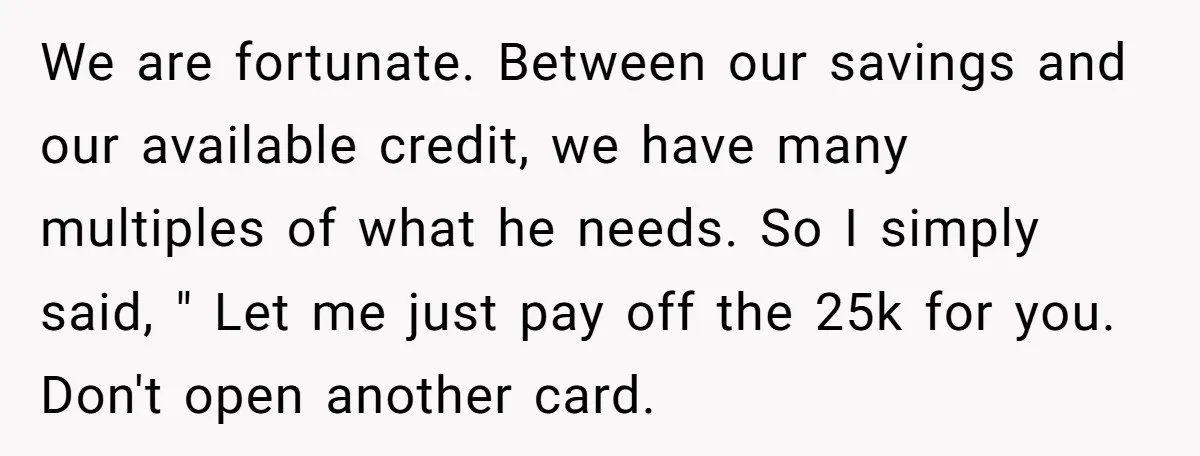

AITA for refusing to lend my brother-in-law $25k so he can kite his credit card debt?

