AITAH for taking my sister’s wedding money that my mom gave me to transfer to her?

A 25-year-old woman dips into six months’ savings to bail out her 29-year-old sister after a home disaster, despite a spotty repayment history and her own student loans. The sister swears she’ll pay back every cent. Three months later? Zero dollars, plus excuses about wedding chaos and raising a 7-year-old niece.

Then mom wires a hefty wedding chunk to the younger sister’s account—”just forward it”—since she can’t locate the bride’s details. Instead of hitting send, the lender keeps it as partial offset. Mom cries theft; sister rages. The lender digs in, insisting it’s fair game against the massive unpaid loan.

‘AITAH for taking my sister’s wedding money that my mom gave me to transfer to her?’

The loan originates from crisis and reluctant trust:

Repayment stalls amid confrontation:

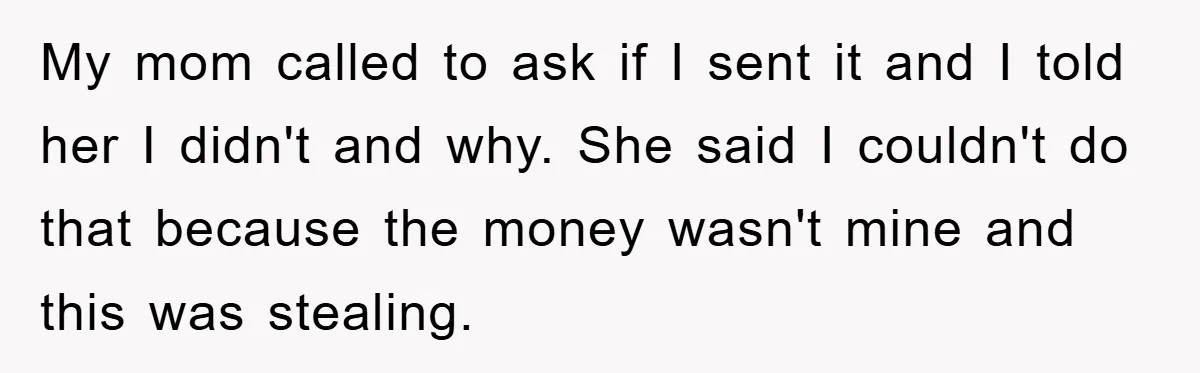

Mom’s transfer becomes the flashpoint:

