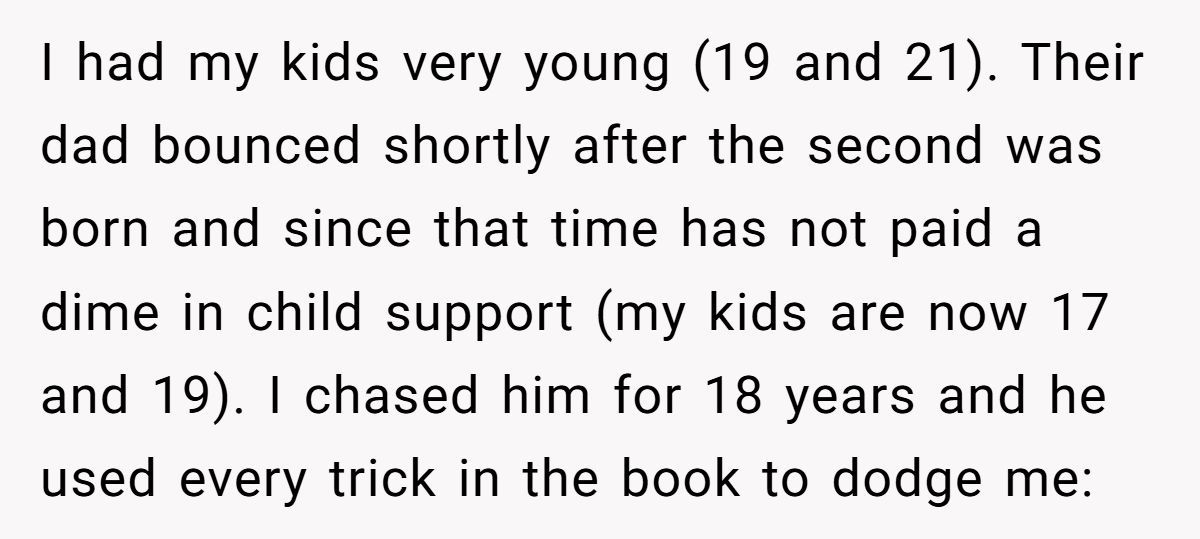

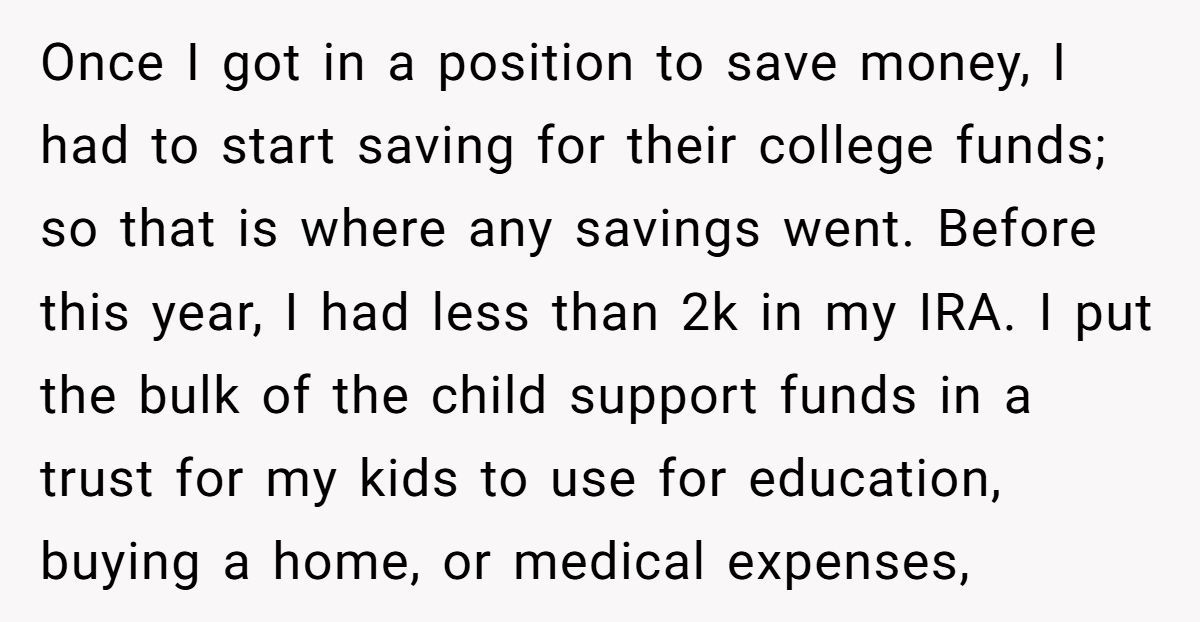

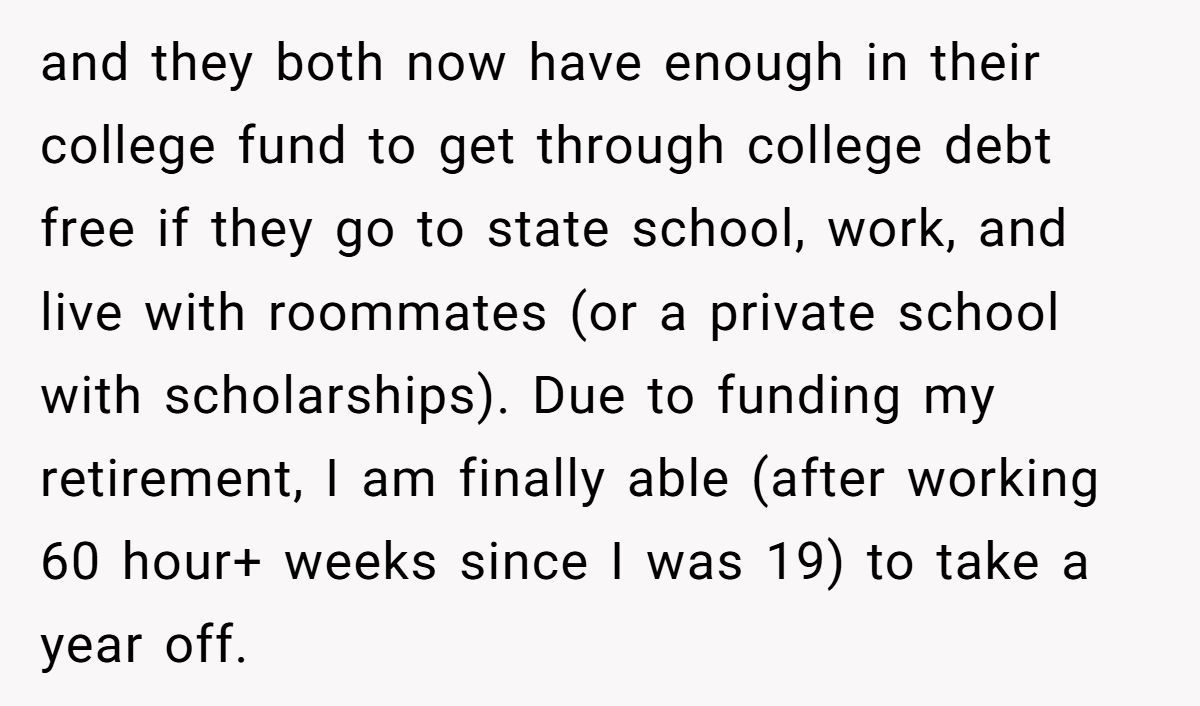

