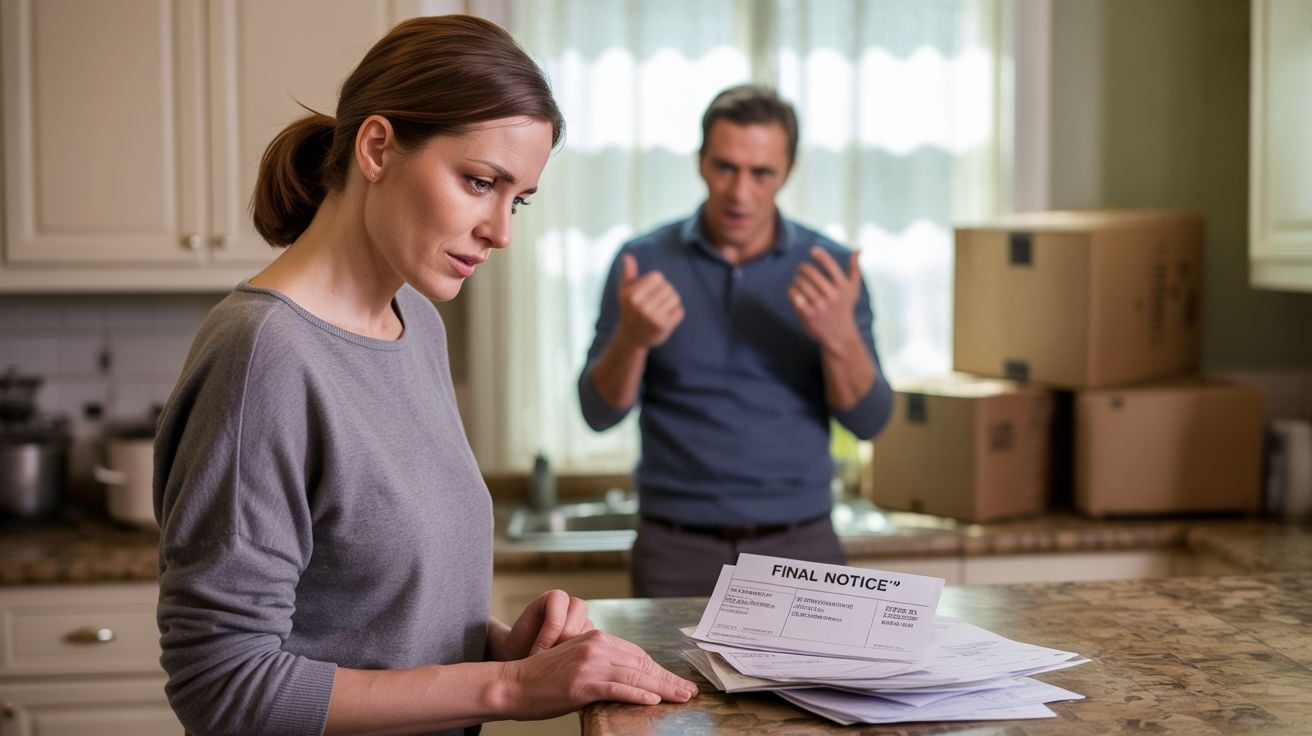

AITA for telling my husband I will not financially support his mother?

The cozy routine of a shared life hit a sour note when a husband proposed sending monthly funds to his financially struggling mother, whose house brims with unused gadgets and impulsive purchases. His wife, scarred by his past secret payments to cover his mother’s credit card bills, drew a firm line: no joint household money would fuel her reckless habits. Her stance, born from frustration and a need to protect their shared future, sparked a heated clash, with accusations of coldness flying.

This wasn’t just about money but a battle over boundaries and responsibility. Living with the mother-in-law during a home renovation revealed her unchecked spending—scams, MLMs, and piles of untouched appliances making the wife’s refusal deeply personal. As the husband defends his role as a “good son,” the couple grapples with balancing family loyalty against their partnership’s stability.

‘AITA for telling my husband I will not financially support his mother?’

The wife’s refusal to fund her mother-in-law’s spending habits is a stand for financial sanity, not cruelty. Her husband’s secret payments in the past breached trust, and his push to use joint funds now ignores the root issue: his mother’s compulsive behavior. The mother-in-law’s dismissal of their warnings—falling for scams and MLMs while claiming superior wisdom—suggests a deeper issue, possibly compulsive spending, that money alone won’t fix.

This scenario reflects broader challenges in managing family finances. The husband’s desire to help his mother is natural, but funneling money without addressing her habits enables rather than resolves her issues. His accusation that his wife is punishing him overlooks her valid concern: protecting their shared resources from a cycle of financial mismanagement that shows no sign of stopping.

Dr. Brad Klontz, a financial psychologist, has noted, “Enabling compulsive spending harms both the spender and the family’s stability.” This perspective validates the wife’s boundary—joint funds are for shared goals, not bailing out self-inflicted crises. Her offer to support non-financial help, like a payment plan or carer, shows care without compromising their partnership’s integrity.

