AITA for Keeping My Daughter’s College Fund from Her?

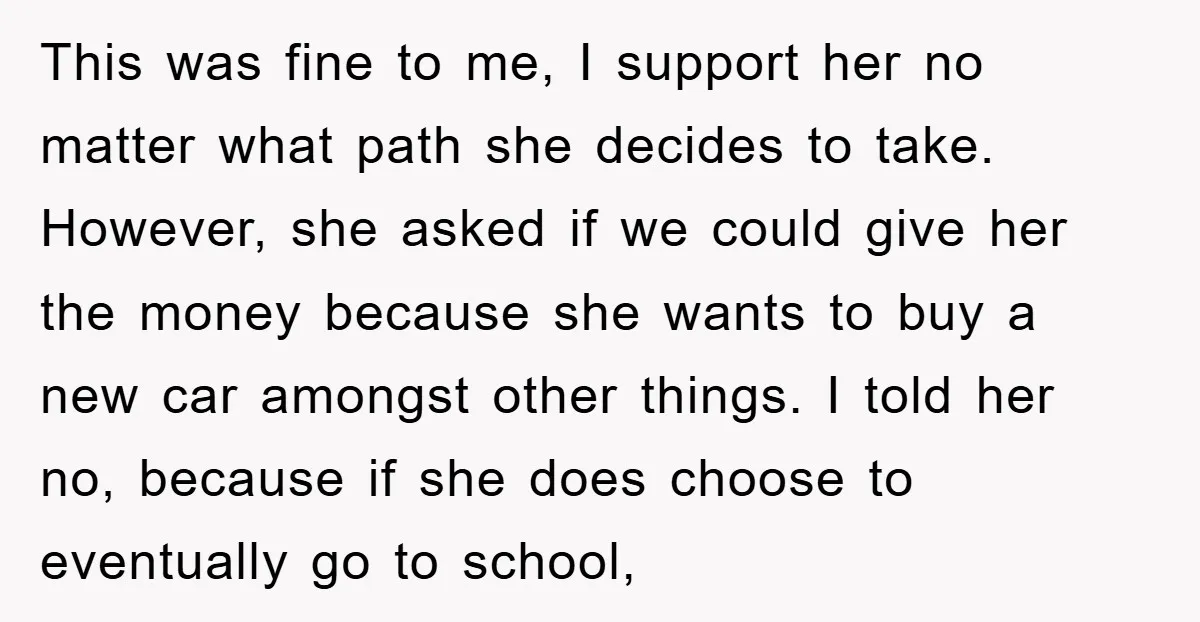

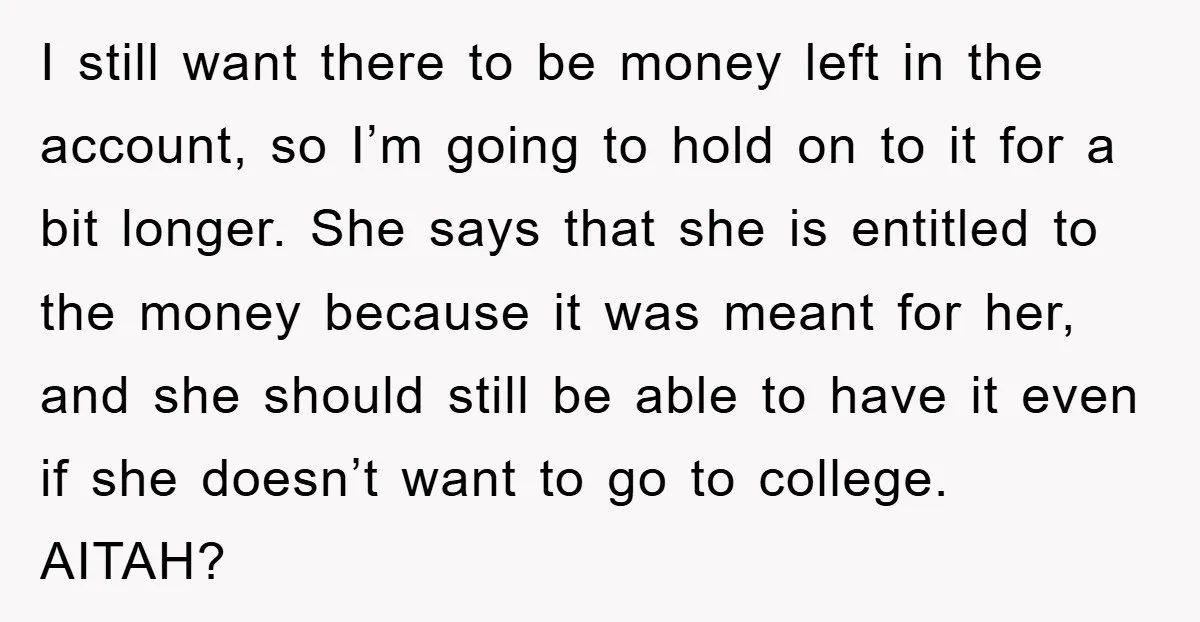

A mother and father saved nearly $200,000 for their daughter’s college education, but at 17, she wants to skip the traditional college path, get a job, and use the fund for a car and other expenses. Supporting her choice to explore her future, they refused her request for the money, wanting to preserve it for potential education later. She argues she’s entitled to it since it’s “for her.”

Now, with tensions high, they’re questioning if holding firm was fair or overly controlling. This story dives into the clash of parental foresight, teenage autonomy, and the purpose of a college fund. Were they right to say no, or is she entitled to the money?

‘AITA for Keeping My Daughter’s College Fund from Her?’

The conflict began when their daughter rejected the college path:

Her request for the college fund sparked a firm refusal:

This couple’s decision to withhold their daughter’s college fund reflects prudent foresight, prioritizing her long-term opportunities over immediate wants. At 17, her desire to skip college and explore other paths is valid, but her claim to the $200,000 as “her money” overlooks the fund’s specific purpose: education. Handing over such a large sum to a teenager, even a responsible one, risks reckless spending, as impulse control and financial literacy are still developing at her age. Studies show that young adults often mismanage windfalls without guidance (Kahneman, Thinking, Fast and Slow).

The parents’ support for her non-traditional path is commendable, but their refusal to release the fund is wise, especially if it’s in a 529 plan, where non-educational withdrawals incur penalties and taxes. Her argument that the money is “for her” ignores their intent as the savers—it’s for her education, not discretionary spending. Dr. Laura Markham notes, “Setting boundaries with teens teaches them responsibility while showing love” (Peaceful Parent, Happy Kids). By holding the fund, they’re protecting her future options, as she may later choose college or trade school.

Still, her frustration suggests she feels unheard. They could validate her autonomy by discussing alternative uses for part of the fund later—like a business venture or vocational training—if she remains set against college. A compromise, like offering a small amount for a modest car if she meets certain goals (e.g., steady employment), could bridge the gap. For now, keeping the fund intact and having an open conversation about its purpose, perhaps setting a future age (e.g., 25) for reevaluating its use, is a balanced approach. They should also clarify the fund’s legal status and their control over it to avoid further entitlement claims.

Here’s what the community had to contribute:

