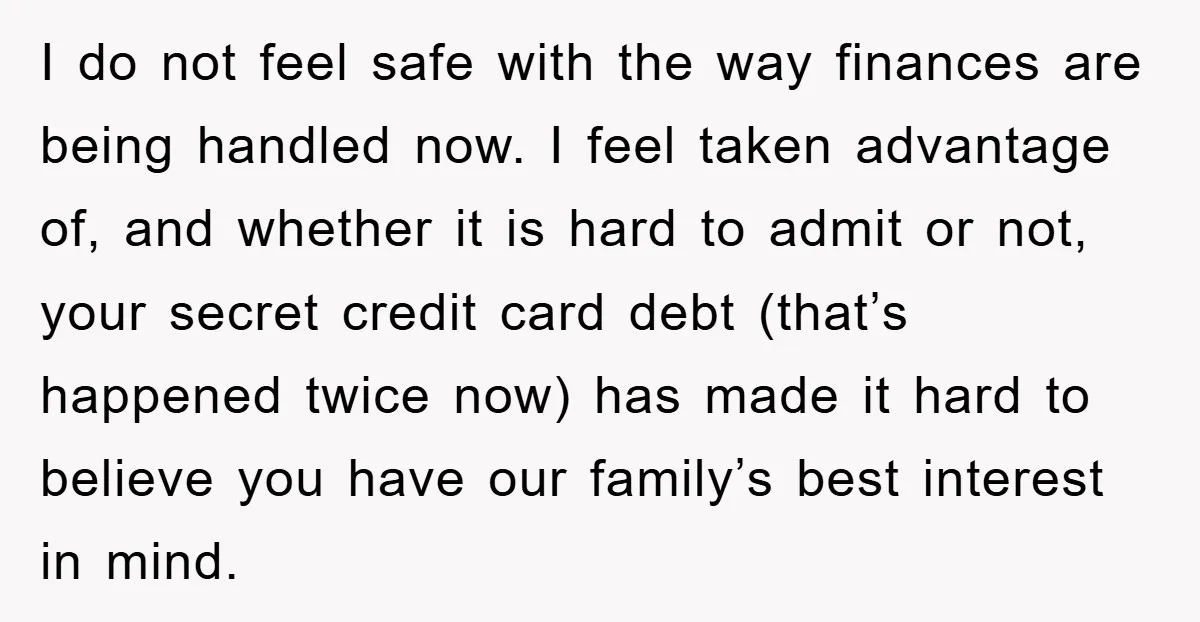

AITAH for not wanting to fund my stepkids savings accounts?

