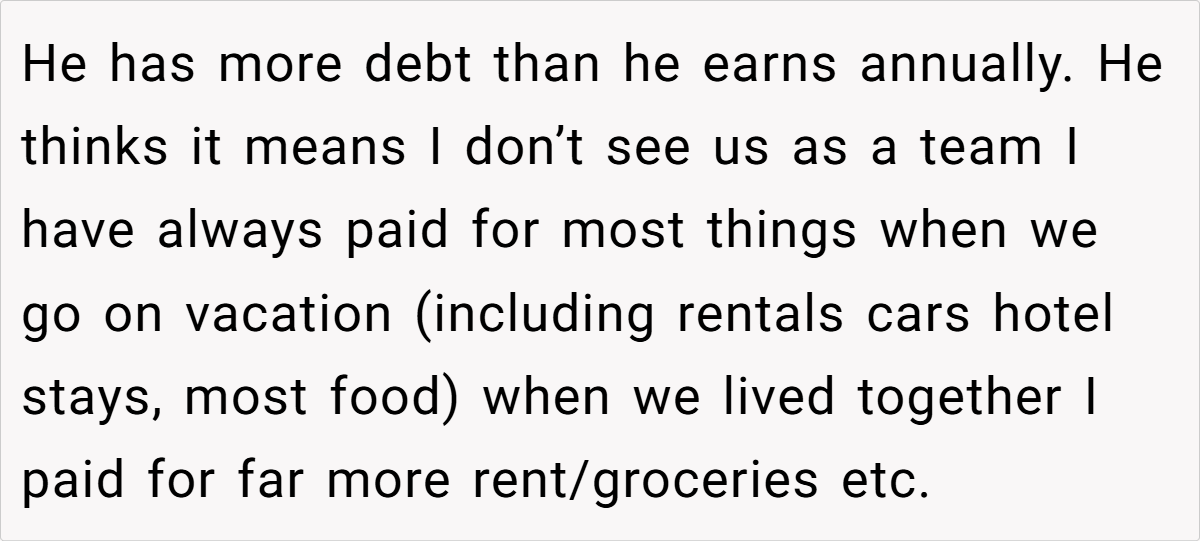

My 36F Fiancé 30M wants to be added to my mortgage/title of home, but I think he’s being unreasonable. Thoughts? AITAH?

In relationships, merging finances can be as challenging as finding the perfect balance between personal ambitions and shared dreams. One Redditor’s dilemma perfectly illustrates this tension—a successful, independent woman faces pressure from her fiancé, who is struggling with debt, to be added to the mortgage and title of the home.

Despite her achievements and hard-earned financial stability, his insistence that this move symbolizes their “team” spirit has ignited a heated debate about fairness, responsibility, and protecting one’s investments.

The situation is particularly delicate because it pits genuine love and commitment against the practical realities of financial inequality. With one partner shouldering the lion’s share of expenses, the question arises: should love overcome financial prudence, or is it wiser to wait until circumstances change? This modern conundrum invites us to rethink what partnership really means in today’s economic landscape.

‘My 36F Fiancé 30M wants to be added to my mortgage/title of home, but I think he’s being unreasonable. Thoughts? AITAH?’

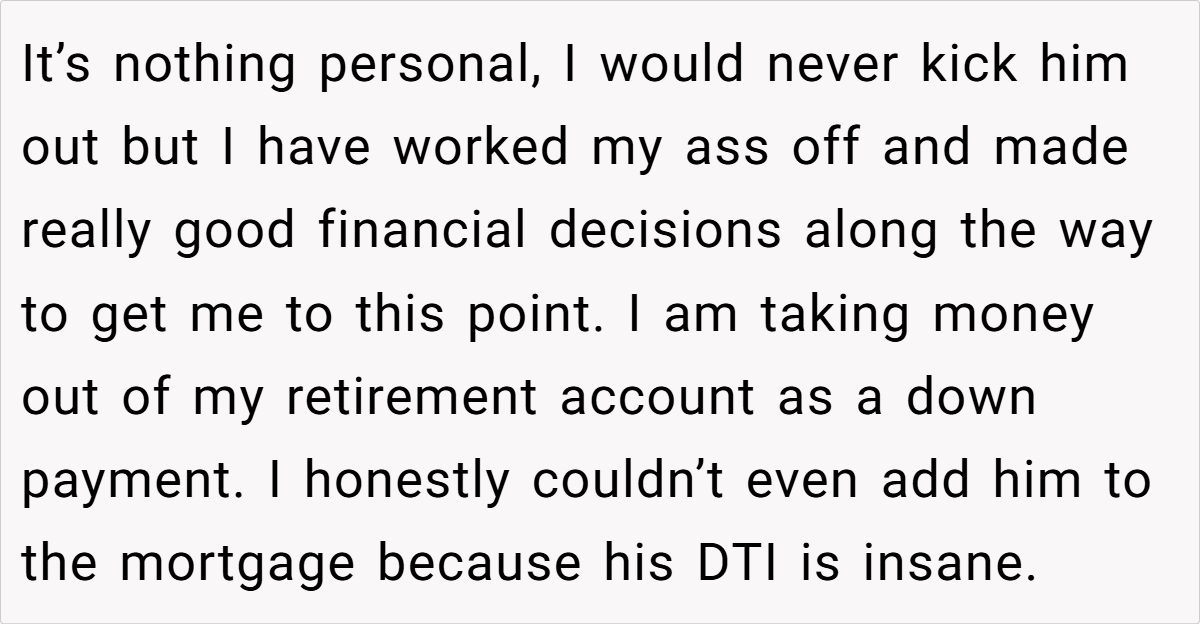

Merging financial lives is one of the most significant decisions a couple can make, and this case is no exception. When one partner is financially stable and the other is burdened by debt, the idea of adding a name to a mortgage or title can create a risky imbalance. Financial experts advise caution in such scenarios to protect one’s long-term interests, ensuring that both partners contribute equitably to shared assets.

In discussing this issue, renowned financial expert Suze Orman once stated, “Your home is likely your biggest asset, and you shouldn’t jeopardize your financial security by making decisions that might hurt your future.” Her words resonate here, suggesting that while love is important, protecting hard-earned wealth is equally crucial. It’s vital to ensure that financial decisions are made on a sound footing and not merely as a gesture of unity.

The situation also highlights a broader issue in modern relationships—the need for transparent, balanced financial planning. When one partner shoulders most expenses and takes on significant financial risk alone, it’s a red flag that should prompt honest conversation. In this case, the fiancée’s careful approach reflects a commitment to preserving her financial stability, a decision that many experts deem responsible when faced with a partner whose debt-to-income ratio is unsustainable.

Moreover, blending finances without proper safeguards can lead to future conflicts. Legal advisors often recommend creating clear agreements or even prenuptial arrangements to protect both parties. These measures aren’t a sign of mistrust; rather, they provide a safety net in case circumstances change.