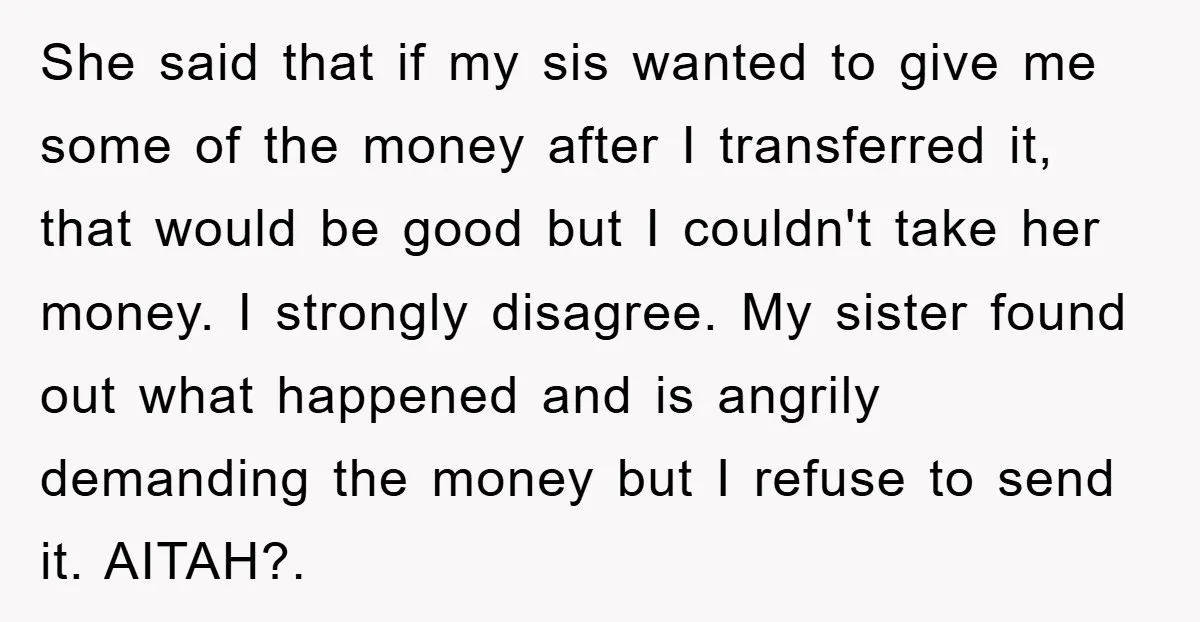

Fallout erupts with accusations:

The crux is intent versus ownership: the sister borrowed with explicit repayment vows, creating a verbal contract. Non-payment after promises, especially redirecting funds to luxuries like weddings, breaches good faith. Keeping mom’s transfer as offset feels like vigilante justice—morally gray, legally dicey.

Mom’s angle holds water; she designated the funds for a specific purpose, making the younger sister a conduit, not owner. Diverting it without consent edges into conversion. Yet the lender’s frustration is valid—lending to serial defaulters invites this mess. Financial therapist Amanda Clayman advises: “Never loan what you can’t gift; treat it as gone to preserve relationships.”

Legal experts note verbal loans under $10K (varies by jurisdiction) are enforceable with evidence like texts or transfers. Small claims court could recover the original sum, potentially garnishing wedding gifts. Mom’s workaround—bypassing direct transfer—raises eyebrows; apps like Zelle exist for a reason.

Solutions: Document everything, file in small claims for the full loan minus kept amount as credit. Cut future lending; suggest sister downscale the wedding or take formal loans. Family therapy could unpack enabling patterns—mom’s role fuels the cycle. Bottom line: ESH lightly, but the lender’s move, while theft-adjacent, spotlights deeper entitlement issues worth addressing formally.

Check out how the community responded:

Buckle up, money-drama lovers—the thread exploded into a mix of “keep it!” cheers and “technically theft” lectures!

