Dad Borrowed His Child’s Name for a Storage Unit, Now a Surprise $1,800 Bill Changes Everything

We all know that moment when a quick favor for a parent suddenly spirals out of control. For one twenty-nine-year-old, a casual agreement to help their dad between moves just turned into an expensive nightmare.

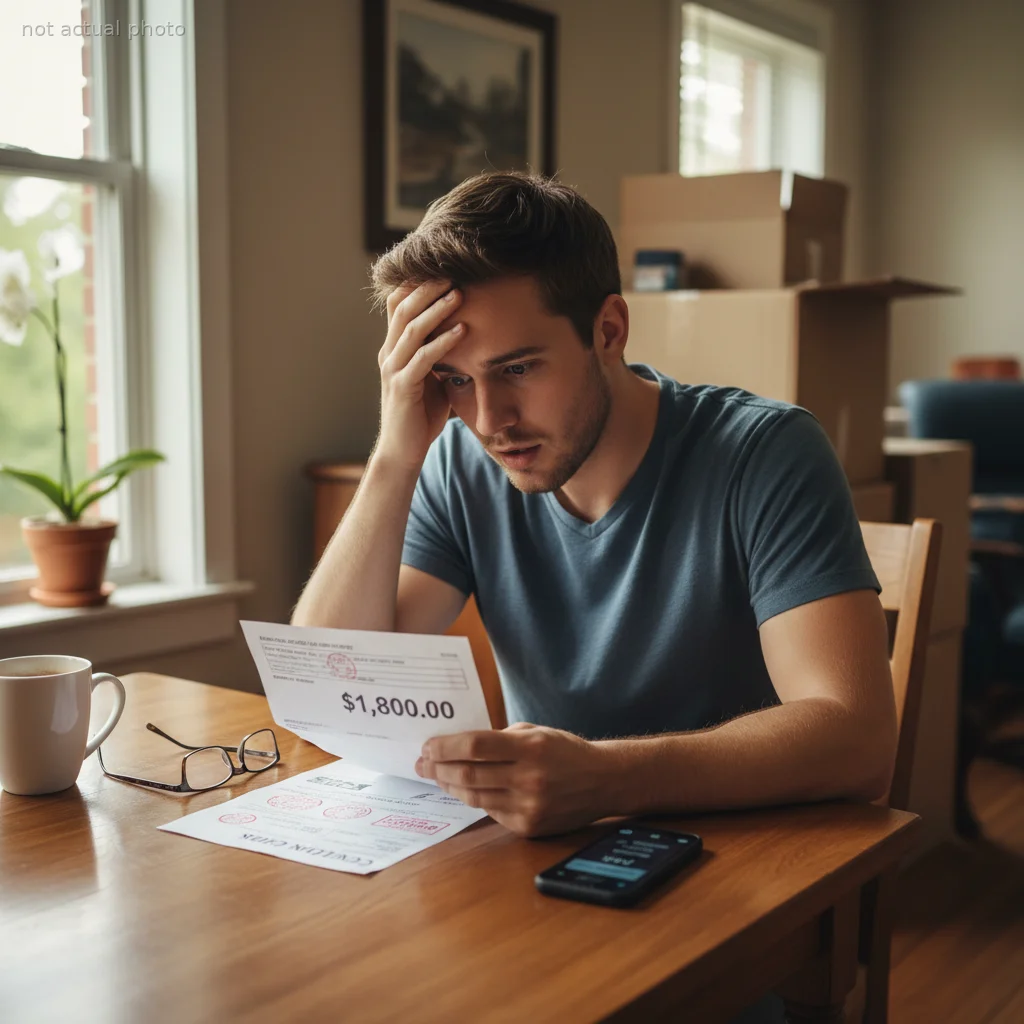

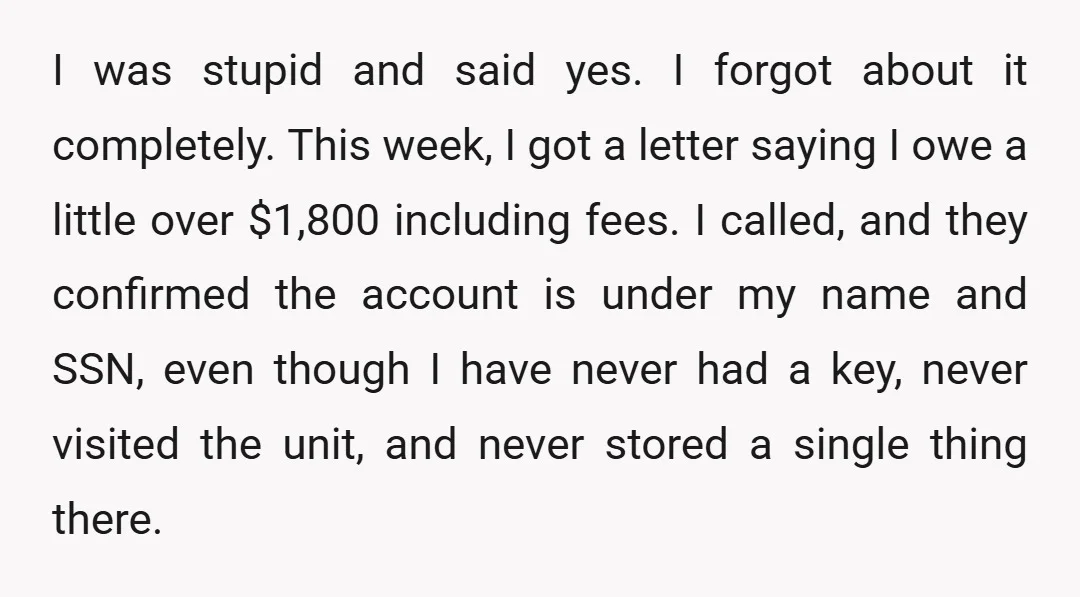

Back in 2021, the original poster (OP) agreed to let their father use their name for a temporary storage