AITA for not putting my boyfriend’s name on the mortgage?

Buying a dream home turned tense when a 29-year-old woman’s boyfriend demanded his name on the mortgage. With her father’s generous help, she’s navigating a tough housing market to secure a house she loves. But her boyfriend, contributing nothing financially, refuses to pay rent unless his name is included, leaving her feeling controlled and confused.

Shared on social media, this story sparked heated debates, with many urging her to protect her finances. Is she wrong to keep her boyfriend off the mortgage? The community’s reactions shed light on the clash between personal goals and relationship dynamics. Let’s break it down.

‘AITA for not putting my boyfriend’s name on the mortgage?’

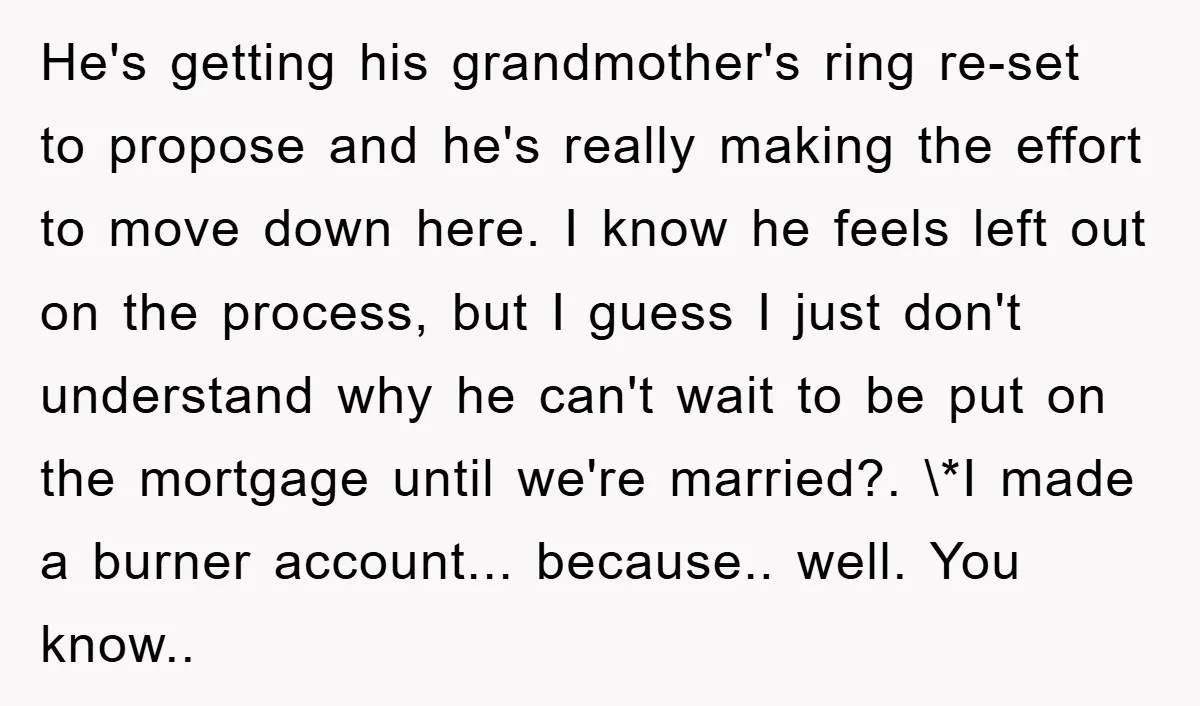

A move back home came with a bold plan.

A perfect home came with a catch.

Tensions rose with an unexpected demand.

She weighed his feelings but stood firm.

Buying a home is a massive financial step, and adding someone to a mortgage can have lasting consequences. This woman faced pressure from her boyfriend to include his name on the mortgage despite his lack of financial contribution. His refusal to pay rent unless included raises red flags about fairness and financial responsibility.

Financial expert Suze Orman advises, “Never mix finances with someone you’re not married to, as it can lead to legal risks if the relationship ends” (The Money Book for the Young, Fabulous & Broke). The boyfriend’s demand for ownership without contributing to the down payment is unreasonable. His stance on not paying rent further suggests he may be seeking benefits without accountability.

His concerns about the housing market and unfamiliar area are valid but don’t justify demanding ownership. Society often expects couples to share everything, but when one partner bears the financial risk, protecting personal assets is crucial. Her decision to keep him off the mortgage, especially before marriage, is prudent.