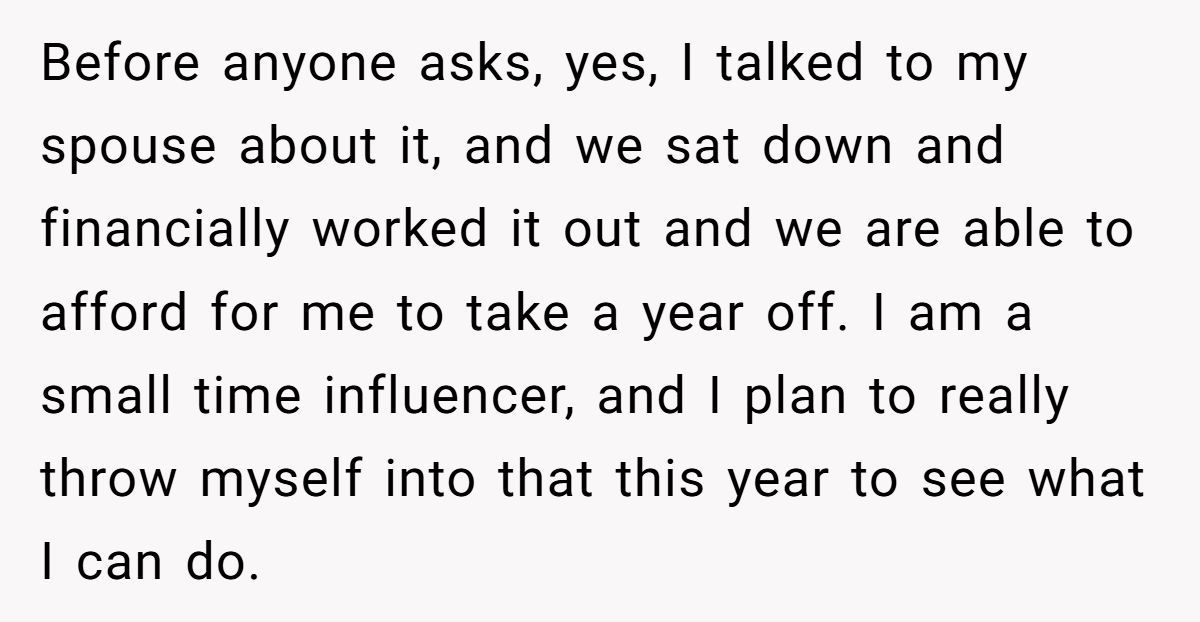

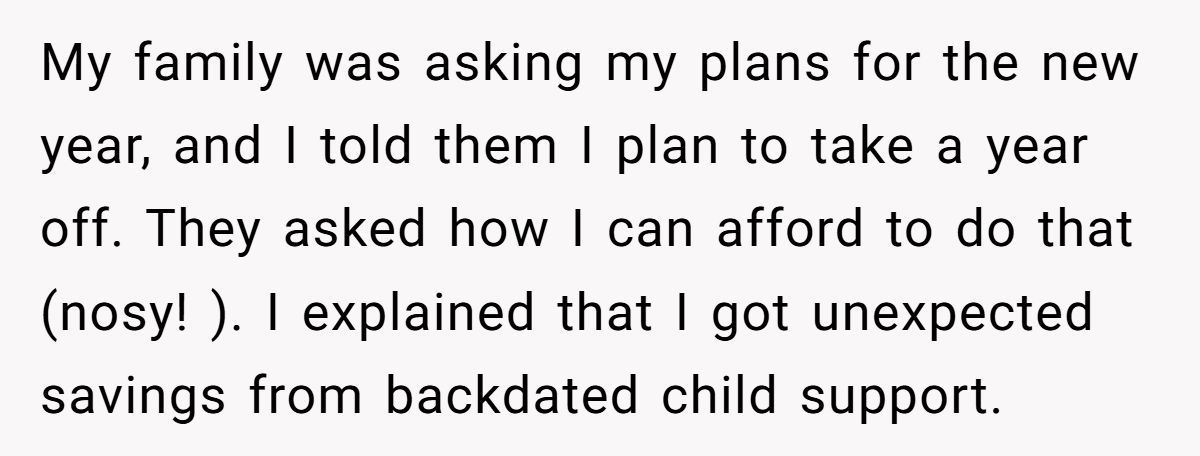

AITA for using my kids child support for my retirement?