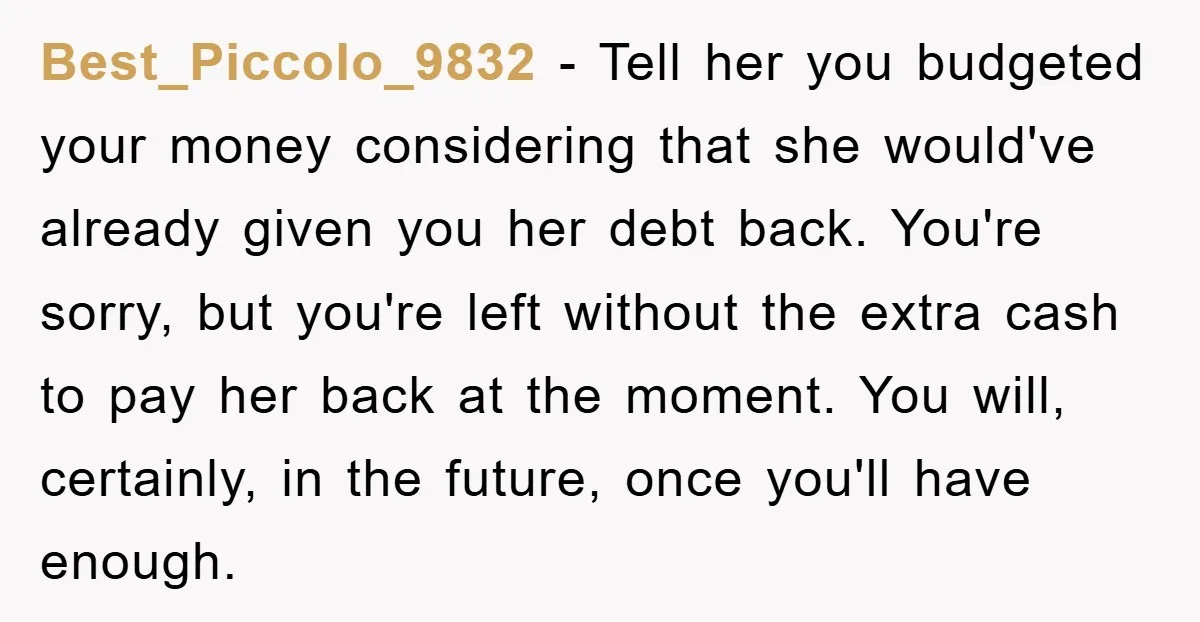

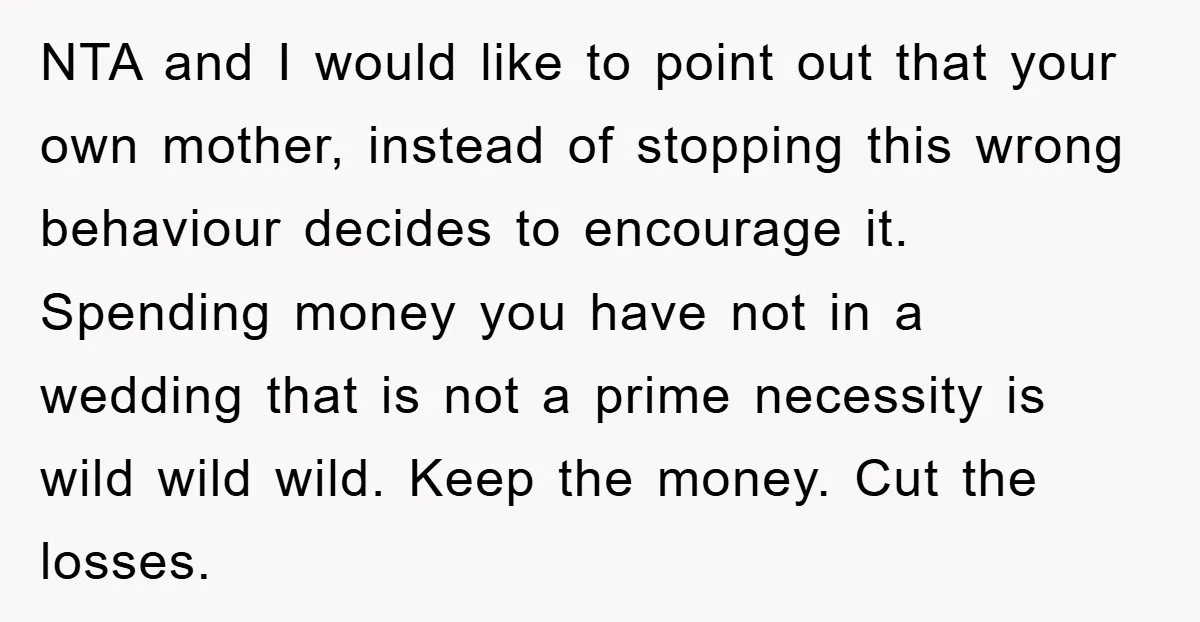

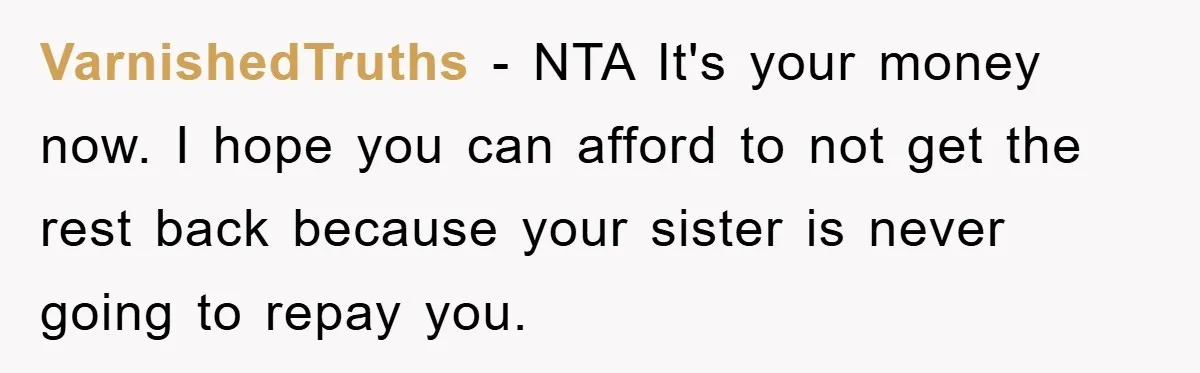