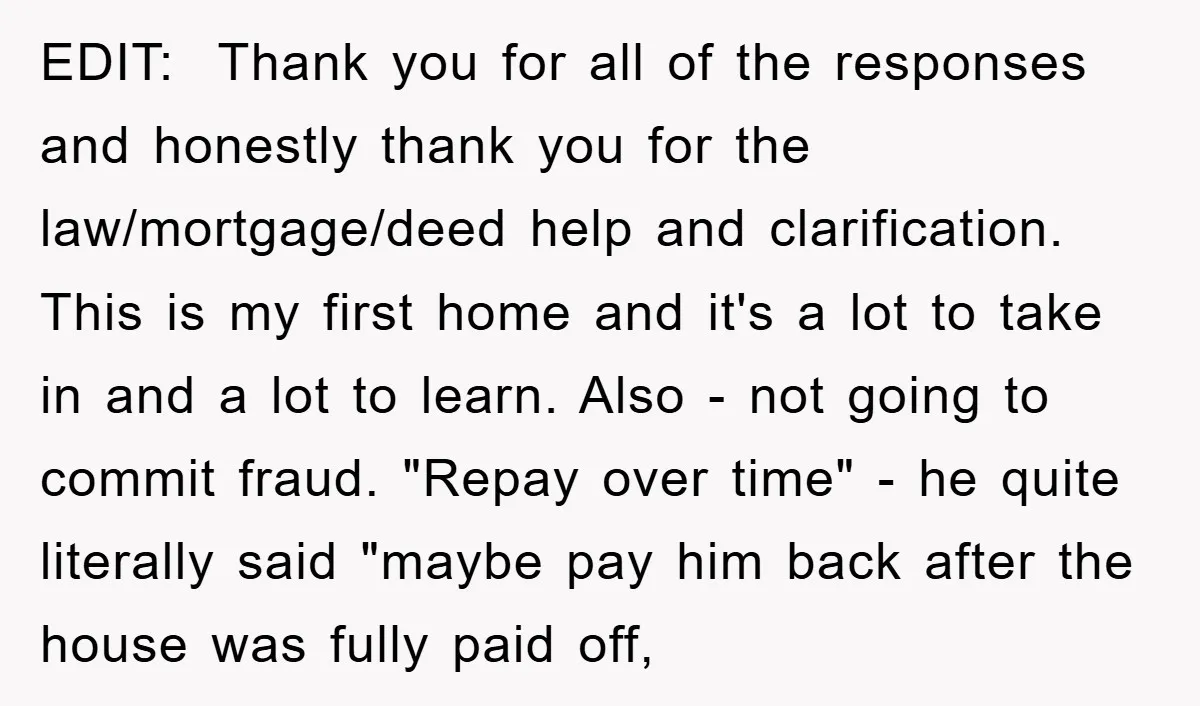

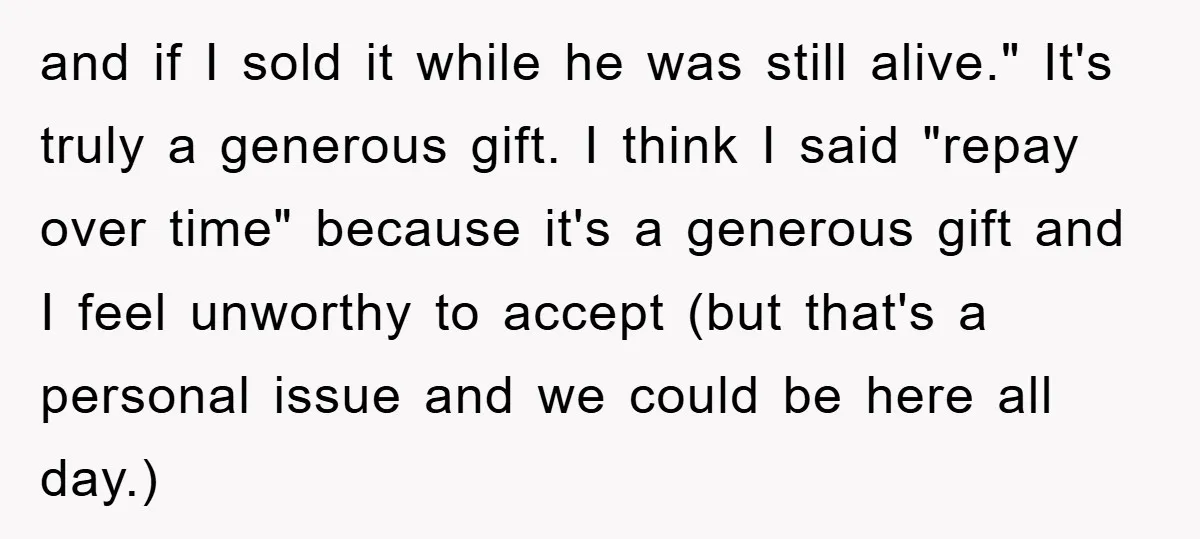

She should proceed with the purchase if she can afford it independently, discussing rent as a fair way for him to contribute to living costs. If he refuses, she should reassess the relationship’s balance. Consulting a lawyer about premarital property laws and documenting her father’s contribution legally can prevent future disputes. Open communication is key to aligning their goals.

Let’s dive into the reactions from Reddit:

The online community weighed in, largely supporting her decision and raising concerns about her boyfriend’s motives.