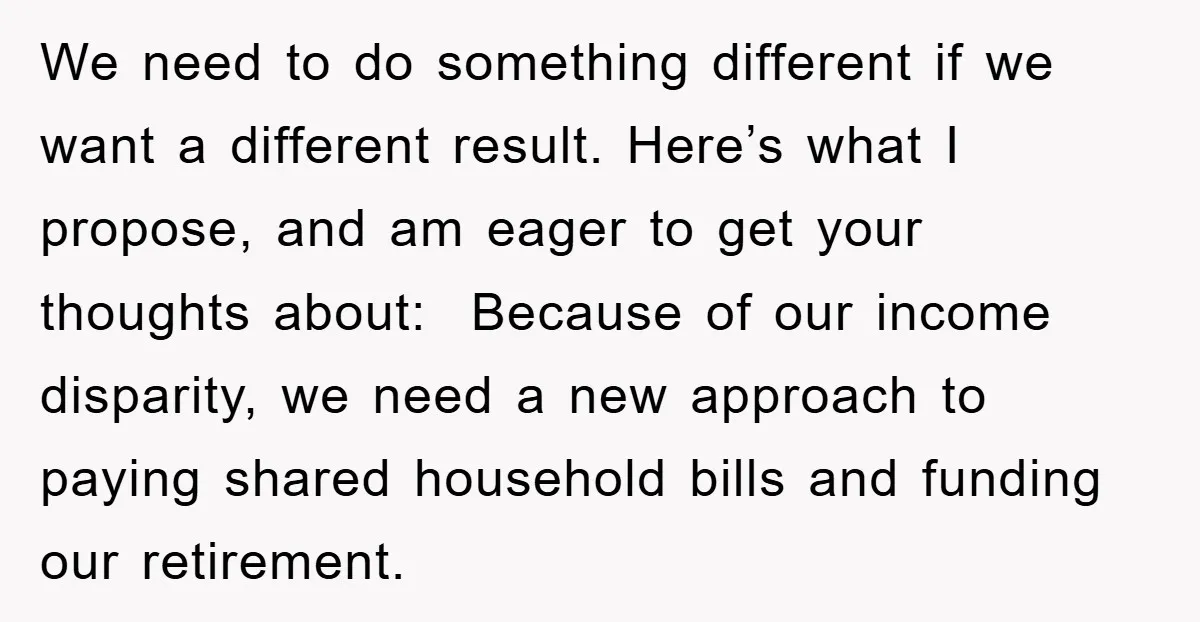

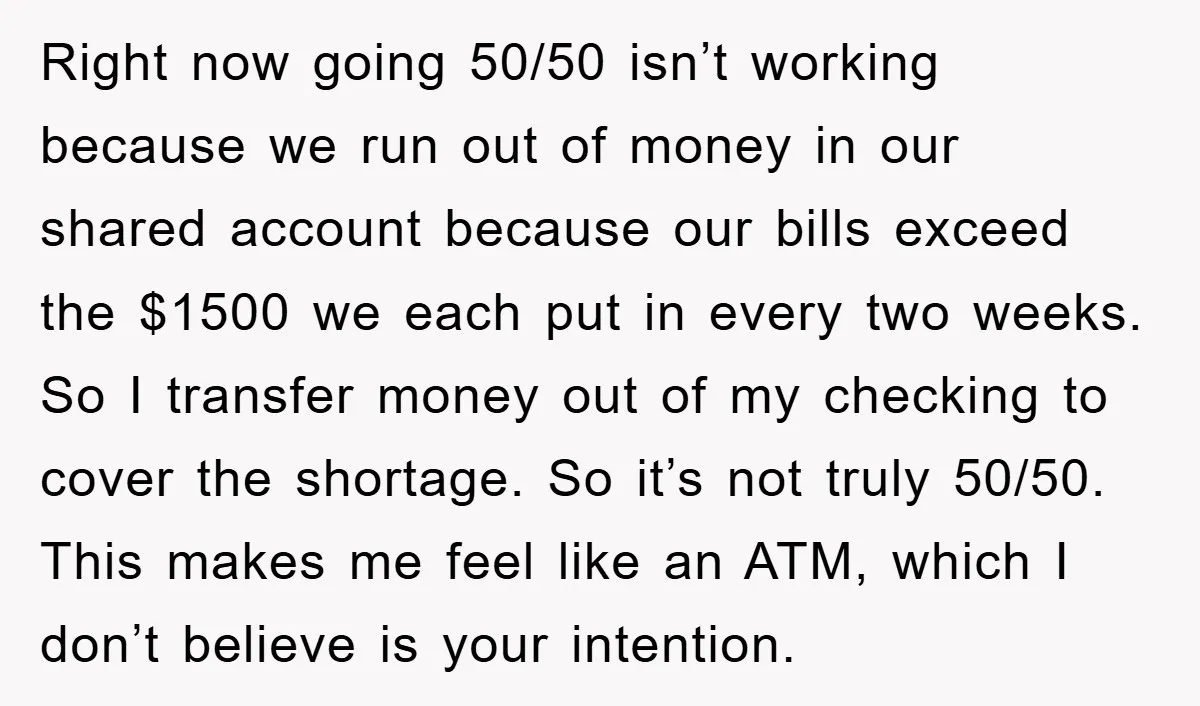

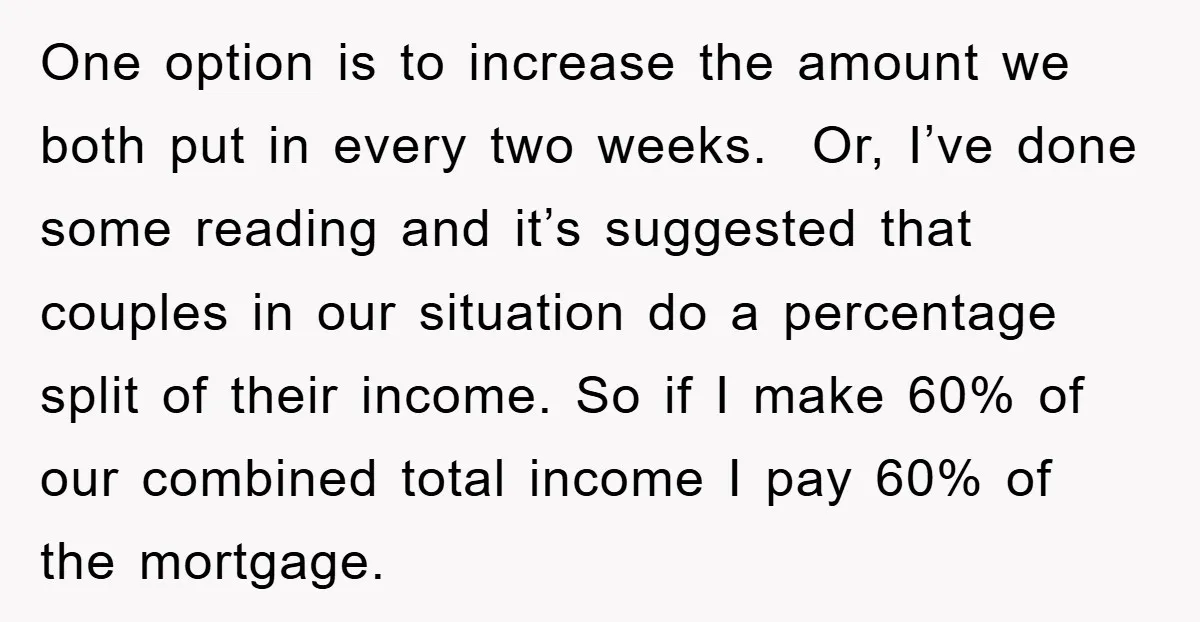

A high-earning entrepreneur refuses to bankroll college funds for her teenage stepkids now that her husband suddenly wants three maxed-out investment accounts—one for each child, including their new baby. She already covers most household shortfalls despite equal biweekly deposits, plus twice paid off his secret credit-card debt.

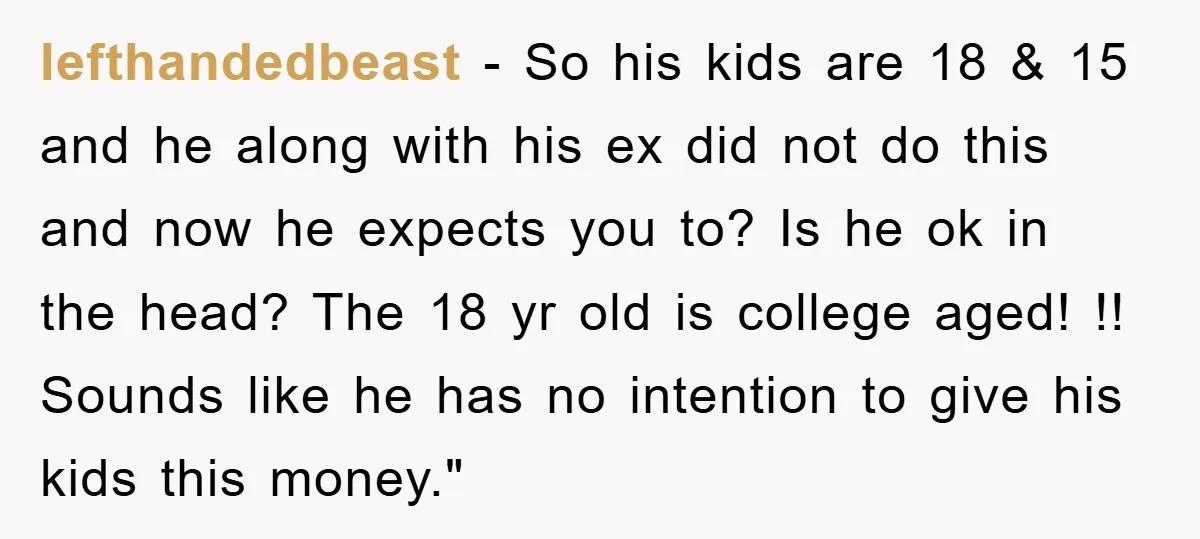

What makes the story more complicated is the timing: the stepkids are 18 and 15, never had savings before, yet the moment her income stabilizes their lifestyle, funding them becomes urgent. She sees exploitation; he frames it as fatherly duty. With trust shattered and a newborn in the mix, she draws a hard line: her money, her bio daughter only.

‘AITAH for not wanting to fund my stepkids savings accounts?’