As one expert noted, “Couples who plan ahead for financial uncertainties tend to have fewer conflicts down the road.” This approach encourages both partners to work toward a secure future together without compromising personal assets.

Ultimately, while the emotional desire for shared ownership is understandable, the practical realities of debt and income disparities cannot be ignored. It might be more prudent to revisit the conversation once financial circumstances improve. By balancing love with fiscal responsibility, couples can lay a foundation that supports both emotional and financial well-being, ensuring that both partners feel secure in the partnership they are building.

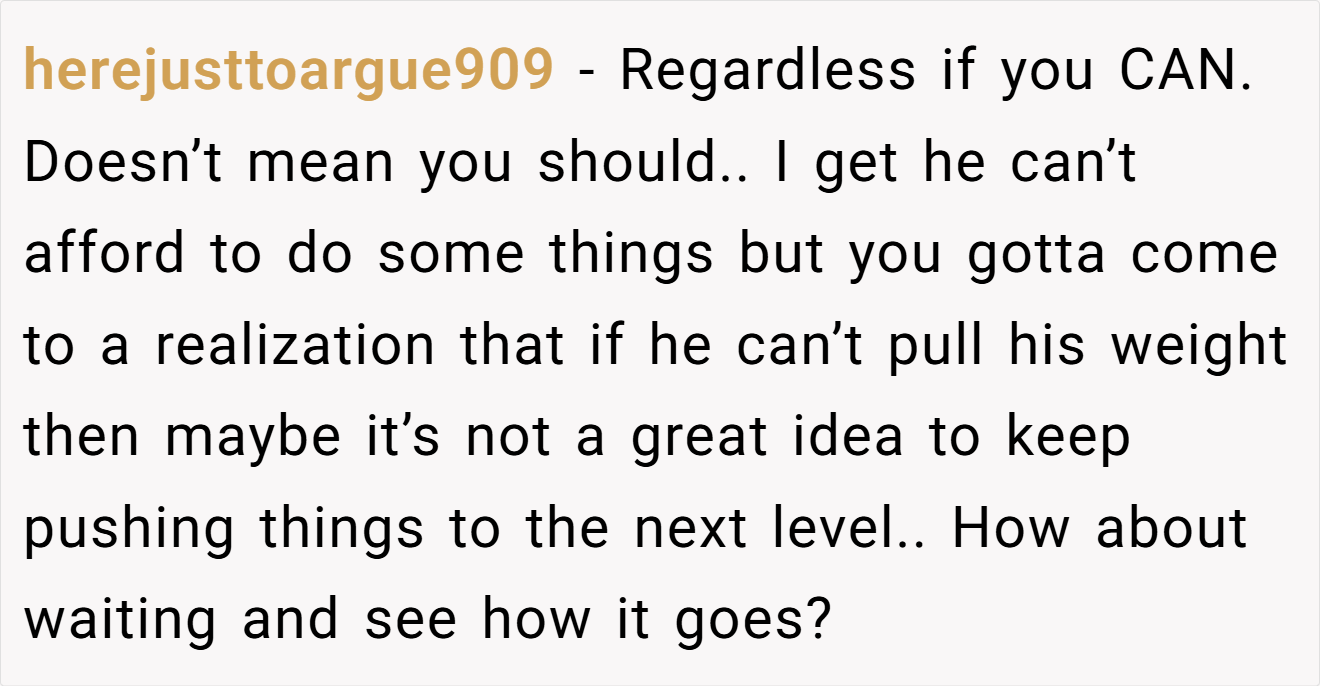

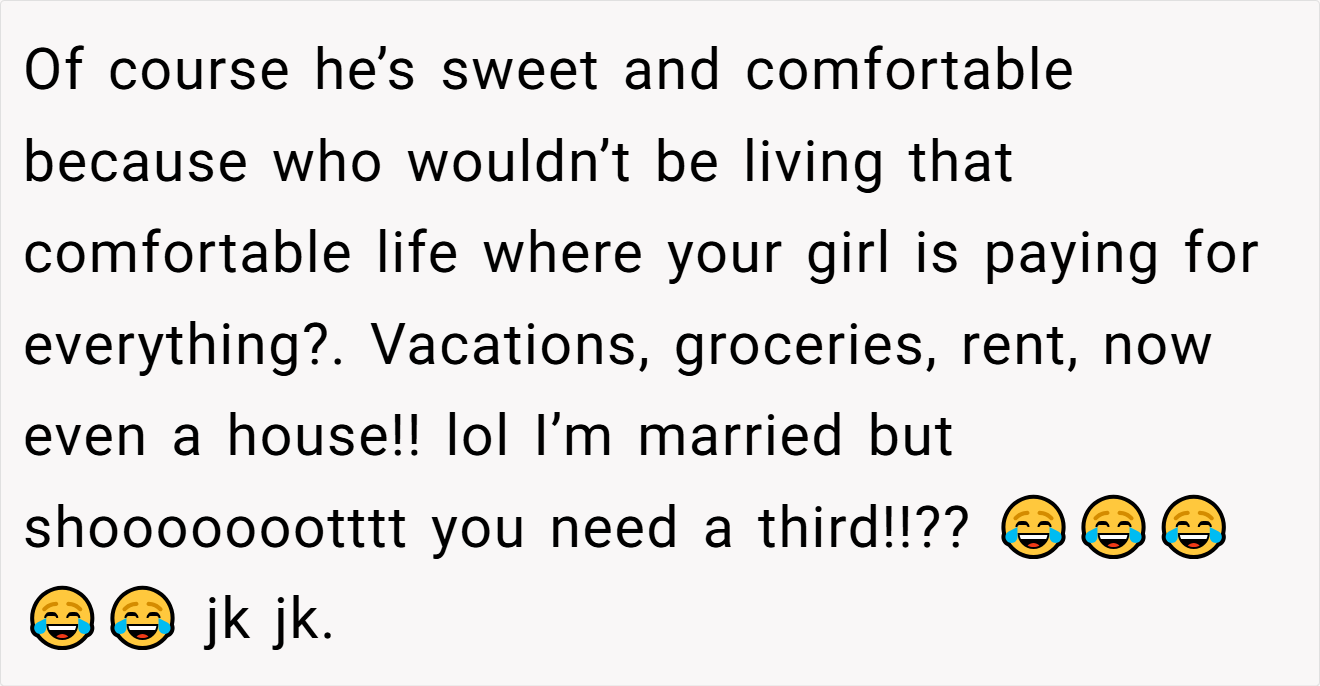

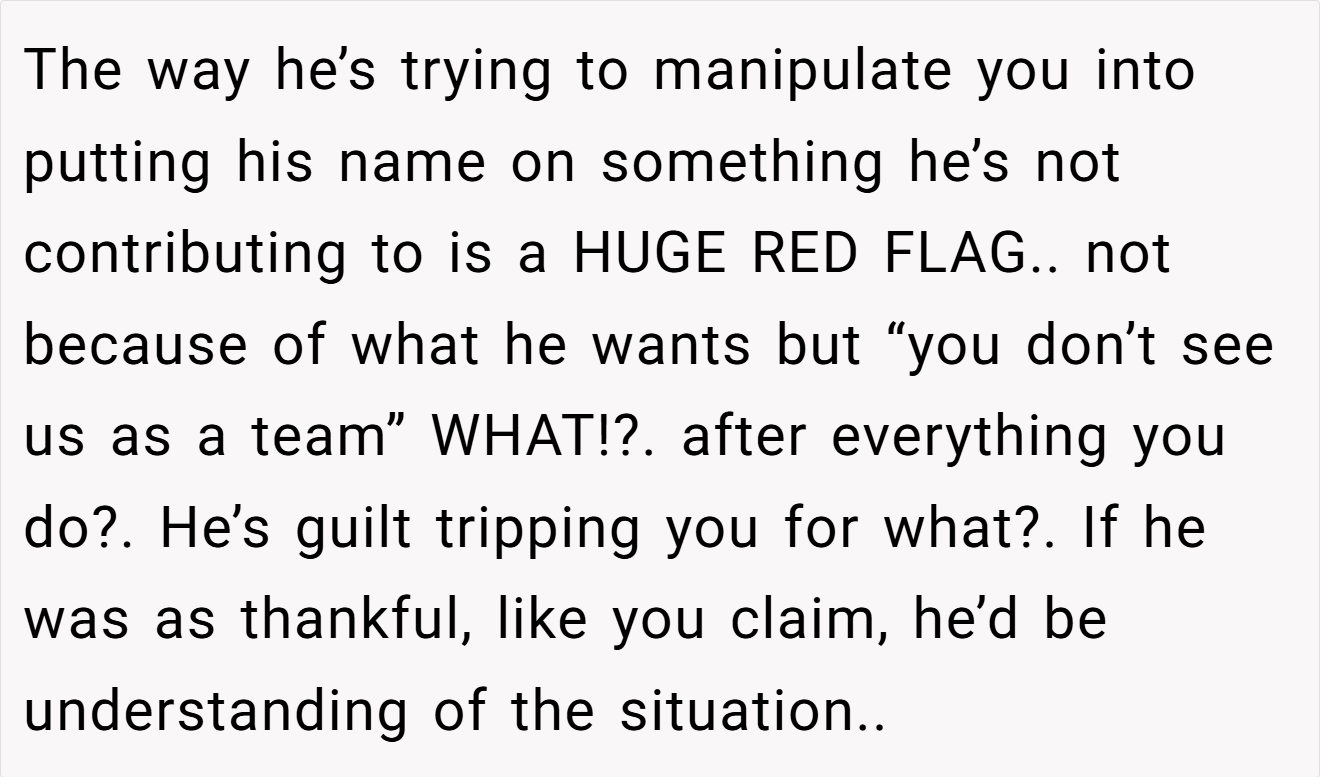