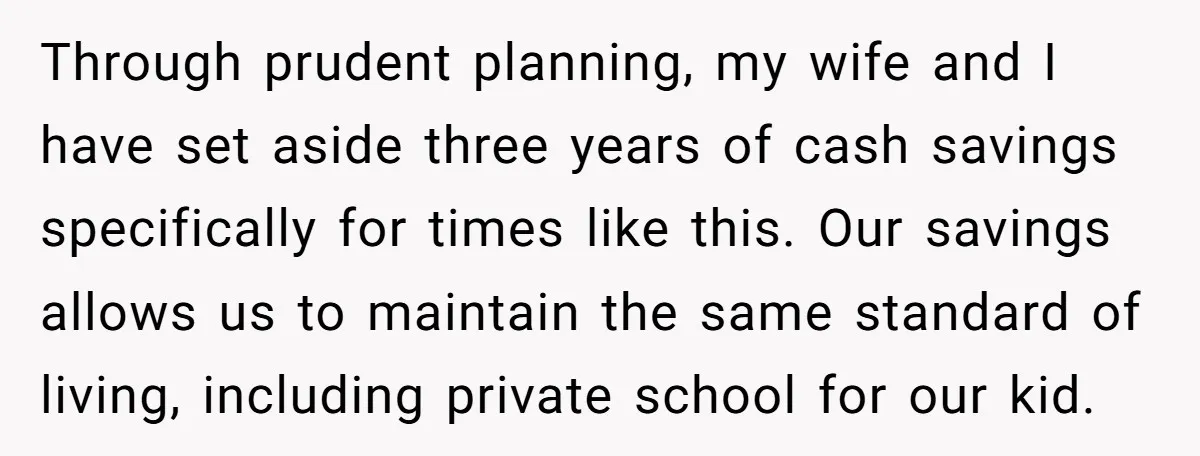

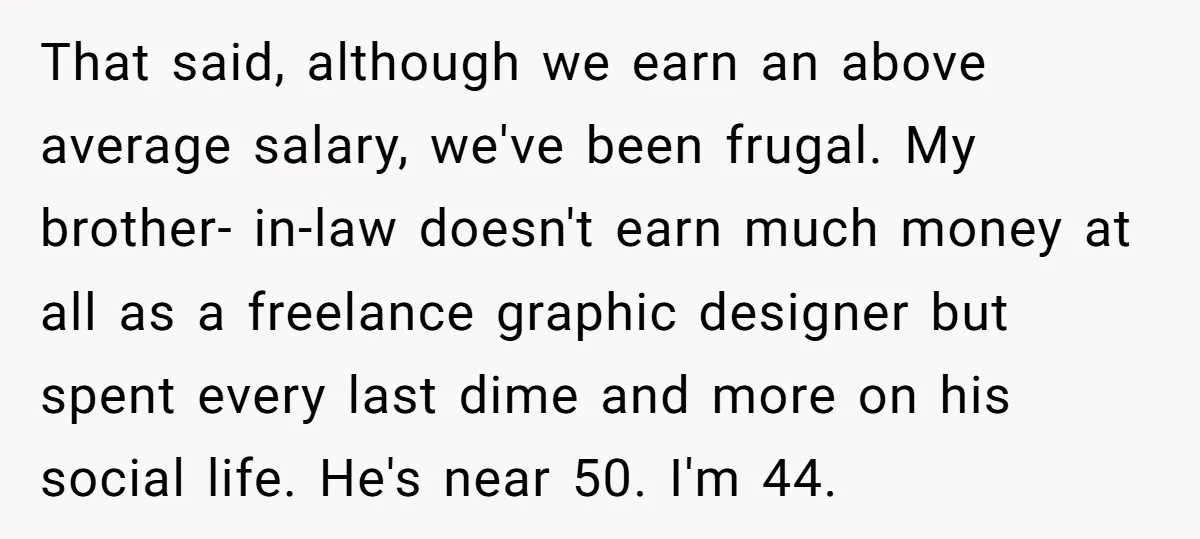

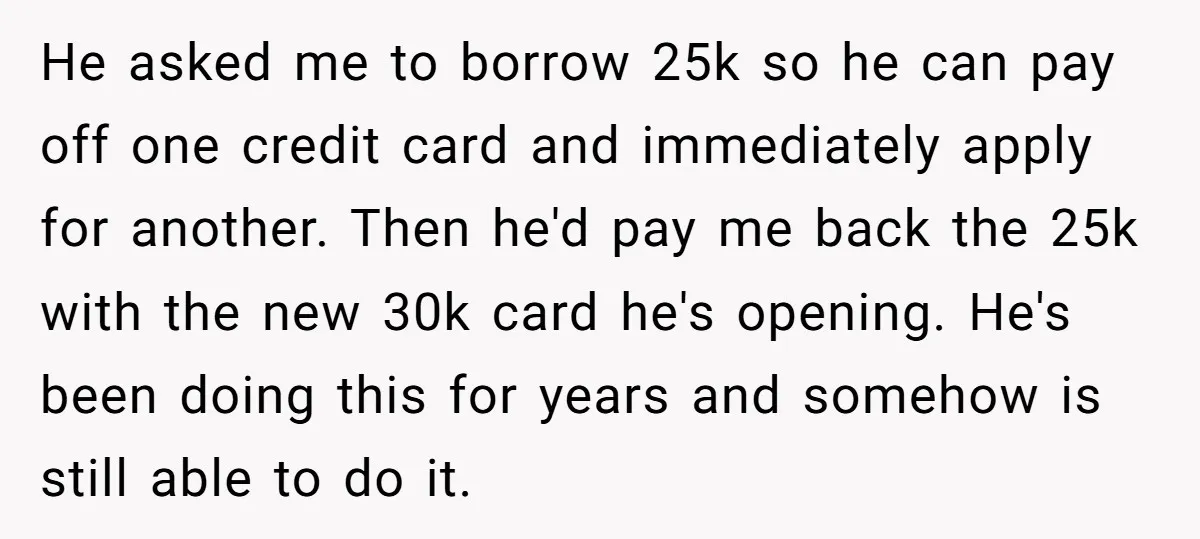

A financially secure couple has built up solid savings through years of careful planning. When the husband’s brother-in-law—nearing 50 and deep in debt from an extravagant lifestyle—asked to borrow $25,000, it wasn’t for an emergency. It was purely to pay off one maxed-out credit card so he could immediately apply for another and keep the cycle going.

