AITA for refusing to give my daughters financial help even though I’m worth over $10 million?

A 74-year-old widower sits on a $10 million fortune—mostly in stocks—yet hands his two working daughters just $50 each at Christmas. He paid for their college, seeded modest home down-payments, and tucked away $80k per grandchild for school. Nothing more. When a slip reveals the eventual inheritance, the daughters stay silent, but a friend brands him selfish.

The knot tightens: he fears capital-gains taxes, wants ironclad end-of-life care, and refuses to touch principal. Parallel lives unfold—his daughters scrape by paycheck to paycheck while he calculates decades of hypothetical expenses. What starts as prudent conservatism morphs into a family rift over money that could change lives today.

Inheritance snowballs into eight-figure wealth under careful stewardship.

Daughters receive measured support, then radio silence.

Financial strain surfaces without a single request.

Priorities lock on personal security and tax avoidance.

A friend’s accusation prompts soul-searching.

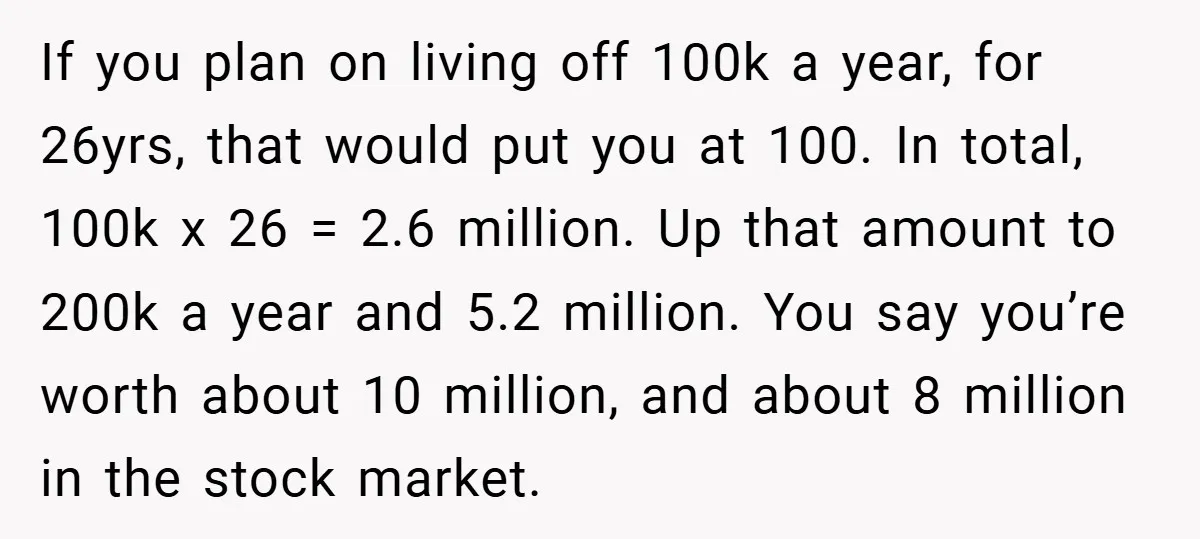

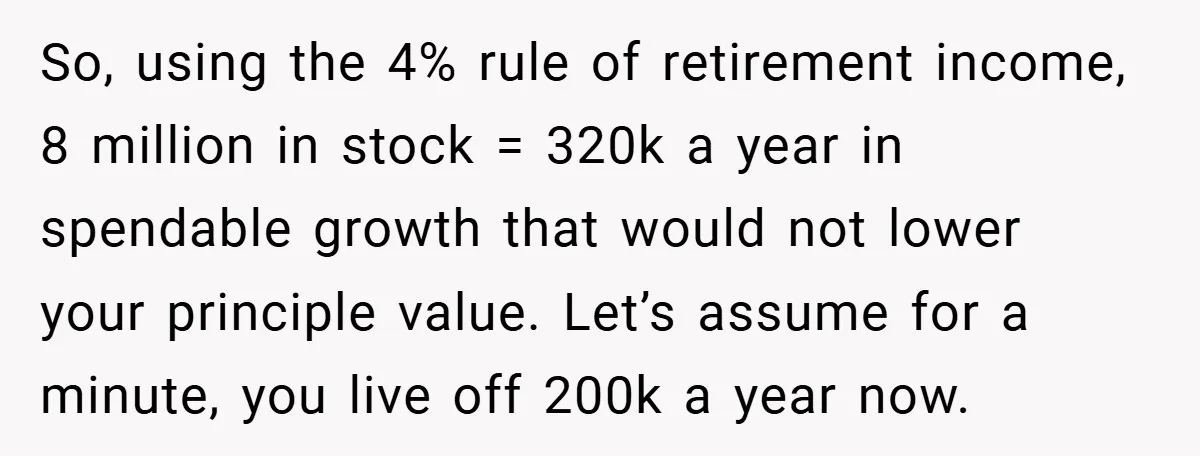

Wealth hoarding at life’s final stage often masks anxiety, not prudence. The poster’s $8 million in equities could yield $320k annually via the 4% rule without touching principal—far beyond typical retirement needs.

Opponents highlight tax aversion and the daughters’ silent struggle. Beyond that, $80k per grandchild may fall short against rising tuition. What makes the story more complicated, gifting $17k per daughter yearly avoids gift tax entirely.

Gerontologist Ken Dychtwald notes, “Many affluent seniors fear outliving assets despite evidence to the contrary; generosity becomes the casualty”. Liquidating even 10% now could fund memories without denting security. The verdict leans selfish—money unused today is opportunity lost tomorrow.

Here’s how people reacted to the post:

Many users rallied behind the daughters, urging the father to loosen his grip and share while alive.

A few commenters offered nuance, acknowledging his rights while gently pushing for compromise.

Light-hearted voices chimed in to deflate the tension, poking fun at the absurdity without malice.

![[Reddit User] − So, it’s your money. But let’s do some maths. You’re 74. The average life expectancy of a U. S. male is 77. Chances are, your home and...](https://en.aubtu.biz/wp-content/uploads/2025/11/wp-editor-1761984602431-1.webp)

The poster clings to millions while his daughters count pennies—math says he can loosen the grip without risk. Legacy isn’t just what’s left behind; it’s what’s shared while breathing. Would you rather fund memories now or mortgages later? How much is “enough” to feel secure at 74? Drop your numbers and stories below.

YTA. I commend you for supporting the educational expenses of you daughters, so that they have no school loan debt, you should be creating a Revocable Trust for your wealth, to protect it from taxation. You did not share your talents with your kids. You should have taught your daughters how to invest in their teens, and encouraged them by bankrolling them, and rewarded their successes. Teaching financial smarts was your duty as a savvy parent. After 20 years, they each might have had a nice portfolio, and be able to make wise investment decisions. You could have set up 529 accounts for you grandchildren’s college education. I question that this posting is from a real person.