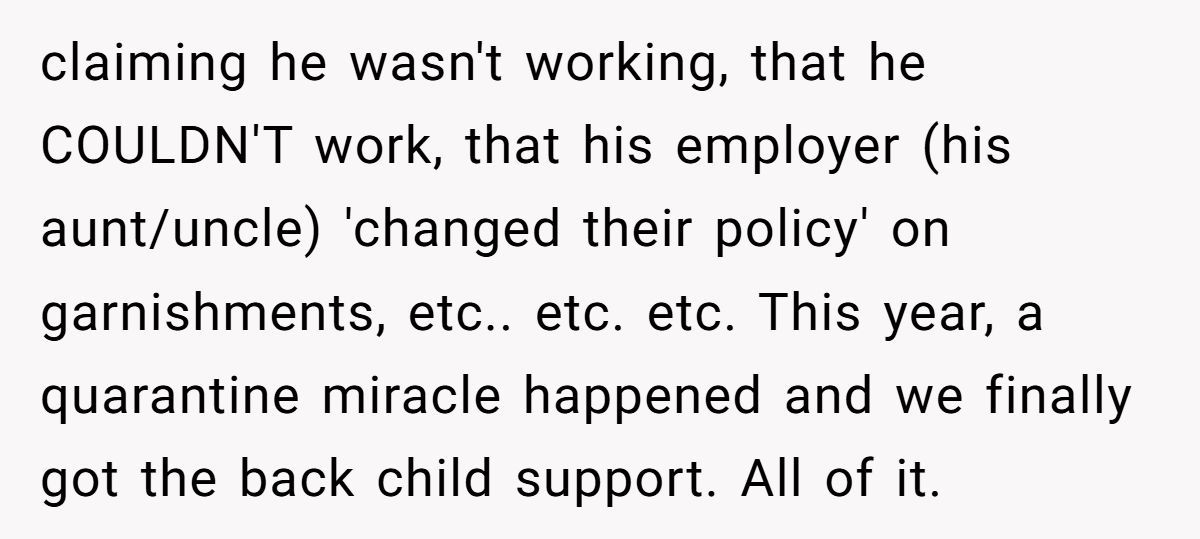

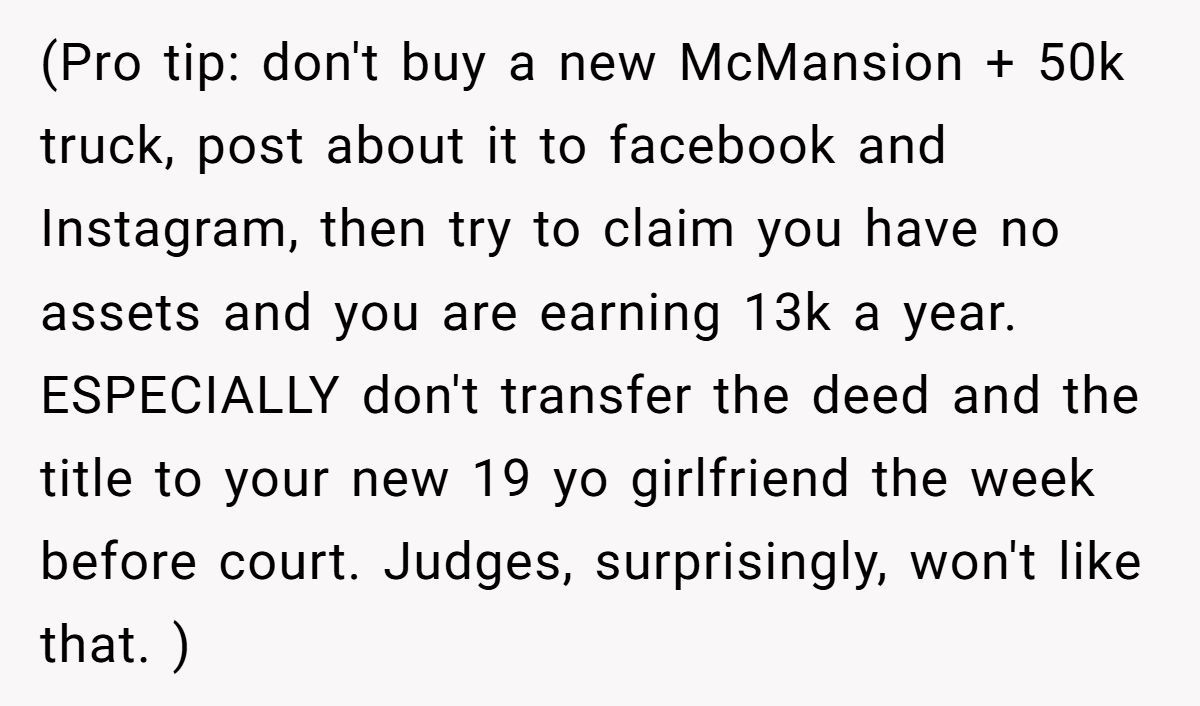

In a world where single parents juggle bills like circus performers, one mom’s story sparks a fiery debate. After 18 years of chasing her ex for child support, she finally hit the jackpot—a hefty sum that could rewrite her future. Picture her, a woman who’s worn thin from working 60-hour weeks, standing at a crossroads: secure her retirement or face the family’s raised eyebrows. Her choice to fund her IRA with part of the backdated child support has tongues wagging and Zoom calls buzzing.

This tale isn’t just about money; it’s about sacrifice, resilience, and the blurry line between self-care and selfishness. With her kids’ futures cushioned by a trust fund, she’s carving out a rare year off to chase her dreams as an influencer. But when family calls her out, is she really stealing from her kids, or just claiming what’s hers?

‘AITA for using my kids child support for my retirement?’