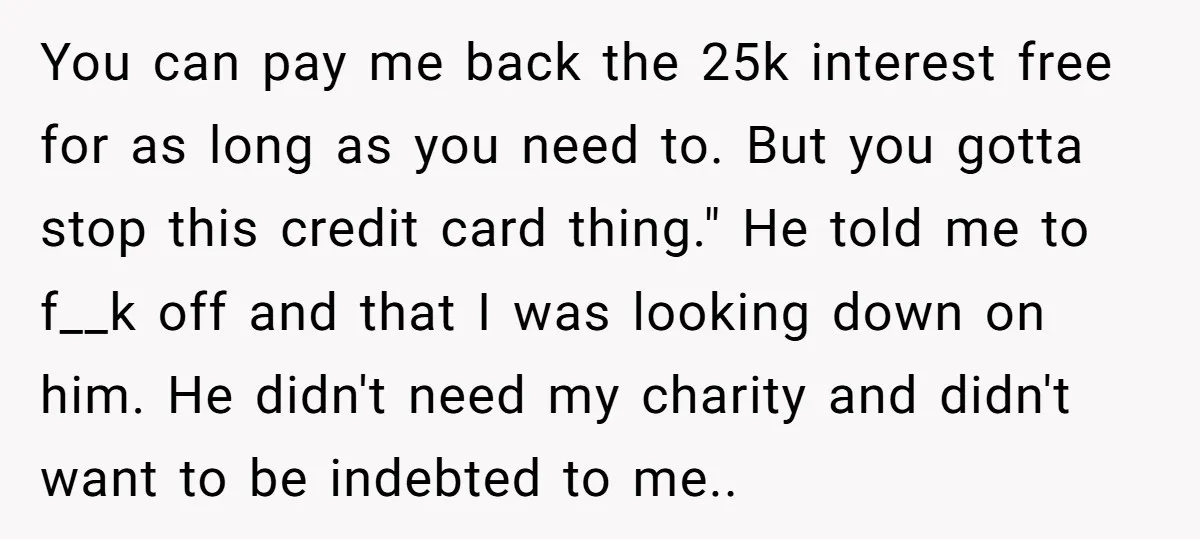

The husband countered with a generous alternative: he’d cover the $25K outright, interest-free, with no rush on repayment—as long as the brother-in-law stopped the dangerous debt juggling. The response? A furious “f**k off,” accusations of looking down on him, and name-calling. Now the husband wonders if he was wrong for drawing that line.

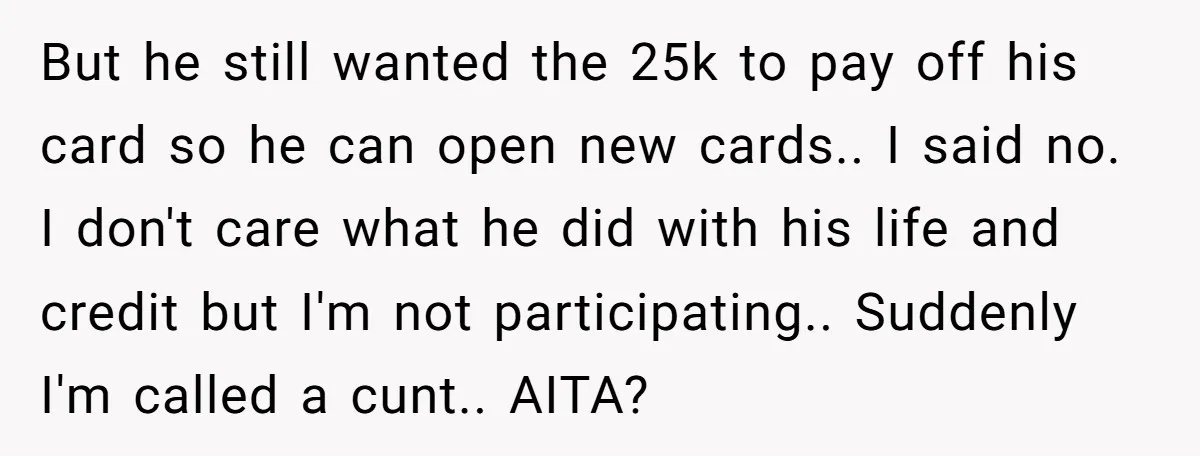

‘AITA for refusing to lend my brother-in-law $25k so he can kite his credit card debt?’