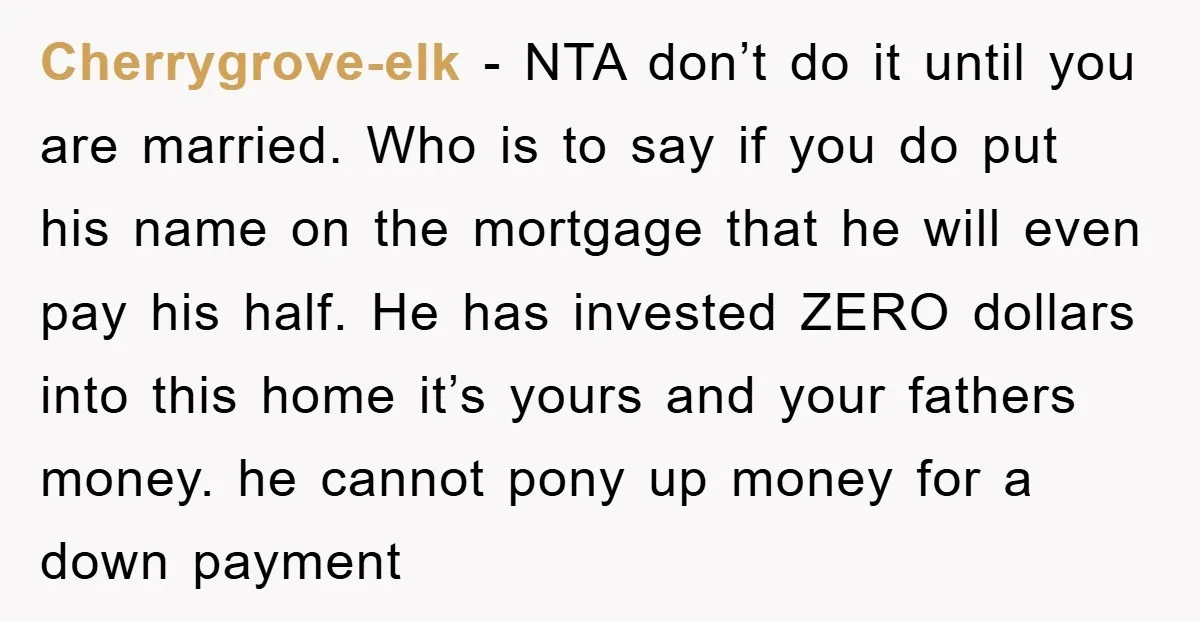

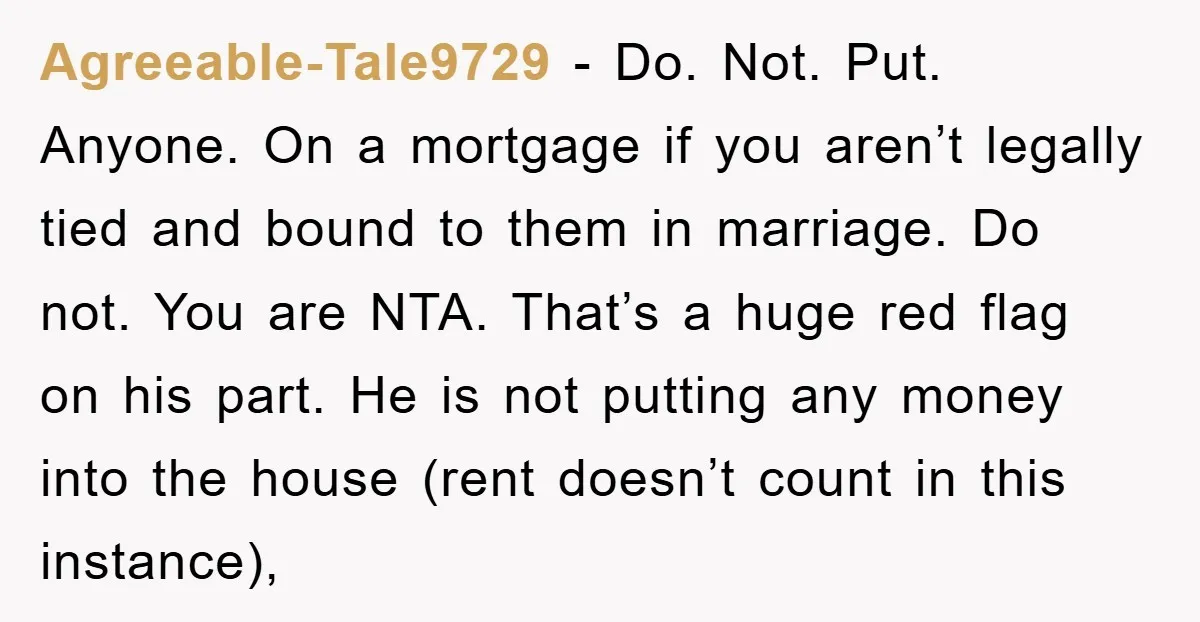

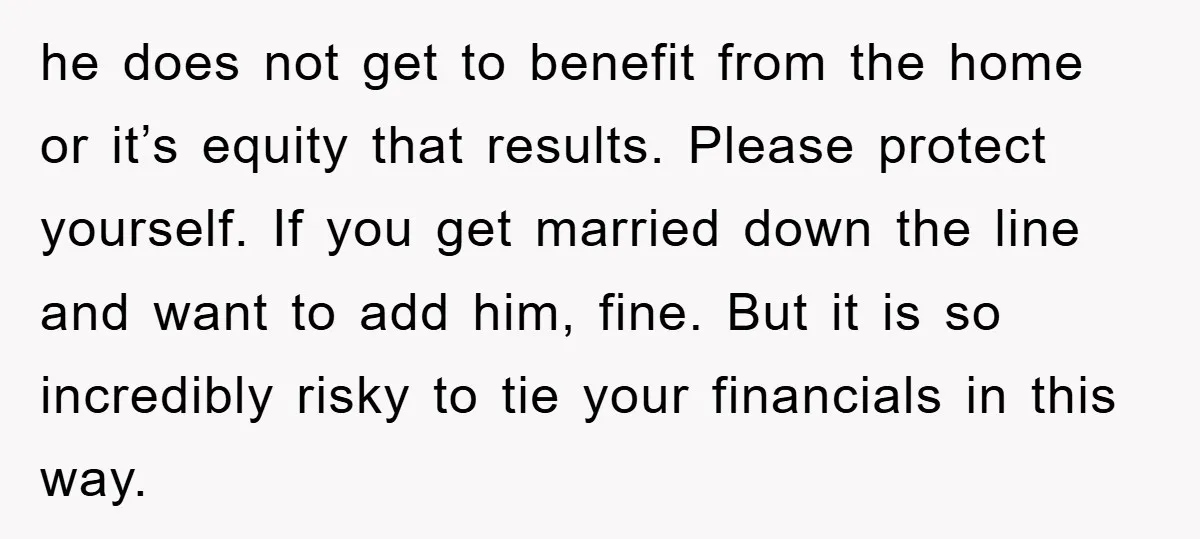

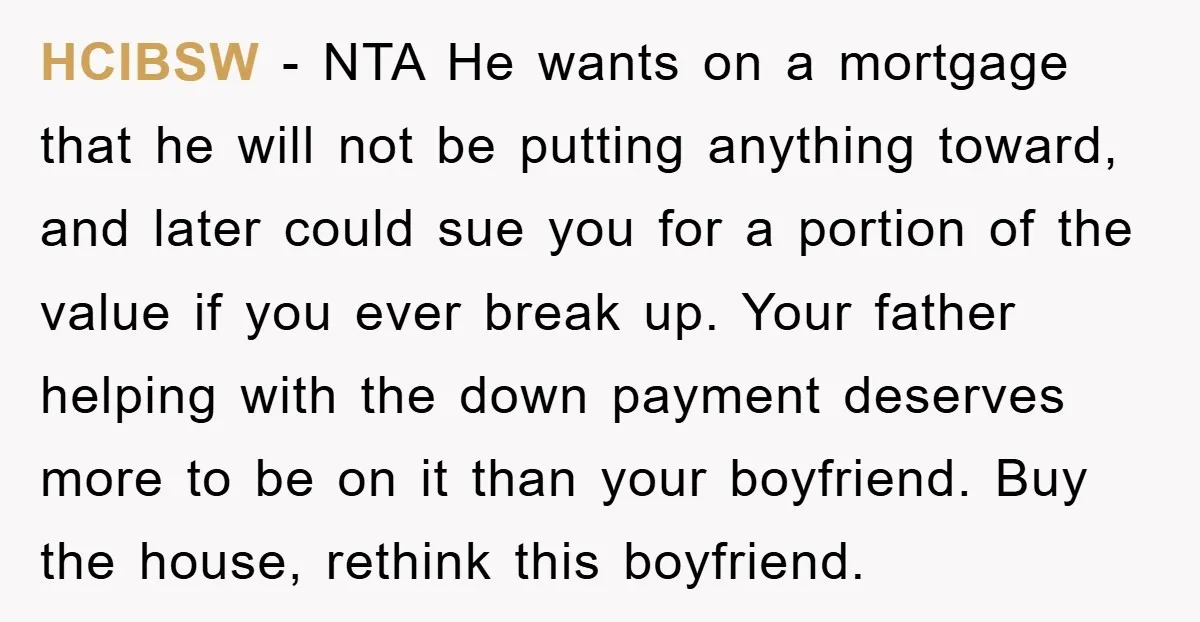