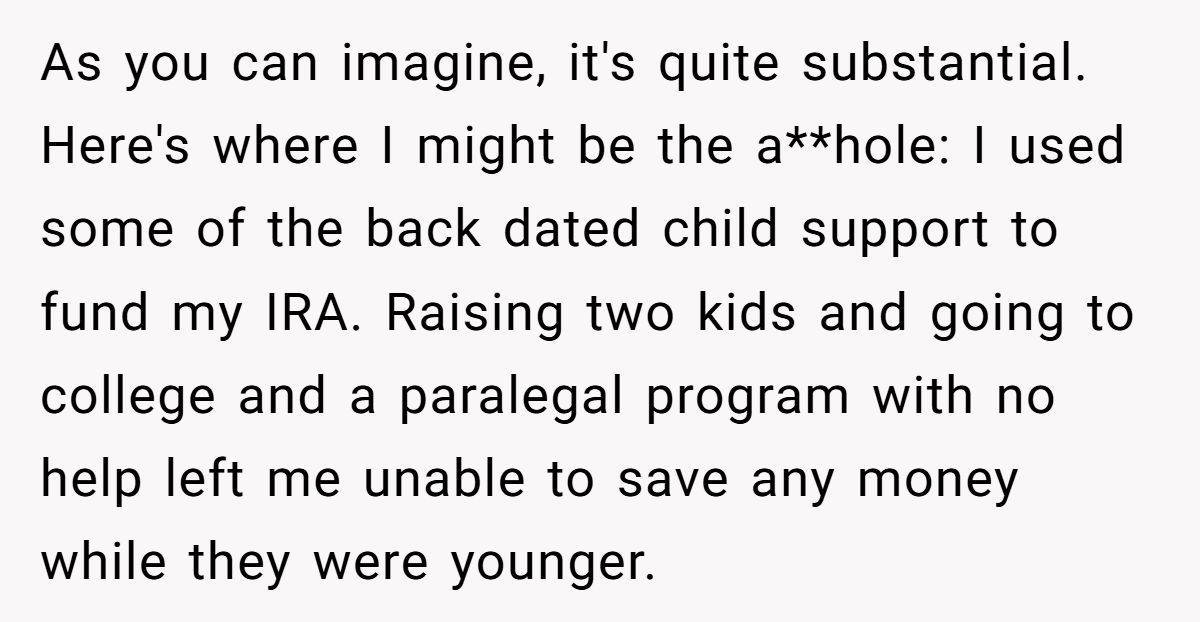

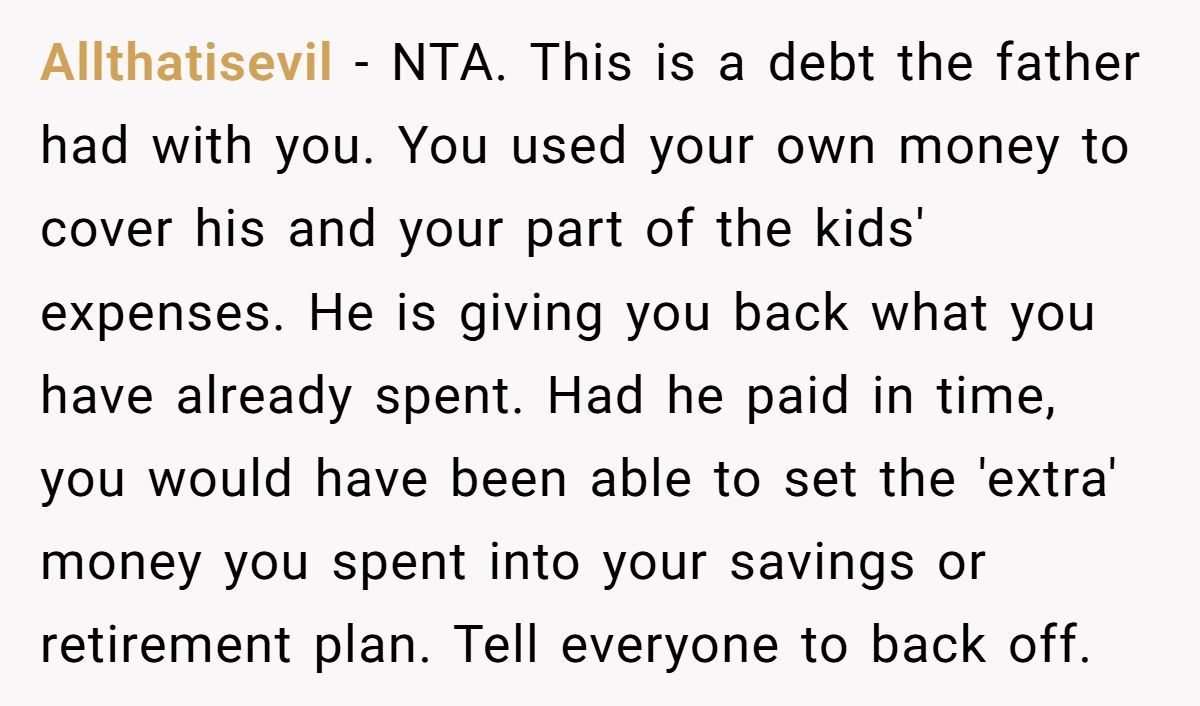

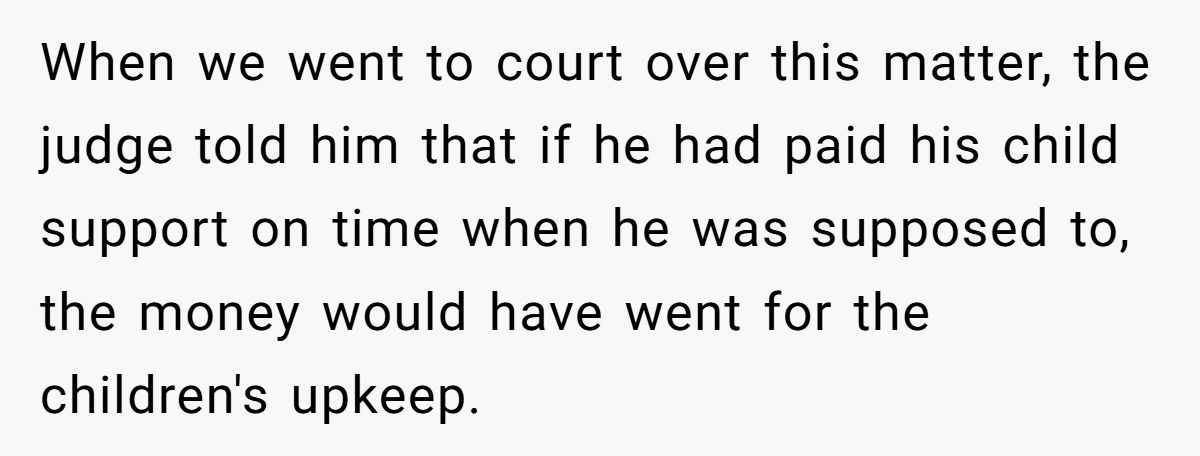

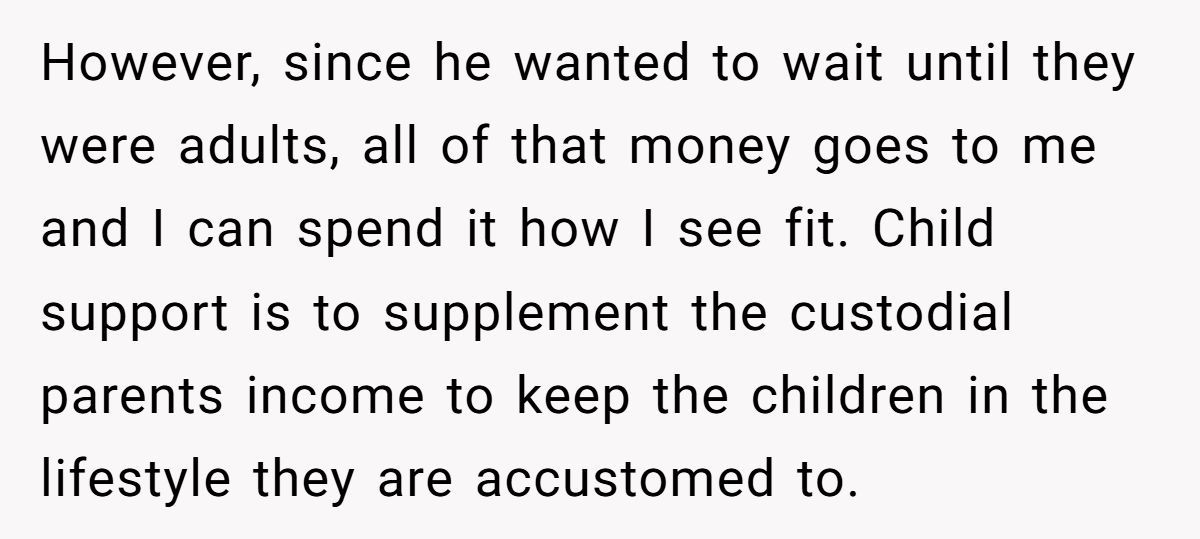

This mom’s decision to dip into backdated child support for her retirement is a bold move, layered with nuance. Financial planner Kristin O’Keeffe Merrick notes, “Child support is meant to reimburse the custodial parent for expenses already incurred” (Forbes). Here, the mom single-handedly bore the cost of raising two kids, sacrificing her own savings. Using part of the funds to secure her future isn’t theft—it’s balancing a ledger long in the red.