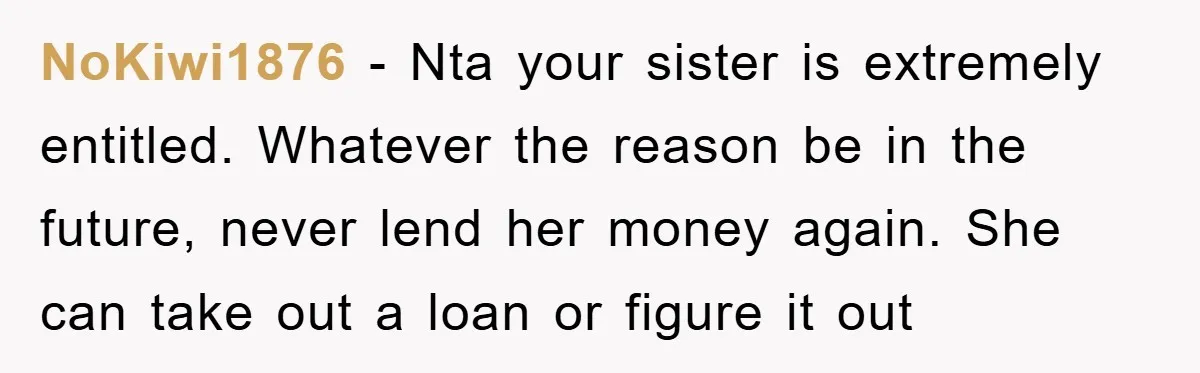

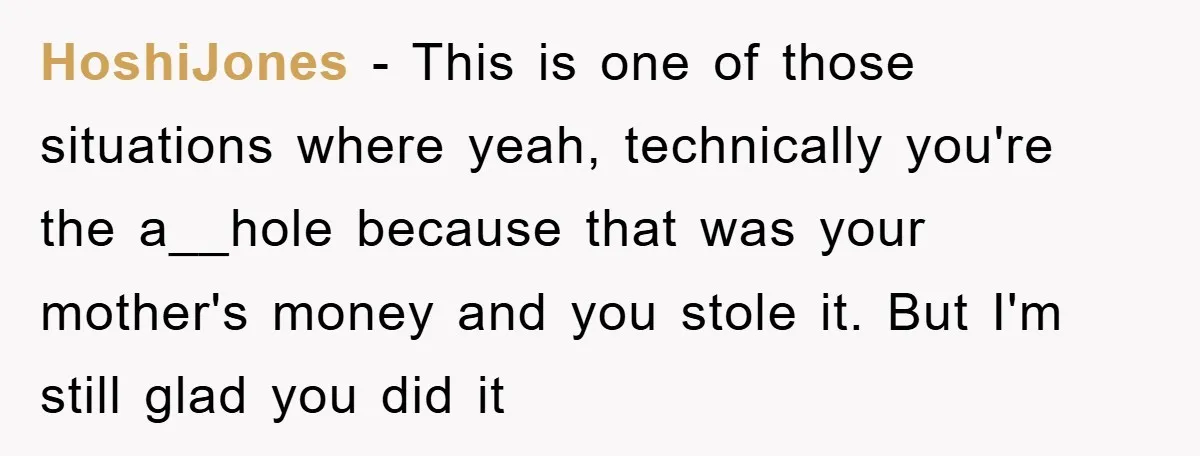

Most folks sided with the lender, praising the offset as sweet justice against a deadbeat.

