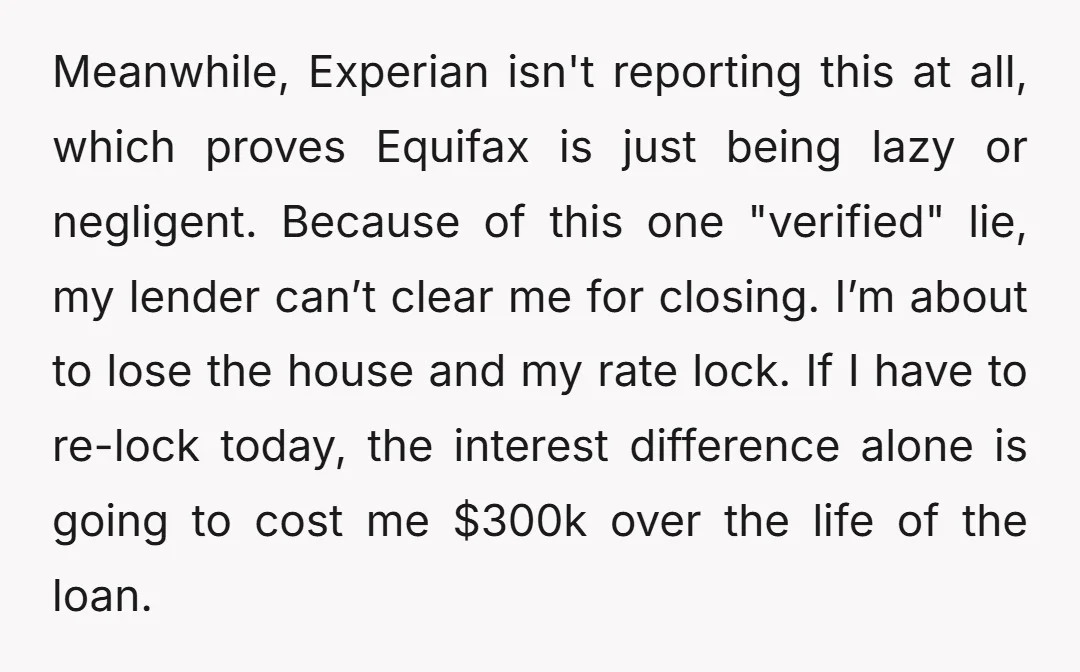

Veteran Is About to Lose His First Home Because Equifax Flagged a $0 Balance as “Delinquent”

We all know that moment when a mindless bureaucratic glitch threatens to derail our most carefully laid plans. For one 17-year Air Force veteran, the dream of closing on a first home turned into a waking nightmare thanks to a single line of bad data. He had locked in a fantastic interest rate and was ready to sign the papers when a bizarre credit reporting error brought everything to a screeching halt.

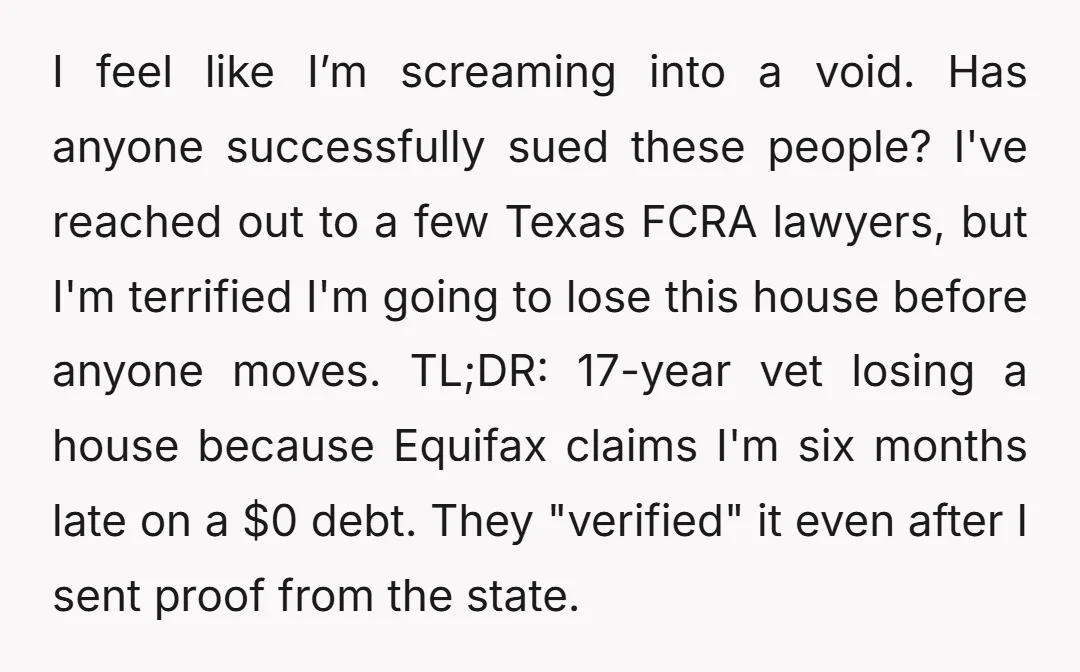

Despite having official documentation proving his innocence, the veteran found himself trapped in a loop of automated rejections that no human seemed willing to override. With hundreds of thousands of dollars in future interest on the line, the clock is ticking on his closing date. Curious how it all unfolded? The full story is right below.

