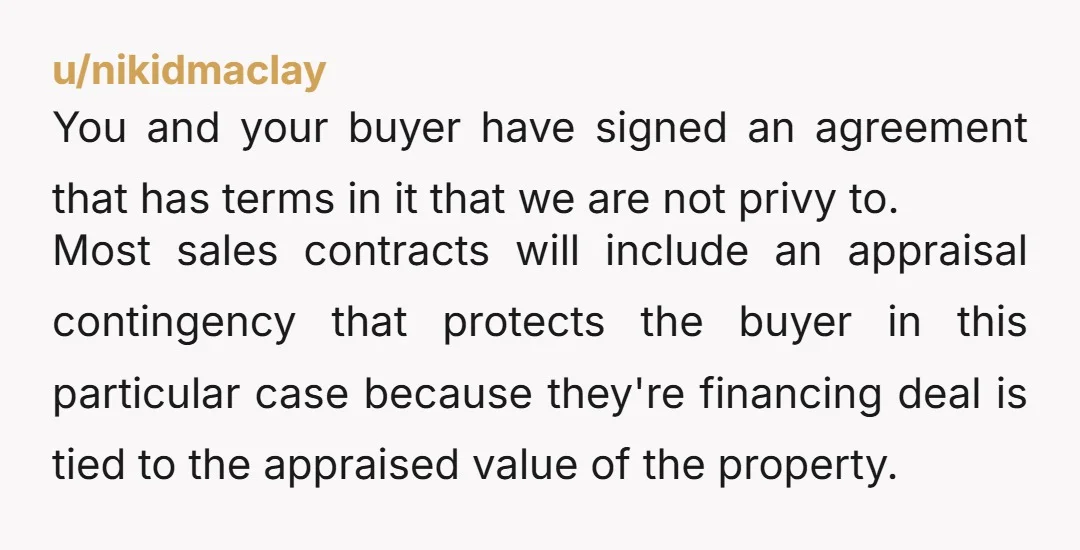

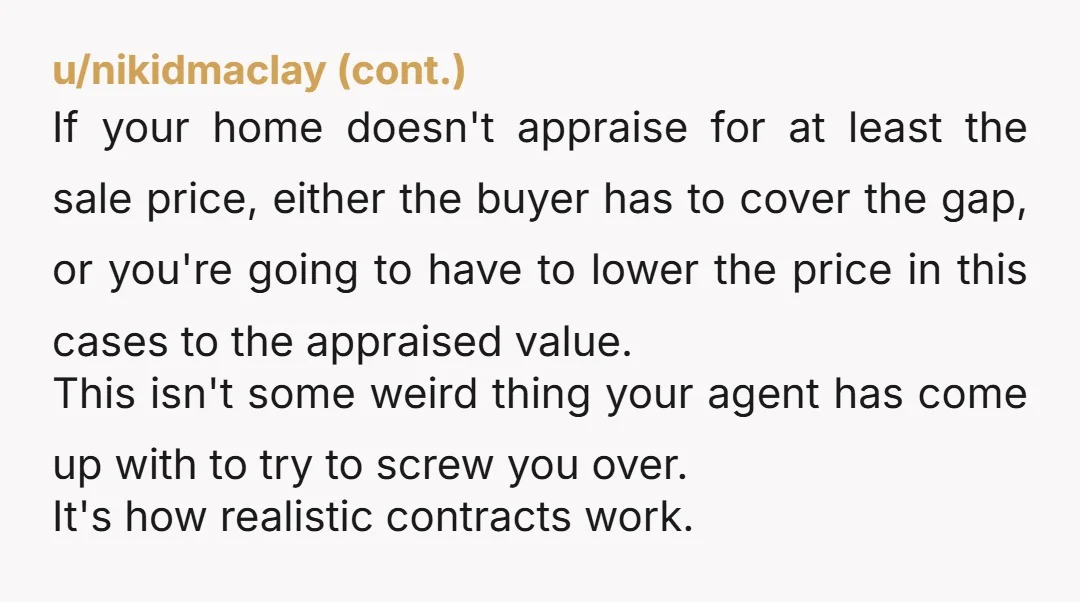

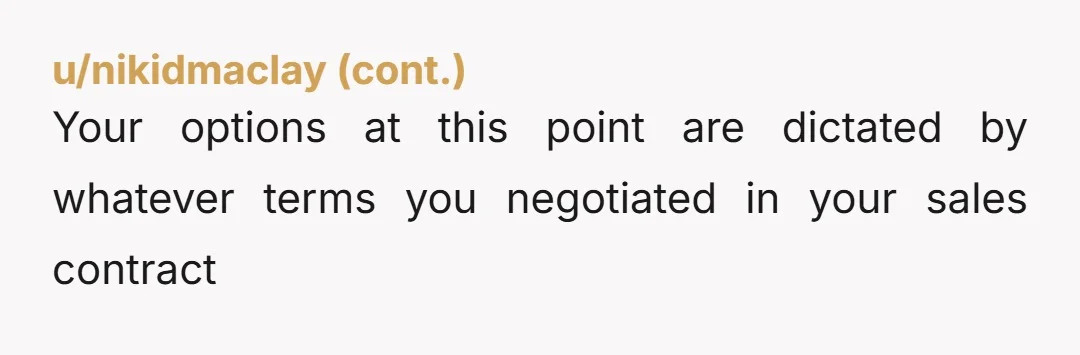

A few veteran agents reminded everyone that appealing the appraisal or restructuring the seller credits were still viable options.

Navigating a real estate transaction is rarely a straight line, especially when banks and appraisals get involved. The gap between perceived value and market reality often forces tough financial decisions at the closing table. Do you think the seller should lower the price, or should the buyer be responsible for covering the gap out of pocket? And how would you handle the situation if your own home appraisal came in surprisingly low? Drop your thoughts in the comments below!