AITAH for asking my stay at home wife to use some of my money for myself?

He grinds 48-62 hours welding steel, clocks weekends with the Air Force Reserves, and flips custom furniture on the side—all while funneling every paycheck into a family account his stay-at-home wife runs like a fortress. She handles bills, taxes, mortgages, everything. He just brings home the cash.

The one crack in the system? His $100 weekly plasma money, earned by literally bleeding twice a week. He’s been stashing it for a tattoo he’s wanted forever. When she asks to cash it out for “family needs,” he pushes back—and suddenly he’s the villain for daring to spend his own blood money on himself.

‘AITAH for asking my stay at home wife to use some of my money for myself?’

He’s the sole earner—steel mill welder, part-time reservist, and side-hustle carpenter—pouring every cent into the family pot:

He loves providing, adores his wife, and rarely asks for anything over $10 without running it by her first:

During a steelworkers’ strike, he picked up extra gigs—including plasma donation at $50 a pop, twice weekly—to stay afloat:

She flipped, insisting the money was needed elsewhere and accusing him of choosing “trivial” ink over family:

He feels he asks for little and just wants this one personal win from literal blood money:

In an edit, he thanks the community and vows to sit down for a full financial review:

Handing one partner total financial control works only when both stay fully informed—this setup leaves him blind and brewing resentment. Certified financial planner Ramit Sethi warns that “ignorance of your own money is a recipe for disaster, even in happy marriages.”

The plasma cash sits in a gray zone: it’s extra income he physically earns through bodily sacrifice. Treating it as communal without discussion ignores the effort behind it and erodes his sense of agency.

A healthy fix starts with a joint budget meeting—spreadsheets, logins, recurring bills laid bare. From there, carve out guilt-free “fun money” for each adult, no questions asked. Even $50 monthly per person prevents these flare-ups.

Transparency isn’t accusation; it’s insurance. If numbers check out, great—tattoo funded. If not, they tackle the real problem together instead of letting mystery money poison trust.

Here’s the feedback from the Reddit community:

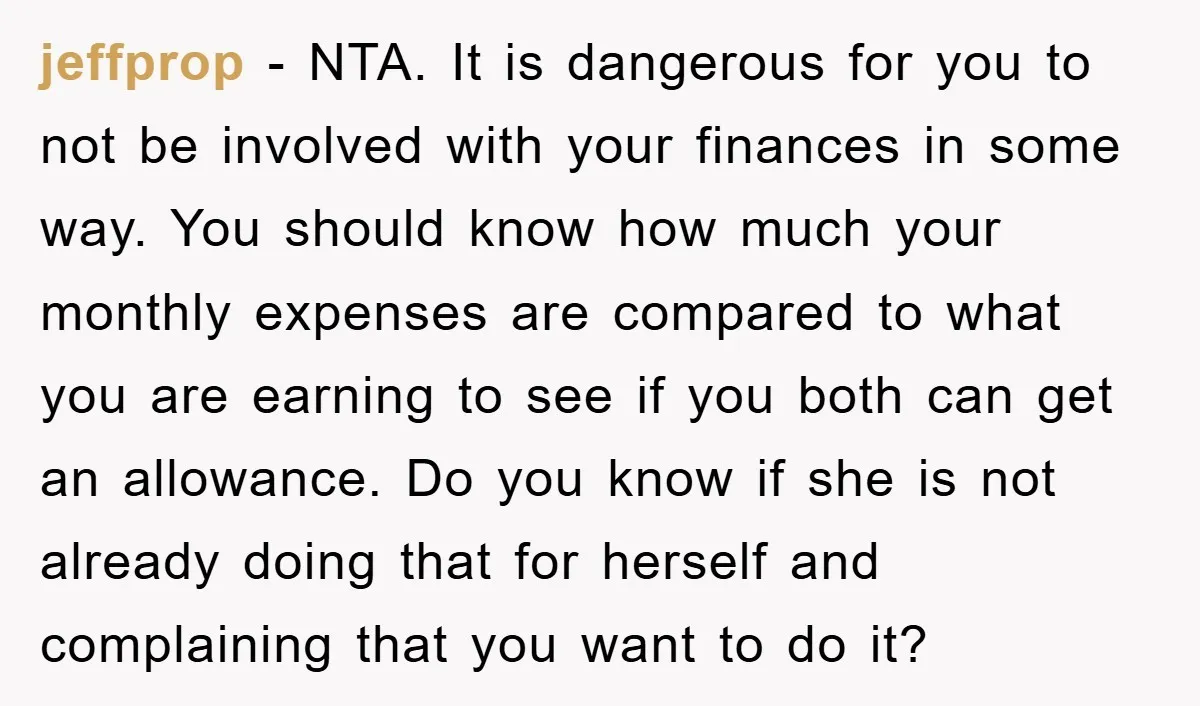

Most demanded a full financial sit-down to end the blackout:

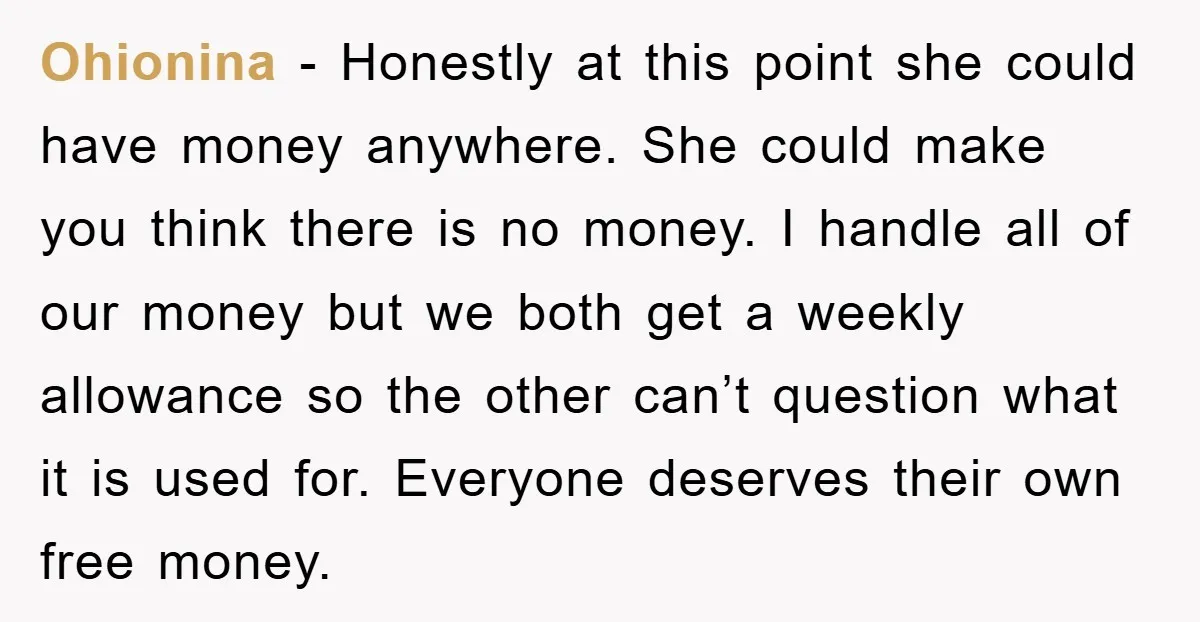

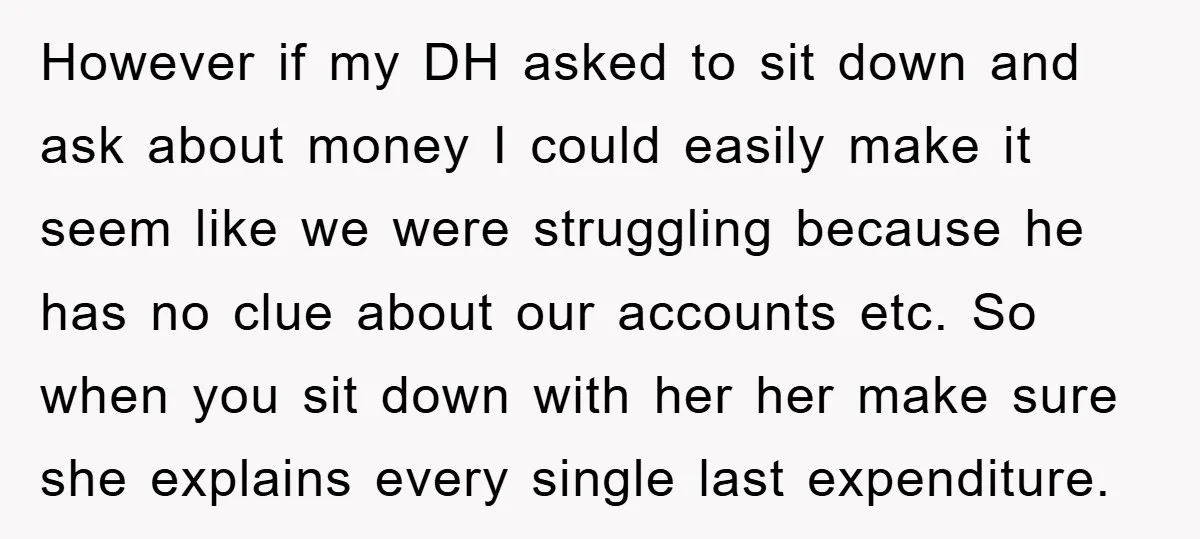

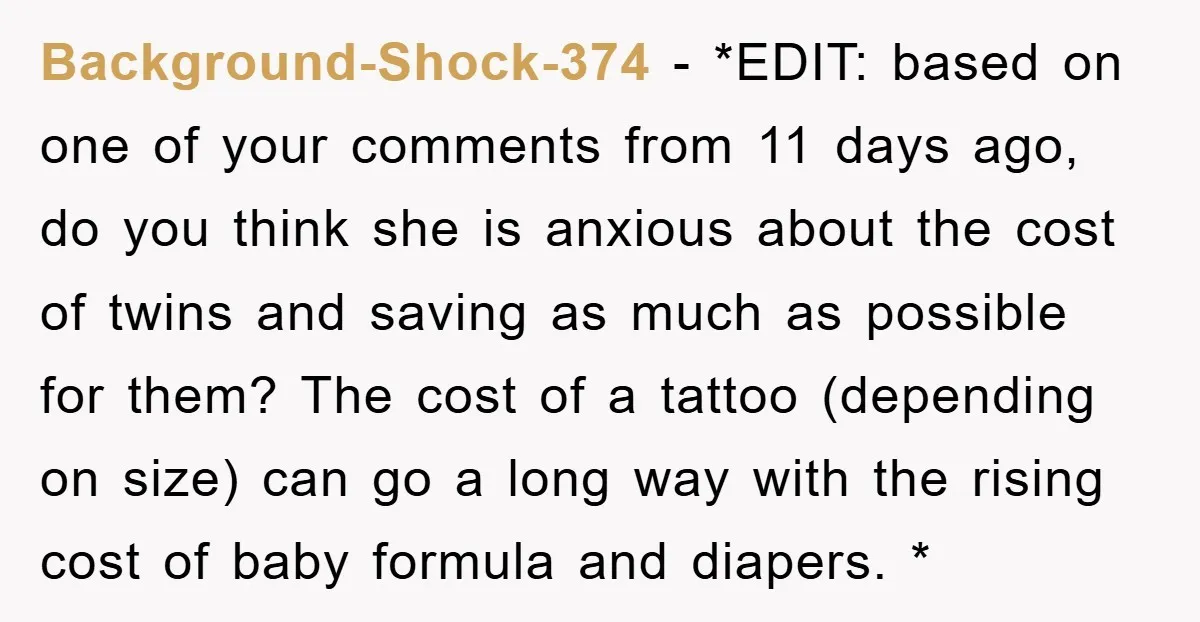

Some sniffed potential hidden spending or secret savings:

A few flipped the script—if extra cash matters, she could donate plasma too:

One wife chimed in from the other side, pleading for shared visibility:

Others highlighted the absurdity of needing to bleed for basics:

He’s gearing up for that big sit-down, spreadsheets in hand, ready to trace every plasma dollar and uncover what’s really draining the account—tattoo dreams paused until the full picture emerges.

These money blind spots can turn even rock-solid marriages into resentment factories, but ripping off the bandage with total transparency might just ink that tattoo and rebuild trust stronger than ever. Sole providers like him deserve their slice without the guilt trip, and a simple “yours and mine” fun fund could end these fights for good. What about you—would you keep bleeding for that ink, or demand the login and budget breakdown first? Drop your take below!