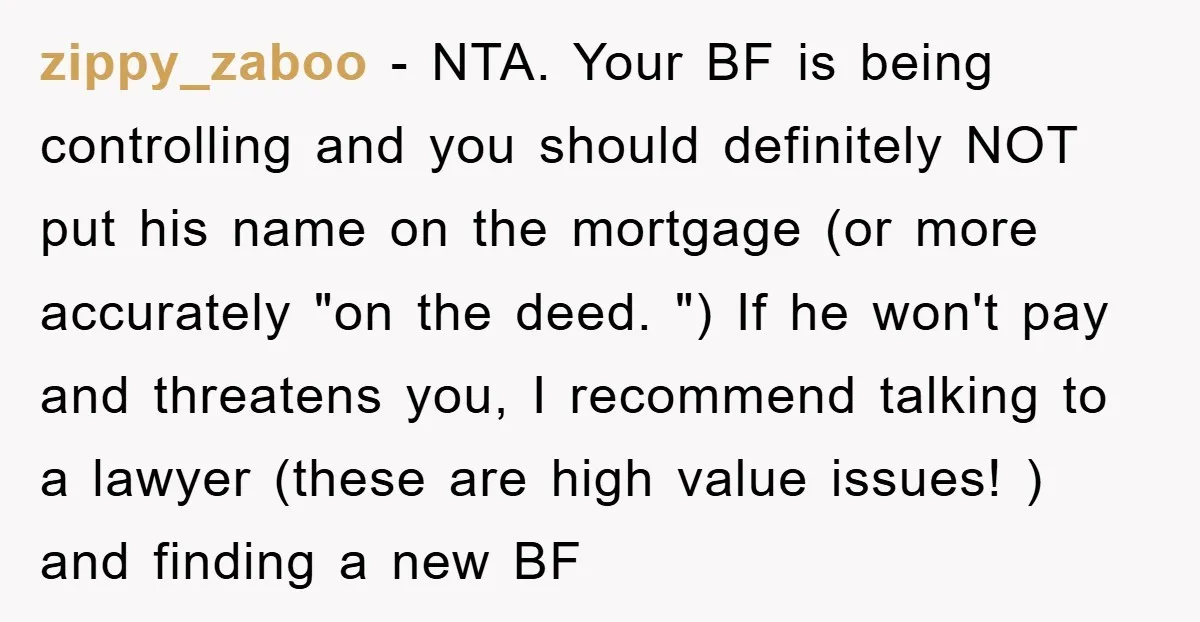

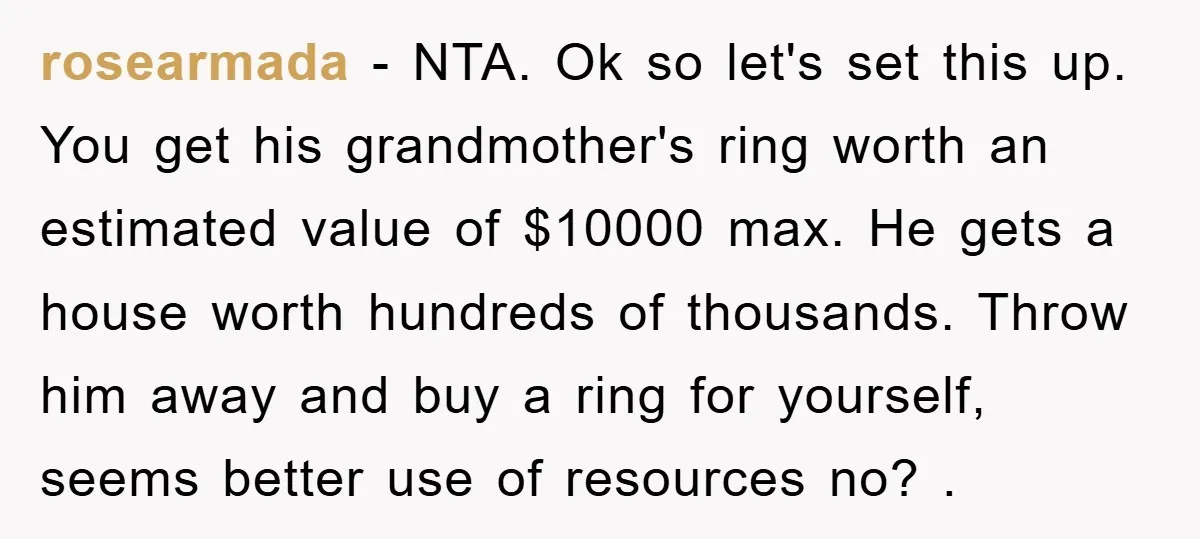

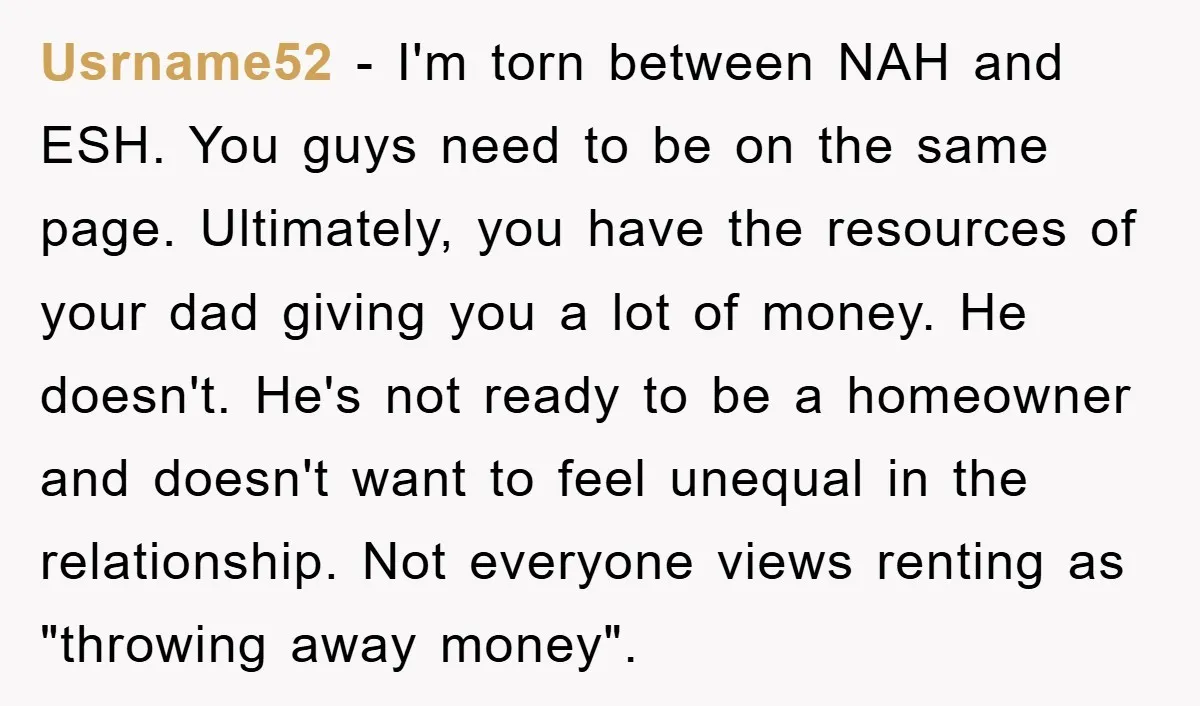

Many urged her to keep the mortgage in her