AITA for not wanting to gift my husband’s mother money?

A wife is furious after her husband suggested using $150,000 from her premarital savings to buy his mother a house—and commit to paying half the mortgage since his mom can’t afford it alone. She already agreed to let her mother-in-law live with them indefinitely, even though it wasn’t part of her marriage expectations. The money is her premarital inheritance, saved for their own house deposit, which feels increasingly out of reach with rising prices.

Her husband insists it’s just a “discussion,” but she’s incredulous and angry that he even raised it. Now she’s questioning: Is she wrong for refusing? For being so upset? For calling it “my money” after less than five years of marriage? The community is overwhelmingly on her side, with many urging her to protect her assets and reconsider the relationship.

‘AITA for not wanting to gift my husband’s mother money?’

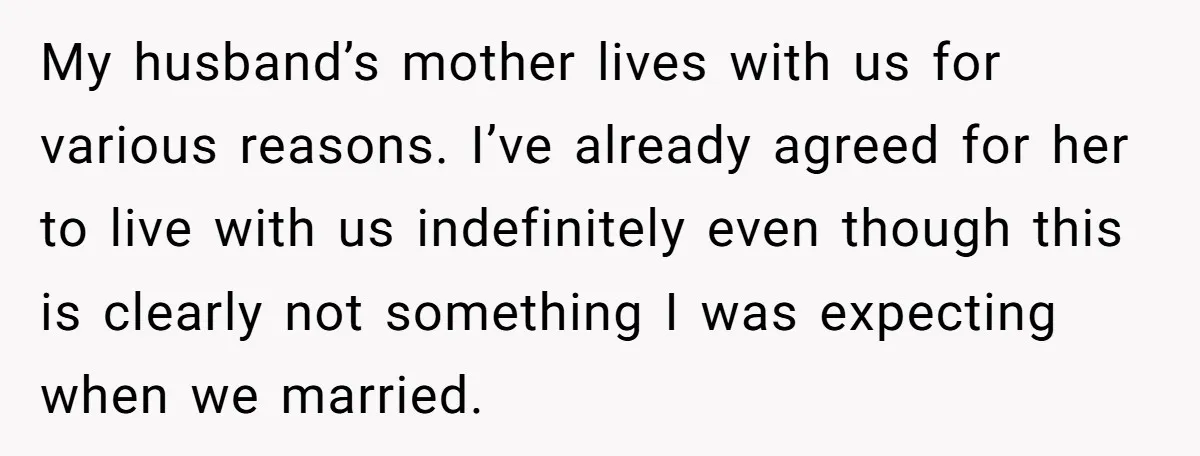

The mother-in-law already lives with the couple:

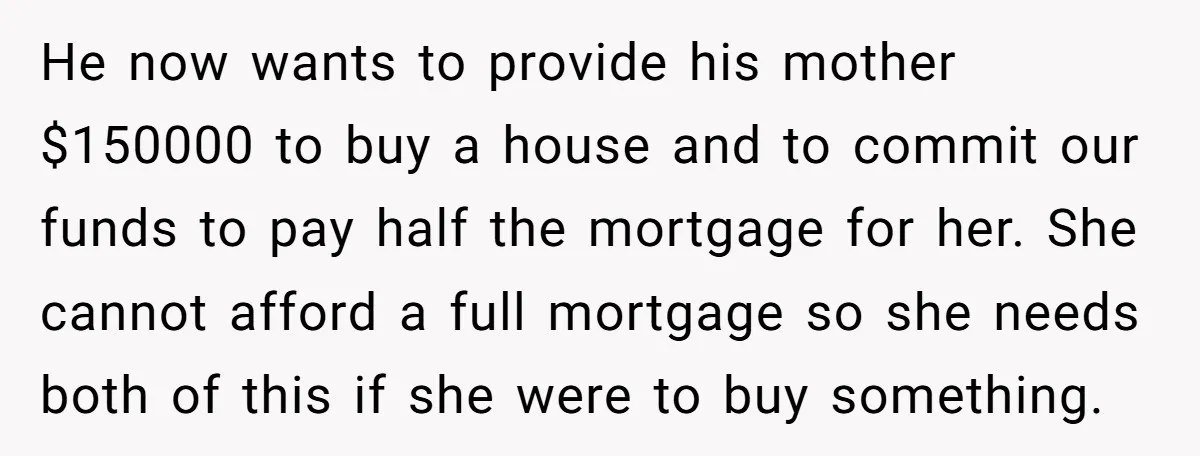

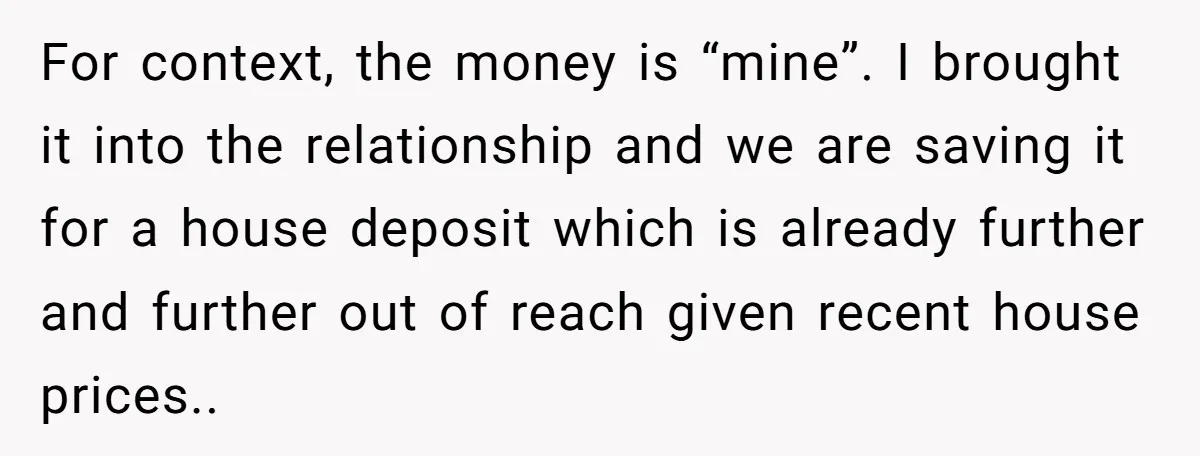

The husband proposed using her premarital savings:

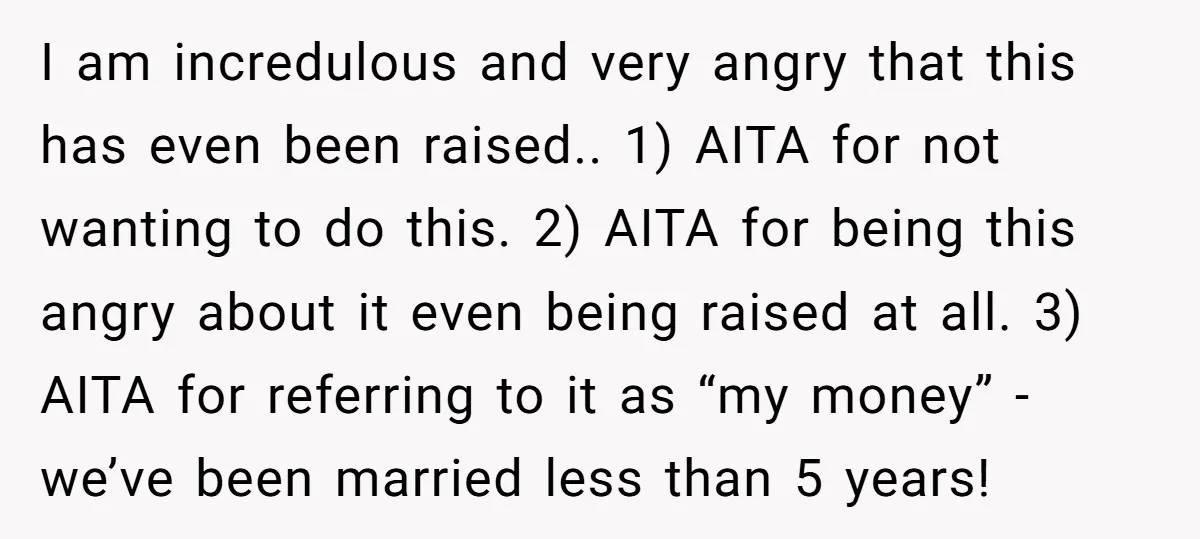

She was shocked and angry:

This situation reveals a major red flag in the marriage: a husband attempting to redirect significant premarital assets to benefit his family, disregarding his wife’s goals and financial security. The money is clearly premarital (inheritance/savings brought into the relationship), and using it for his mother’s house would deplete the couple’s own home deposit—potentially leaving them renting forever while his mom owns property. This isn’t just about generosity; it’s about priorities and fairness.