unit. Fast forward a few years, and that forgotten favor has resurfaced as an $1,800 collections notice tied directly to their Social Security number.

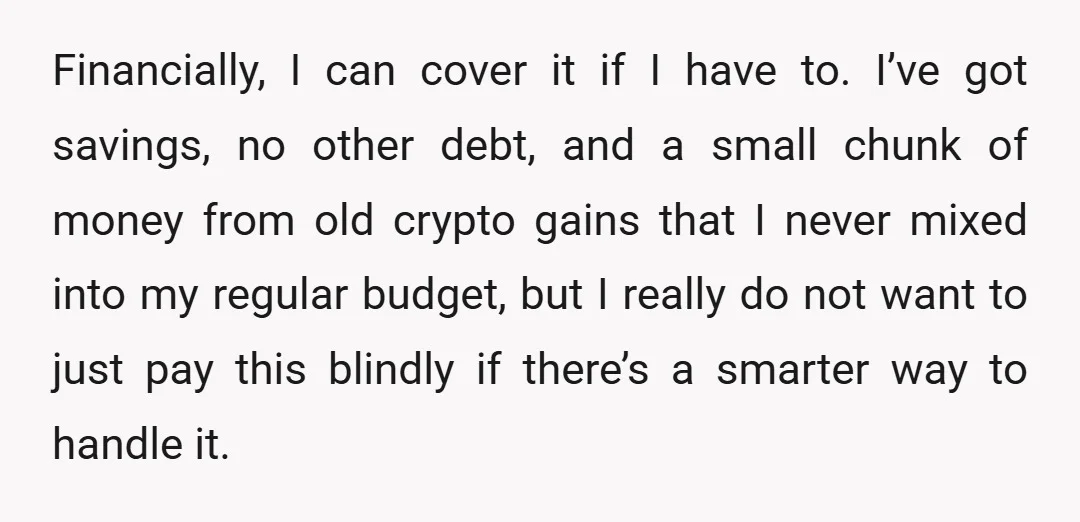

While OP has the savings to cover the unexpected hit, the betrayal stings, especially since the father keeps brushing off the debt with empty promises. Now, OP is trapped between protecting their own financial future and holding their dad accountable. Want the juicy details? Dive into the original story below!