name, stressing the risks of shared ownership.

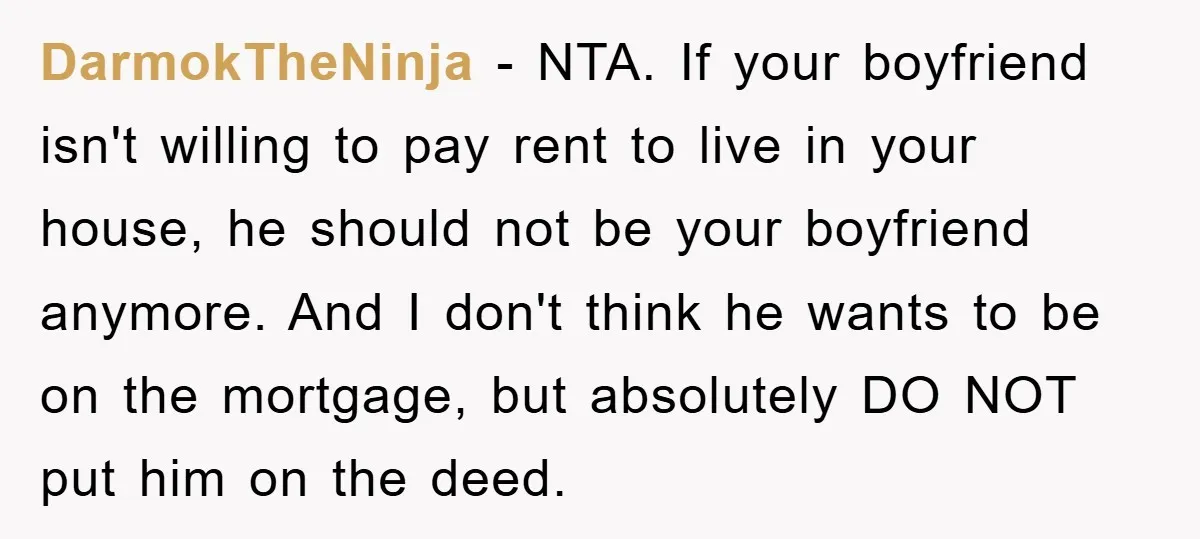

Some saw the boyfriend’s demands as manipulative or financially exploitative.