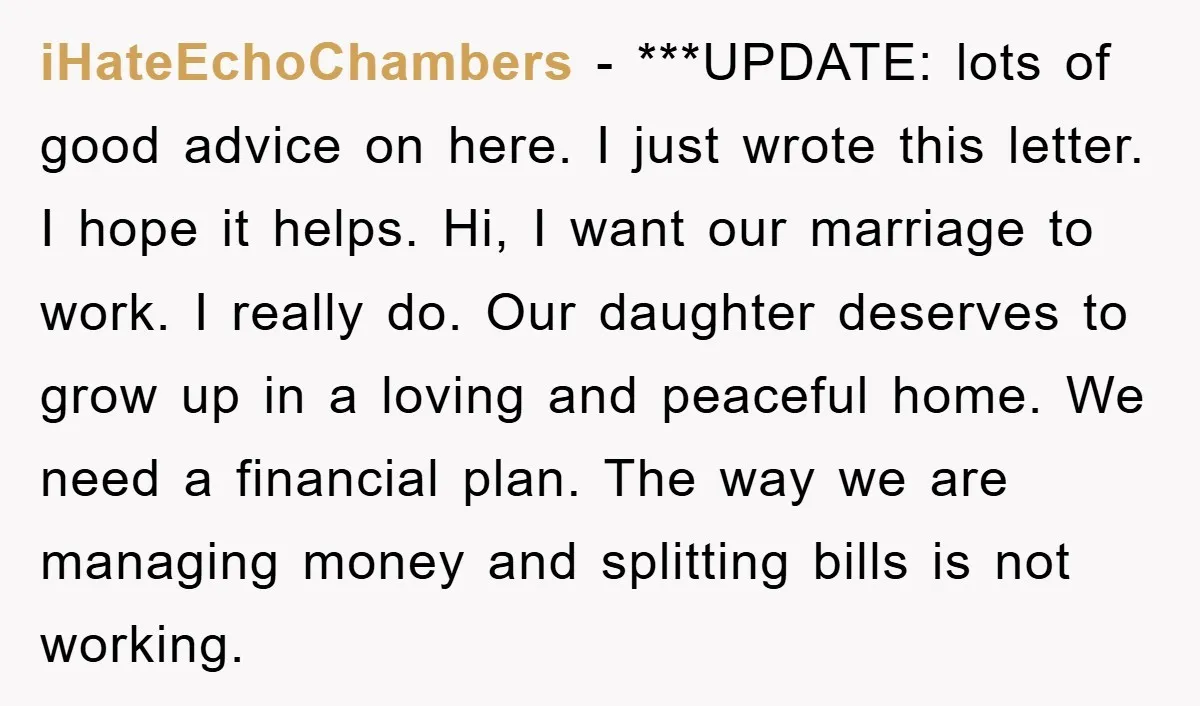

A new mom balks when her husband announces college funds for all three kids using mostly her cash.

Income disparity and past financial betrayal set the stage for tonight’s bombshell.

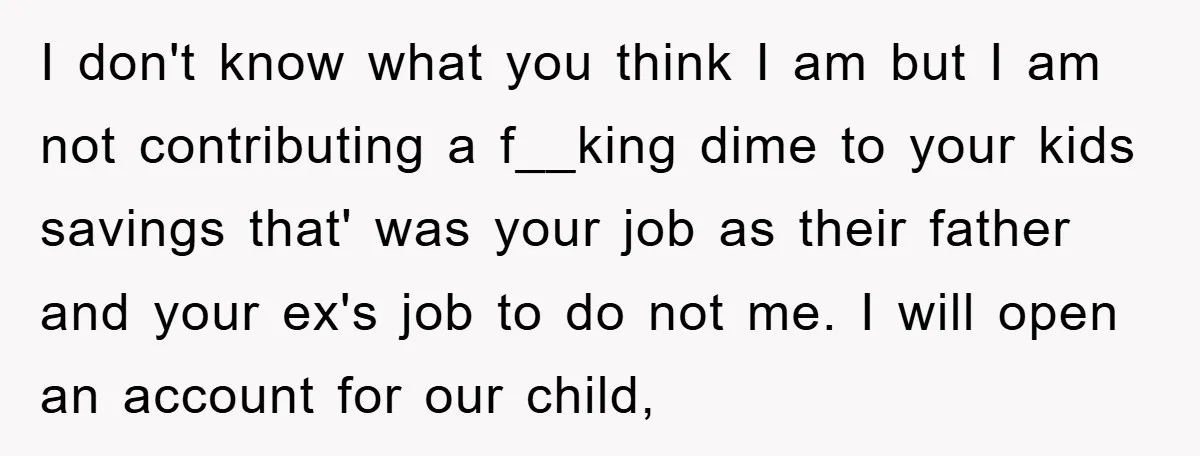

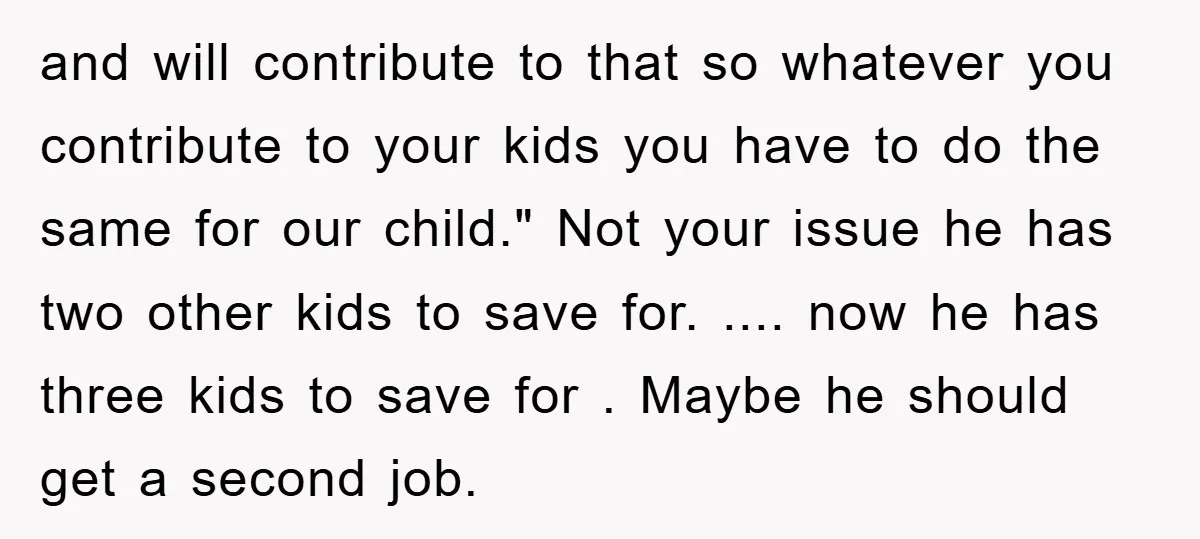

The savings plan reveal triggers an immediate shutdown—she won’t subsidize his prior kids.