A simple family favor quickly set the stage for a massive financial headache years down the line.

Despite having zero access to the actual property, the financial burden landed squarely on the child’s shoulders.

When family favors cross into legal obligations, the path forward requires tactical boundary setting rather than just emotional arguments. Financial advisors frequently note that one of the biggest mistakes adult children make is absorbing the consequences of their parents’ financial missteps. When dealing with family debt, experts emphasize that your financial boundaries are not optional.

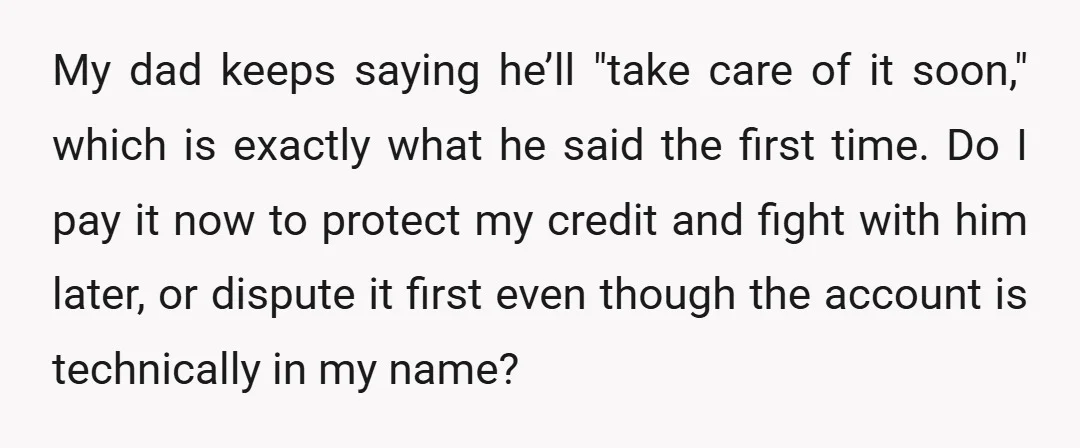

In this scenario, OP is trapped by their past consent. Even though they didn’t physically sign the contract, giving verbal or written permission to use their name created a legally binding vulnerability. Fighting the collection agency on the grounds of identity theft would require filing a police report against their own father—a nuclear option most families want to avoid.

The most practical step is to address the immediate threat to their credit score, but treat it as a hard lesson in financial boundaries. Moving forward, OP must refuse any requests to co-sign or lend their name. If you find yourself in a similar situation, consider requesting a formal transfer of the account or negotiating a settlement directly with the collections agency.

Navigating the fallout of a parent’s broken financial promise is never easy, especially when your own credit is on the line. The tension between protecting your financial stability and preserving family harmony often forces people into impossible choices. Ultimately, establishing firm boundaries is the only way to prevent history from repeating itself.

Do you think OP should pay the debt immediately to save their credit, or force their dad to handle the mess he created? And how would you rebuild trust after a financial betrayal like this? Share your thoughts below!