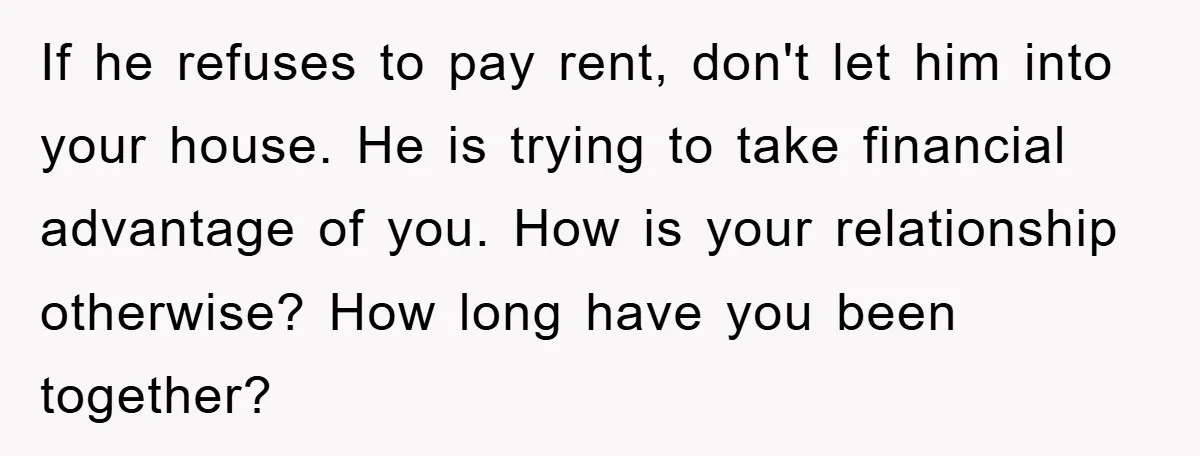

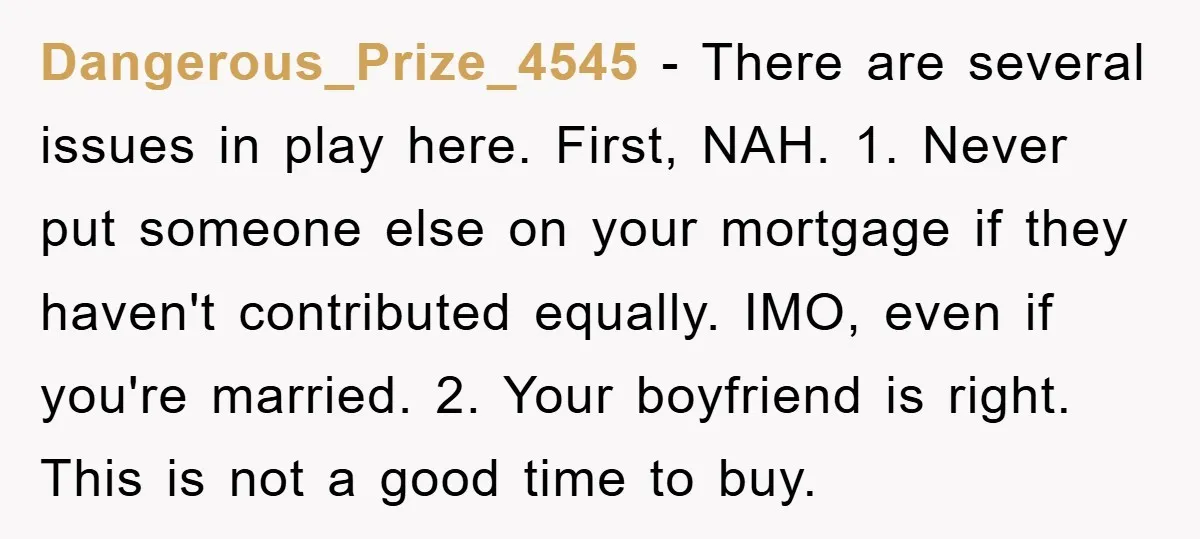

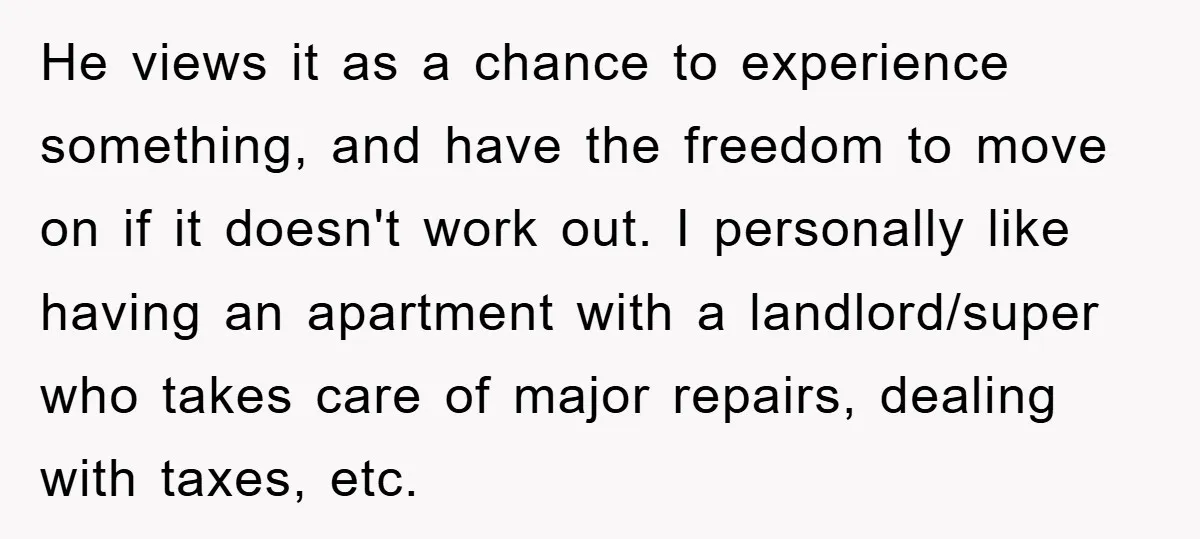

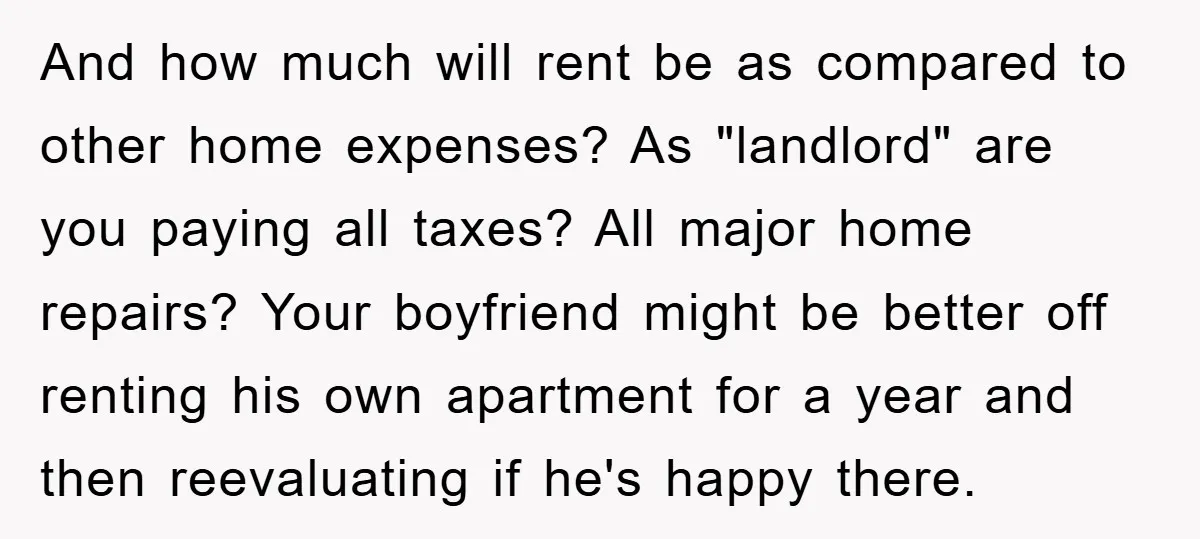

A few offered nuanced perspectives, urging dialogue and caution about timing.

