AITA for not giving my parents loans at 16?

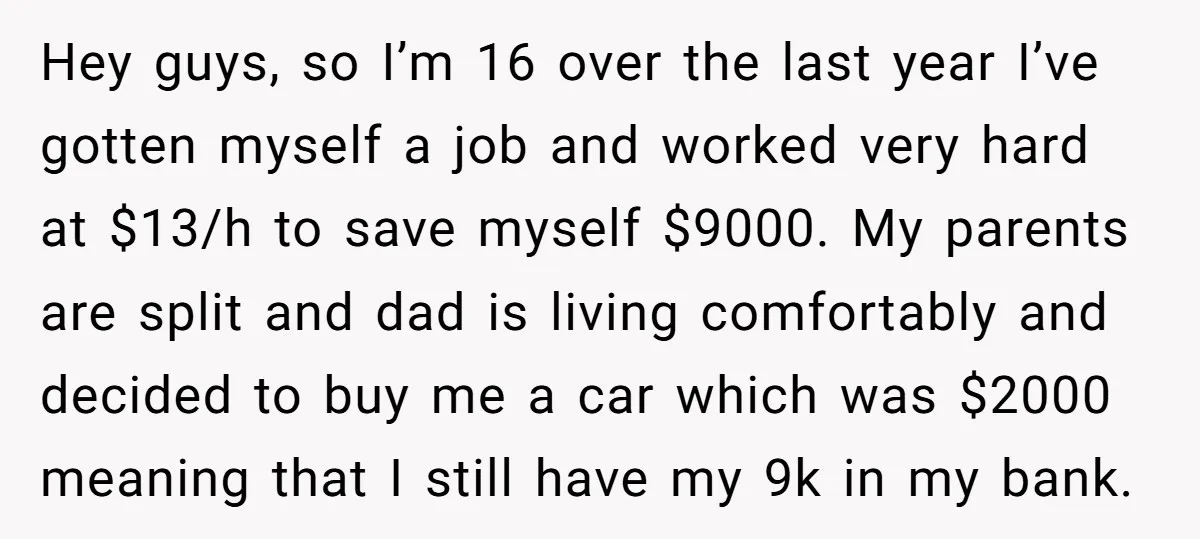

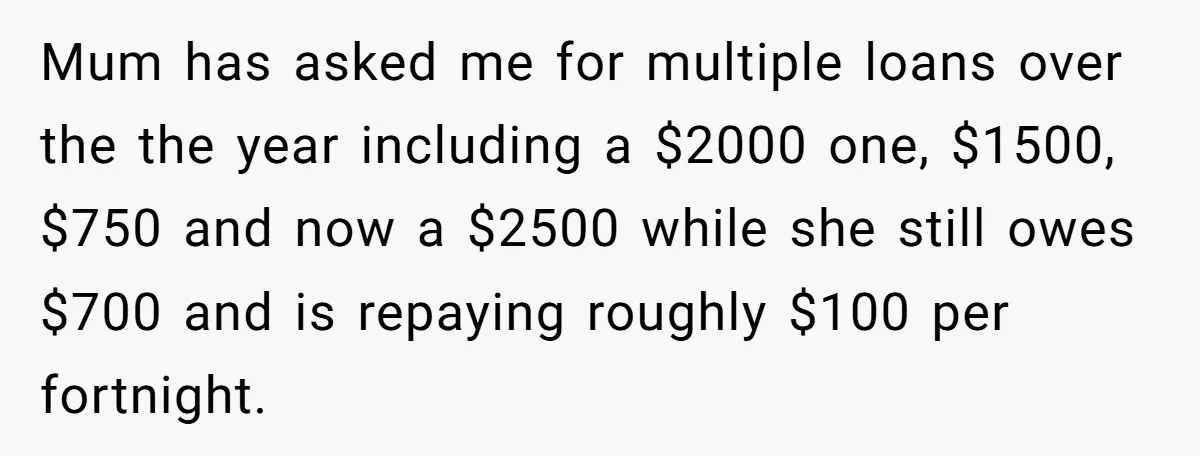

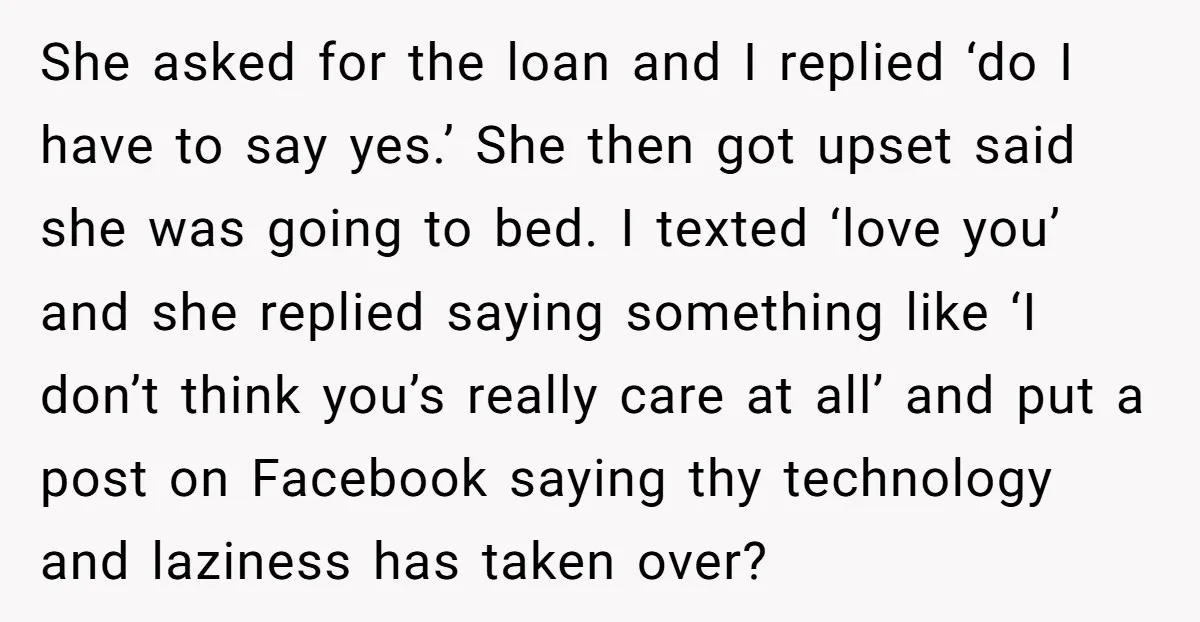

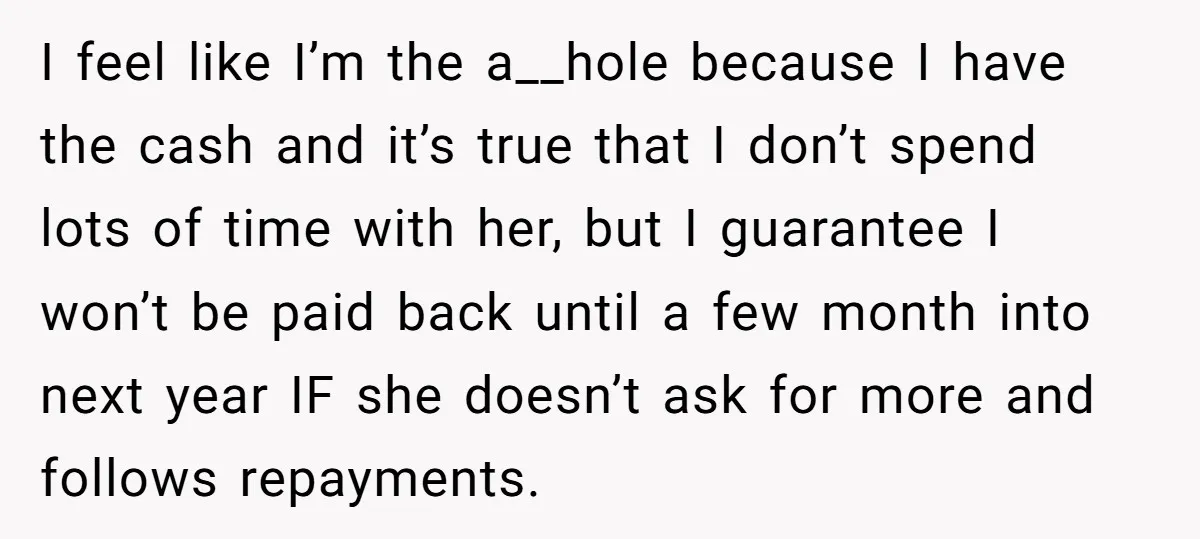

A 16-year-old has saved $9,000 from grueling weekend and Friday shifts at $13 an hour, plus he got a $2,000 car from his dad—meaning his savings are intact. But his mom, who lives separately and makes questionable financial choices, has repeatedly asked for loans: $2,000, $1,500, $750, and now $2,500, while still owing $700 with slow $100 fortnightly repayments. When he questioned if he had to say yes, she got upset, went to bed, and later posted vaguely about “technology and laziness taking over” on Facebook.