Community Opinions

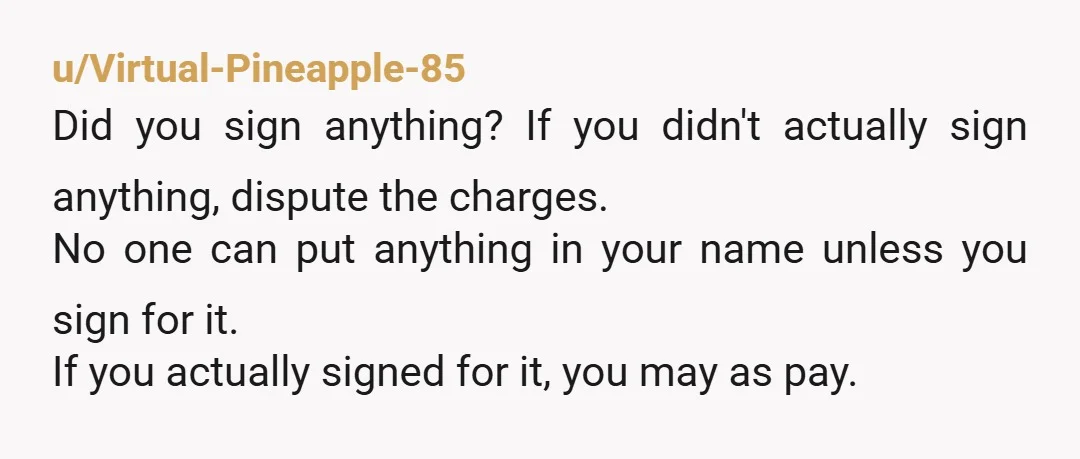

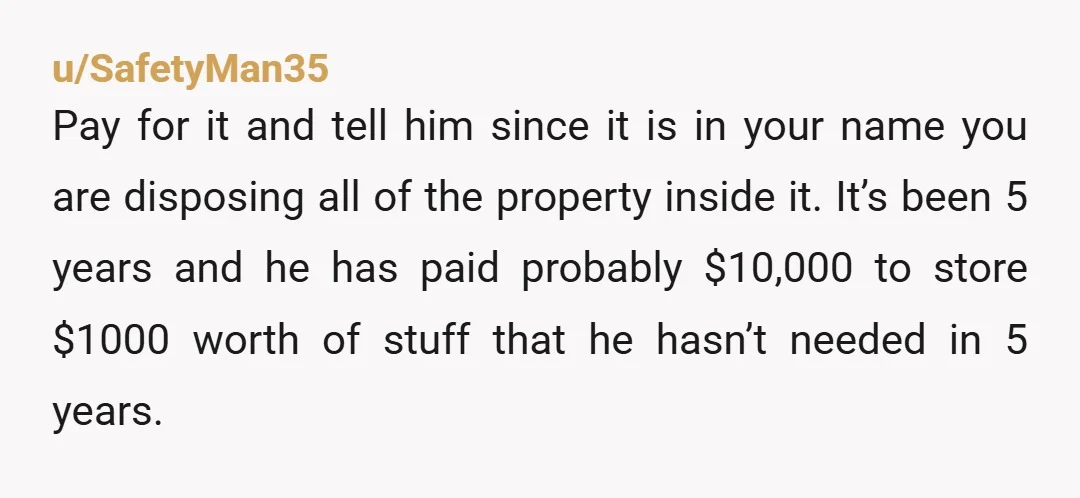

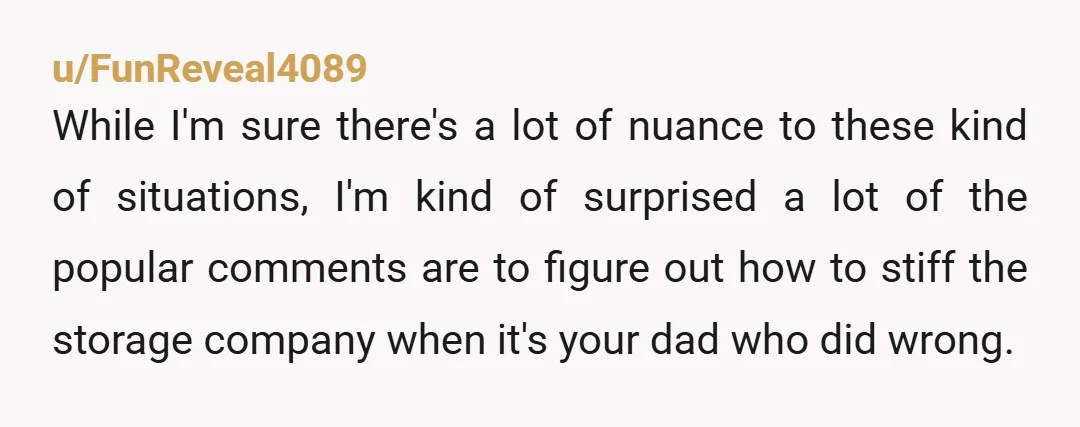

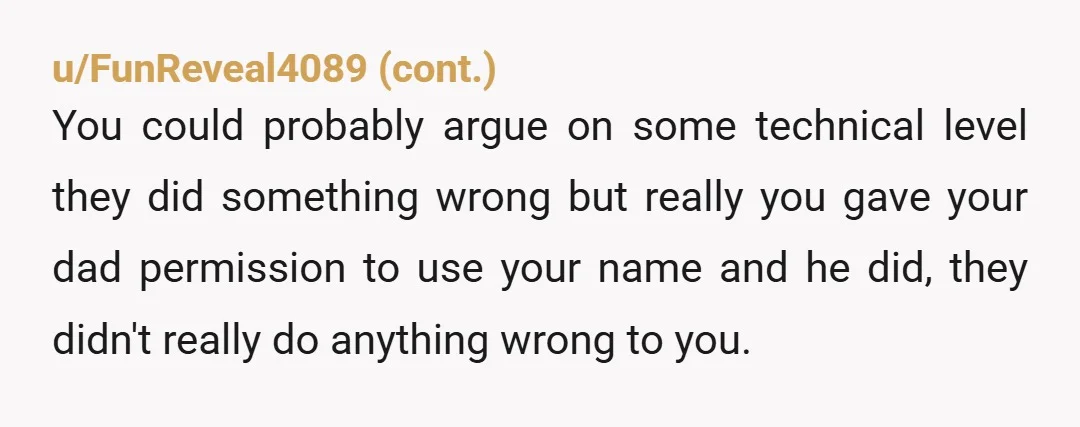

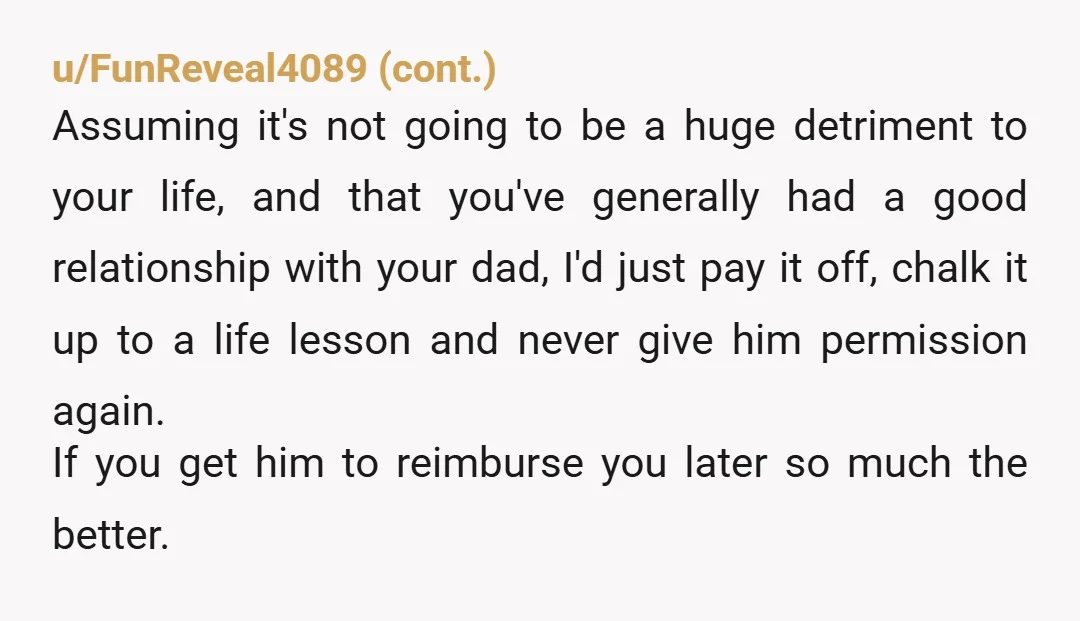

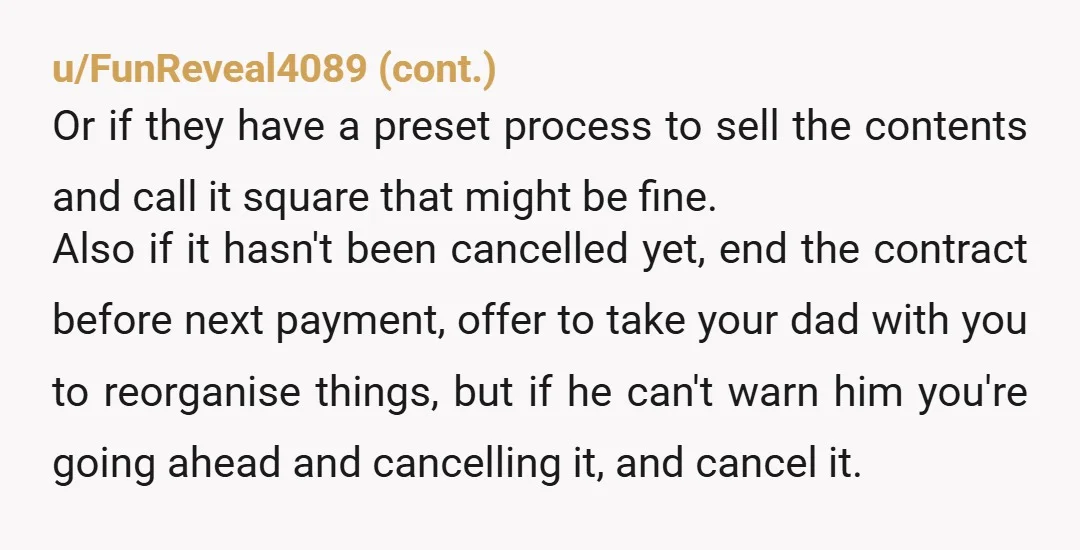

