AITA for Telling My Wife She Can’t Quit Her Job Because I Don’t Want to Be the Sole Breadwinner?

Marital decisions can often blend financial realities with personal fulfillment, making every choice feel like a high-stakes negotiation. In this story, a couple finds themselves at a crossroads when the wife, overwhelmed by burnout, decides she wants to quit her job without a backup plan.

Meanwhile, her husband, who shoulders the entire household income, argues that any major change should be a joint decision to avoid future financial strain. The simmering tension is palpable, reflecting deeper questions about fairness, shared responsibility, and the evolution of modern partnerships.

Set against the backdrop of everyday life, their conversation becomes a microcosm of larger societal issues: balancing personal happiness with practical responsibilities. The narrative paints a vivid picture of two people caught between dreams and duty, illustrating the complex interplay of emotions and reason in relationships. This scenario invites us to explore how couples can navigate personal needs while ensuring financial security.

‘AITA for Telling My Wife She Can’t Quit Her Job Because I Don’t Want to Be the Sole Breadwinner?’

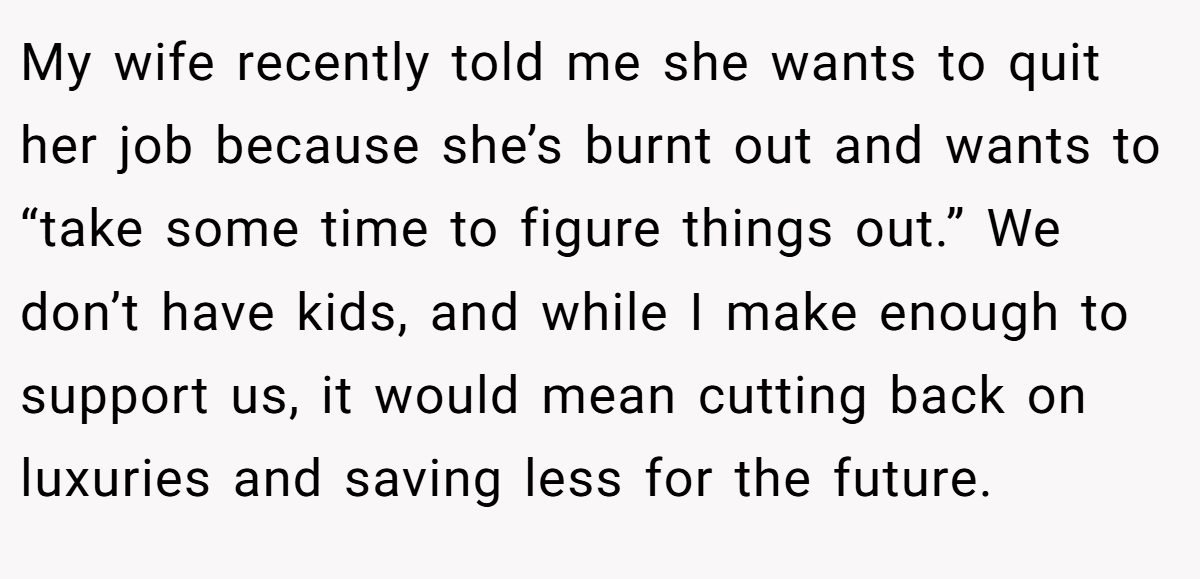

Letting personal exhaustion drive major financial decisions can lead to unintended consequences. In this case, the wife’s declaration of quitting without a clear plan has sparked friction. The husband emphasizes that while burnout is real, it isn’t fair to abruptly upend their lives without exploring alternatives. Their situation exemplifies the challenges faced by modern couples: when personal well-being and fiscal responsibility collide, joint decisions become essential to avoid long-term regret.

The core issue here revolves around the value of planning together. Although the wife feels the need for a break, the husband’s concerns echo a broader anxiety about financial stability in today’s unpredictable economy. Their exchange highlights the importance of transparency and teamwork in managing household finances, particularly when one income supports dreams, luxuries, and future goals. This friction can serve as an opportunity to reassess shared goals and expectations.

Broadening the discussion, this dilemma mirrors a common struggle for many couples who navigate the fine line between career fulfillment and financial security. Statistics show that households with two earners are better equipped to handle unexpected expenses and economic downturns. When one partner makes a unilateral decision without thorough discussion, it can shake the foundation of trust and mutual support essential for long-term stability.

Many financial planners and relationship counselors stress the importance of making such decisions together. According to relationship expert Dr. Ramani Durvasula, “When significant changes aren’t mutually agreed upon, it can lead to emotional disconnection and financial missteps that ripple through every aspect of a partnership.” (Learn more at Psychology Today – Dr. Ramani Durvasula) This insight reinforces the need for collaborative problem-solving.

Both partners must balance personal well-being with the practicalities of shared financial responsibilities. Open dialogue and professional financial advice, such as consulting a financial advisor or counselor, can help bridge the gap between personal aspirations and economic demands.

Ultimately, fostering a respectful conversation about roles, finances, and future plans is crucial. The couple might benefit from setting up a joint session with a financial planner who can illustrate the realistic outcomes of various scenarios. This approach not only validates individual emotions but also reinforces the strength that comes with unity. By finding common ground, they can transform a moment of discord into an opportunity for growth.

Here’s the feedback from the Reddit community:

Overall, the Reddit community reactions emphasize that major life changes affecting shared finances should be carefully negotiated as a joint decision. Many commenters agree that while burnout is a valid concern, leaving a job abruptly without a solid backup plan can jeopardize the household’s stability.

The consensus points toward the importance of transparency and proactive planning—rather than unilateral decisions—in balancing personal well-being with financial responsibilities. Some users even suggest the involvement of a neutral financial expert or counselor to help mediate the discussion. Ultimately, the general tone of the community leans toward supporting a collaborative approach, which validates the husband’s request for a deliberate, thoughtful discussion about the change.

In conclusion, this story captures a pivotal moment where personal well-being meets financial pragmatism. The husband’s insistence on a joint decision underscores the importance of shared responsibility, while the wife’s burnout serves as a reminder that mental health must never be sidelined. Their exchange challenges us to consider how we balance career fulfillment with financial security in our own lives. What would you do if you found yourself in a similar situation?