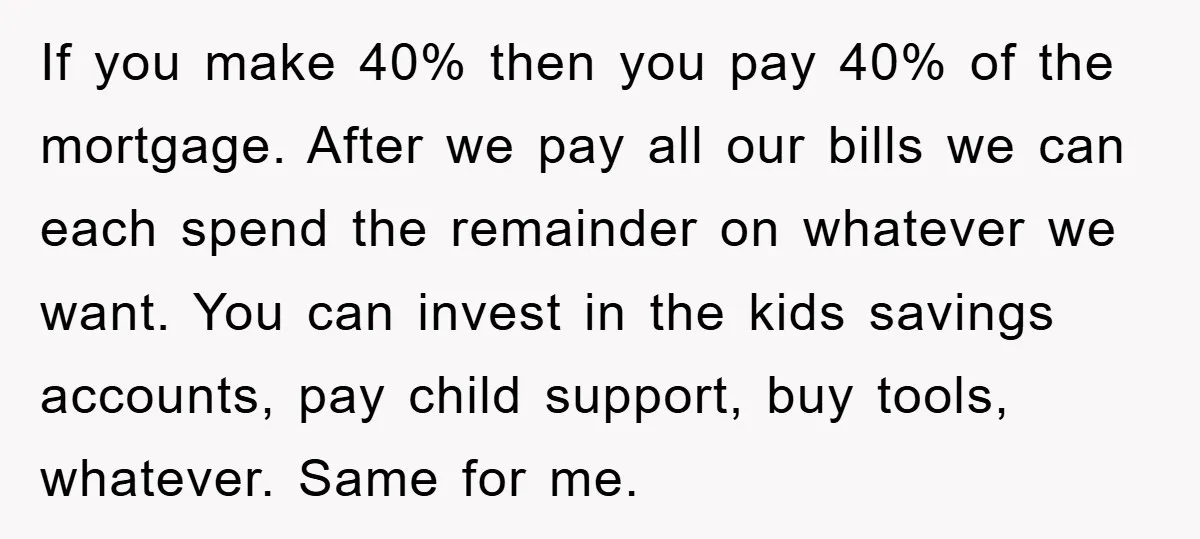

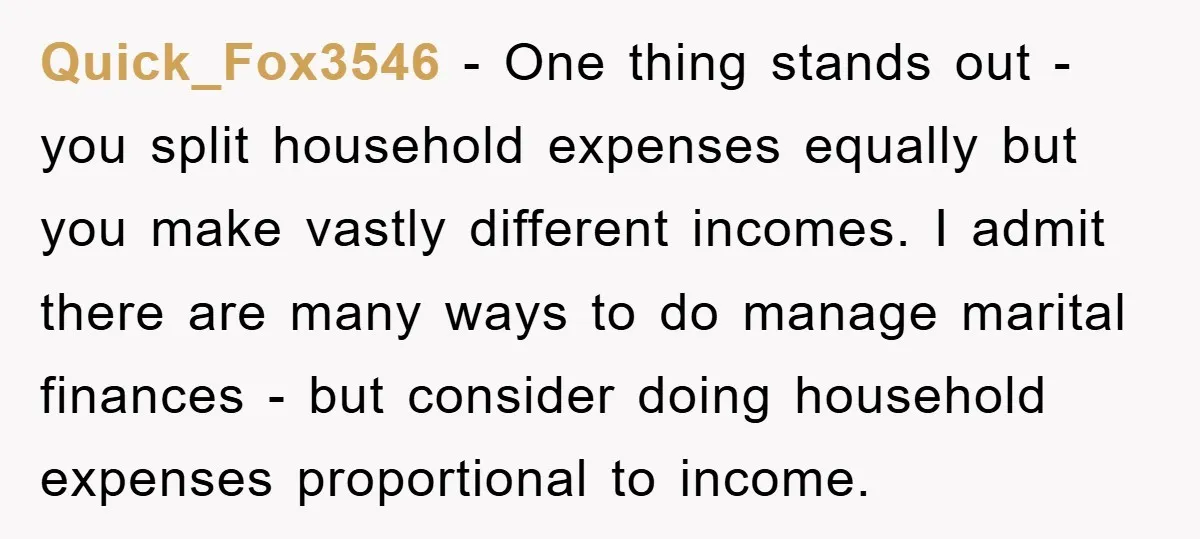

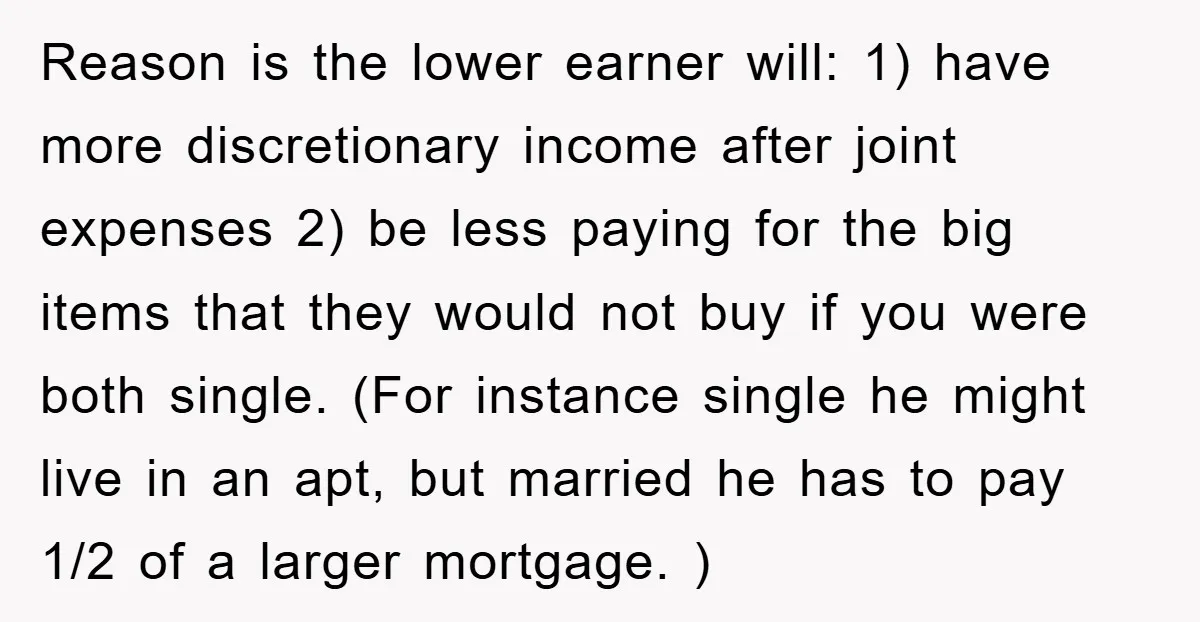

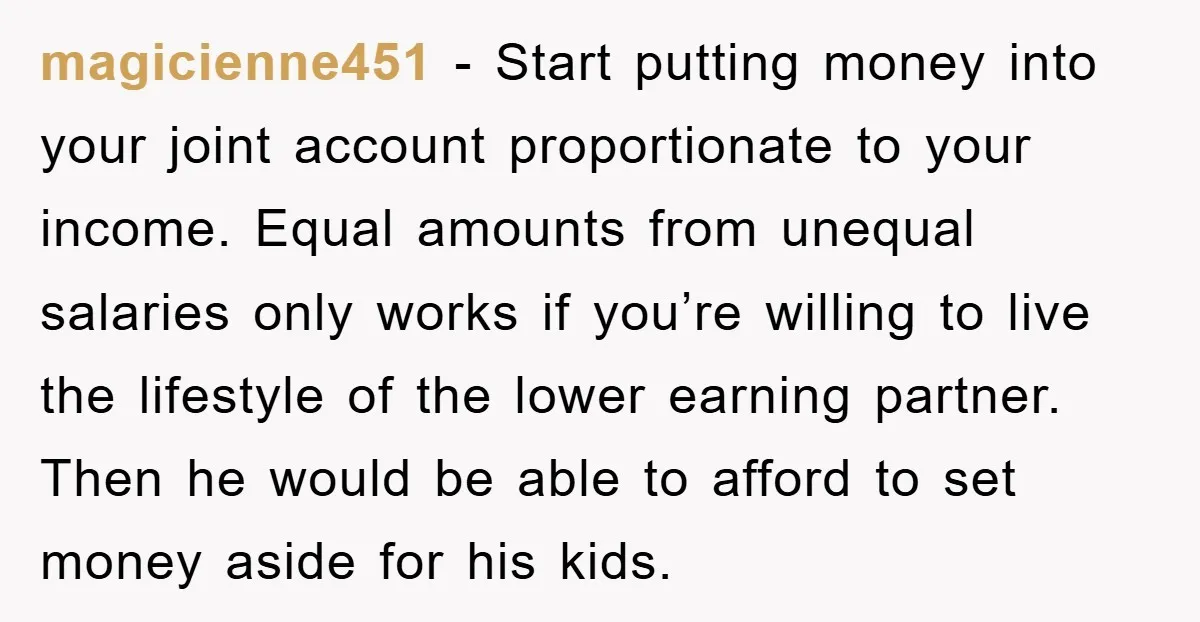

Refusing to finance stepchildren’s futures isn’t cold—it’s boundary-setting after repeated financial deception. Secret debt twice in two years signals deeper irresponsibility; announcing three maxed accounts without consultation is entitlement disguised as parenting. Her higher income doesn’t obligate equal gifting across all kids—stepkids have two bio parents already.