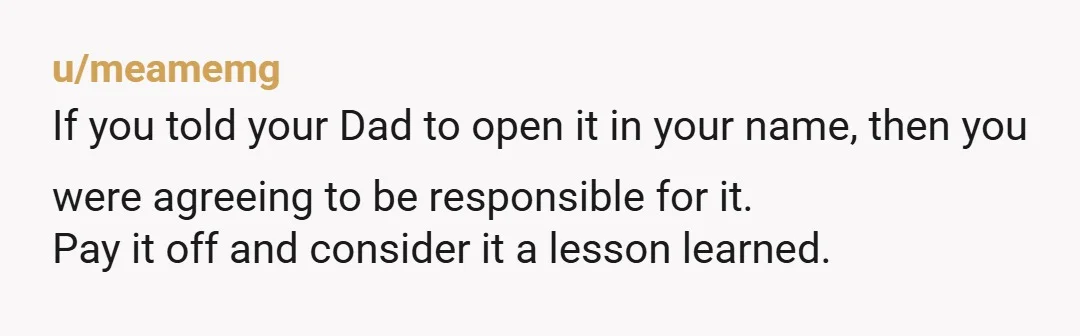

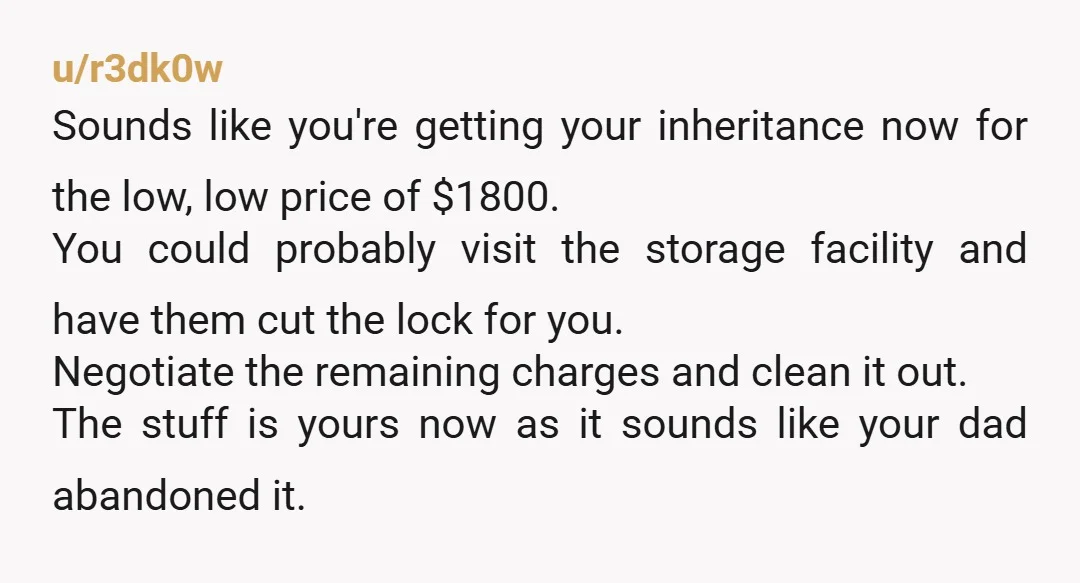

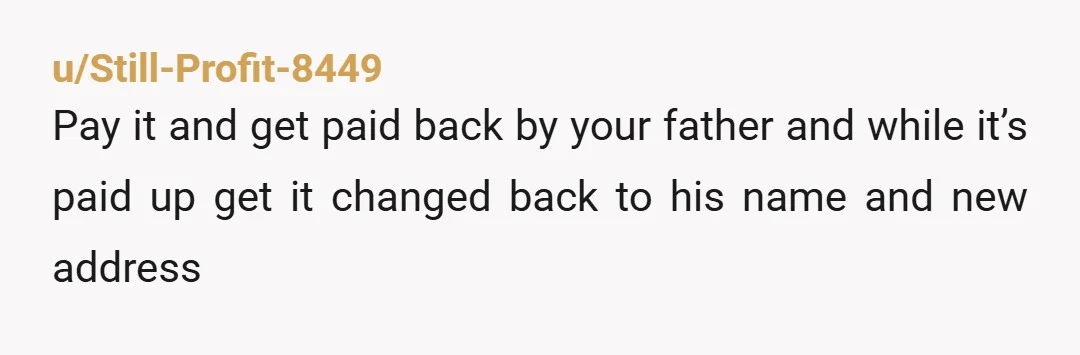

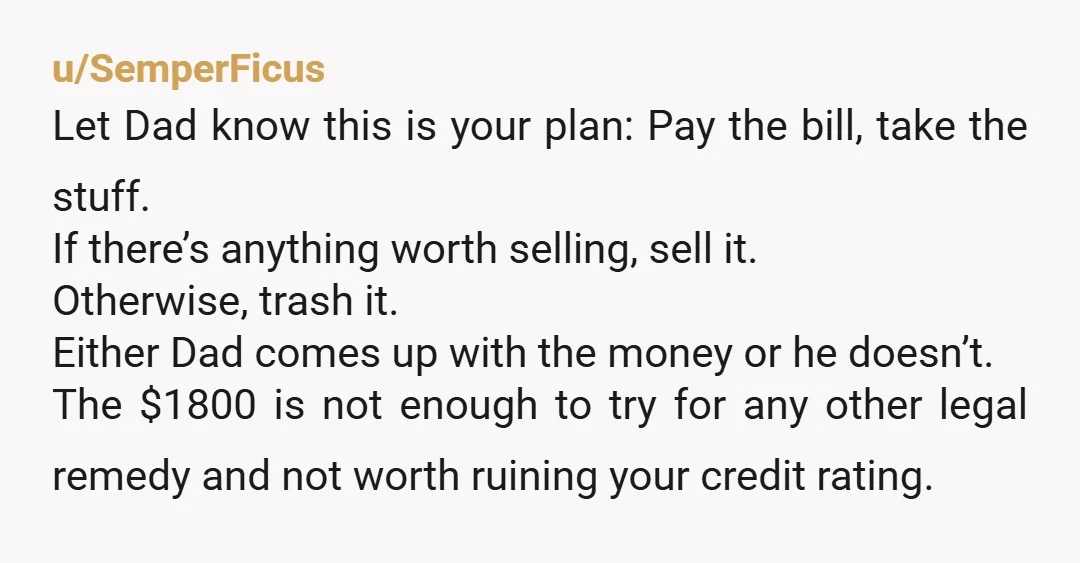

Reddit came in hot—nearly unanimous in their verdict that OP needs to pay the bill to protect