Allowing the mother-in-law to live rent-free is already a huge compromise. Suggesting she use her savings for a separate house for MIL—while paying half the mortgage—creates an unequal burden: the wife funds her MIL’s homeownership while delaying her own. If they divorce, the husband could benefit from the asset; if MIL passes, he inherits. This imbalance can breed resentment and erode trust.

Financial therapist Bari Tessler advises: “Premarital assets should remain separate unless both partners fully agree on commingling. When one spouse pushes to redirect significant funds to their family, it often signals deeper issues around loyalty, entitlement, and financial boundaries. The non-consenting partner must protect their security—especially when the request feels one-sided.”

Practical advice: Immediately move the money to a separate account in her name only. Consult a lawyer about protecting premarital assets in your jurisdiction (many places exclude inheritance if not commingled). Have a calm but firm conversation: “This money is for our future home—I’m not open to using it for your mother’s house.” If he pushes or dismisses her anger, couples counseling is essential to address underlying dynamics. If he refuses to respect her boundaries, divorce may be worth considering before more assets are at risk. She’s not wrong for being angry; she’s protecting her future.

See what others had to share with OP:

The online community was overwhelmingly supportive of the wife, declaring her NTA across the board. Commenters urged her to protect her money immediately, consider divorce, and criticized the husband’s entitlement.

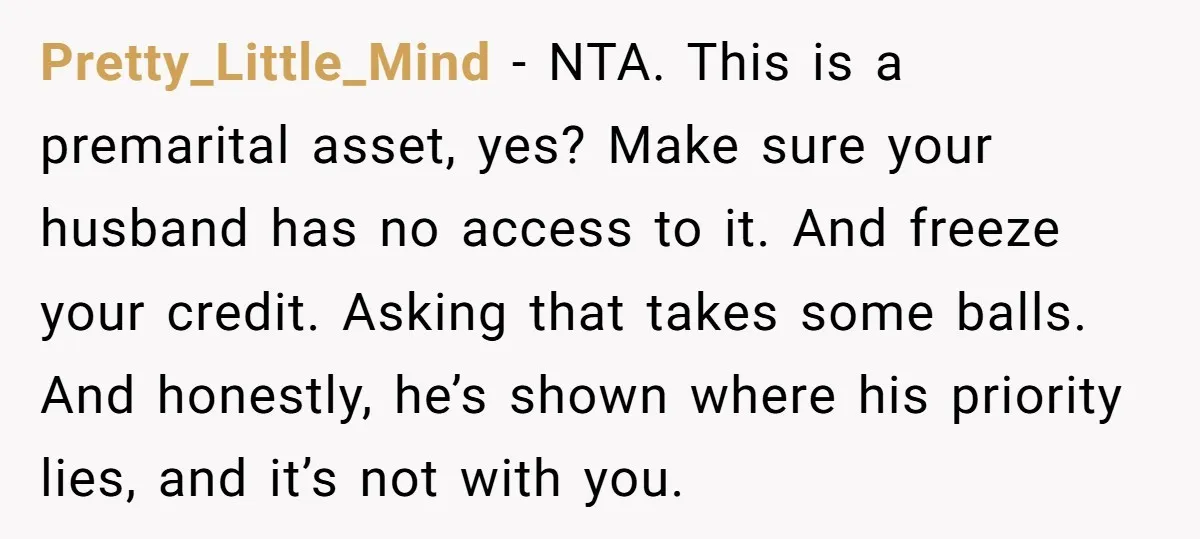

Most emphasized the unfairness and red flags in the husband’s suggestion:

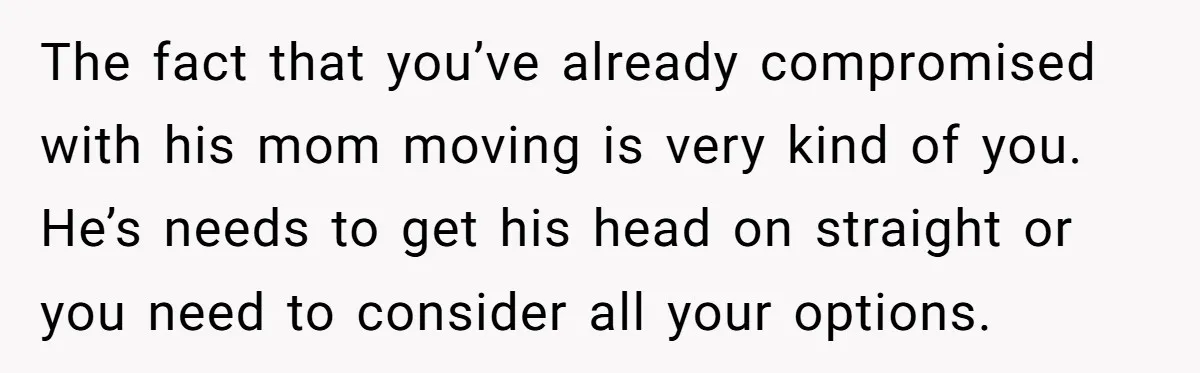

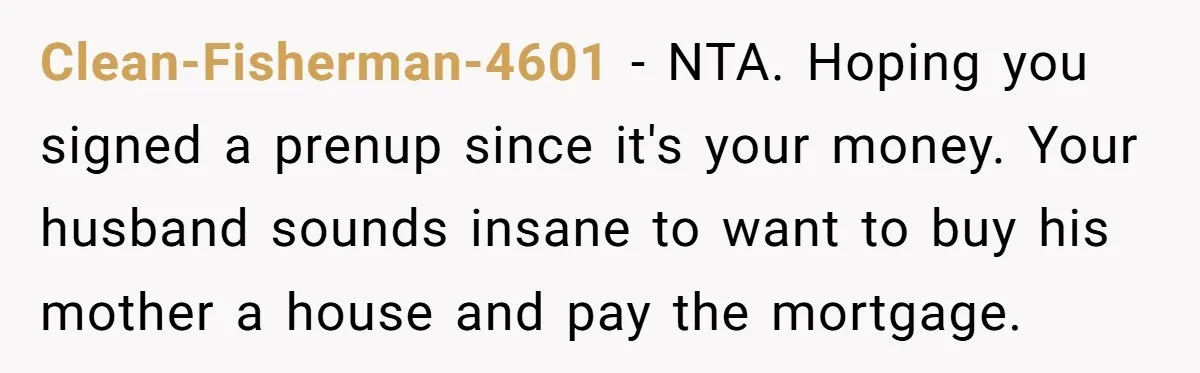

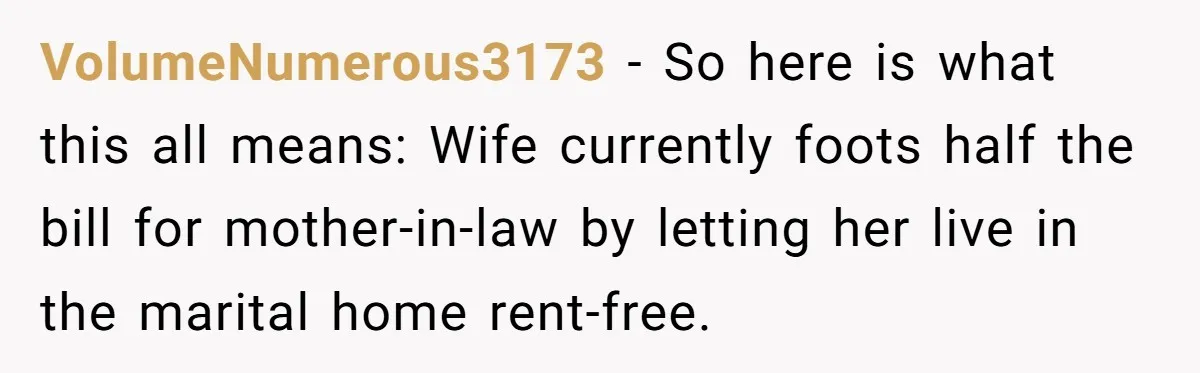