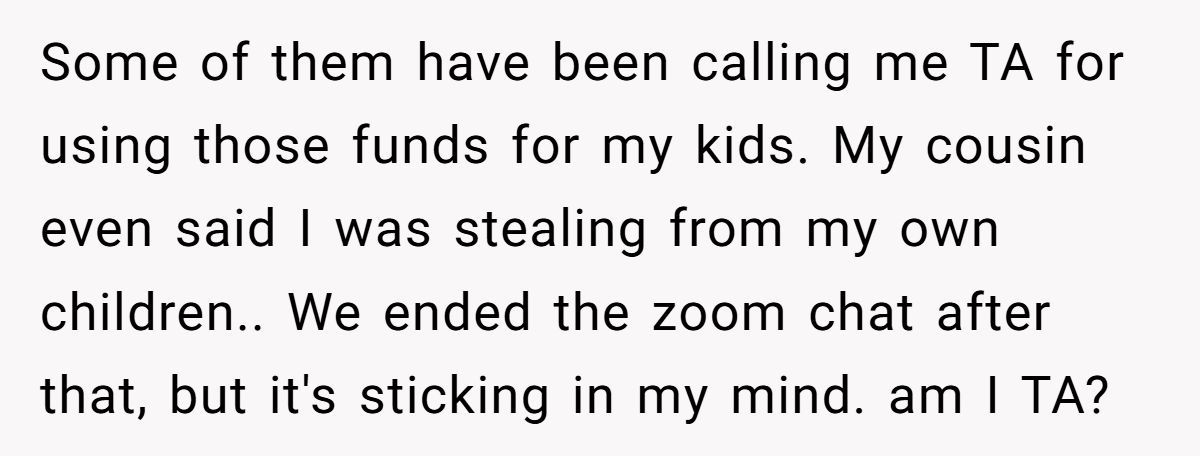

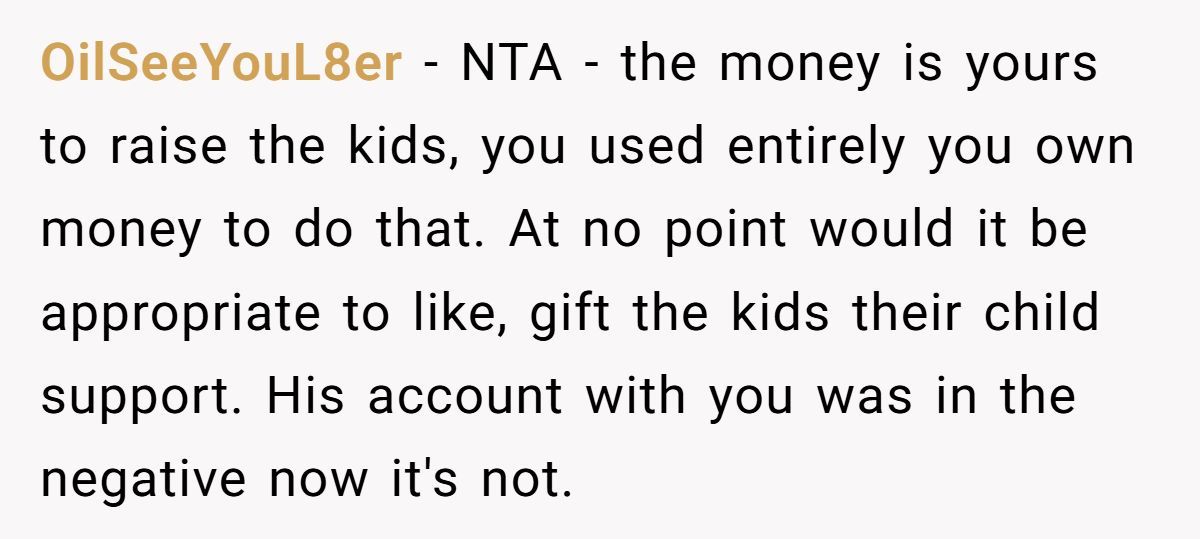

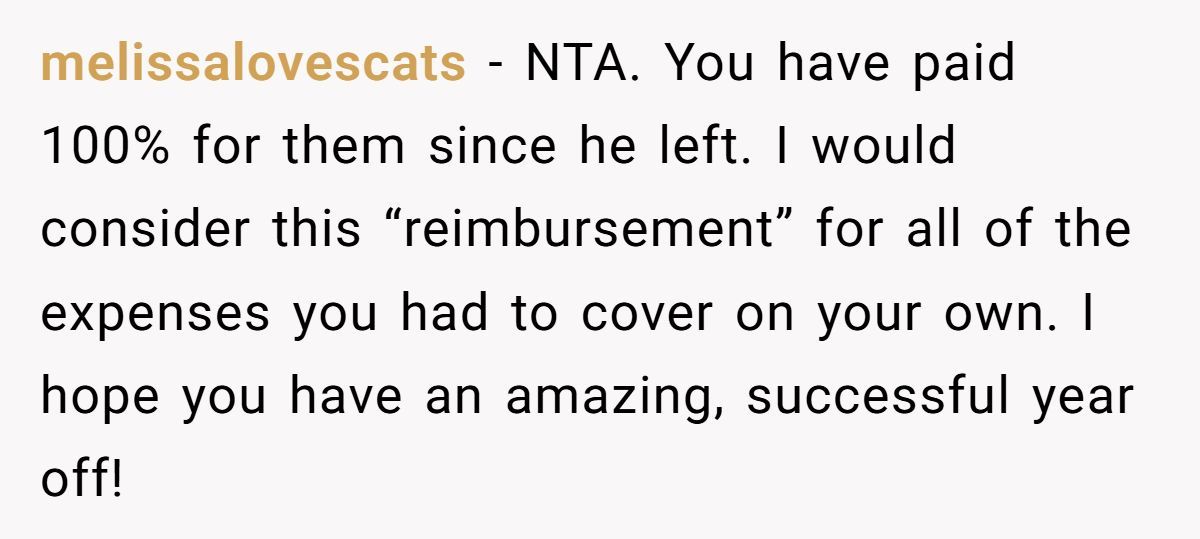

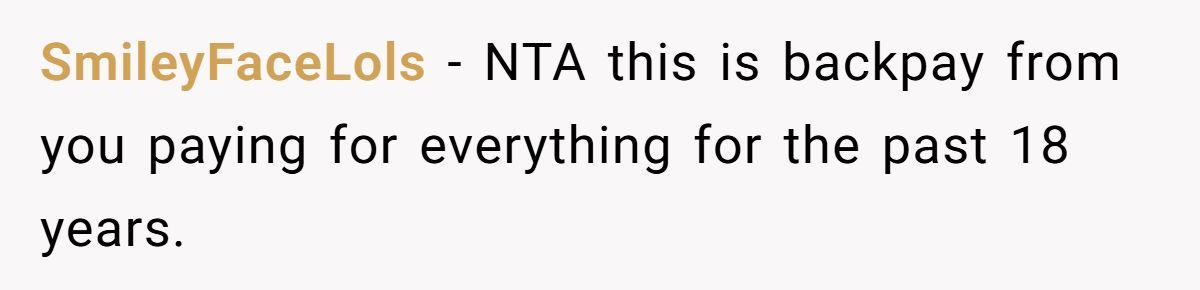

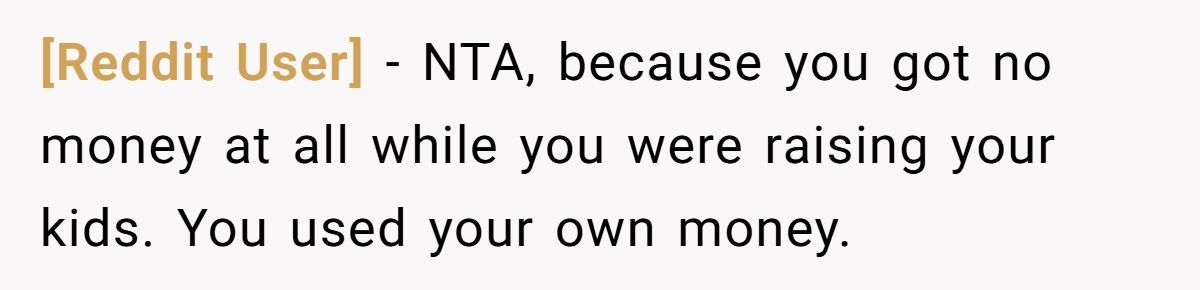

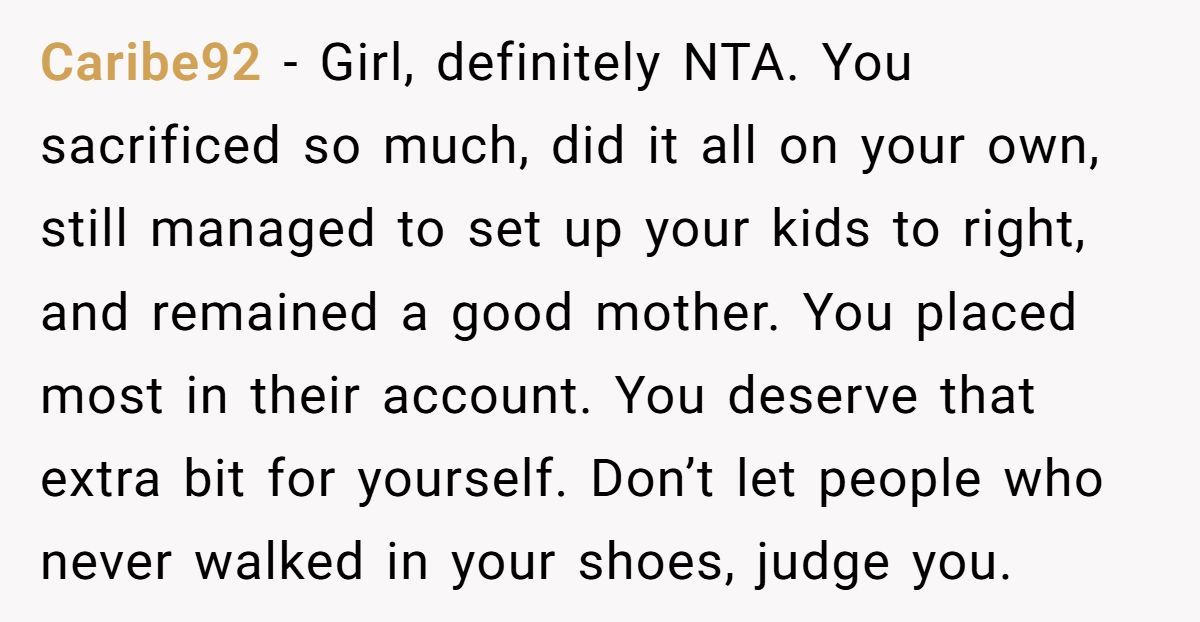

The opposing views? Her family sees it as taking from her kids, arguing the money belongs to them. But this overlooks her 18 years of financial strain, covering 100% of expenses while her ex dodged responsibility. Legally and morally, back child support compensates her past sacrifices, not future obligations.

