AITA For Refusing to Pay Half the Mortgage, Now That Three People Live in the House?

We all know that moment when a perfectly balanced living arrangement suddenly tips sideways. For one first-time homeowner, the joy of purchasing a property with her sister quickly morphed into a financial tug-of-war once a new husband entered the chat. Initially, splitting the household expenses evenly made perfect sense for the siblings.

But when the sister tied the knot and moved her spouse in, the math got blurry. Now, with a new joint bank account in play, the married couple is demanding a return to a strict halfway split, leaving the single sister feeling like she is subsidizing their marital bliss. Cohabitation conflicts are tricky enough, but adding a mortgage into the mix raises the stakes entirely. Curious how it all unfolded? The full story is right below.

The foundation of their living situation started simply enough, born out of pandemic-era practicality.

The math suddenly shifted from a fair roommate split to a frustrating financial burden.

When a romantic partner moves into a shared property, the financial ecosystem is instantly disrupted. Financial professionals often refer to this specific friction point as the equity blindspot. The sister is mistakenly conflating daily living expenses with long-term asset growth. Because she and her husband now share a bank account, she views them as a single financial entity. However, the mortgage isn’t just a bill—it’s an investment.

Financial educators note that when couples move into shared housing, they must establish a clear process that reflects actual usage. Experts often recommend a roommate approach where consumable costs are divided by the number of occupants. But in a co-ownership scenario, the math requires an extra step. Since the sister’s husband is not on the deed, he is effectively a tenant, not an owner.

The most equitable solution requires separating the mortgage from the utilities. The two legal owners should continue splitting the mortgage 50/50 to protect their equal equity. Meanwhile, the husband should pay a fair market rent that goes toward the household, and all consumable utilities should be divided strictly into thirds.

To salvage both her investment and her family relationship, OP needs to sit down with her sister and outline the difference between building wealth and paying for water. She should draft a formal written agreement to clarify these boundaries and ensure everyone understands their financial responsibilities moving forward.