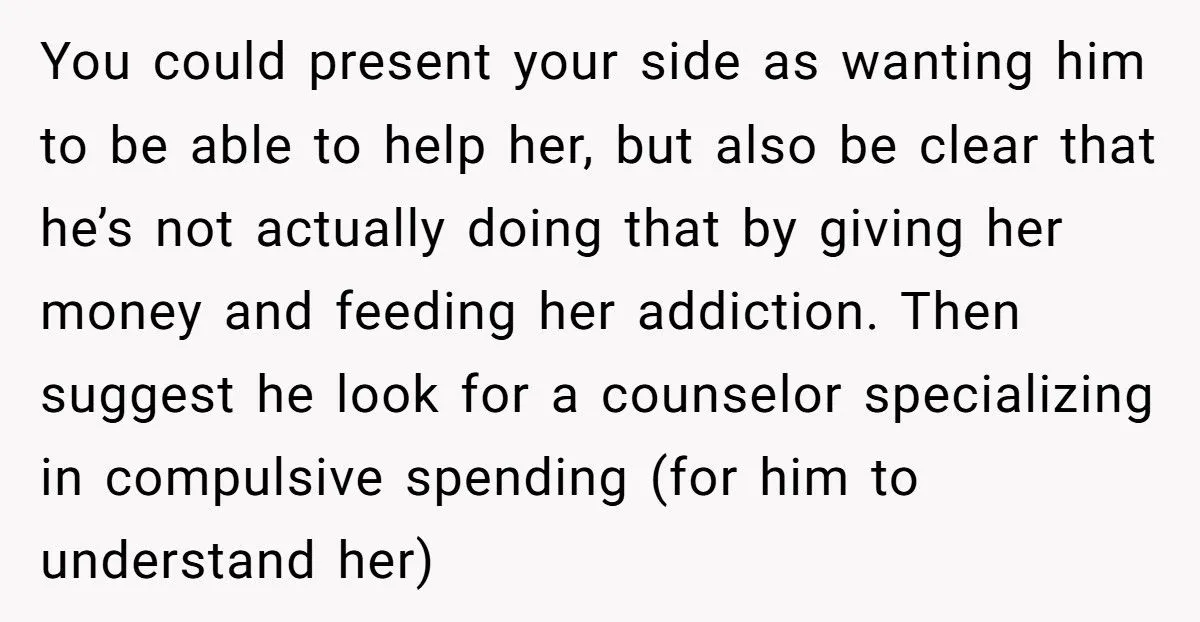

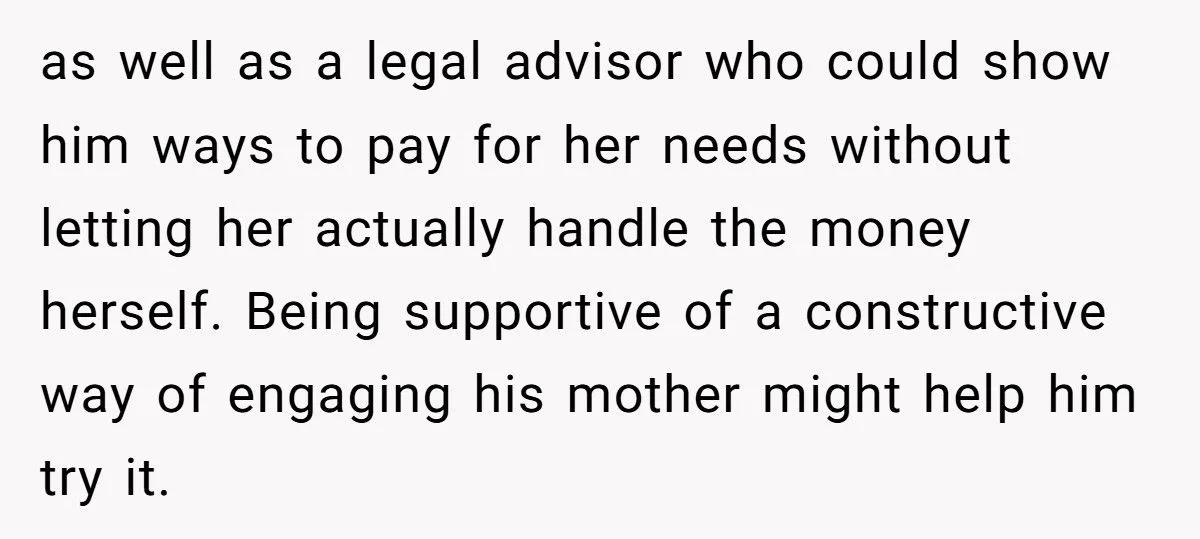

For resolution, the couple could explore professional help for the mother-in-law, such as a financial counselor or therapist specializing in compulsive spending. The husband could use his personal budget for limited support, ensuring household funds remain untouched. This situation invites reflection on how couples can balance filial duty with marital trust, especially when enabling threatens financial security.

Take a look at the comments from fellow users:

Reddit users rallied behind the wife, praising her for setting firm boundaries against her mother-in-law’s reckless spending. They labeled the husband’s actions as enabling, noting that his mother’s financial woes stem from her own choices, not necessity. Many highlighted the breach of trust from his secret payments, emphasizing that joint funds should prioritize the couple’s shared goals.

The community also suggested the mother-in-law needs professional help, like therapy for compulsive spending, rather than cash handouts. They agreed the wife’s offer of non-financial support was reasonable, urging the husband to address his mother’s behavior rather than burdening their marriage. The consensus was clear: enabling poor choices isn’t being a “good son” but a disservice to all.

This marital standoff over a spendthrift mother-in-law highlights the tension between family loyalty and financial responsibility. The wife’s firm boundary protects their shared future, but her husband’s defensiveness risks their trust. How do you navigate supporting family without enabling destructive habits? Share your experiences balancing love for a parent with the needs of your partnership.

Absolutely not! My husband and I raised 4 sons. He died at 64, I was 66. My his and was in the ministry and unfortunately had waived SS due to bad advice and I didn’t work out much, was a SAHM so my SS was small. I kept working until I was 75 then retired. My boys occasionally send me money for things but I have lived alone and supported myself. I refuse to be a burden on my sons.

This mother is a user and the son is an enabler. Do not help support her with your joint account!