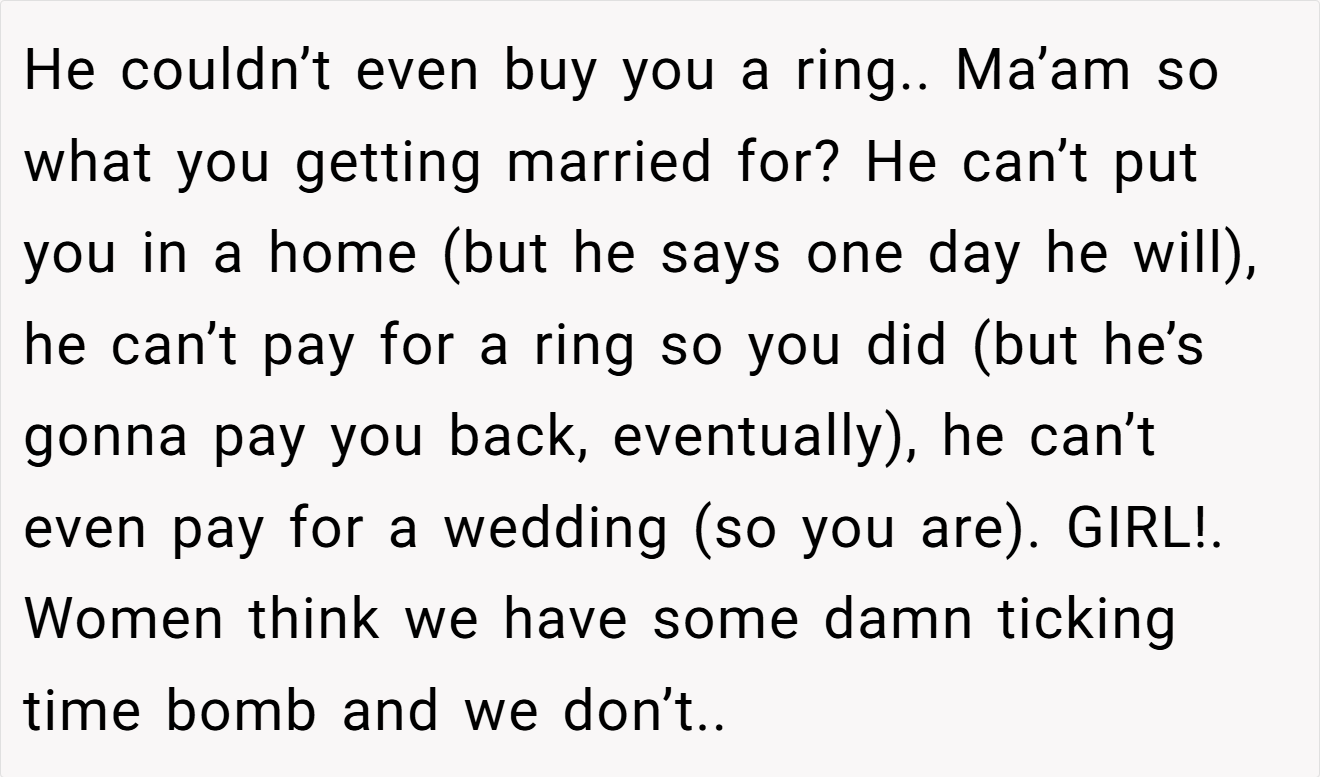

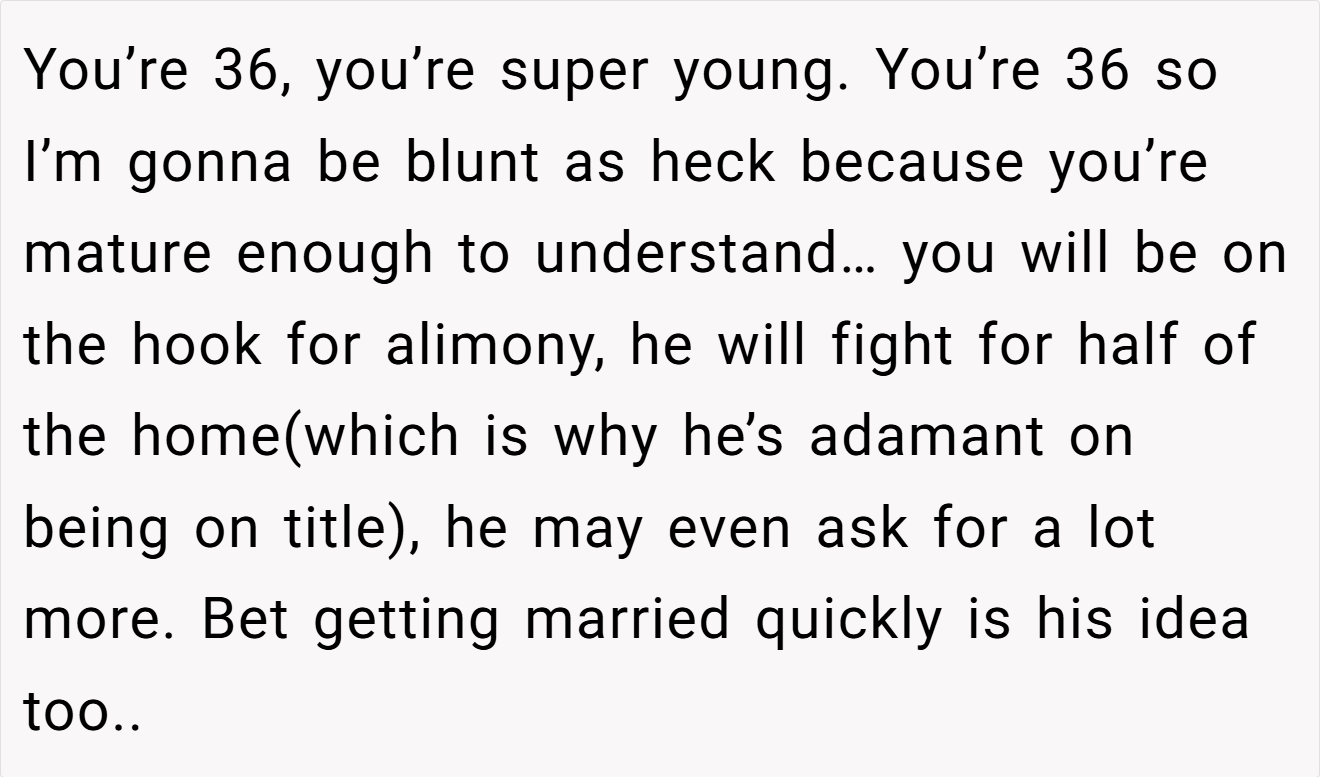

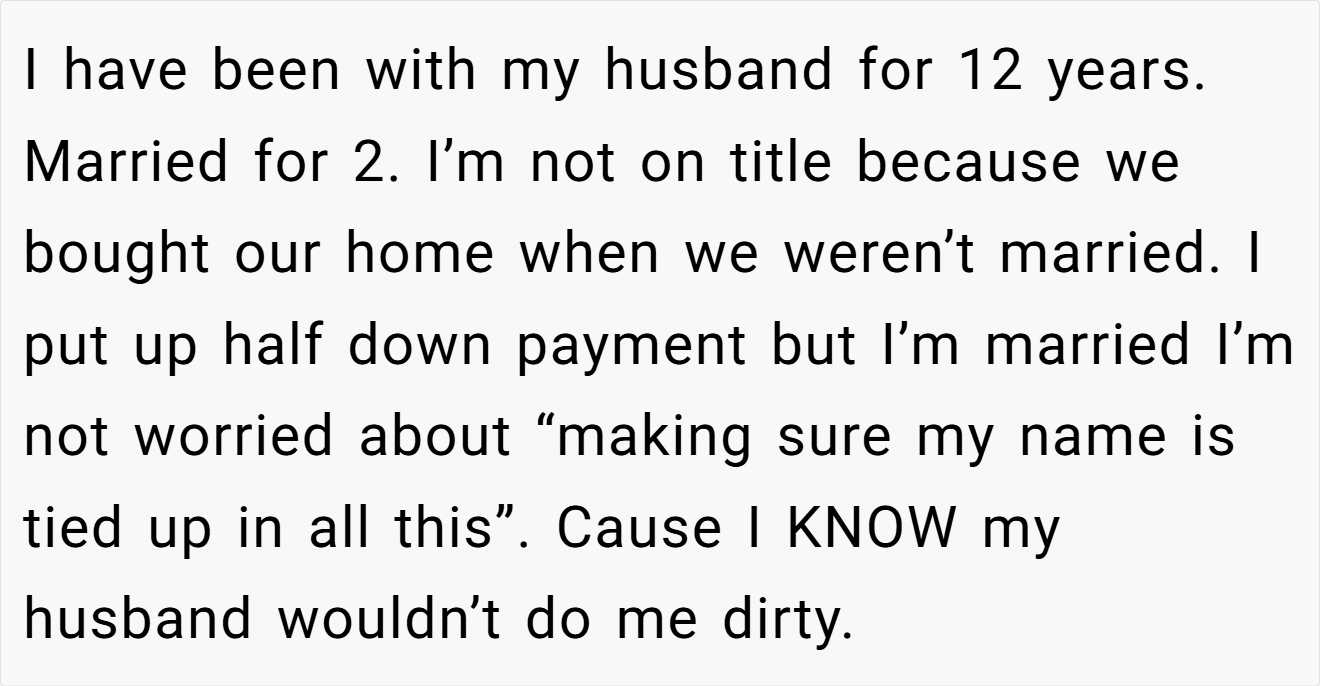

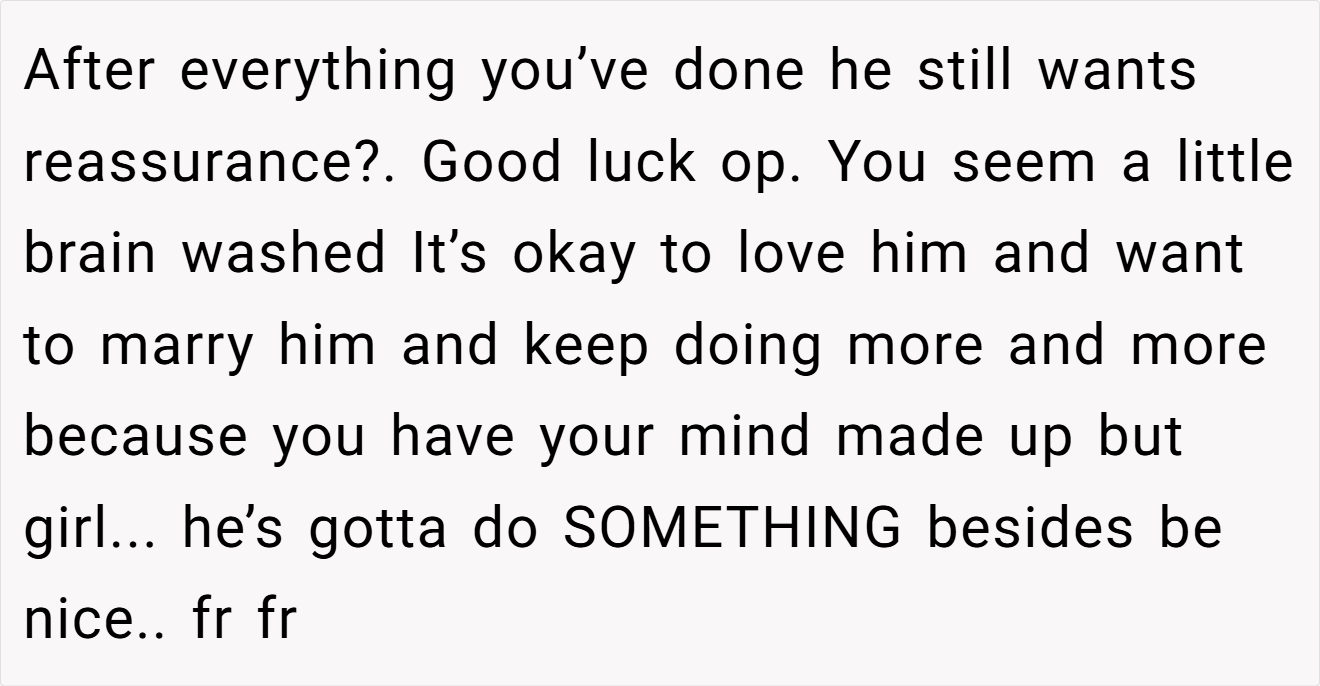

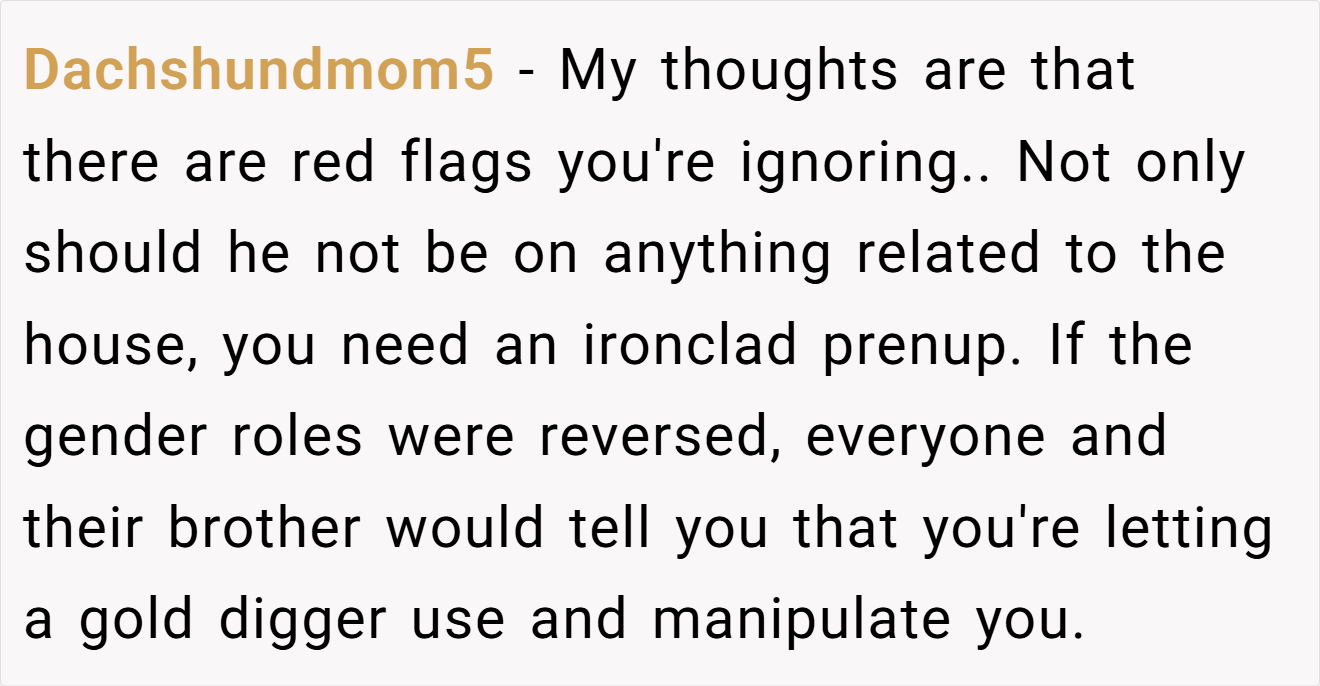

Take a look at the comments from fellow users:

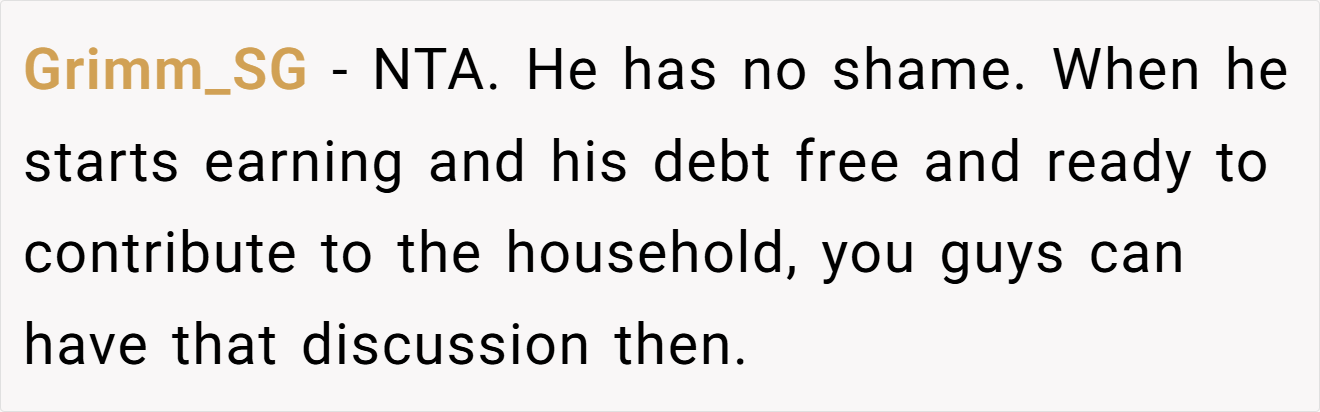

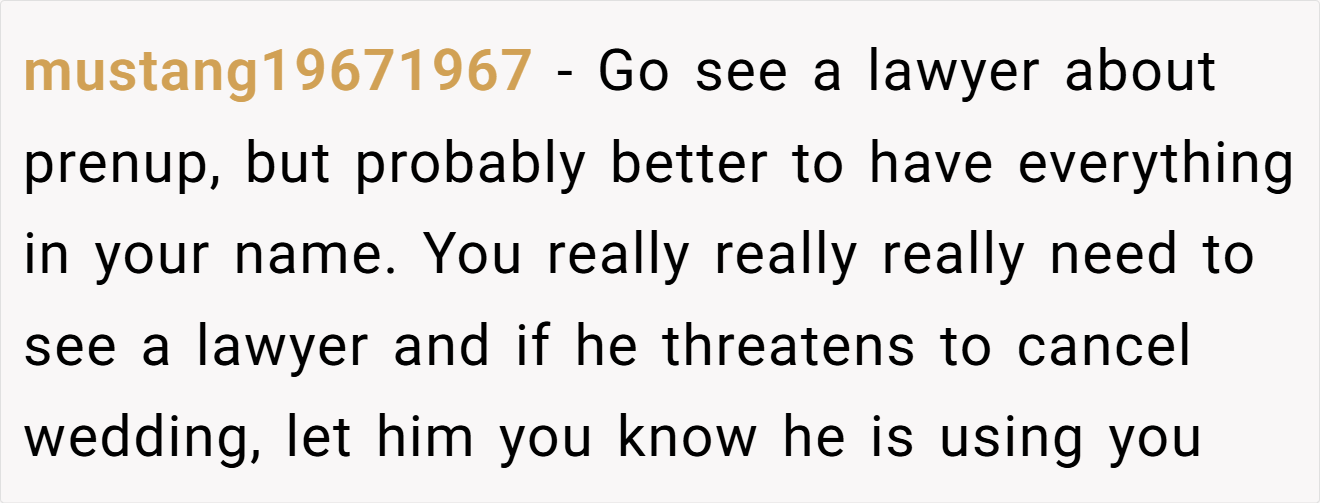

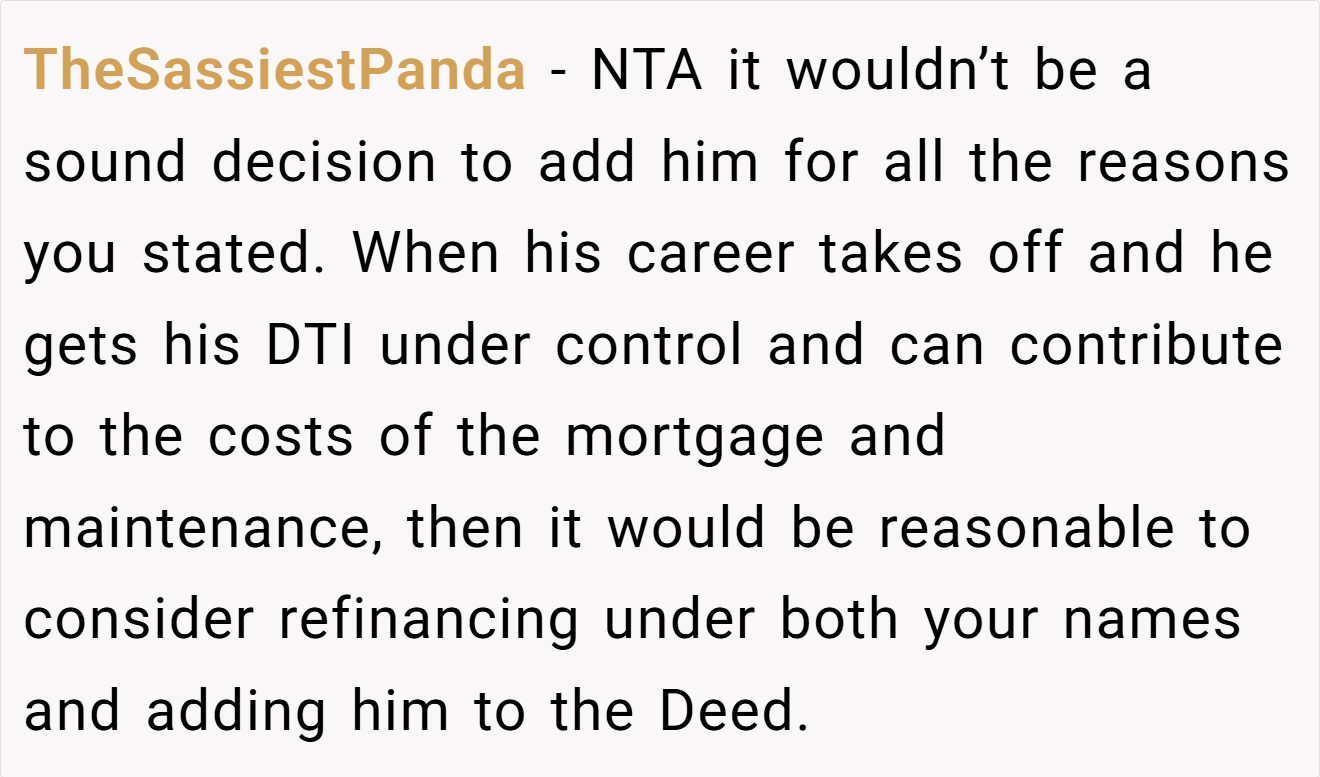

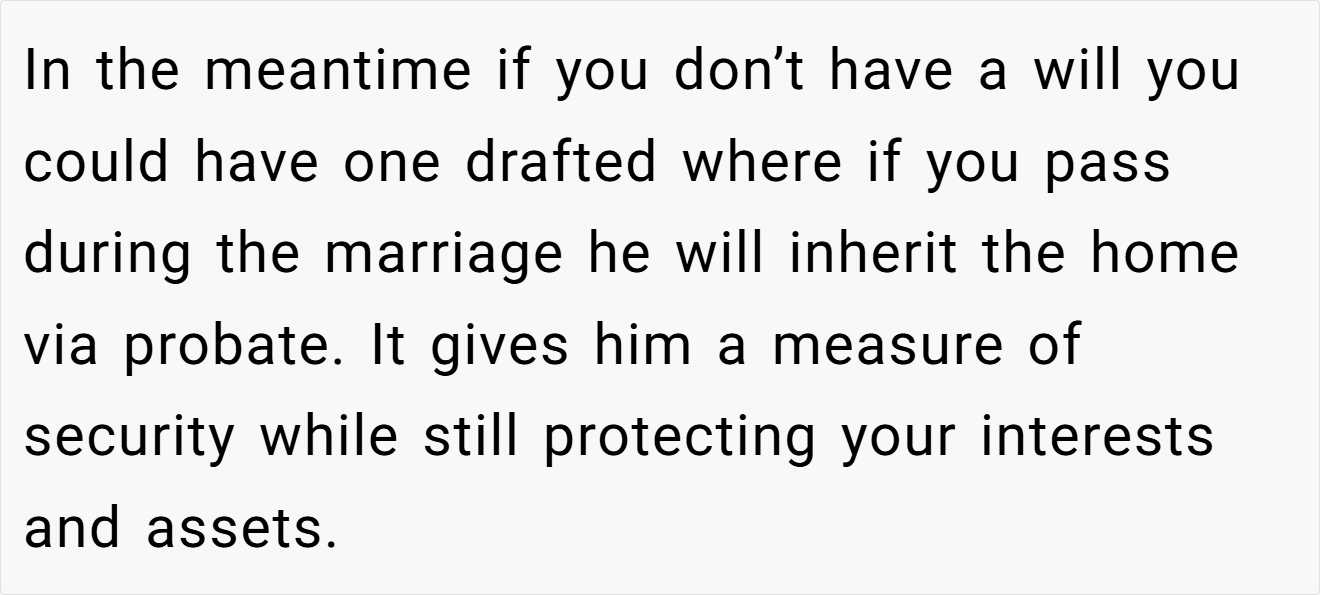

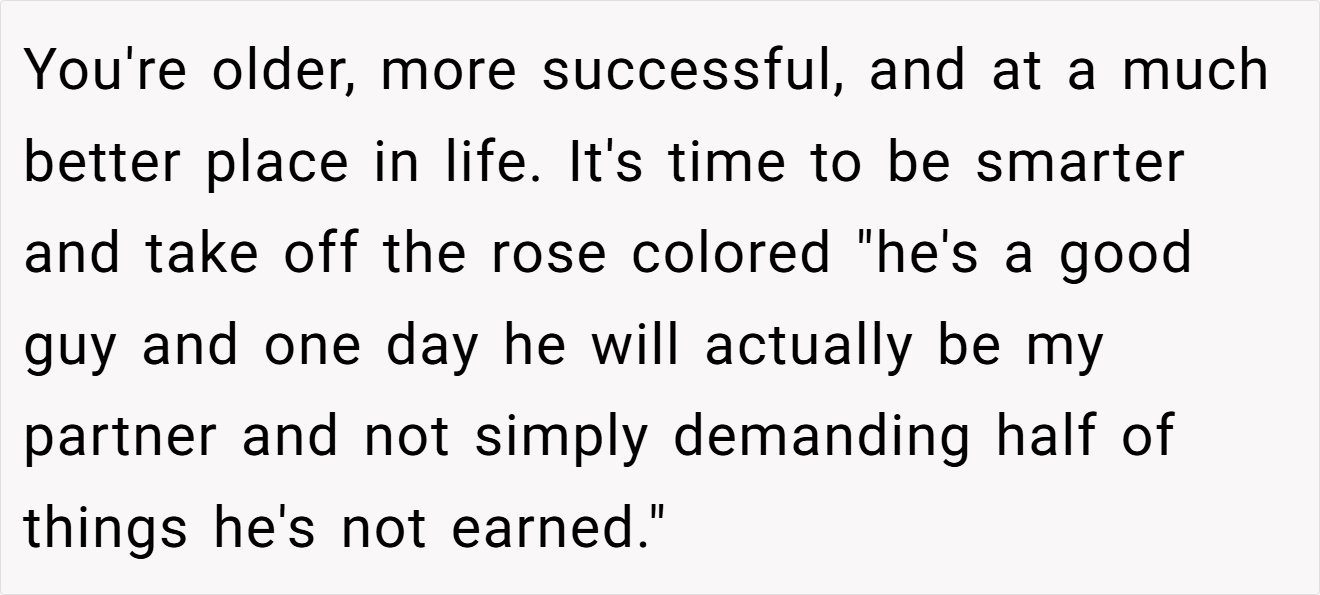

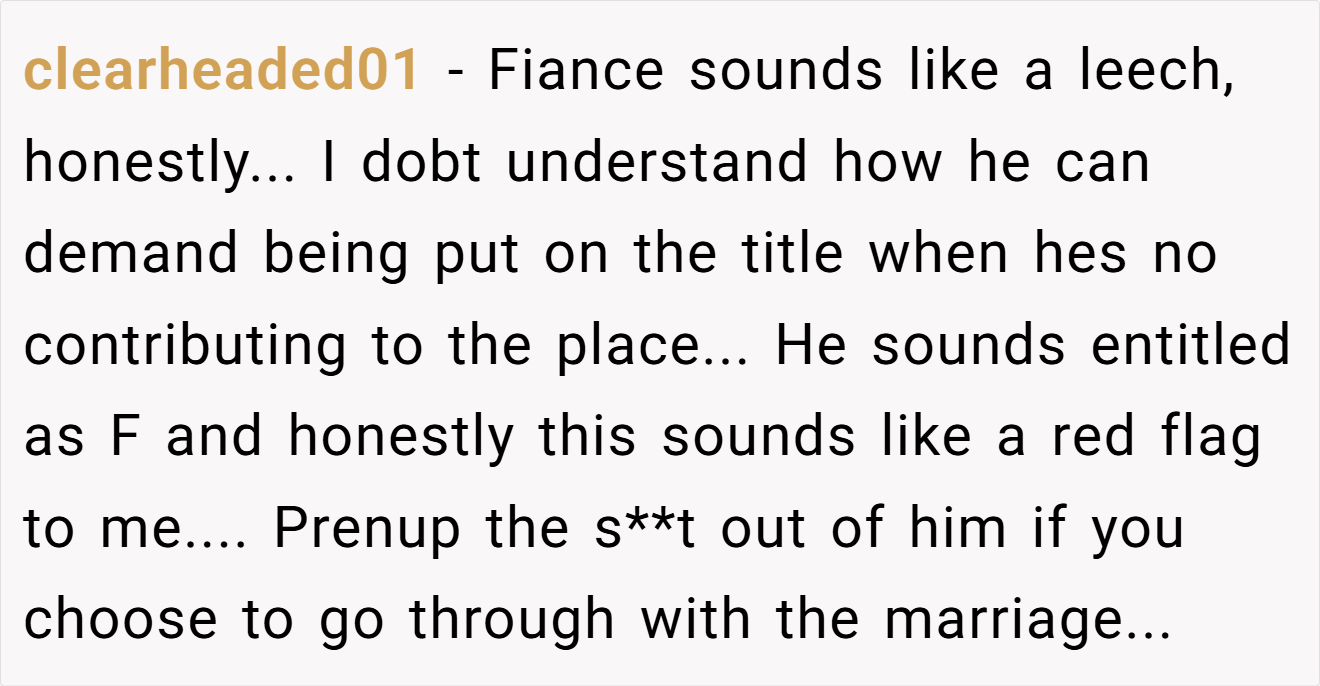

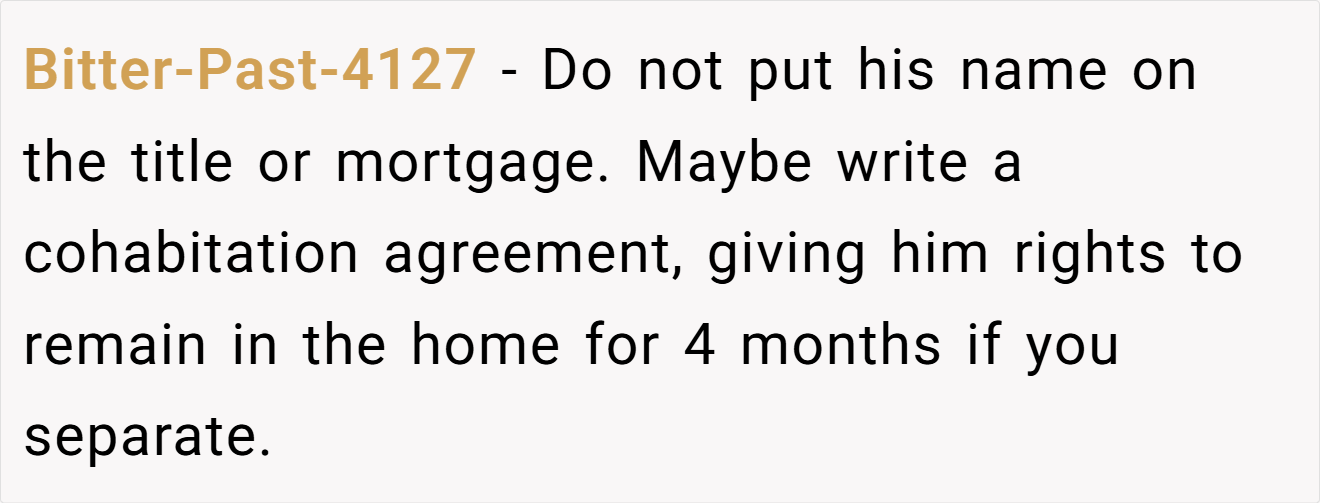

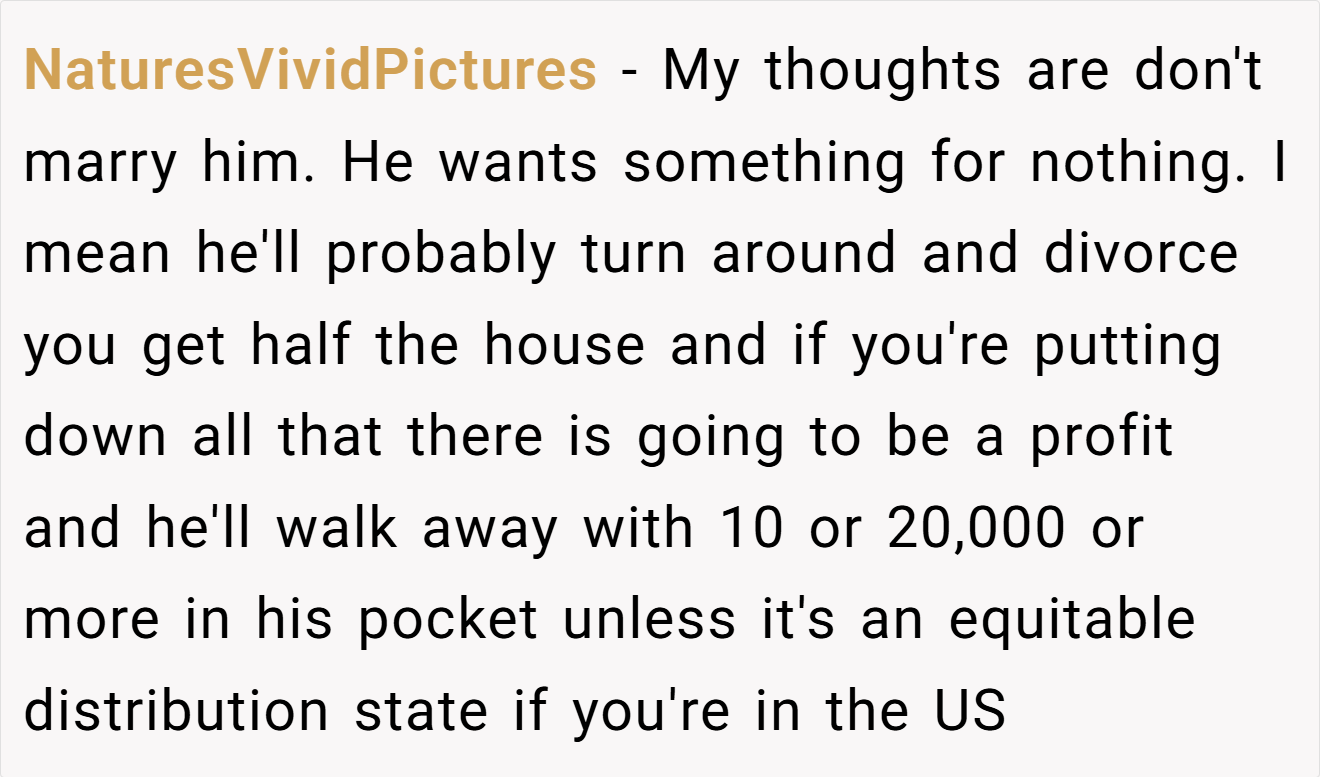

The Reddit community’s reactions to this situation were a blend of practical advice and sharp humor. Many users supported the decision to wait until the fiancé’s financial picture improved, emphasizing that shared assets should be built on mutual contribution.

A common sentiment was that merging finances without equal investment could pose a risk to long-term financial security. While some commenters expressed frustration over perceived entitlement, others suggested legal safeguards like prenuptial agreements to protect both parties. Overall, the discussion underscored the need for clear communication and balanced responsibility.

This story reminds us that while love and commitment are essential, they don’t always equate to shared financial readiness. Protecting one’s financial future sometimes means making tough choices that might seem unromantic in the moment. What do you think? Is it better to keep financial matters separate until both partners are on more equal footing, or can love truly bridge the gap? Share your thoughts and experiences—what would you do if you found yourself in a similar situation?