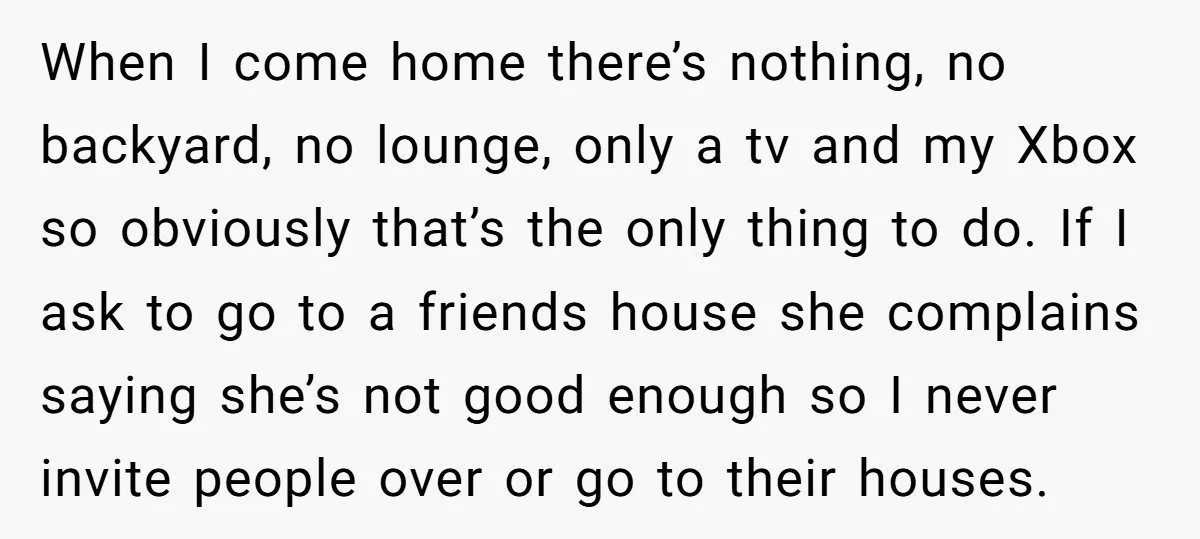

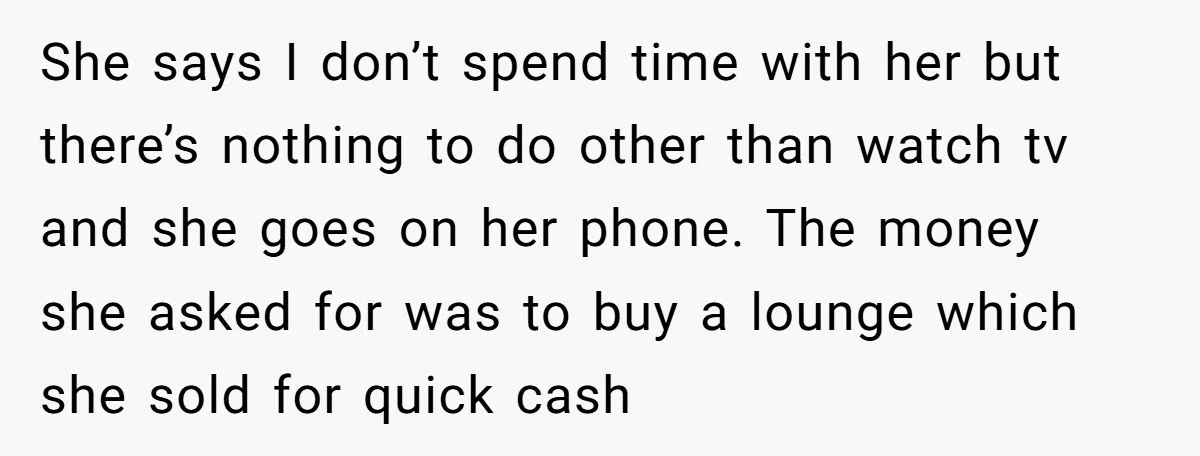

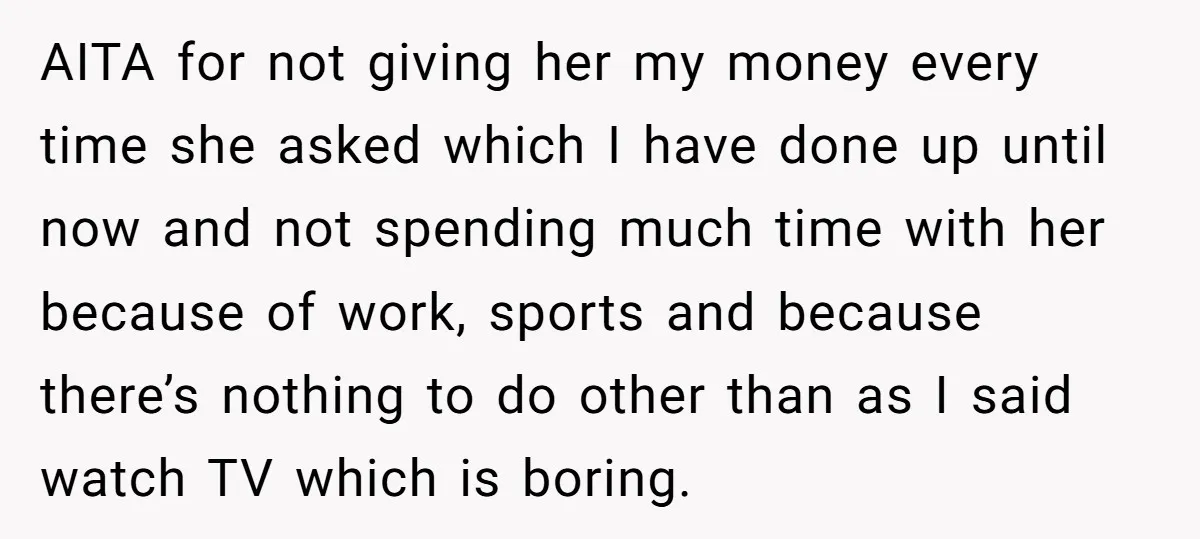

The post quickly drew attention because it exposes a tough reality for some teens: earning your own money only to have a parent treat it like a personal bank, complete with guilt trips and emotional manipulation. The teen feels bad about not spending more time with her—limited by work, sports, and a bare home with just a TV and Xbox—but he’s tired of funding her impulses while she prioritizes repayments last. The internet response was clear: protect your savings.

‘AITA for not giving my parents loans at 16?’