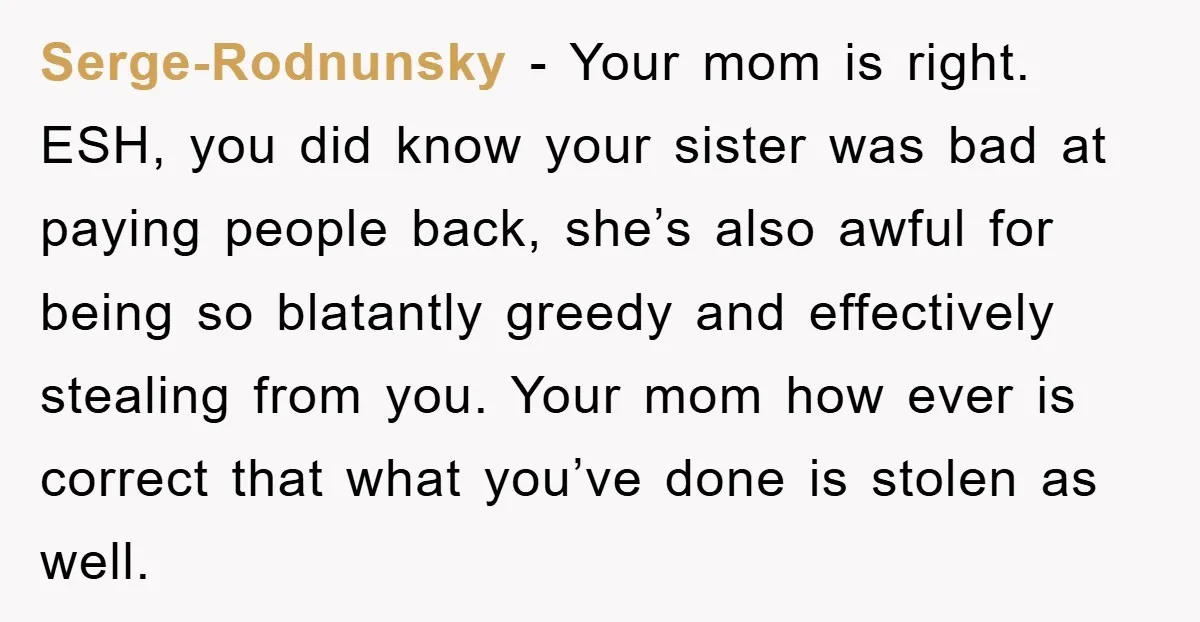

A vocal chunk called technical theft but secretly rooted for the lender anyway.