This situation highlights a broader issue: single parents often face retirement insecurity. A 2023 study from the Center for Retirement Research shows single mothers save 40% less for retirement than dual-income households (Center for Retirement Research). Her choice reflects a desperate need to catch up after years of prioritizing her kids.

Merrick’s advice emphasizes planning: “Single parents should prioritize emergency funds, then retirement, while ensuring kids’ needs are met.” This mom’s trust fund for her kids’ education and housing shows she’s done just that. Her year off, funded partly by this money, is a chance to pivot to a new career.

Here’s the feedback from the Reddit community:

The Reddit crew didn’t hold back, serving up a spicy mix of support and shade. Here’s the raw scoop from the comments, buzzing with cheers for her hustle and a few side-eyes at her family’s nosiness:

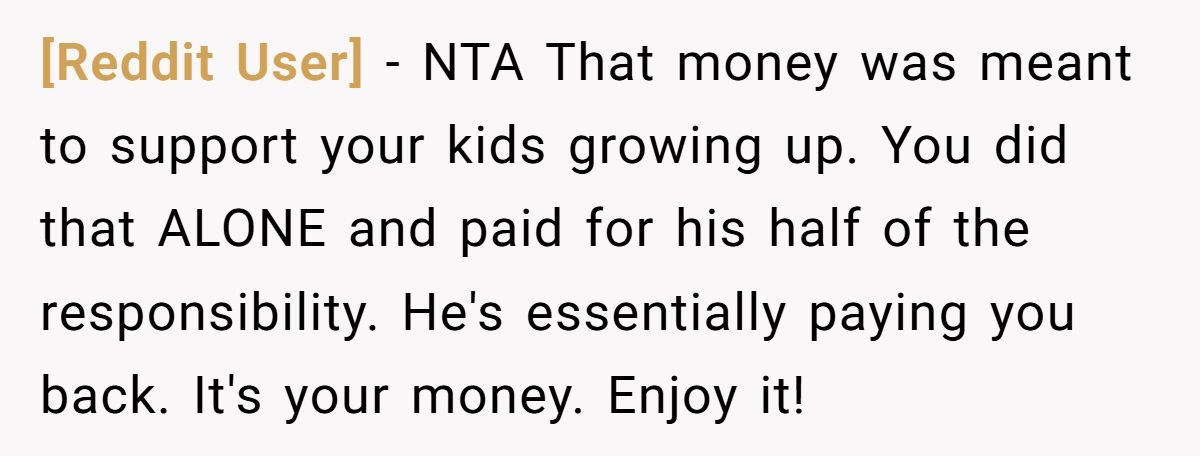

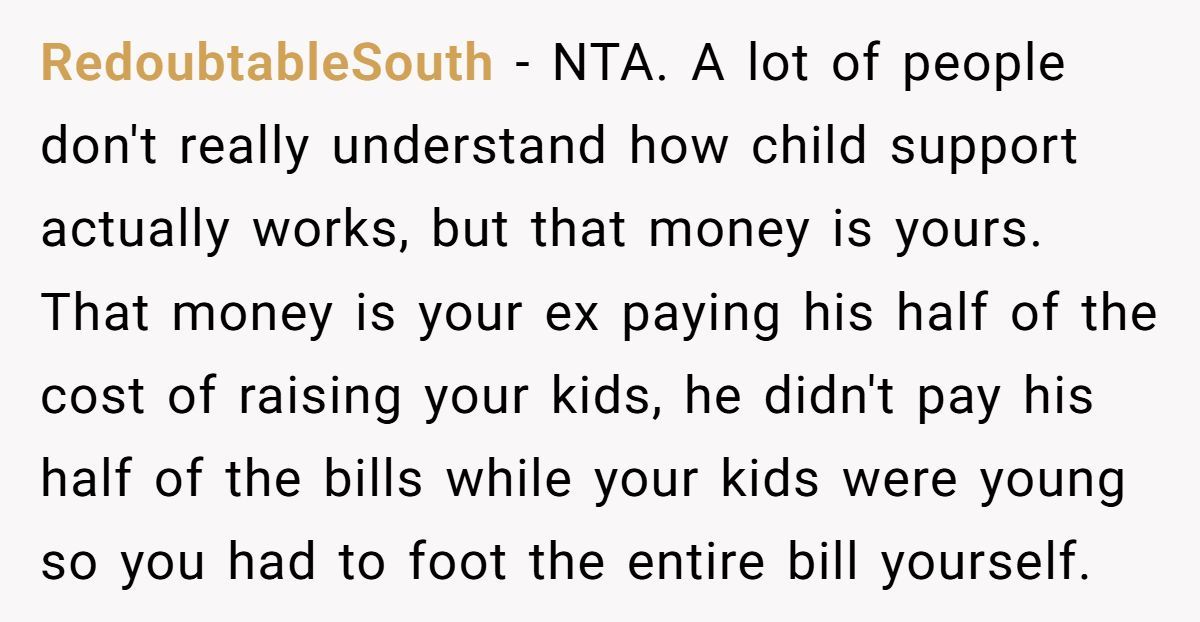

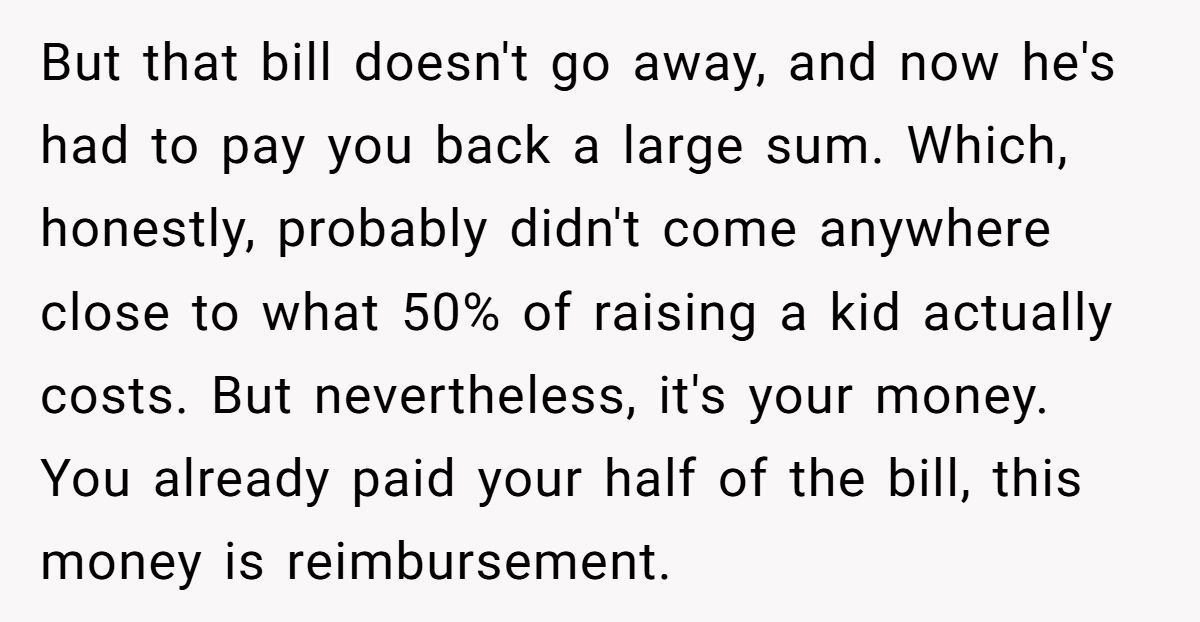

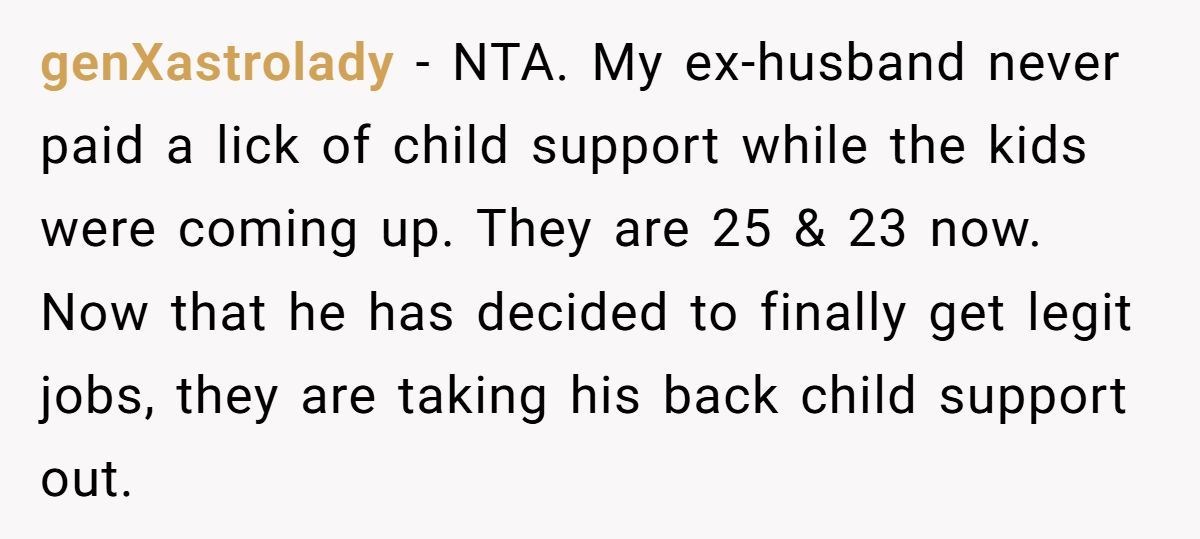

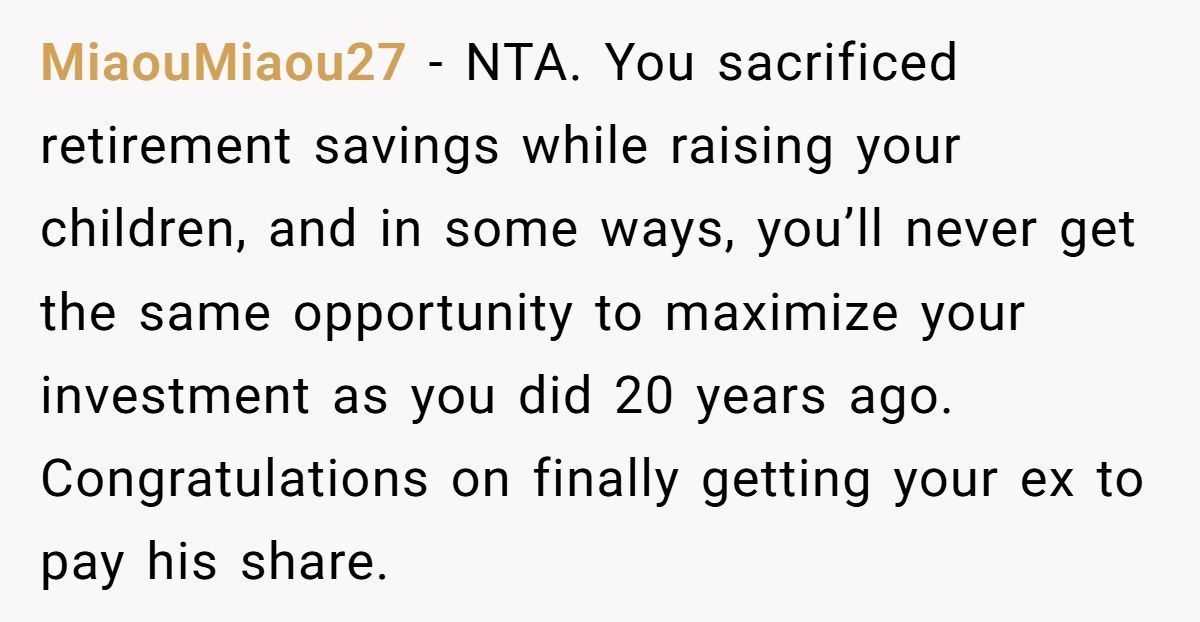

These Redditors rallied behind her, insisting the money was reimbursement for her sacrifices. Some called her family’s judgment clueless, while others questioned if her kids missed out on essentials. Do these hot takes nail the truth, or are they just fueling the drama?

This mom’s story is a rollercoaster of grit and tough choices. After years of carrying the load alone, she’s finally catching a break—but not without family drama. Her decision to fund her retirement while securing her kids’ futures sparks a question: where’s the line between self-care and obligation? What would you do if you were in her shoes? Share your thoughts and experiences below—let’s keep this conversation rolling!