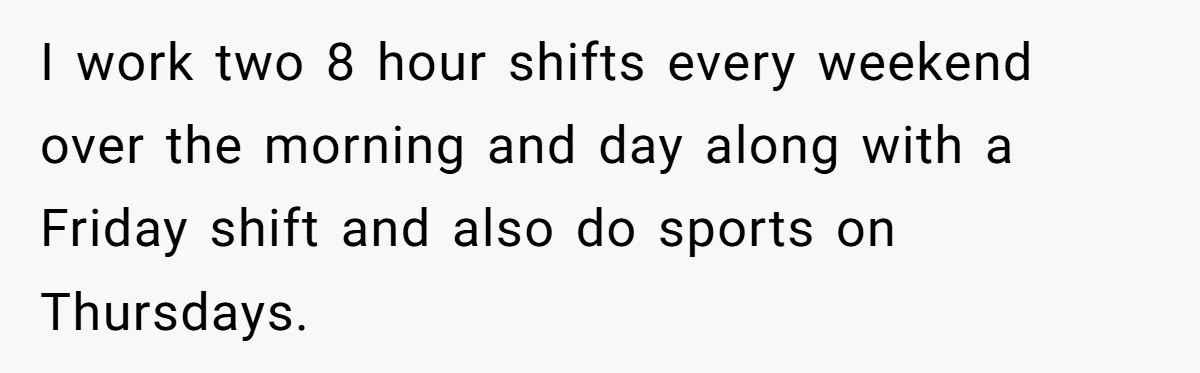

The teen has worked hard to build savings:

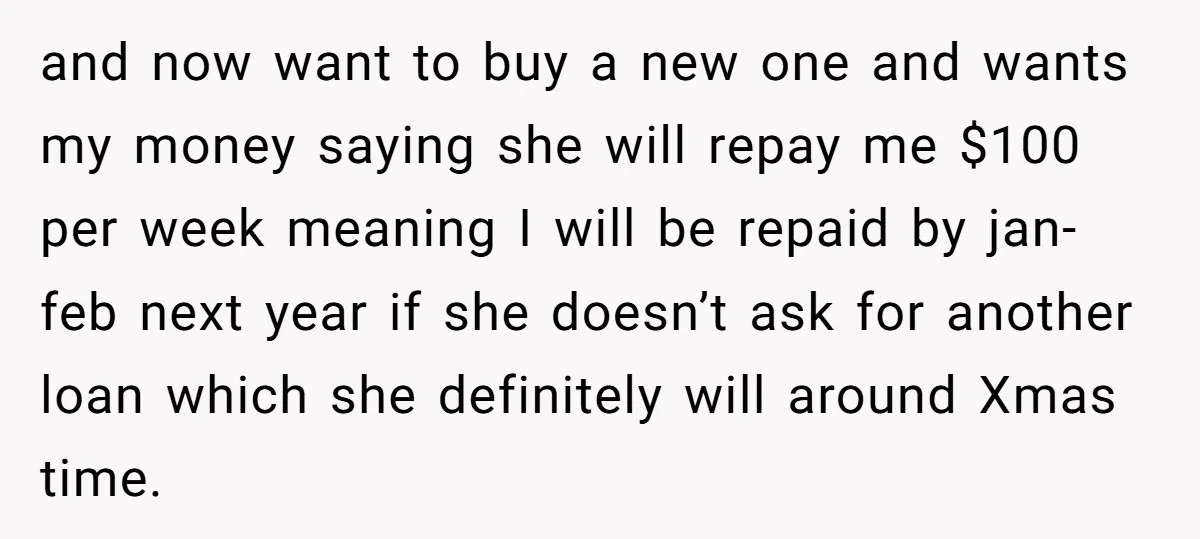

His mom has asked for multiple loans:

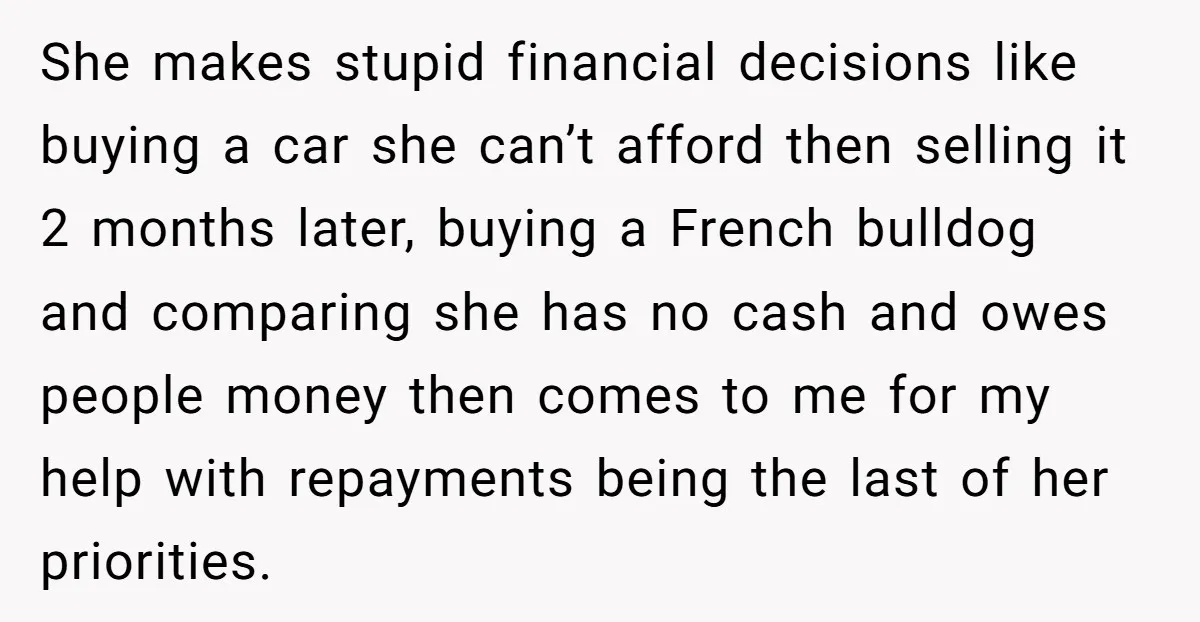

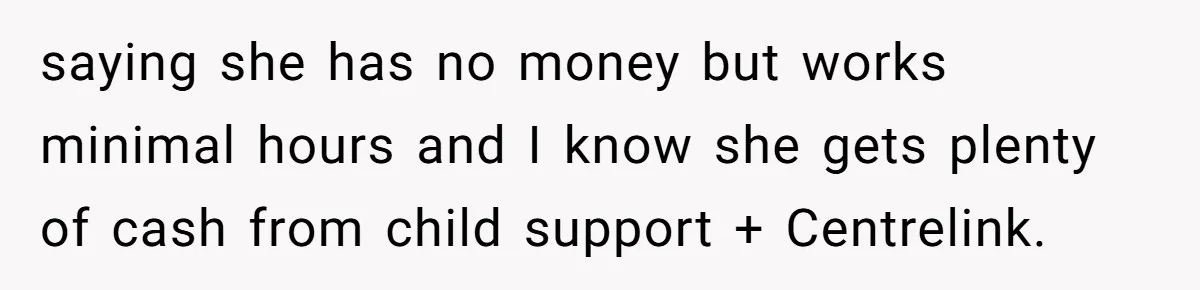

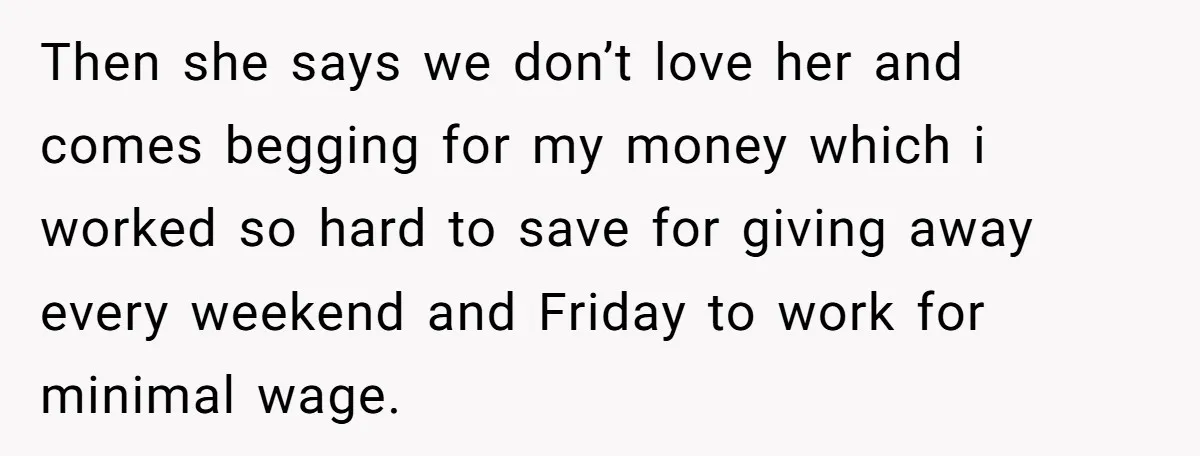

Mom’s financial habits are problematic:

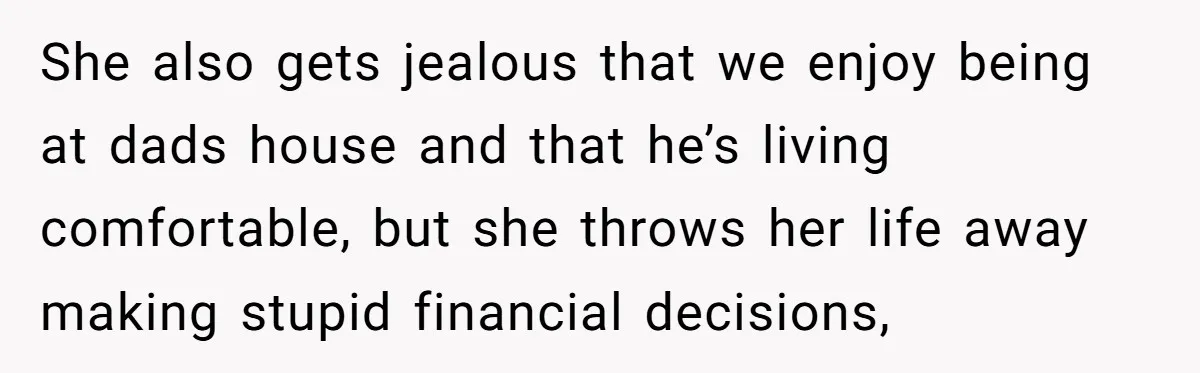

She gets jealous of the dad’s comfortable life:

This situation involves financial abuse, where a parent repeatedly pressures a child for money they’ve earned, often with emotional manipulation like guilt trips or passive-aggressive social media posts. At 16, the teen is a minor—parents have a legal duty to support them financially, not the reverse. In places like Australia (implied by Centrelink/child support mentions), minors aren’t obligated to fund parents, and such requests can cross into exploitation.

From the mom’s perspective, she may feel entitled due to raising the child or current hardships, viewing the savings as “family” resources. But poor decisions—like impulse buys followed by quick sales—shift the burden unfairly onto the teen.

Experts on family dynamics and financial abuse (e.g., from organizations like the National Network to End Domestic Violence or child welfare resources) stress that teens should protect earnings for their future (education, independence). Practical steps: secure accounts (no joint access), document requests, involve a trusted adult (dad, school counselor), and consider full-time living with the stable parent. Building boundaries early prevents escalation—love doesn’t mean unlimited financial access.

The teen’s hard work deserves protection; guilt is a common tactic, but saying no here isn’t selfish—it’s self-preservation.

Here’s what the community had to contribute:

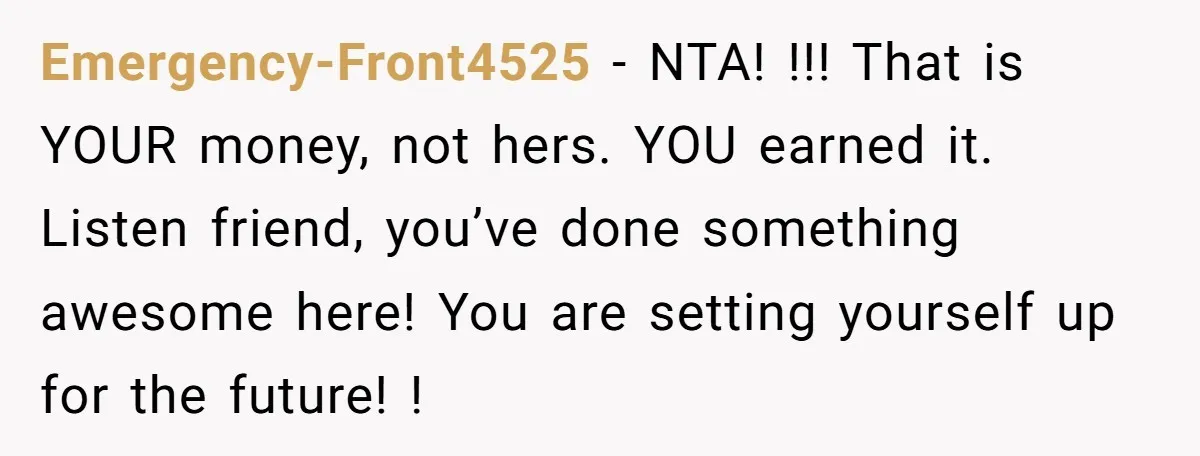

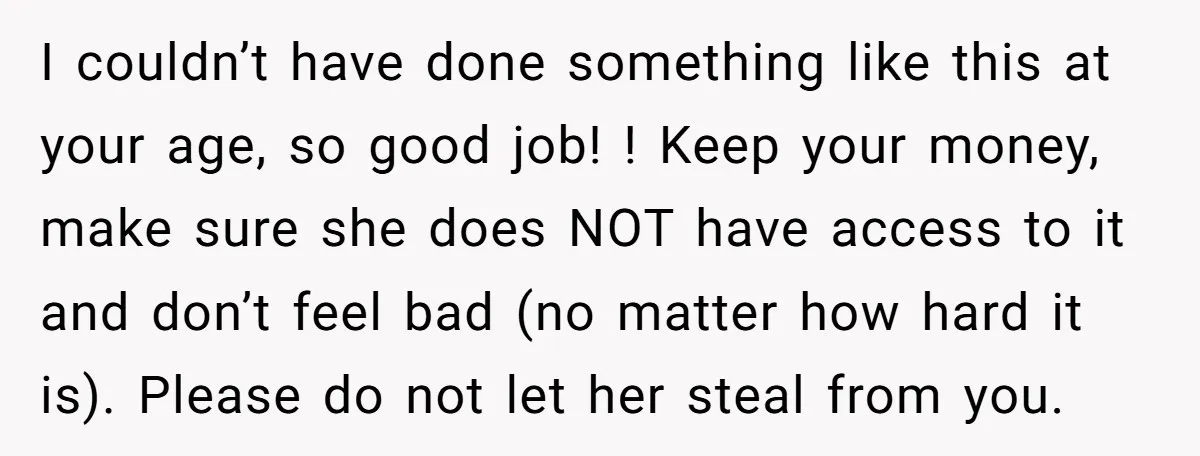

The online community overwhelmingly supported the teen (NTA), praising his discipline and urging him to protect his savings from what many called financial abuse or manipulation. Comments grouped into streams:

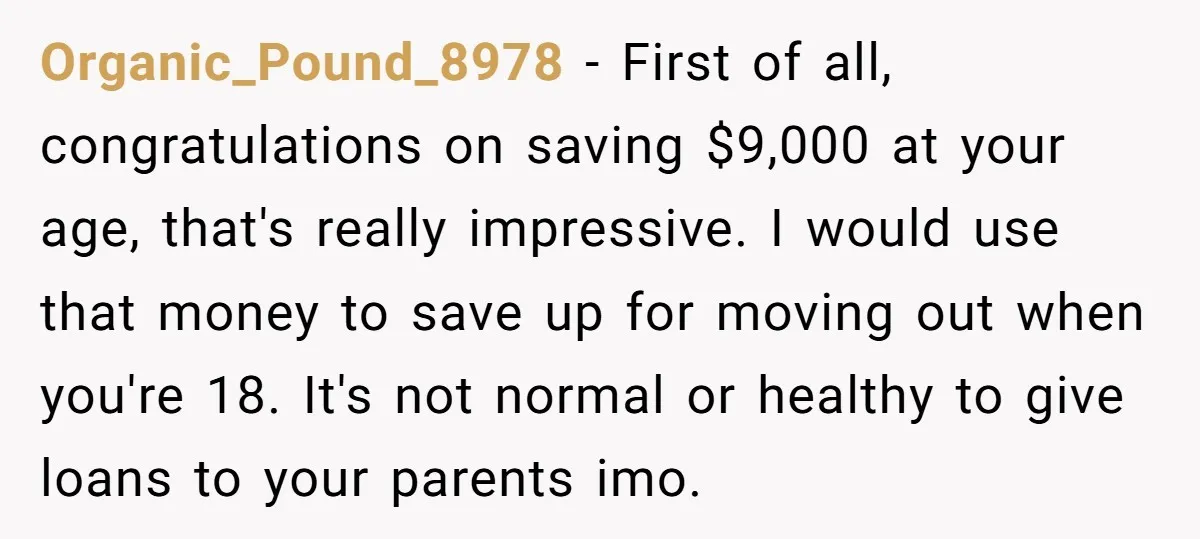

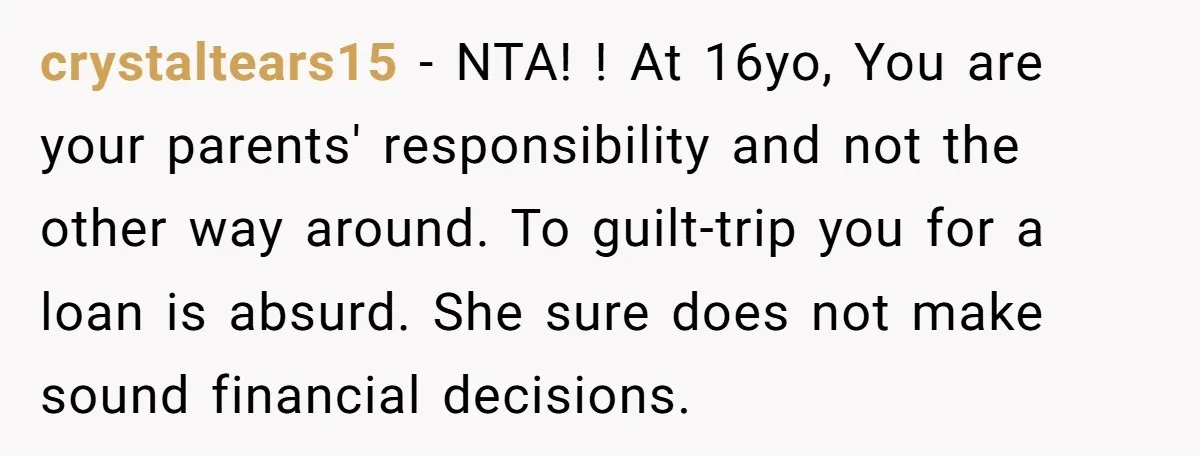

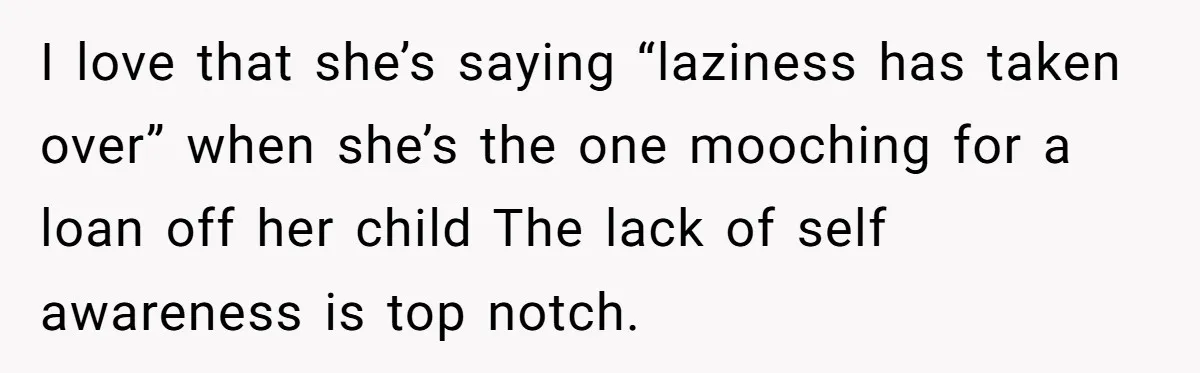

Strong praise for the teen’s hard work and advice to keep the money safe (most common theme):