The setup was picture-perfect: a veteran on the verge of securing his future, until an unexpected roadblock appeared.

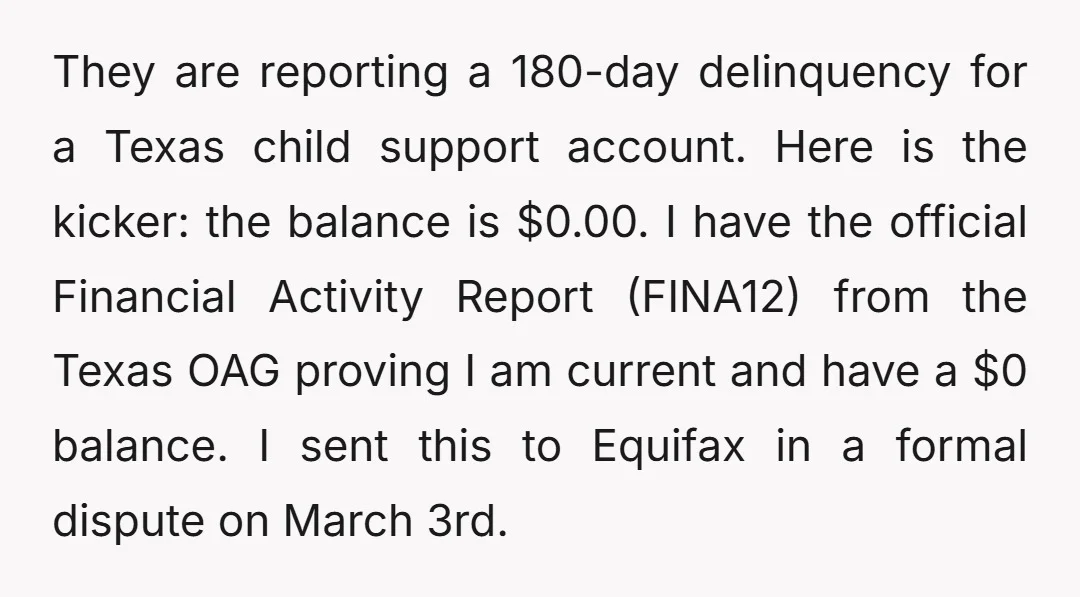

Despite having state-certified proof of a clean slate, the automated gears of the credit system refused to budge.