The request came straight to the point, revealing a long-standing pattern of living way beyond his means:

Credit card kiting—paying off one card with another to chase introductory rates or new limits—is an extremely risky game. It often works short-term but racks up fees, tanks credit scores over time, and leaves people vulnerable to sudden denials when issuers catch on. At nearly 50, continuing this cycle signals deeper issues with spending habits rather than temporary bad luck.

The husband’s counteroffer was remarkably kind: wiping the debt clean without interest or pressure, in exchange for breaking the addiction to new credit. Rejecting that while demanding the loan anyway shows entitlement and avoidance of real change. Financial experts like Dave Ramsey frequently warn against enabling such behavior—lending without conditions prolongs the problem.

Family money requests are tricky because emotions run high. Refusing to fund poor choices isn’t judgment; it’s protecting your own household’s security, which comes first—especially with a child relying on that stability. The explosive reaction confirms the boundary was necessary.

If similar asks arise again, a calm “we don’t lend money to family” policy avoids negotiations altogether. Therapy or financial counseling could help the brother-in-law if he’s open, but that’s his journey—not yours to finance.

Here’s the input from the Reddit crowd:

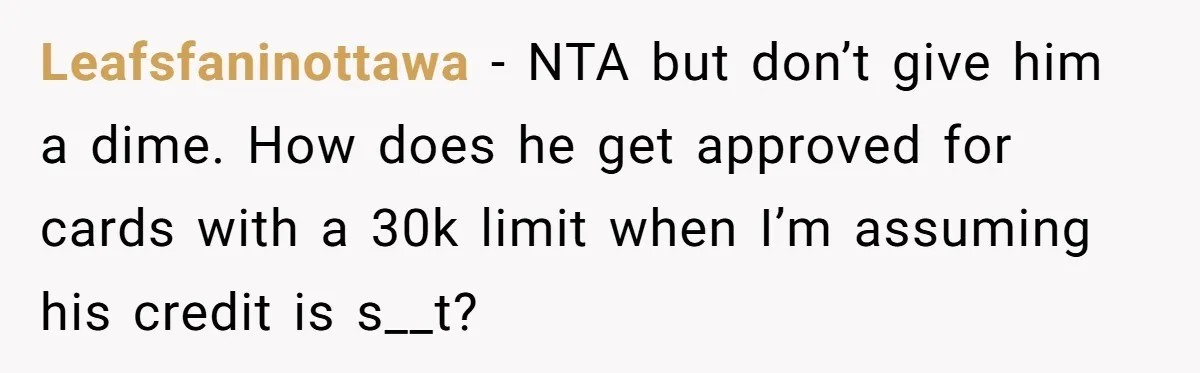

The online crowd was unanimous: the husband is solidly not the asshole, and many urged him to never lend a cent:

![[Reddit User] - NTA. Your money, you get to decide whether or not to loan it out.](https://en.aubtu.biz/wp-content/uploads/2025/12/wp-editor-1766566788504-9.webp)

A couple asked for practical advice or more details:

This husband offered an incredible lifeline—clearing serious debt without interest or deadlines—yet got slammed for trying to end the cycle instead of feeding it. Protecting hard-earned savings from risky schemes isn’t selfish; it’s responsible.

Family doesn’t entitle anyone to fund bad habits, especially when a better path is rejected outright. Would you have made the same counteroffer, or just said no from the start? Ever dealt with a relative’s money mess spilling over? Spill the tea below!

![My[23F] Boyfriend [23M] of 3 Years Stealthily Took My 11 Year Old Dog to a Vet 80km Away to Be Put to Sleep. It Was Only Luck I Found Out and Got Him Back. Bf Doesn't Know I Have My Dog Back but He Comes Back Tomorrow Night](https://en.aubtu.biz/wp-content/uploads/2026/04/ad_featured_2003_1777343520-768x403.webp)