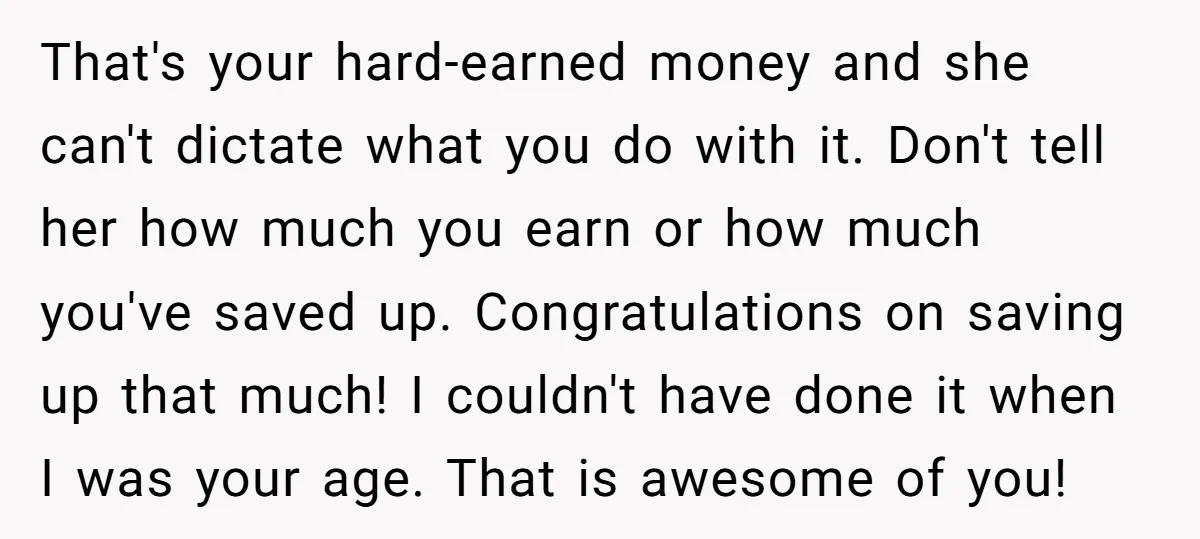

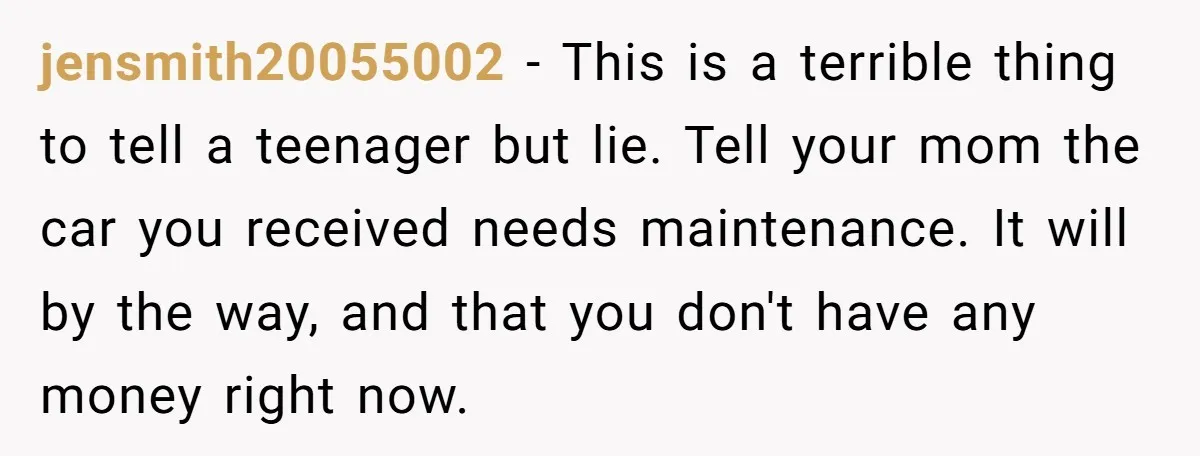

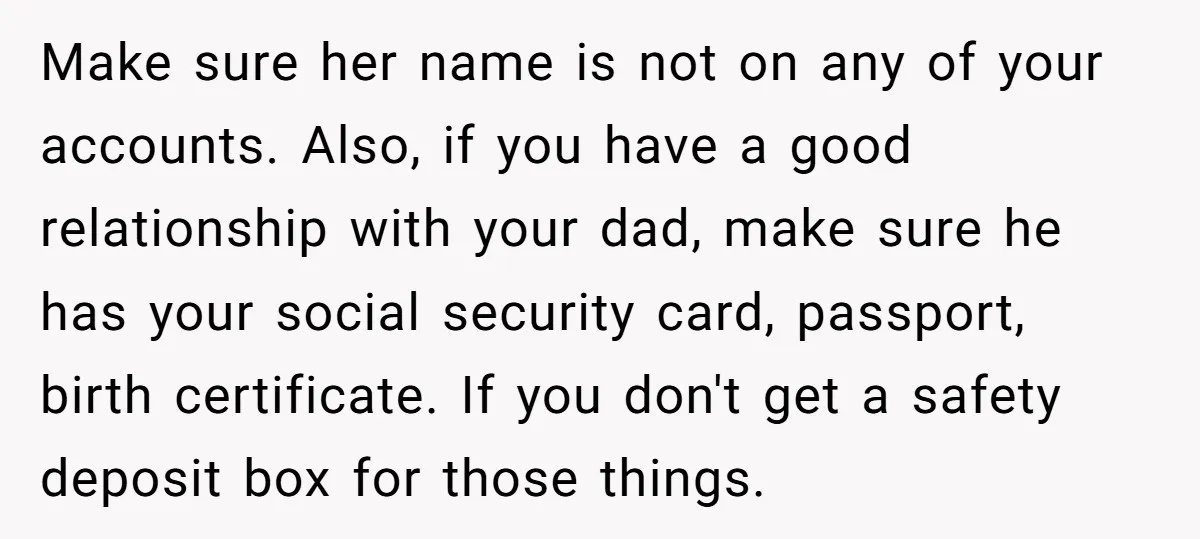

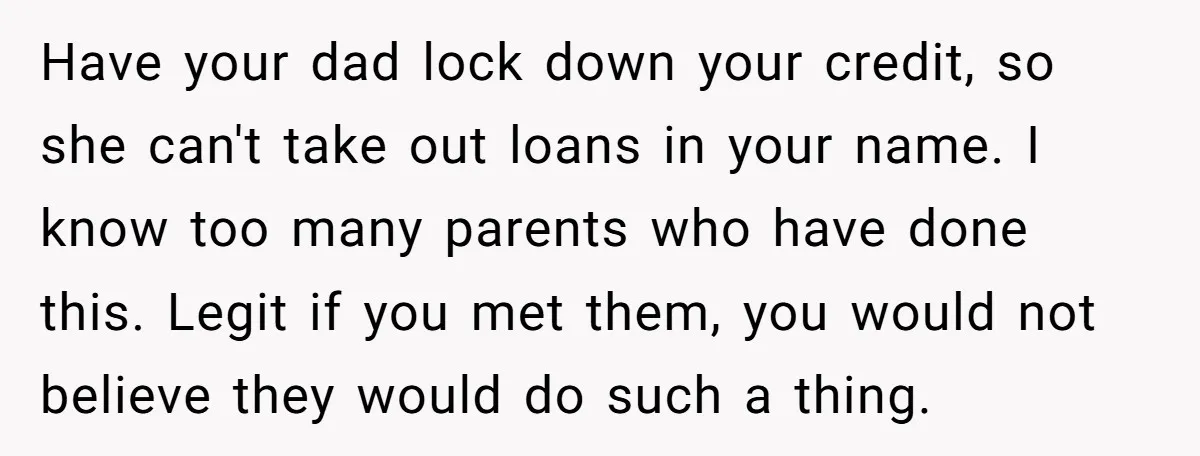

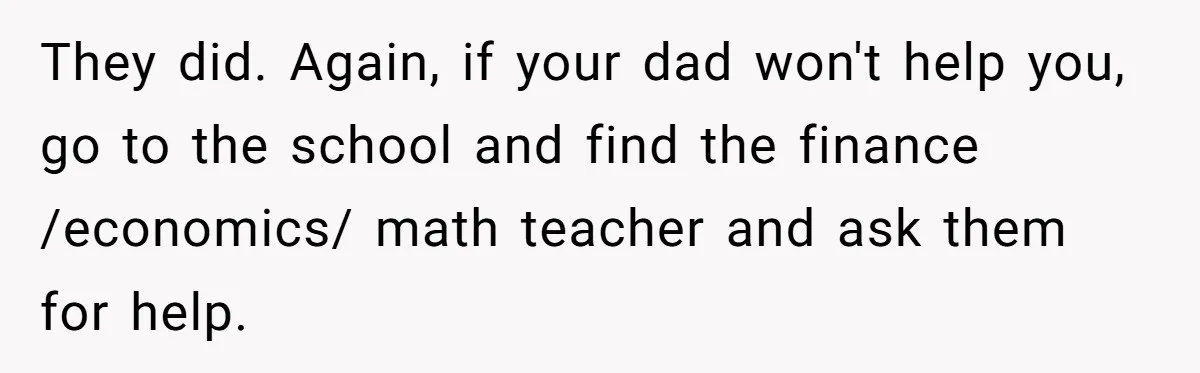

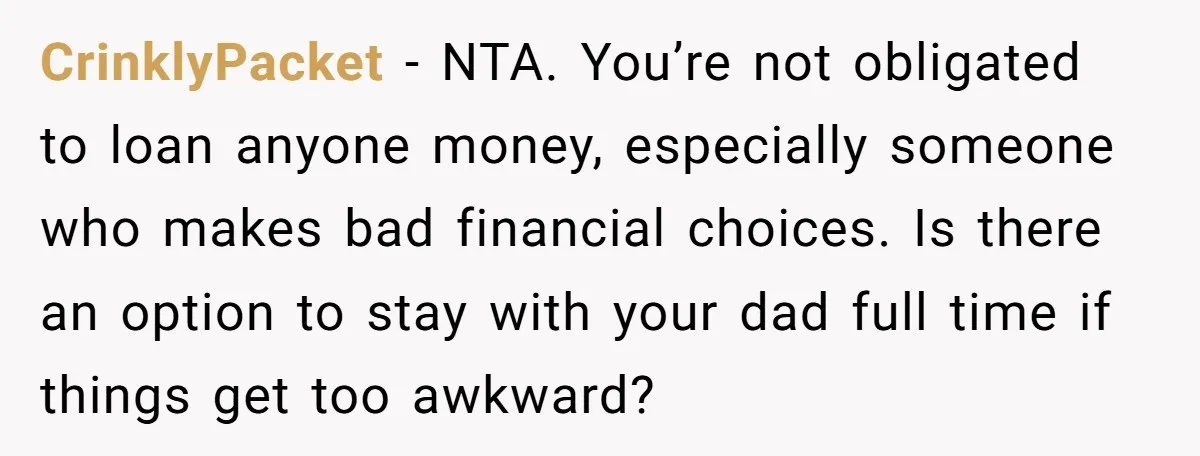

Practical advice on protection (lock accounts, involve dad, secure documents):