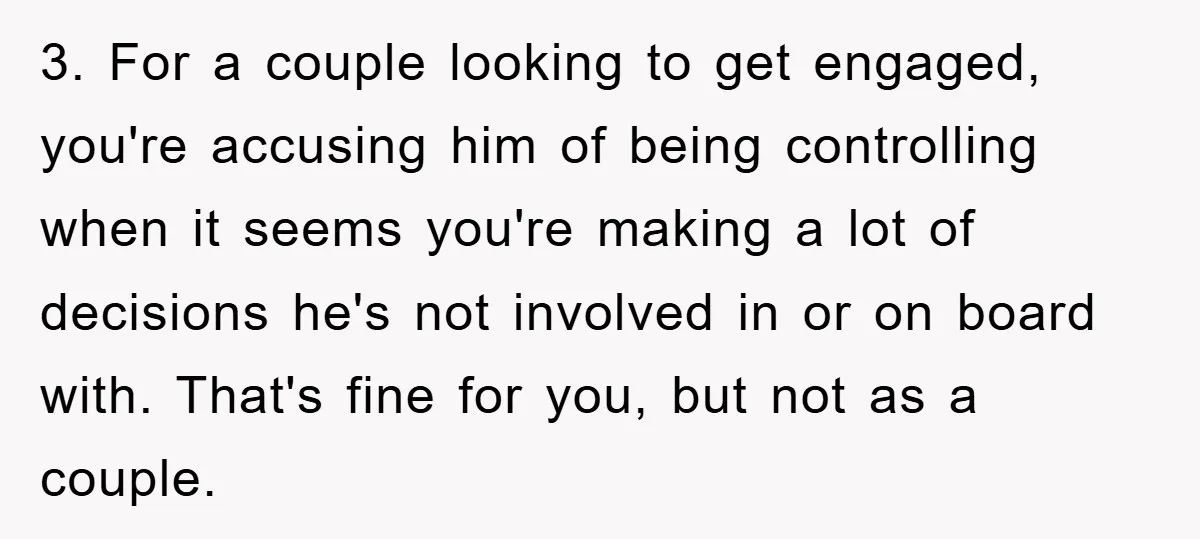

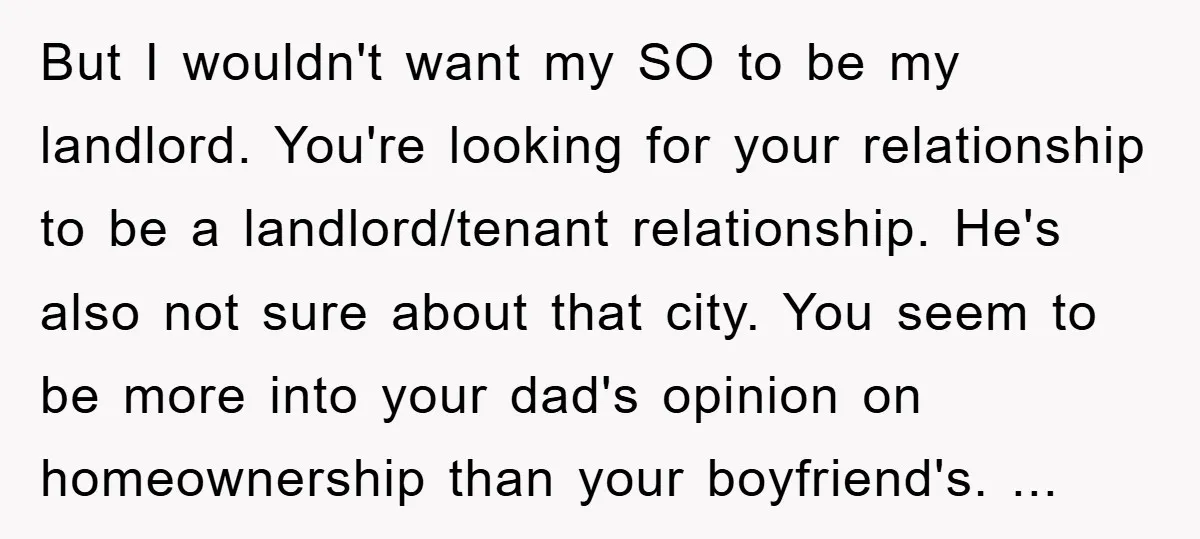

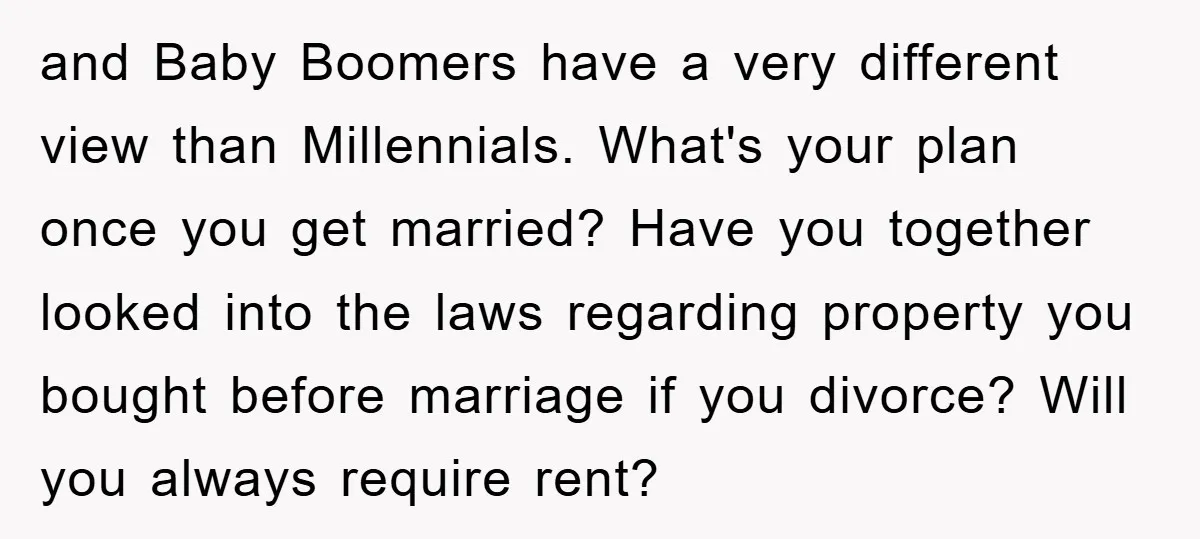

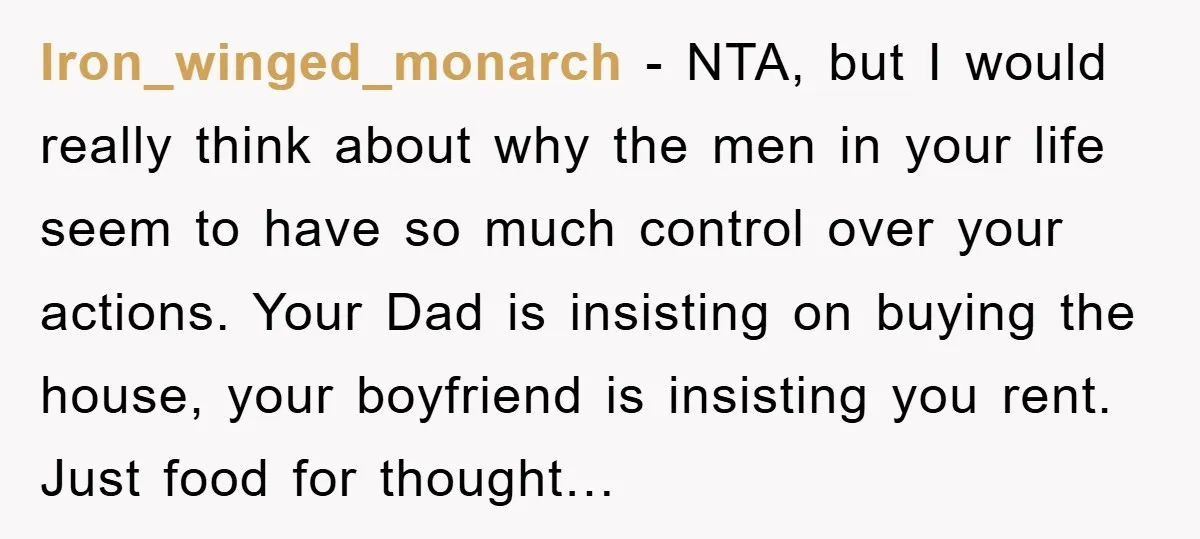

Some questioned the dynamics and external influences in the relationship.

This story boils down to balancing financial independence with relationship goals. The woman faces a tough choice: protect her assets or compromise for her boyfriend. The online community offered varied takes, from cheering her on to urging better communication.

What do you think? Is she right to keep the mortgage in her name, or does her boyfriend have a point? Have you ever faced a financial clash in a relationship? Share your story!