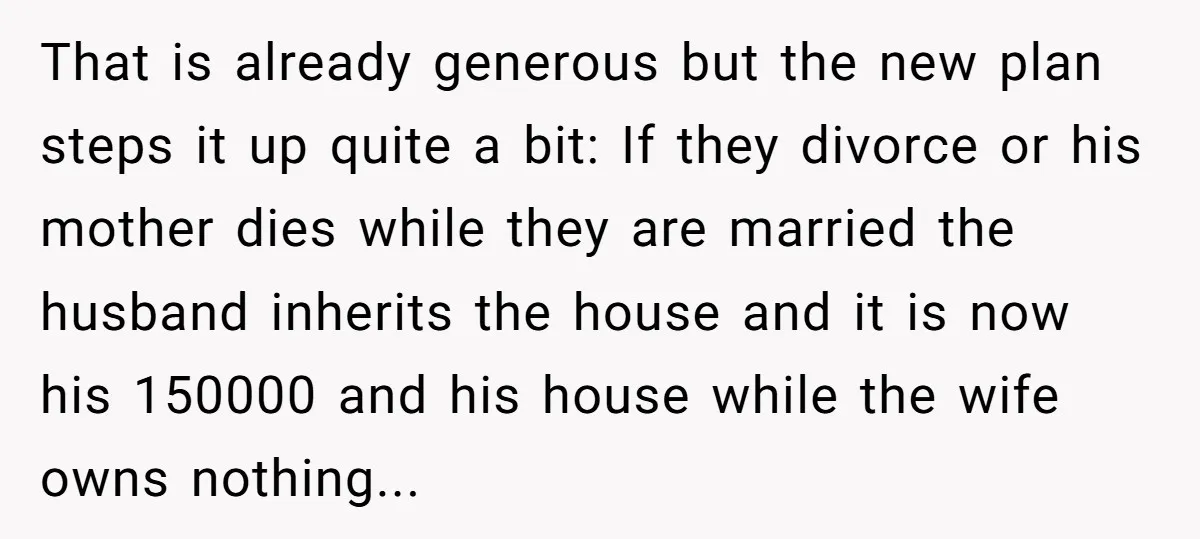

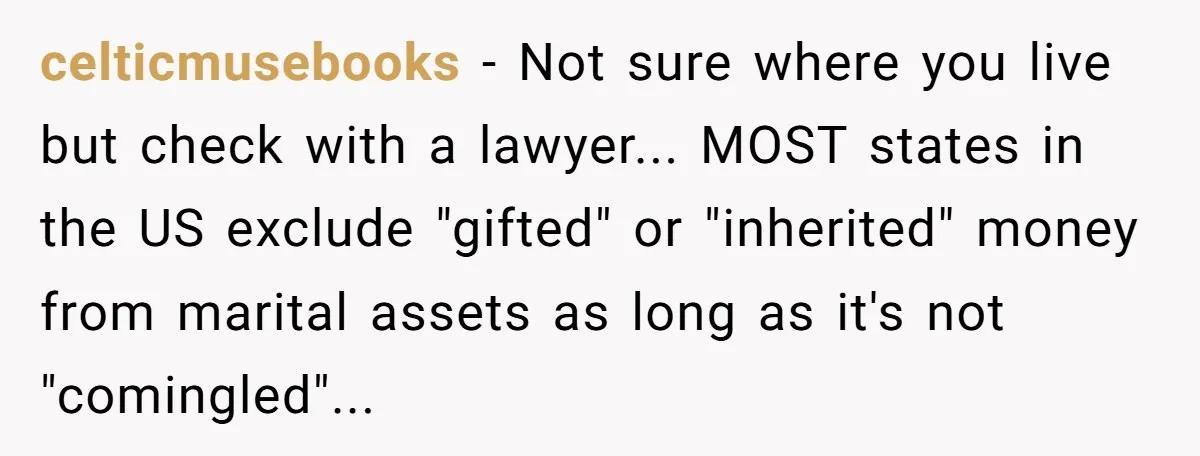

Many suggested ways to protect her money and highlighted the risks:

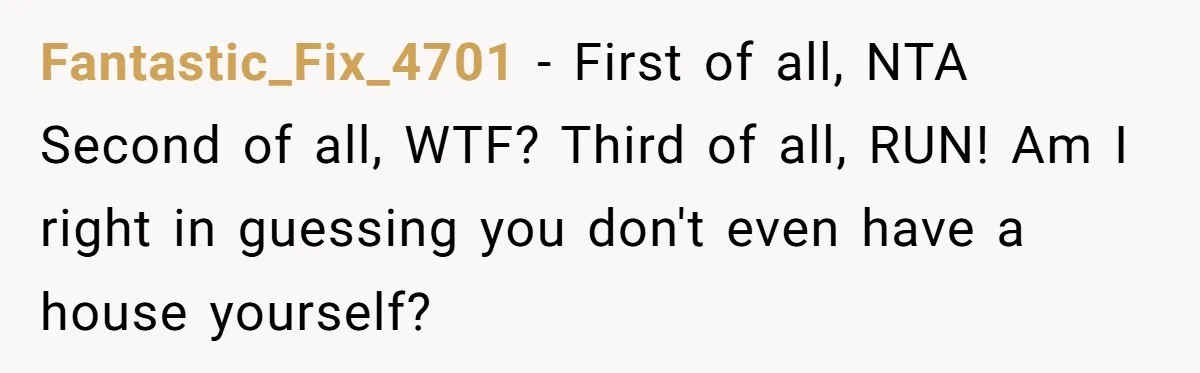

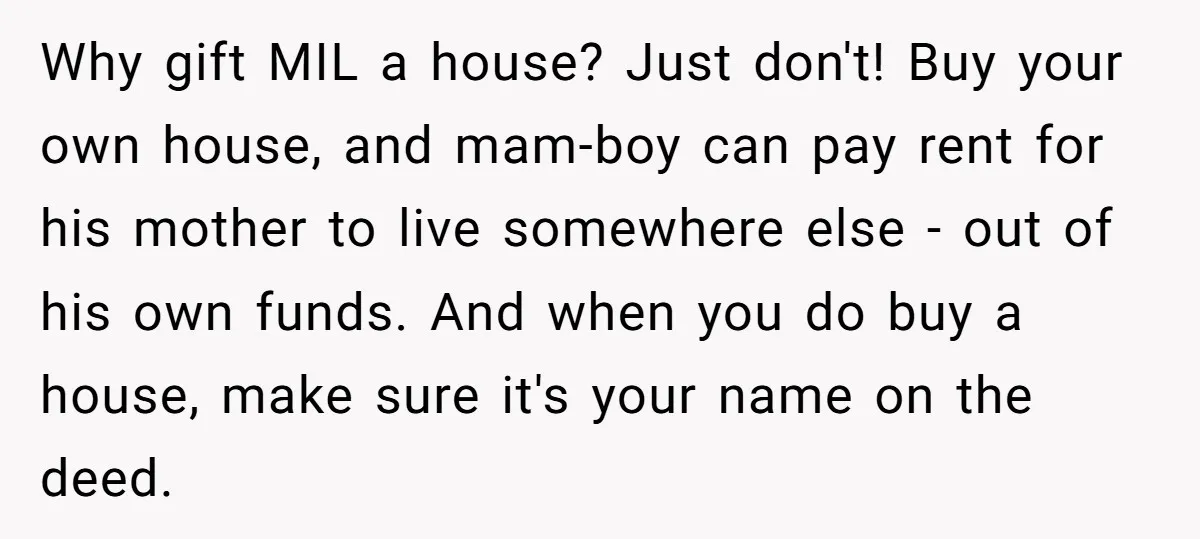

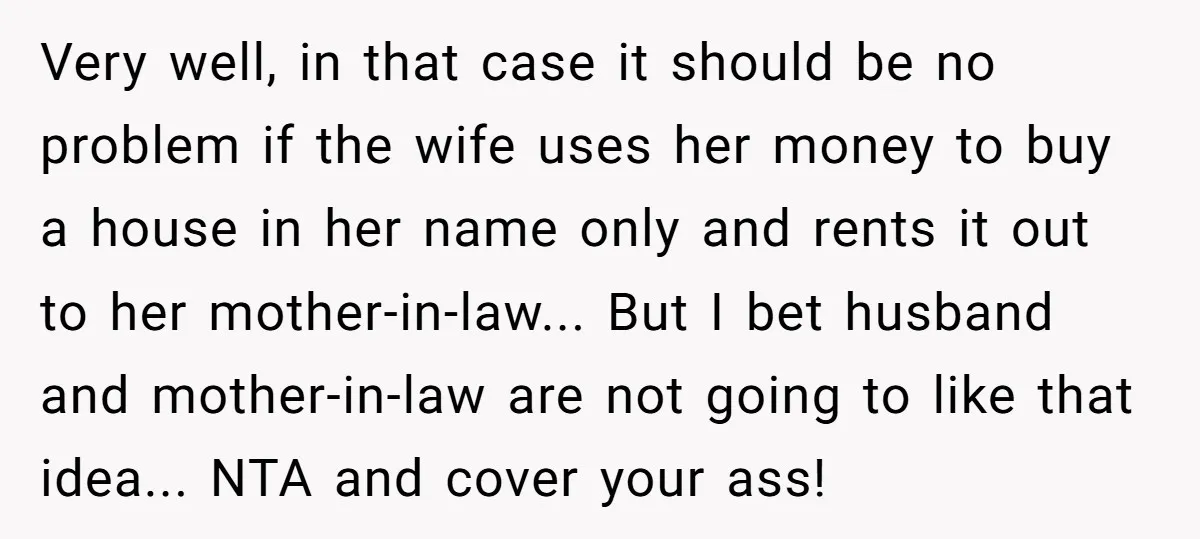

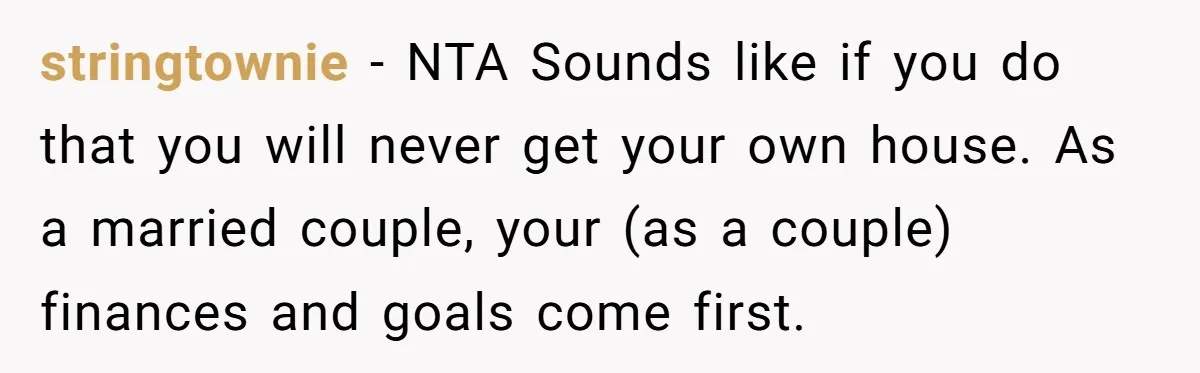

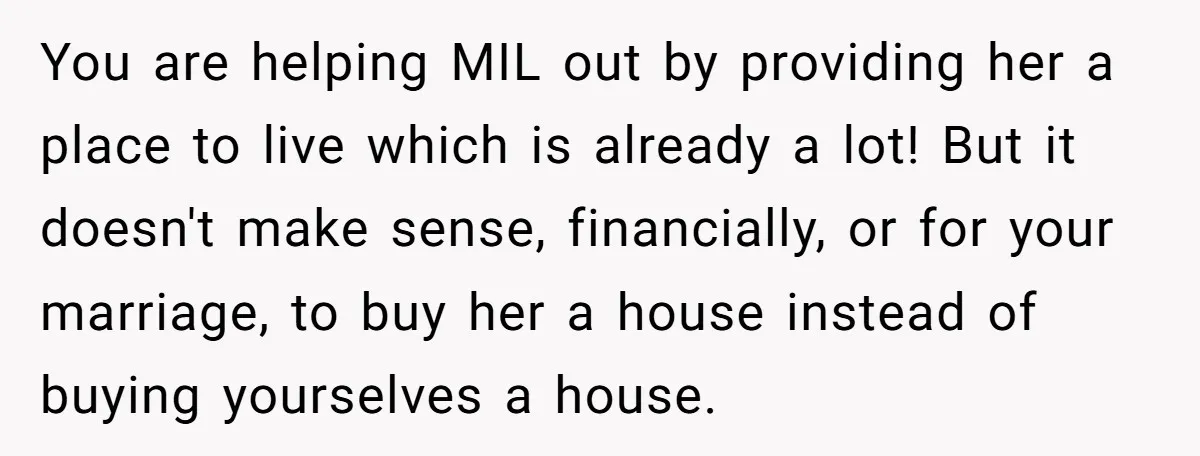

Commenters suggested other solutions and called out the husband’s priorities:

This story highlights a major tension in marriage: when one partner’s family expectations clash with shared financial goals. The wife has already made a huge compromise by letting her MIL live rent-free—asking her to fund a separate house for MIL is unreasonable and unfair.

What do you think? Should premarital money always be shared in marriage, or is it okay to keep it separate? Have you dealt with in-law financial pressure? Share your thoughts in the comments—we’d love to hear your experiences!