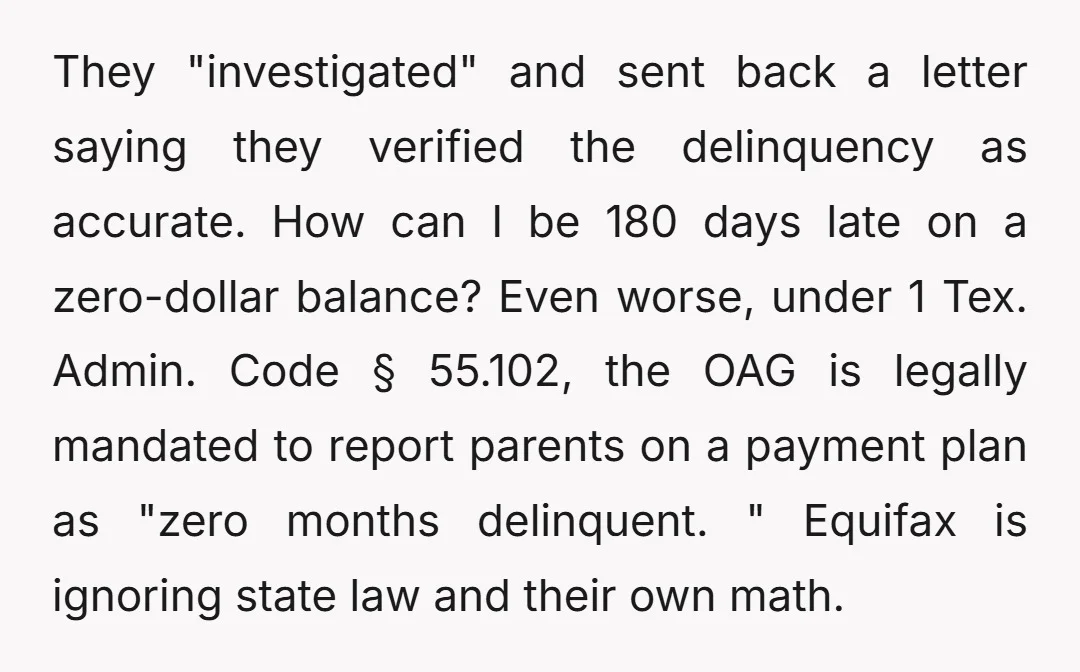

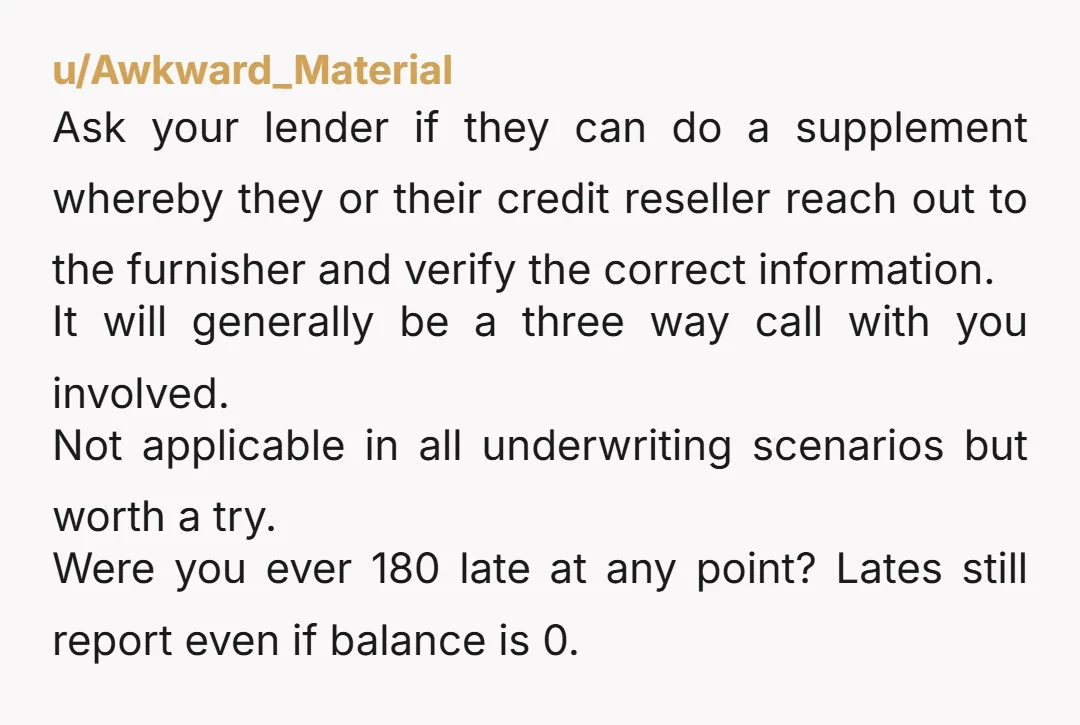

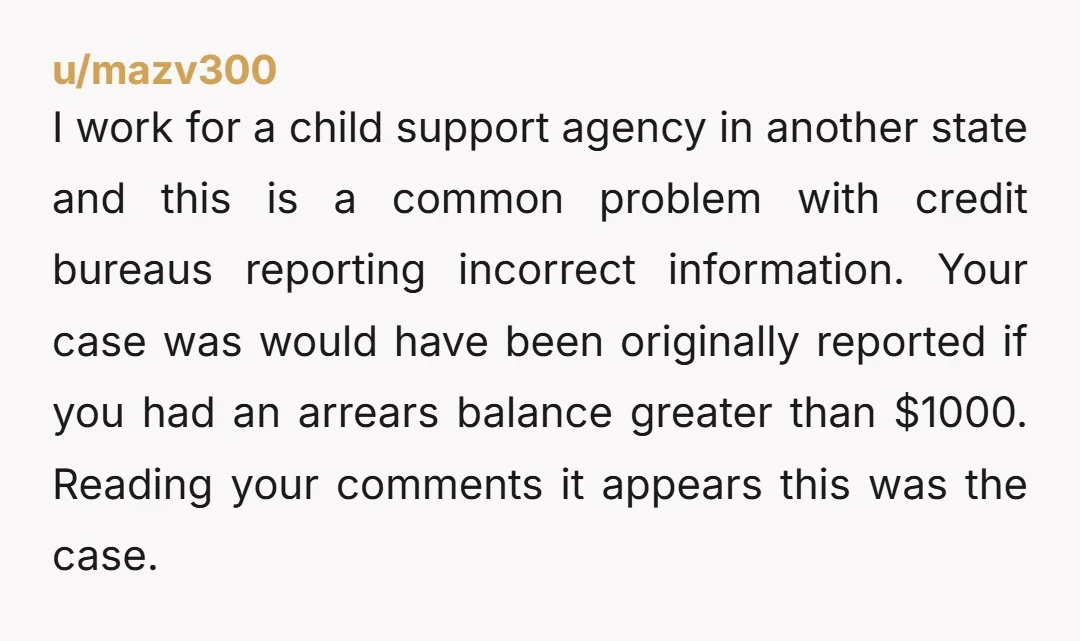

This veteran’s frustrating clash with Equifax clearly illustrates the devastating impact of rigid automated systems on real lives. From a practical standpoint, the issue stems from the way credit disputes are handled behind the scenes. When a consumer submits a dispute with physical proof, credit bureaus often reduce that complex complaint into a simple three-digit code sent through an automated system called e-OSCAR. The data furnisher—in this case, the Texas Office of the Attorney General—likely just verified the account’s existence rather than reviewing the specific $0 balance nuance.

According to the Fair Credit Reporting Act (FCRA), overseen by the Federal Trade Commission, consumers have the right to accurate reporting and can seek compensation for actual damages, such as a lost mortgage rate. To fix this concretely, the veteran should bypass the credit bureau’s basic dispute portal.

Instead, he needs to contact the Texas OAG directly and request that an agent manually submit an Automated Universal Data (AUD) form through the e-OSCAR system to correct the record in real-time. Simultaneously, retaining an FCRA attorney is a smart move, as the impending financial loss of a rate lock provides clear grounds for legal leverage. Anyone dealing with massive financial bureaucracy should always document every interaction and escalate beyond tier-one customer service.