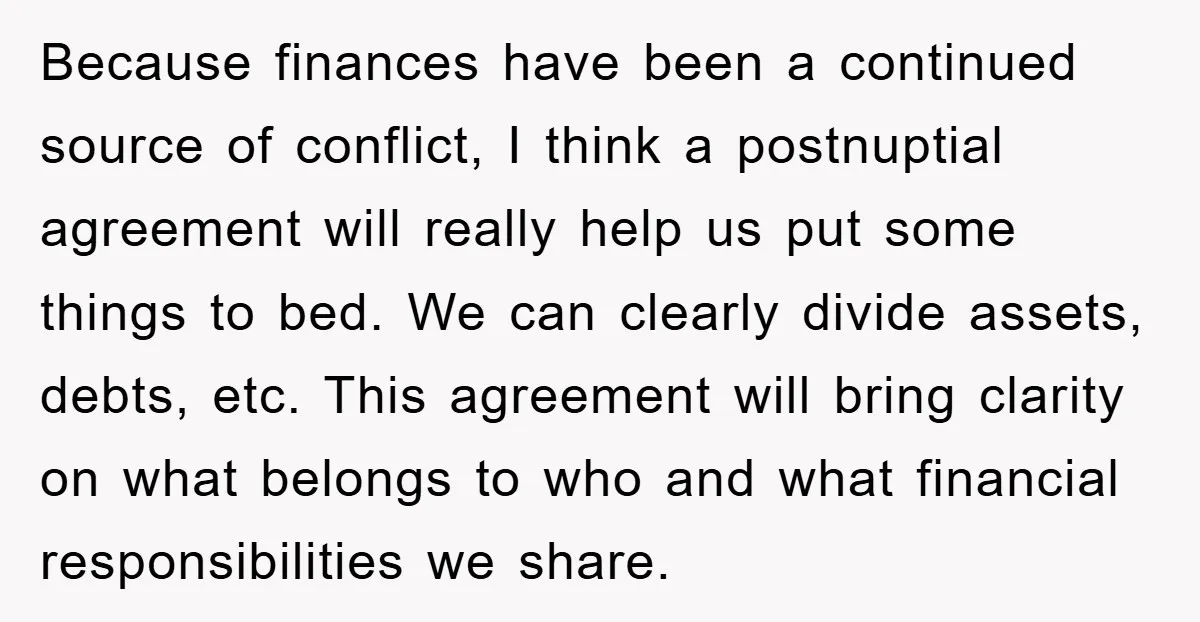

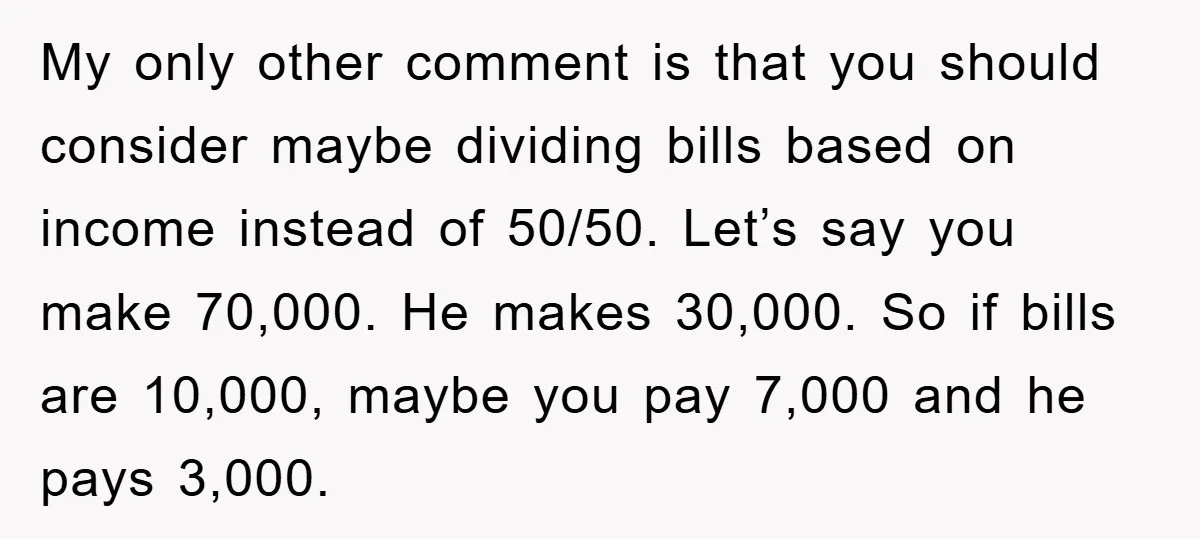

Some argue marriage merges finances fully, and excluding prior children breeds resentment. Yet equal biweekly deposits already strain her; proportional splits would free his leftover cash for his kids without touching hers. Trust erosion demands legal safeguards—postnups, separate accounts—before another “surprise” expense.

Financial therapist Amanda Clayman told Business Insider, “When one partner earns significantly more, proportional contributions prevent resentment; secret spending is financial infidelity—treat it with the same gravity as emotional cheating.” Transparency and separate child-fund streams are non-negotiable.

Let’s dive into the reactions from Reddit:

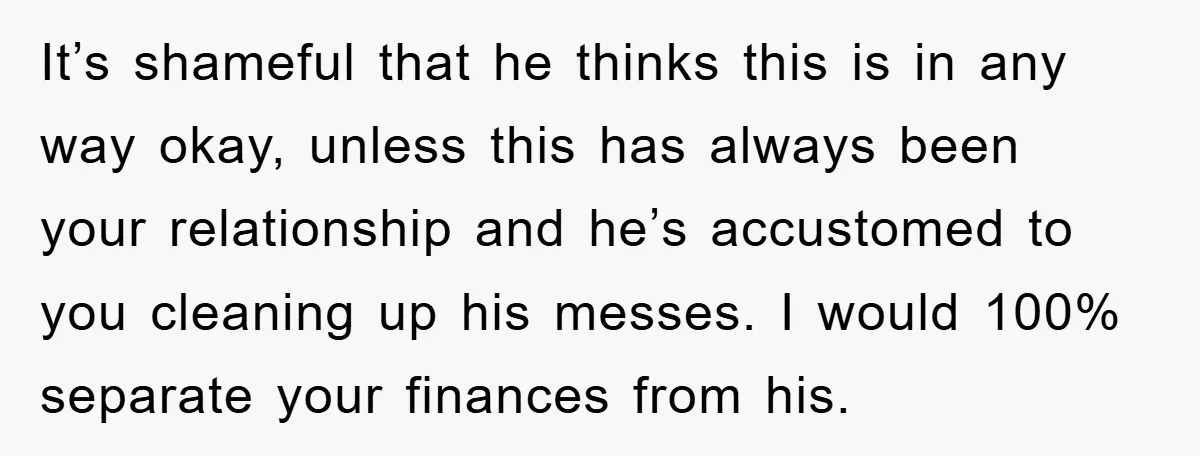

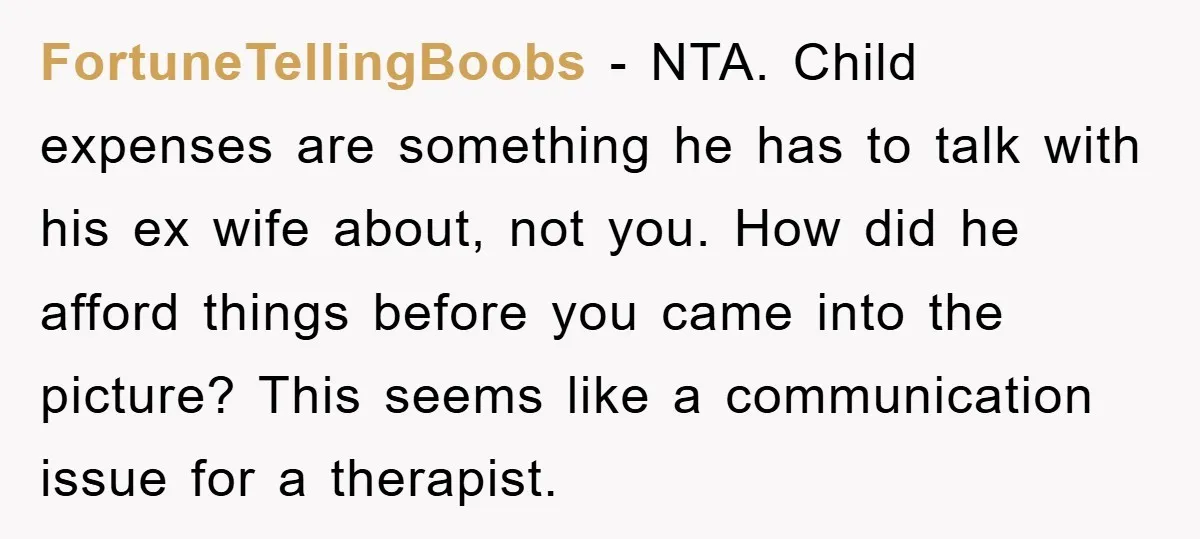

Most users scream “run,” urging lawyers, postnups, and proportional bills to protect her assets.