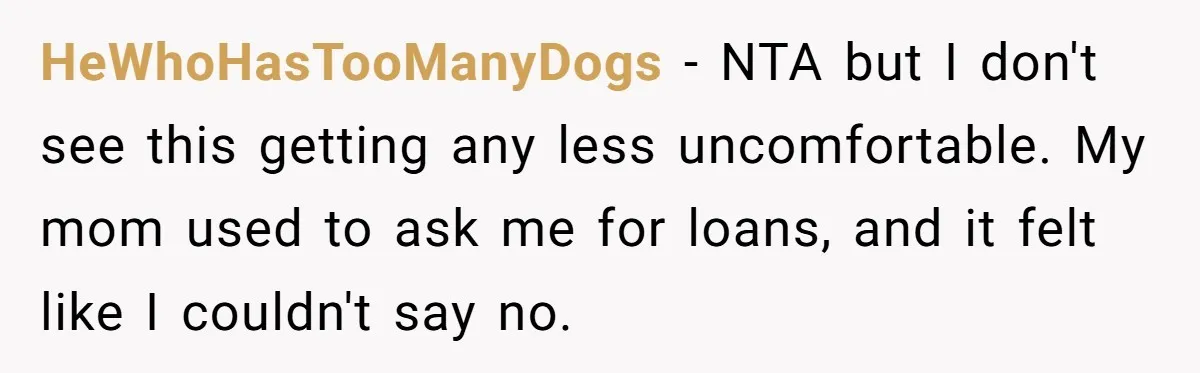

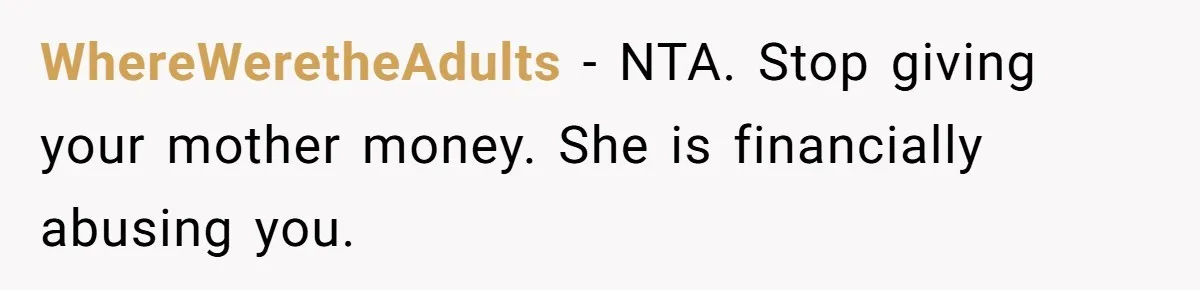

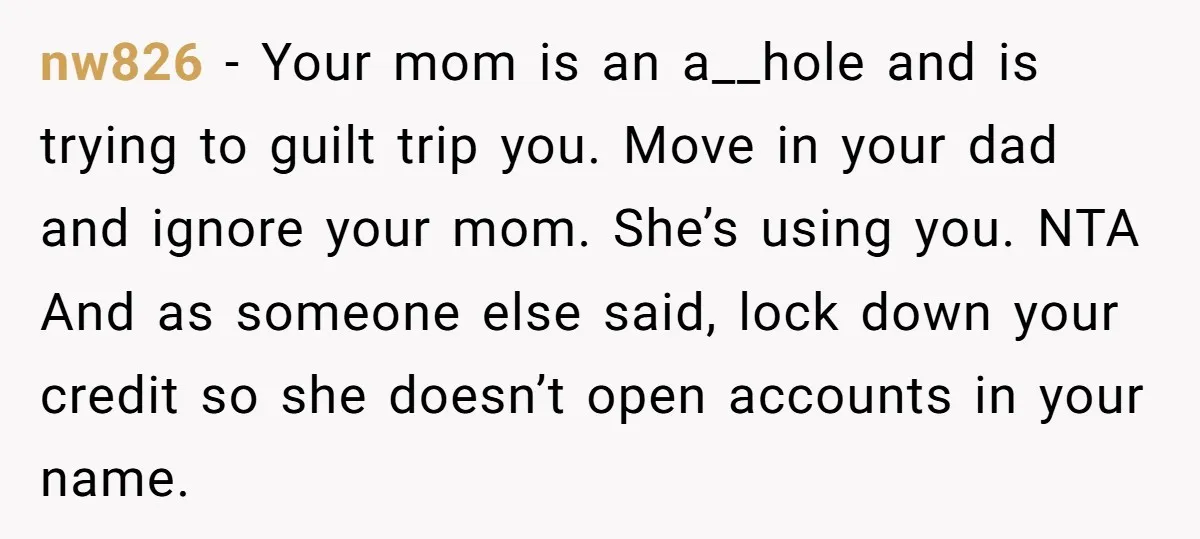

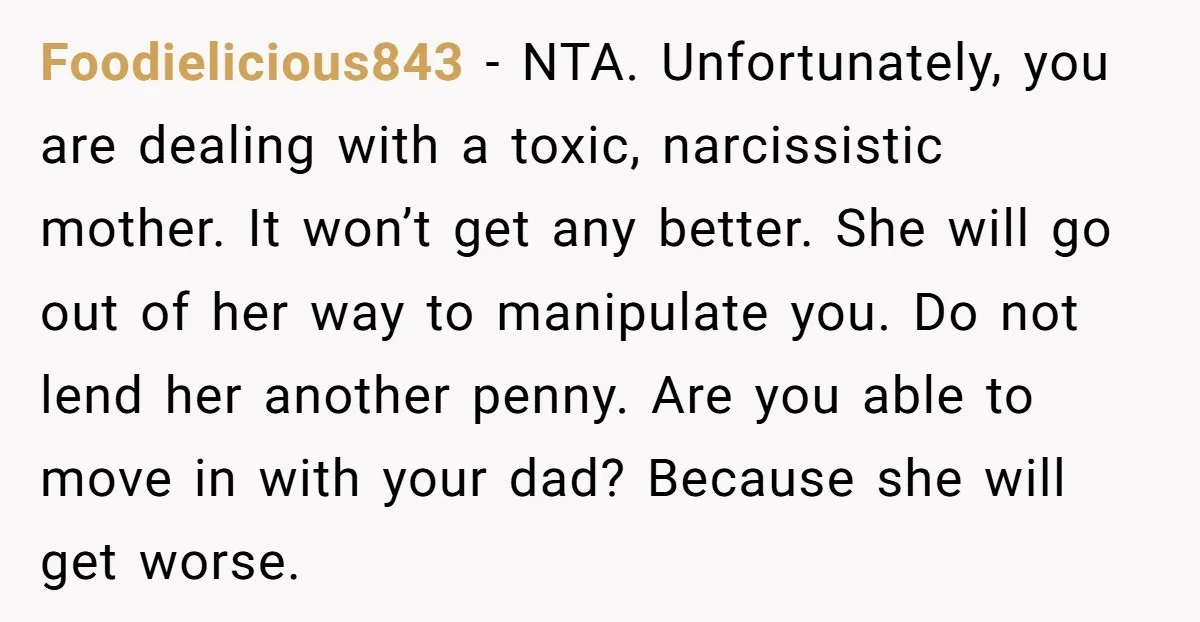

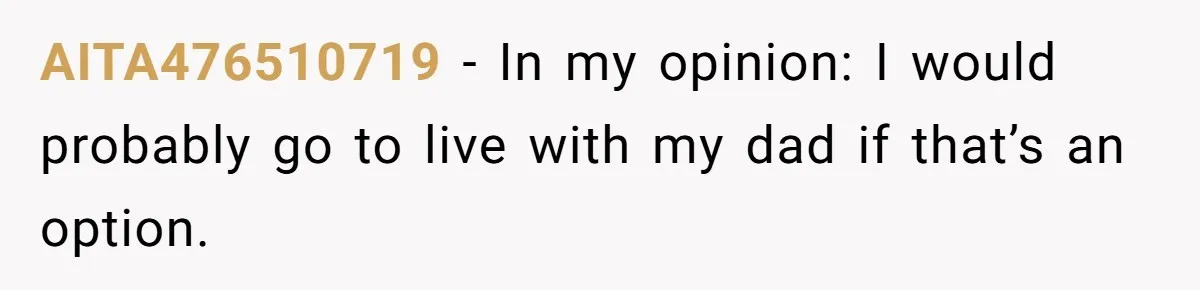

Calls it financial abuse/toxic behavior, suggest moving to dad’s or cutting contact if needed:

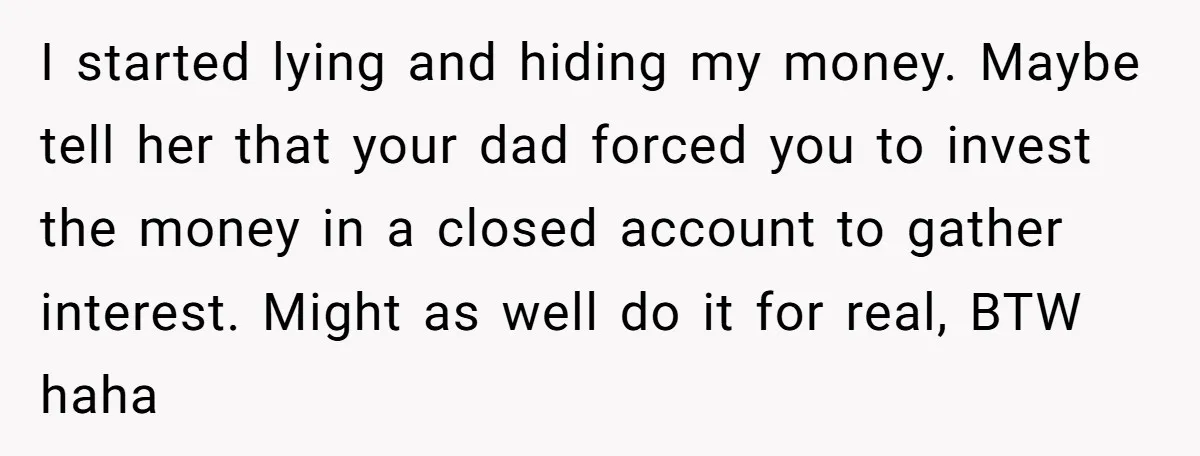

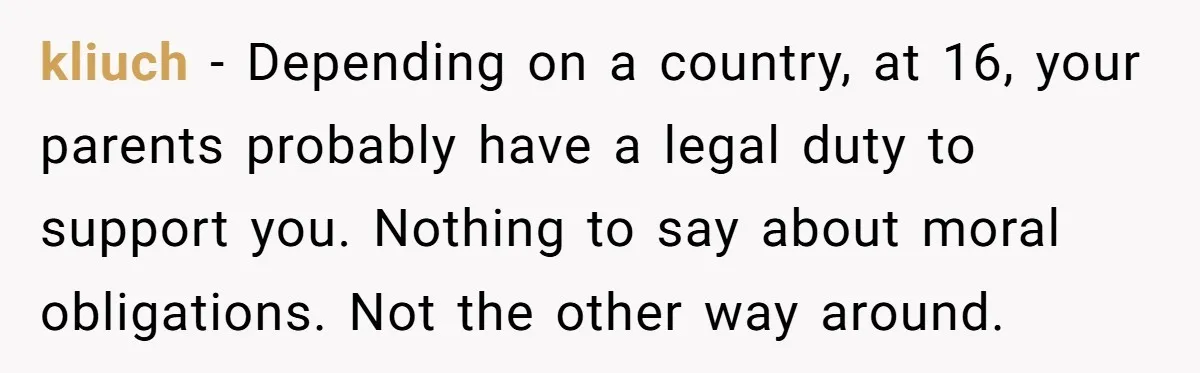

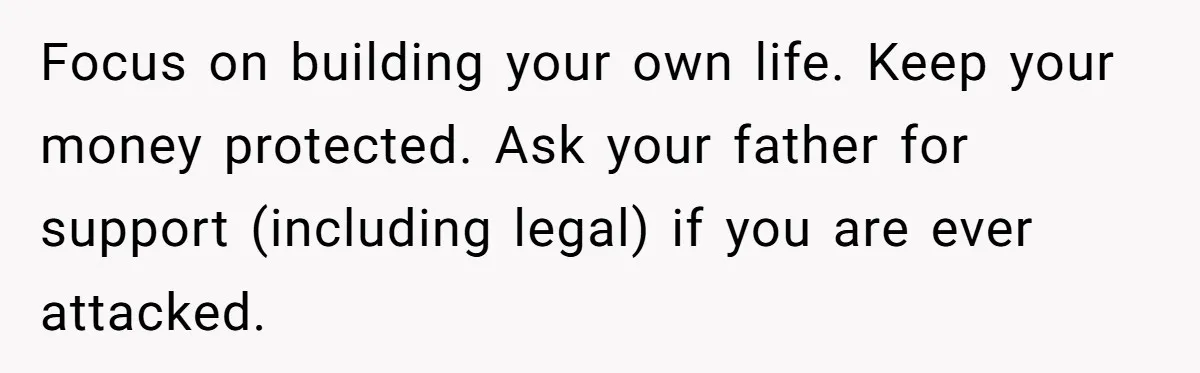

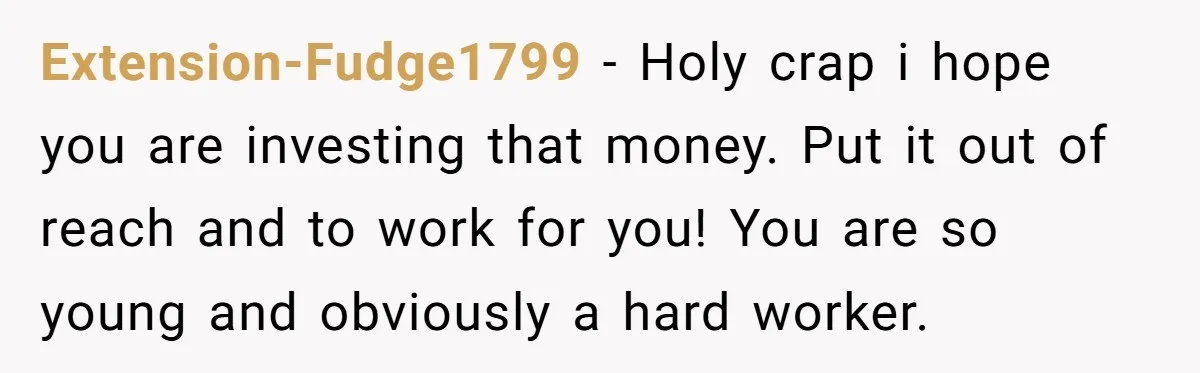

Other supportive notes (legal duty, invest the money):

This teen’s story highlights how hard-earned savings can become a flashpoint when a parent struggles with money management and leans on guilt instead of accountability. Saying no to loans isn’t unloving—it’s smart self-protection, especially when past “repayments” are slow and new requests keep coming. The community agreed: prioritize your future over fixing someone else’s poor choices.

Have you ever been pressured for money by family as a teen? How did you handle it? Share your experiences below—your perspective might help others in similar spots navigate these tough family dynamics!