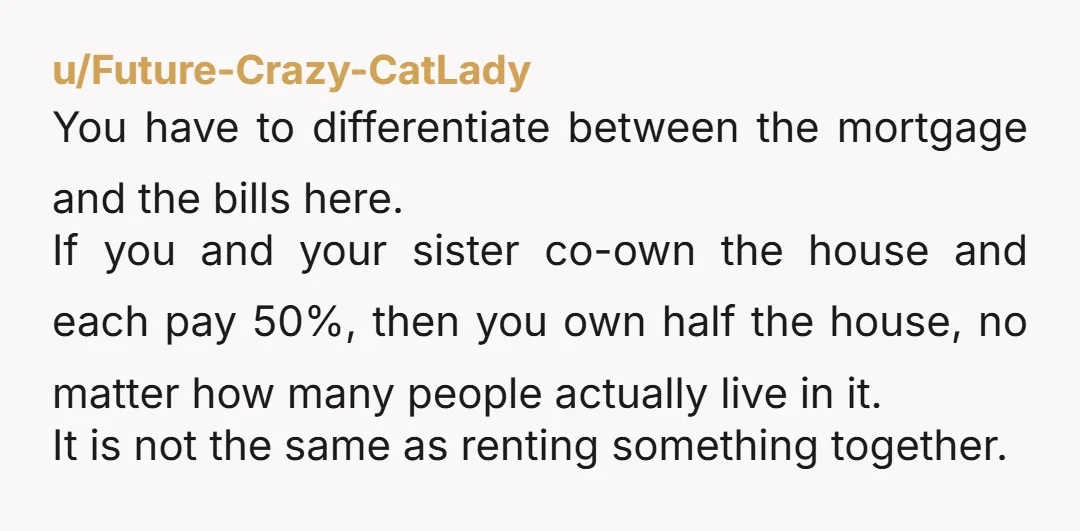

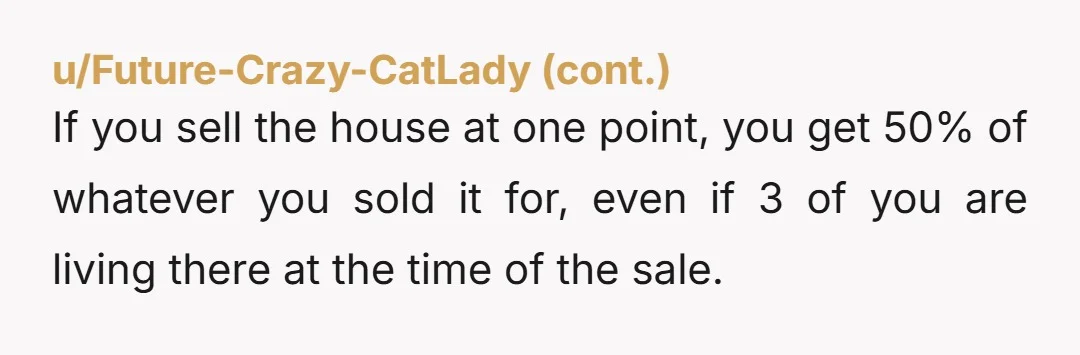

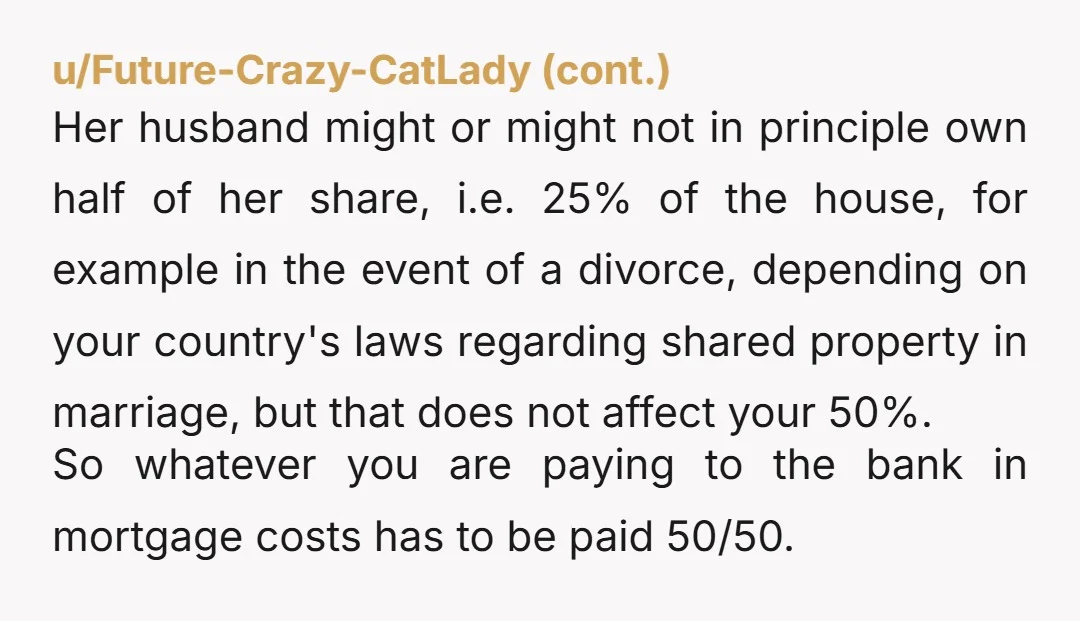

Community Opinions

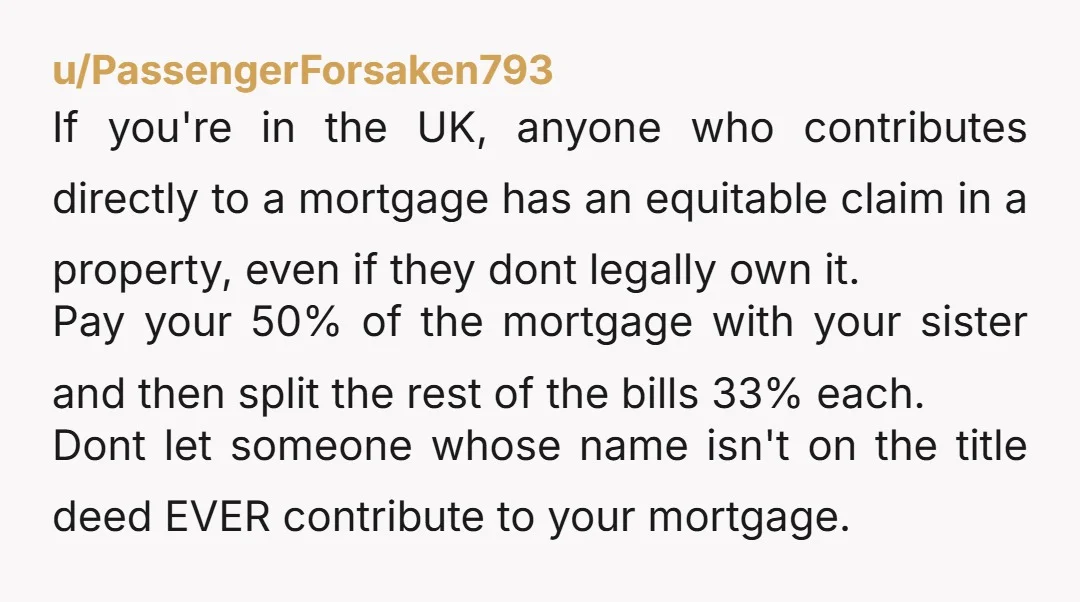

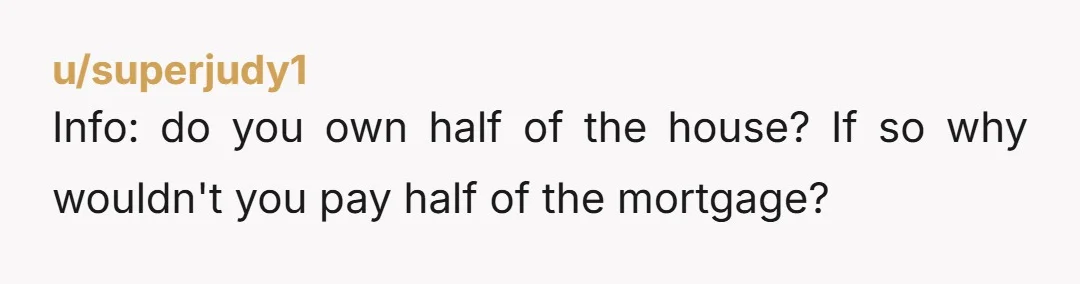

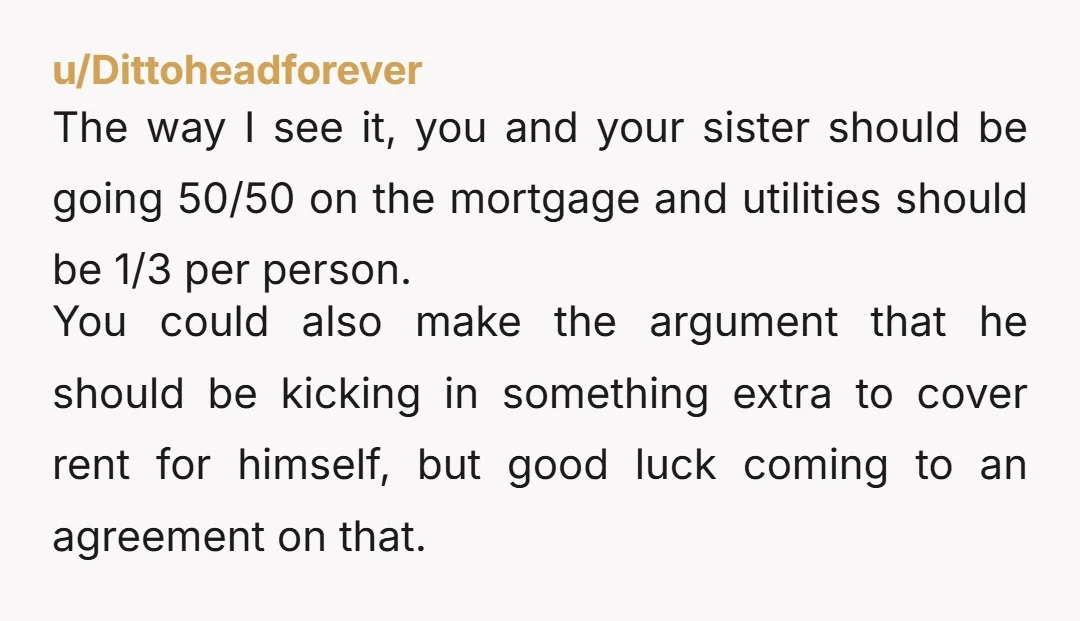

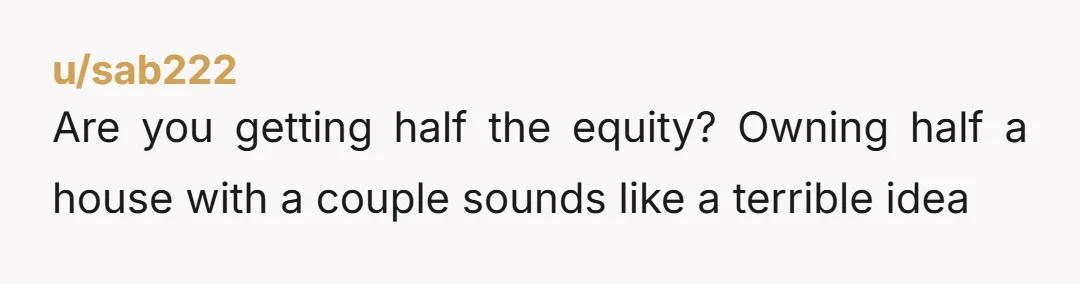