themselves, but with a clever twist on how to handle the dad's stuff.

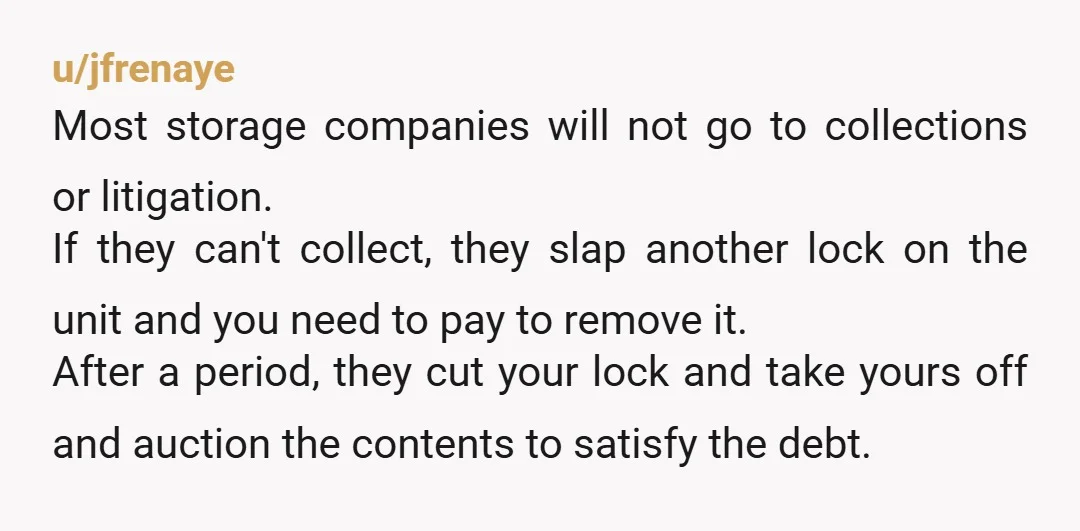

And a few reminded everyone that paying the debt means the contents of that storage unit now legally belong to OP.

The line between helping family and protecting your own financial stability is incredibly thin. While letting a parent use your name might feel like a harmless favor in the moment, it can easily snowball into a credit-ruining disaster. Setting strict rules about money is the only way to keep relationships intact.

Do you think OP should sell their dad’s belongings to cover the $1,800, or did they bring this on themselves by agreeing in the first place? And how would you handle a parent who expects you to foot the bill for their irresponsibility? Drop your thoughts in the comments.