AITAH for not giving my daughter her college fund money?

A dedicated parent who saved nearly $200,000 for their daughter’s education is now facing backlash after denying access to the fund. The 17-year-old senior announced she’s skipping the traditional four-year college path in favor of a gap year, work, and self-discovery—which her mom fully supports. The conflict arose when the teen asked for the money anyway to buy a new car and cover “other things.”

The disagreement boils down to the purpose of the savings versus entitlement. While the daughter sees the fund as hers regardless of its intended use, the parent insists it remains earmarked for future education, protecting both the money and her daughter’s long-term options.

‘AITAH for not giving my daughter her college fund money?’

The parents built a substantial education fund over nearly two decades.

She revealed plans to skip college for now and asked for the money.

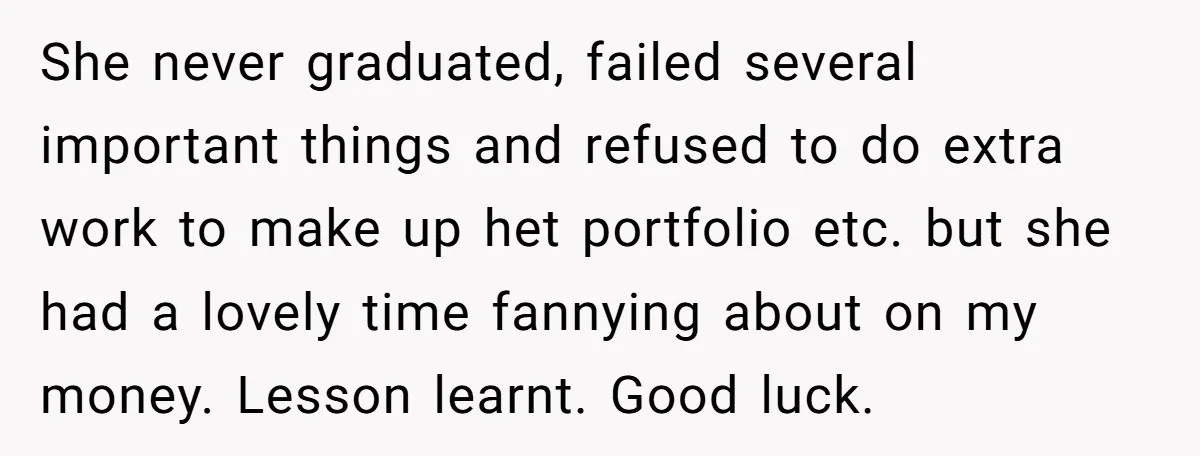

The mom refused, leading to claims of entitlement from her daughter.

This case underscores the difference between conditional parental gifts and outright entitlement. The fund was explicitly created for postsecondary education, not general spending. Releasing a large sum to a teenager risks rapid depletion on depreciating assets like cars or short-term enjoyment, potentially leaving her without resources if she later pursues schooling or faces unexpected needs.

What makes the story more complicated is the daughter’s sense of ownership over money she didn’t earn, combined with the allure of immediate gratification at 17. Many parents in similar positions worry that early access undermines work ethic and financial responsibility. Counterarguments might suggest flexibility if the child shows maturity, but handing over six figures without milestones often leads to regret—for both parties.

Broader trends show rising acceptance of gap years and alternative paths, yet dedicated education funds remain common tools for securing future stability. Holding firm teaches that large financial gifts typically come with purpose-aligned strings, preparing young adults for real-world conditions rather than fostering unrealistic expectations.

These are the responses from Reddit users:

Most users firmly supported the parent, stressing that the money is not the daughter’s to spend freely.

Several highlighted the entitlement issue and potential consequences of releasing the funds.

![[Reddit User] − NTA If she doesn’t go to college that becomes your retirement fund not her car fund.](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1767689360088-5.webp)

A couple kept the tone direct, pointing out risks and parental sacrifice.

The community overwhelmingly ruled the parent not the asshole, agreeing the fund’s purpose is education and releasing it risks wasteful spending while rewarding entitlement. Many praised holding boundaries as responsible parenting that protects both the money and the daughter’s future motivation.

Would you release a college fund for non-educational use during a gap year? How do you teach teens the value of money meant for their future? Have you faced similar demands from your kids—share your stories below.