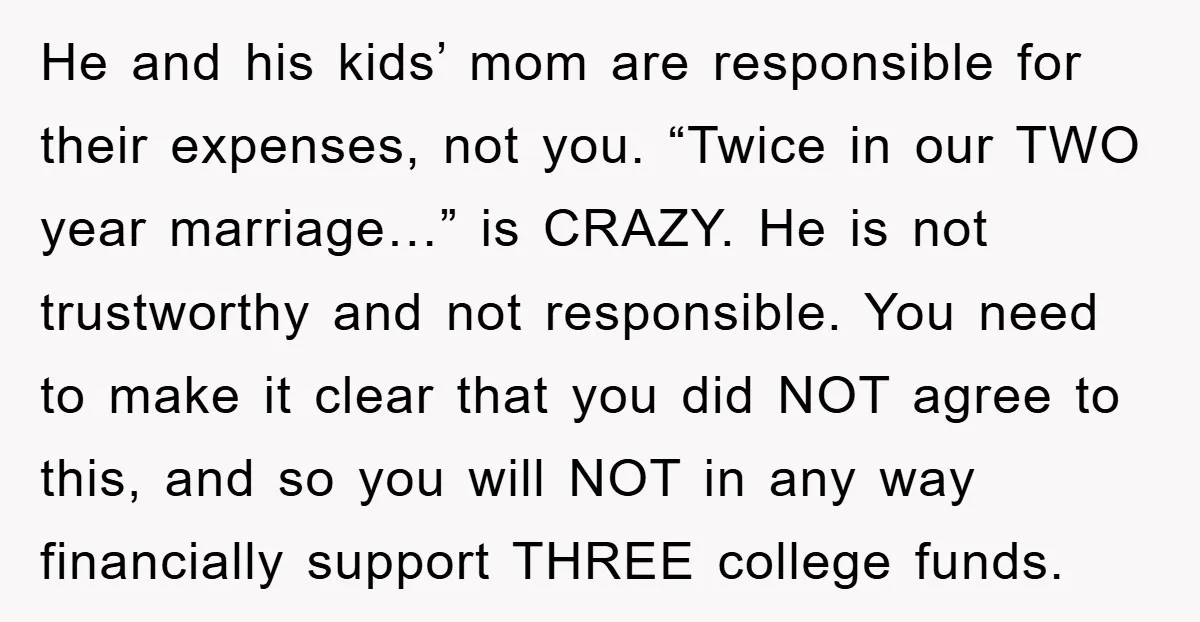

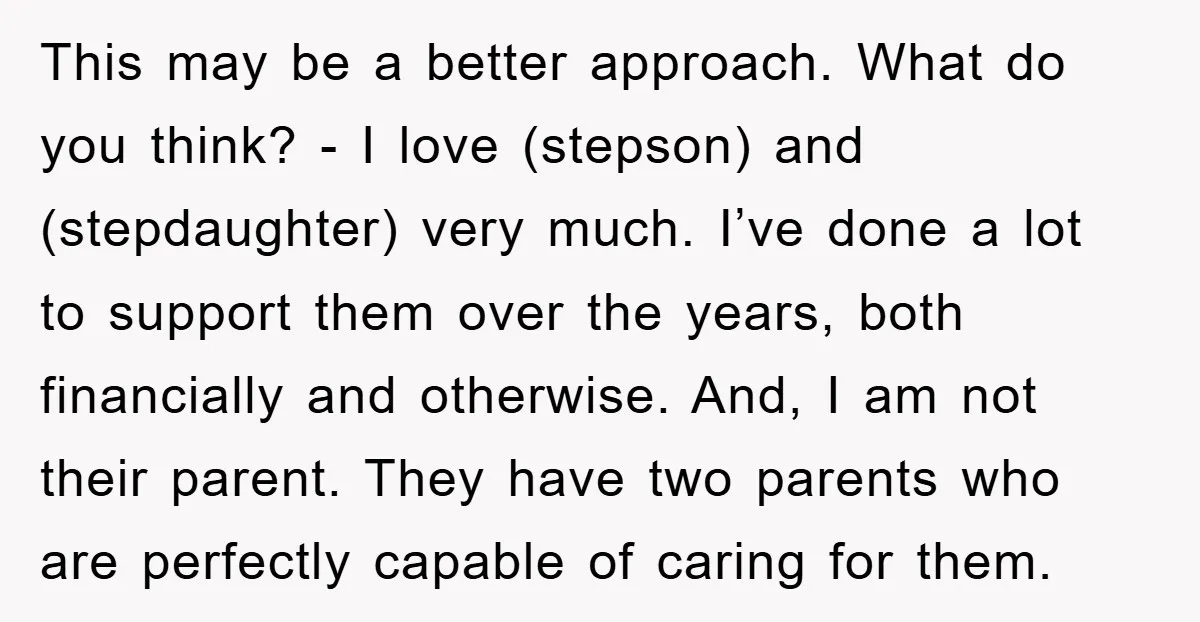

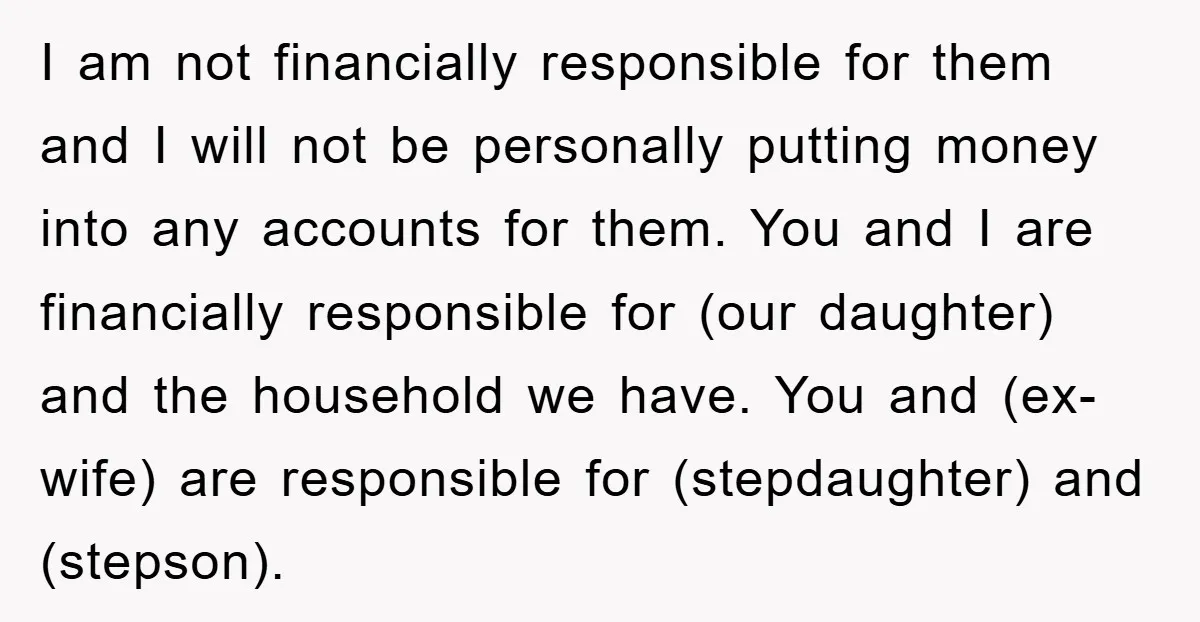

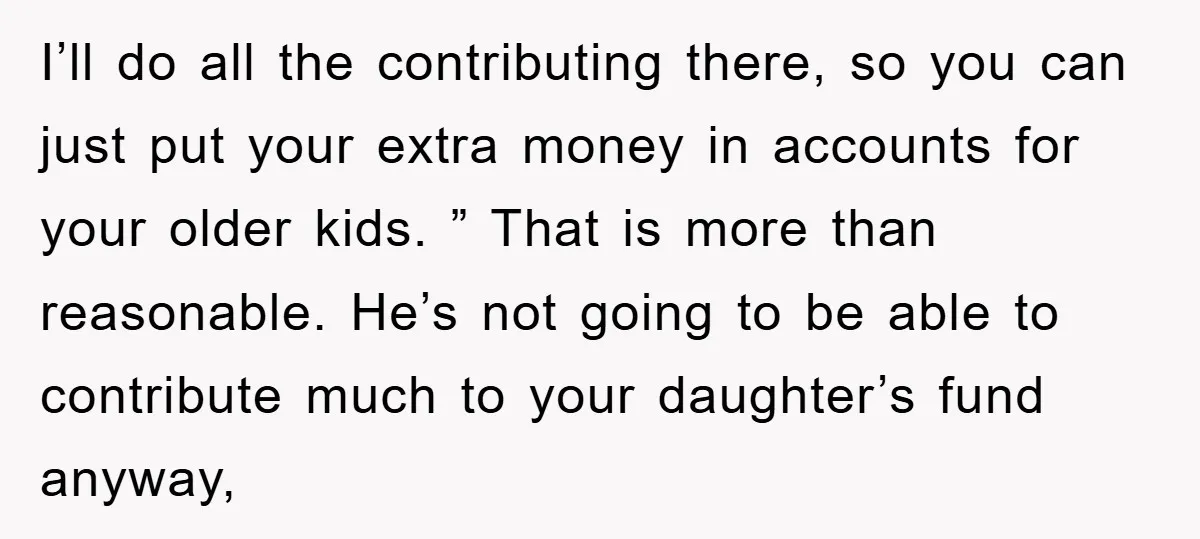

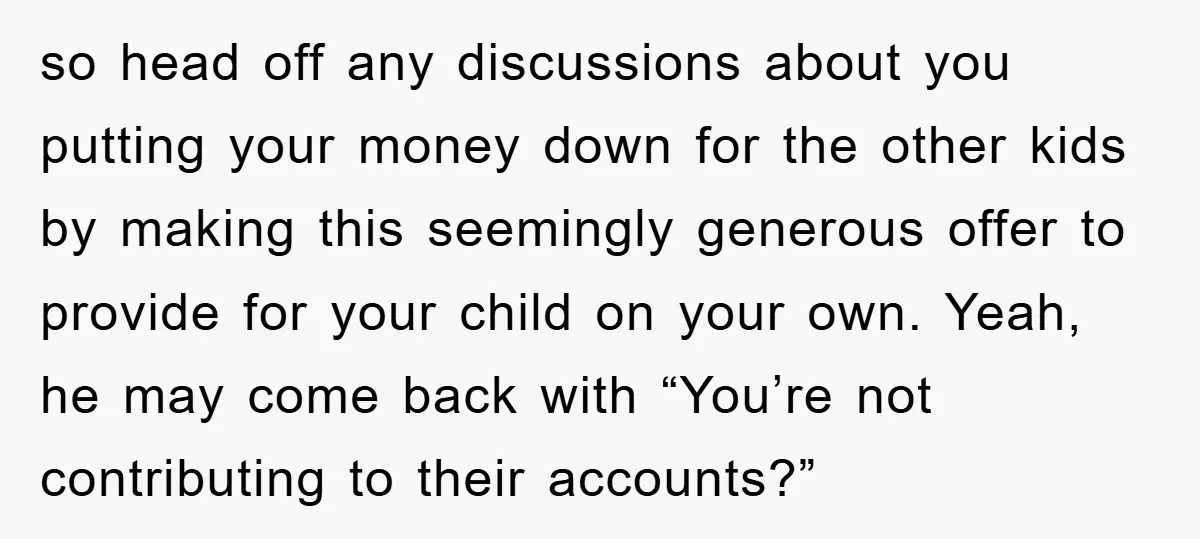

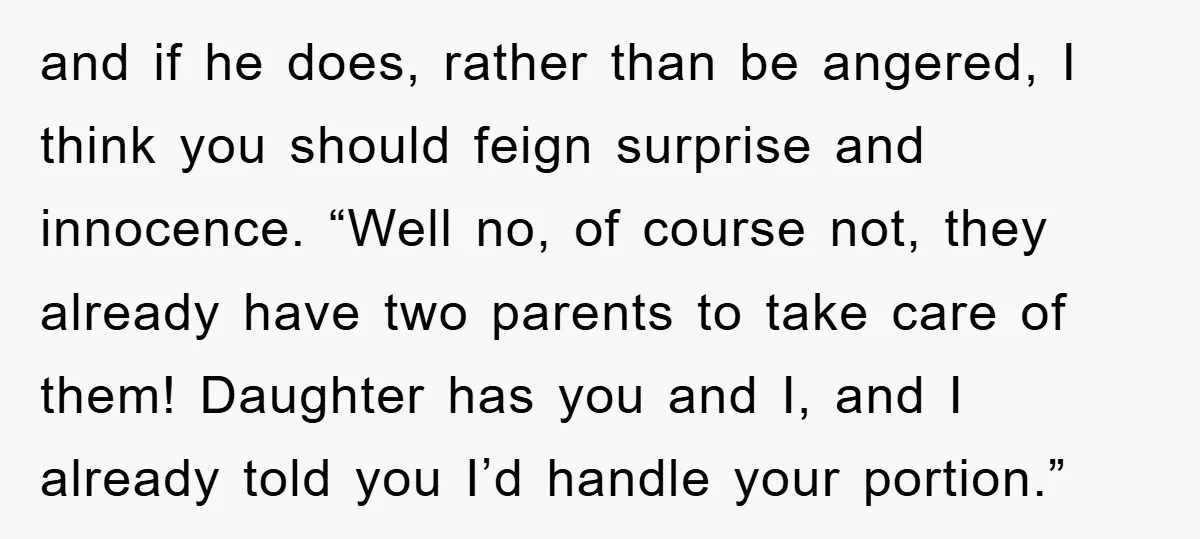

Several applaud the OP’s drafted letter and suggest proportional splits plus ironclad protections.

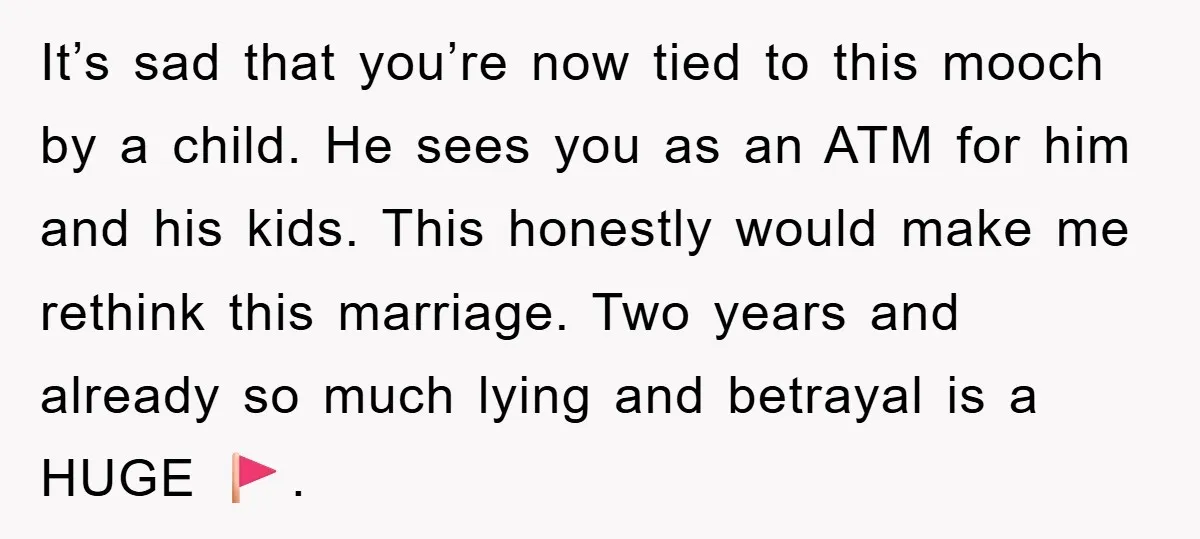

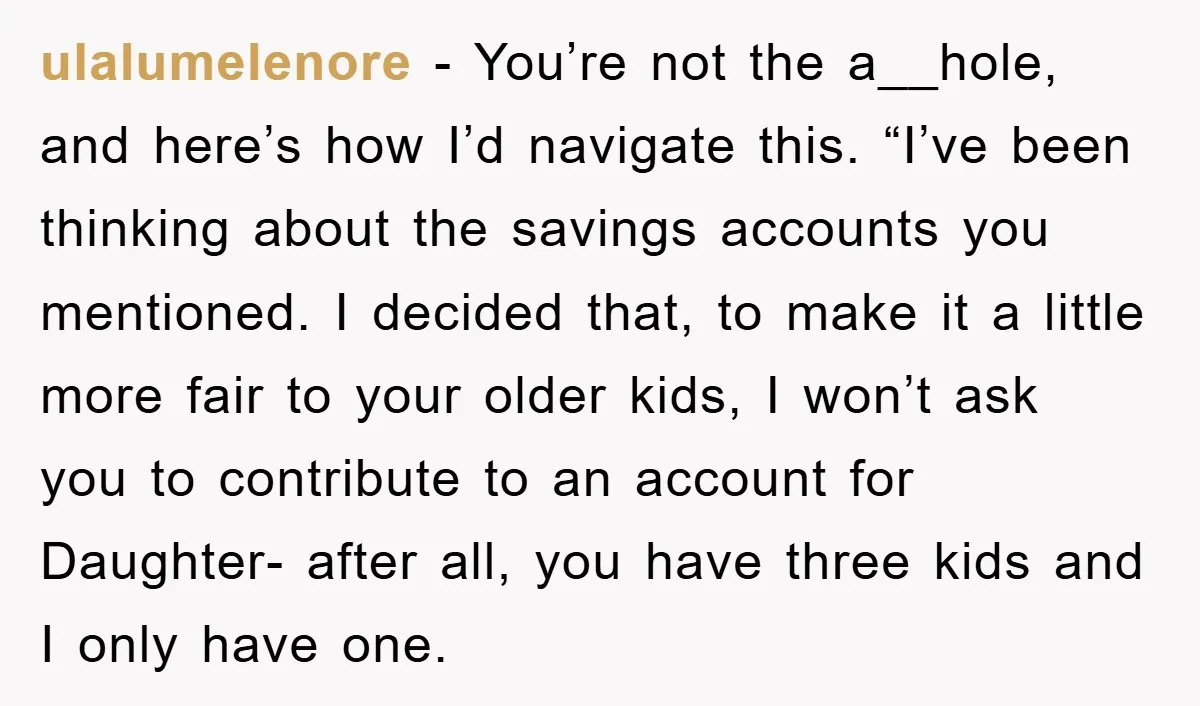

A few offer clever scripts to flip the fairness narrative and lock him out of her child’s fund.

The wife safeguards her earnings for her newborn while her husband—fresh off secret debt scandals—expects her windfall to seed college funds for his teens. Equal deposits mask her subsidizing everything; proportional splits and postnups emerge as the community’s lifeline. Trust hangs by a thread, but clear contracts could salvage the marriage.

When income gaps are wide and prior kids exist, should finances stay fully merged or rigorously separated? Have you used postnups to protect a business or bio child—did it save or sink the relationship?