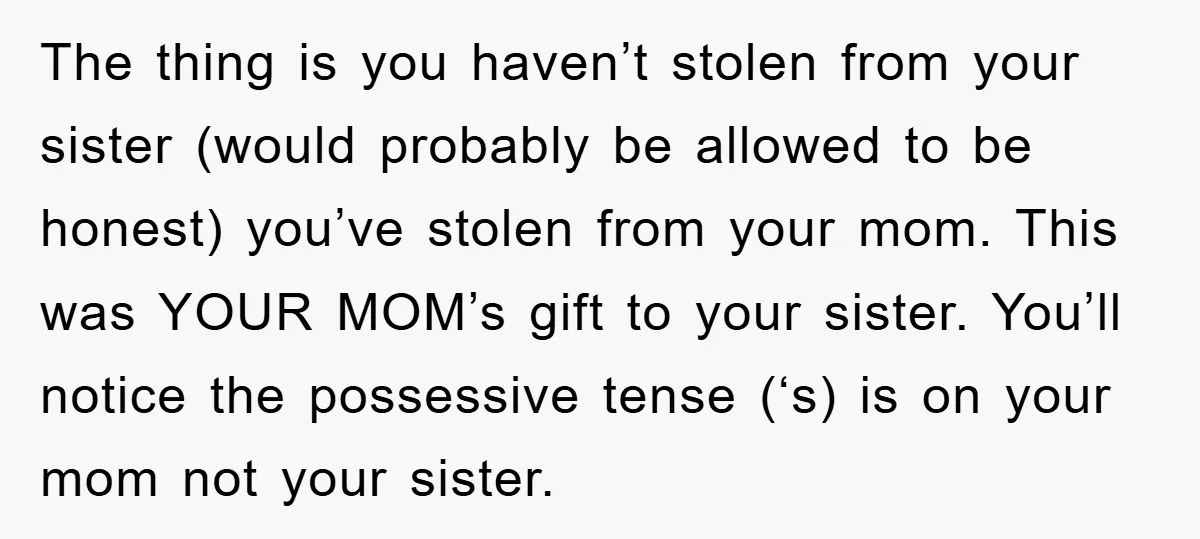

Sharp eyes questioned the setup and advised legal muscle.

![[Reddit User] − #TALK TO A LAWYER GIRL](https://en.aubtu.biz/wp-content/uploads/2025/10/wp-editor-1761898025488-9.webp)

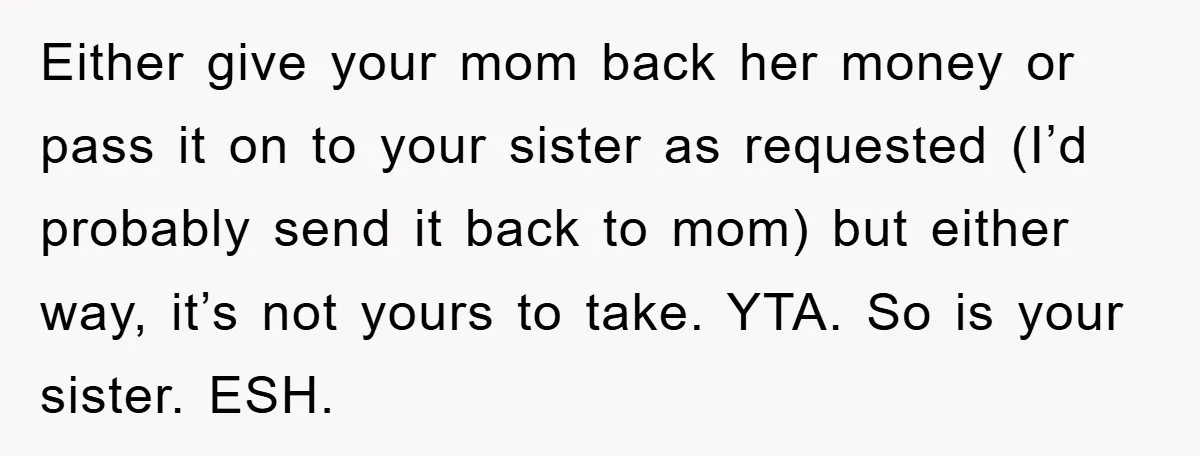

A couple pushed for court and roasted wedding priorities.

Boiled down, it’s a tangled web of broken promises, enabling moms, and one bold offset that screams “lesson learned.” The hive mind leans NTA for the spirit but flags the theft tech—go legal, not vigilante.

Ever reclaimed a loan sideways? Would you sue sis or ghost the family fund? Spill your cash-clash sagas below—we’re popping corn for the replies.