Navigating the labyrinth of modern credit reporting can feel like an impossible battle, especially when automated systems refuse to acknowledge documented facts. The sheer financial weight of a single unverified code highlights a significant vulnerability in how consumer data is managed and corrected.

Do you think the credit bureau should be held liable for the massive lost interest rate, or is the state agency ultimately at fault for the initial reporting? And how should these automated dispute systems be reformed to protect consumers? Share your thoughts below!

Community Opinions

Most sided firmly with OP, urging him to bypass the automated systems and take immediate legal or political action.

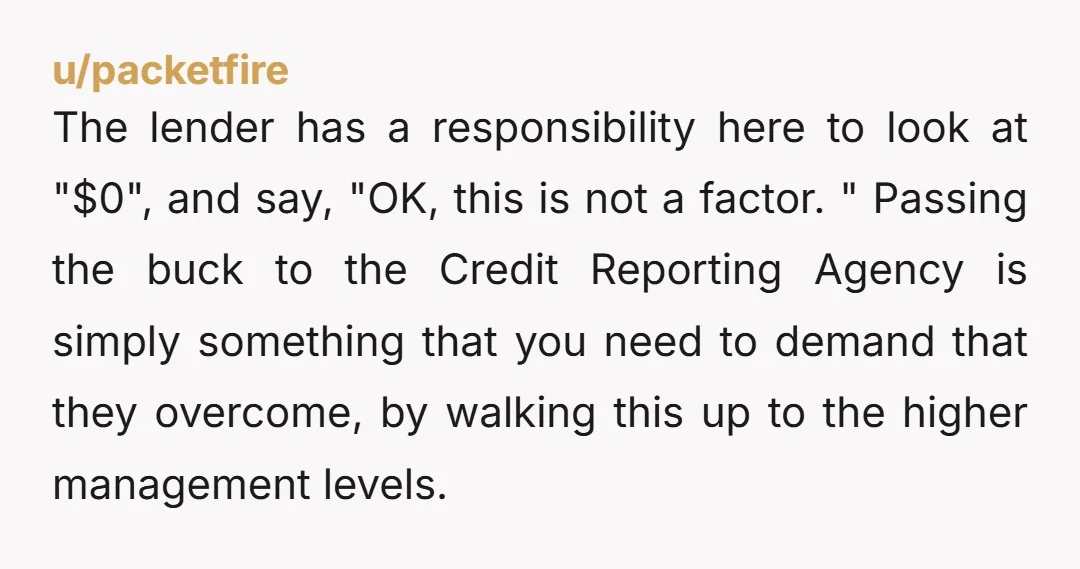

A few industry insiders chimed in to explain the exact technical loopholes causing the nightmare.

The collision of a rigid credit score algorithm and a massive life milestone is a scenario no one wants to face. While the original poster did everything right by providing state documentation, the automated verification process proved to be a formidable, faceless wall.

Do you think the lender should have overridden the zero-dollar error, or did Equifax act negligently by relying on an automated system? And how would you handle a massive financial roadblock right before closing on a house?

Share your hot take below!