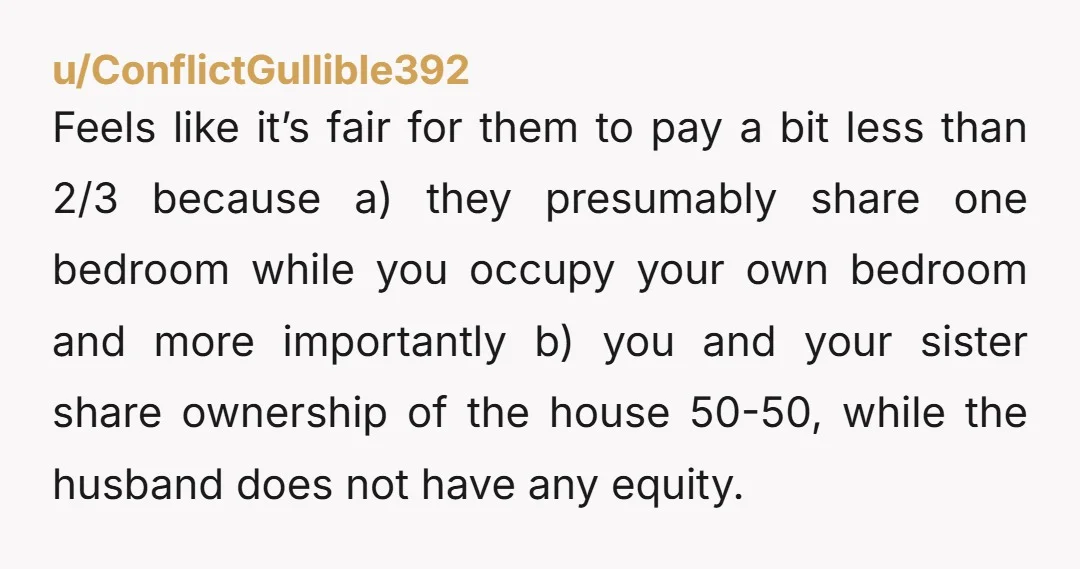

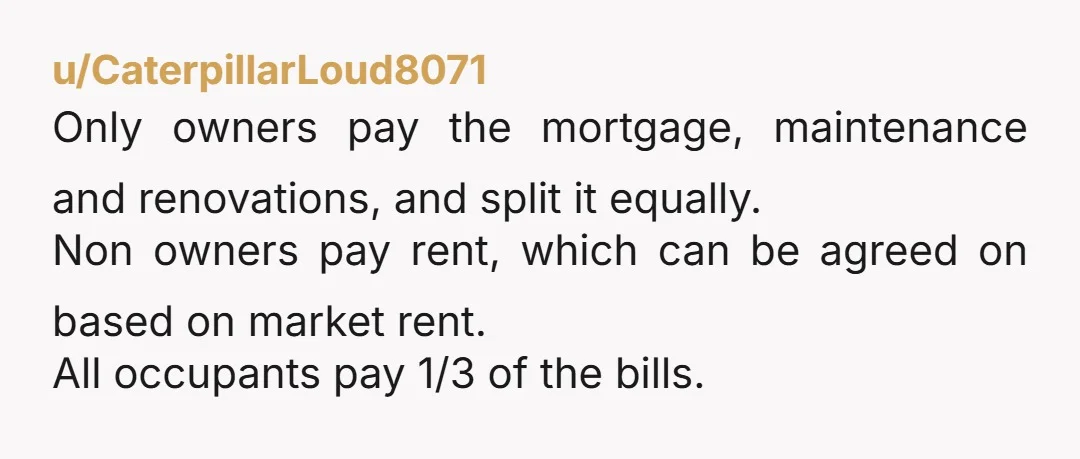

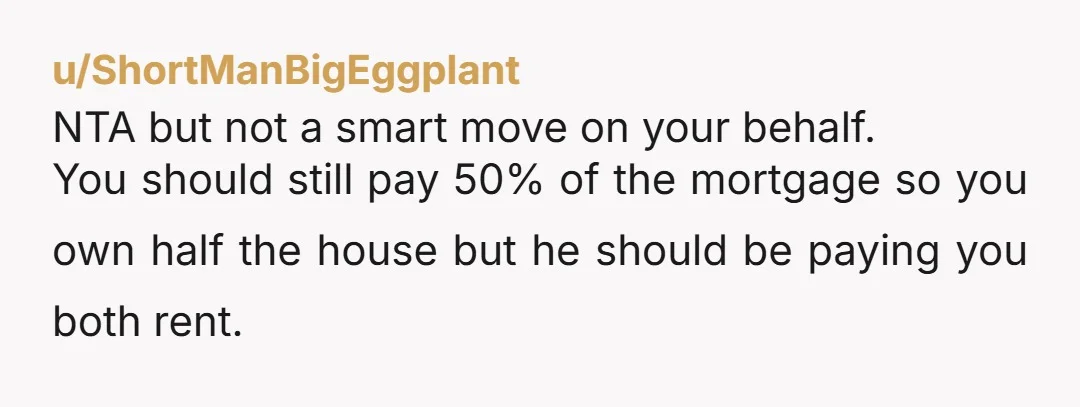

Reddit came in hot with a nearly unanimous verdict, though a few commenters offered nuanced ways to crunch the numbers.

Ultimately, the community agreed that protecting legal ownership should be the top priority over keeping the peace.

Mixing family, real estate, and new marriages is a recipe for complicated math. While some argue that a married couple acts as a single financial unit, others maintain that every adult consuming household resources should pay their fair share. The line between being a co-owner and being a landlord can get blurry fast when relatives are involved.

Do you think the sister is justified in wanting a 50/50 split, or did the husband’s arrival change the financial rules? And how would you divide the bills if you were in this situation? Share your hot take below!