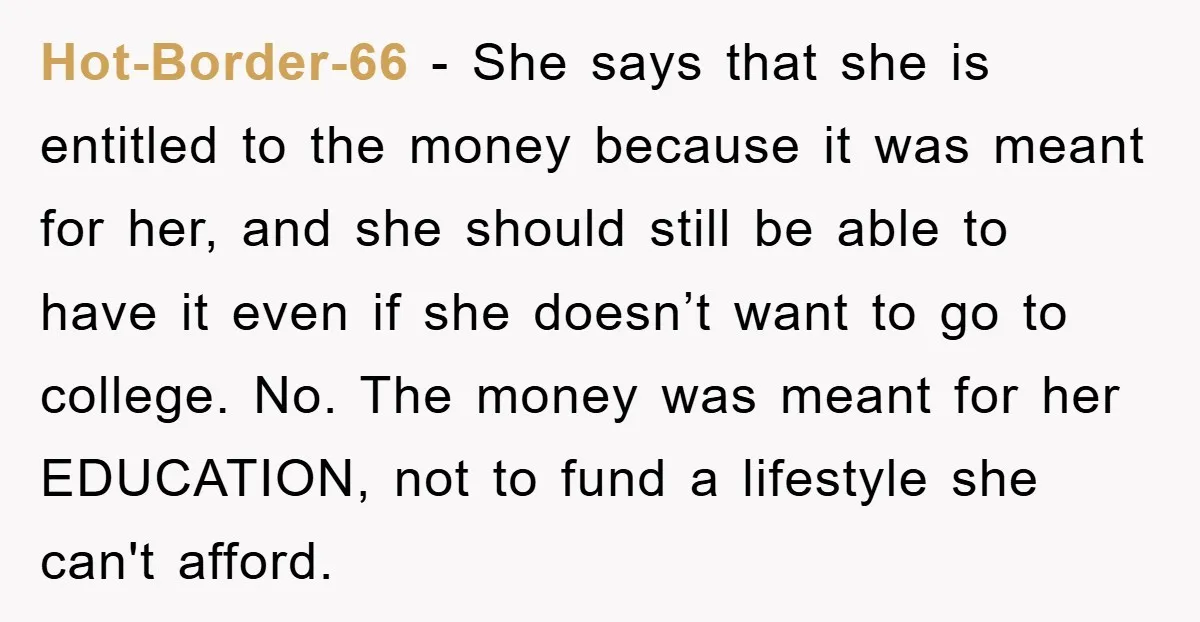

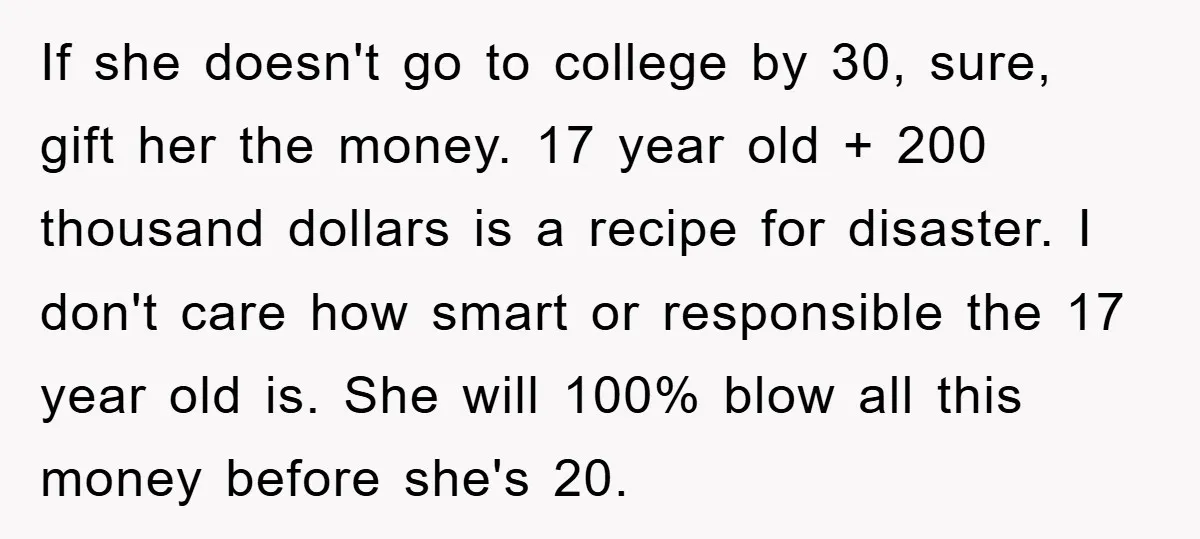

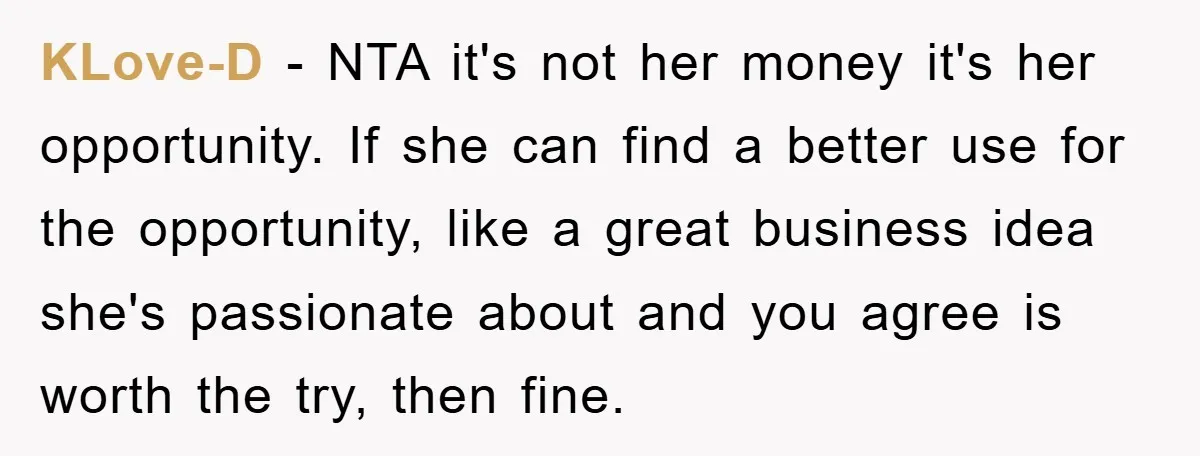

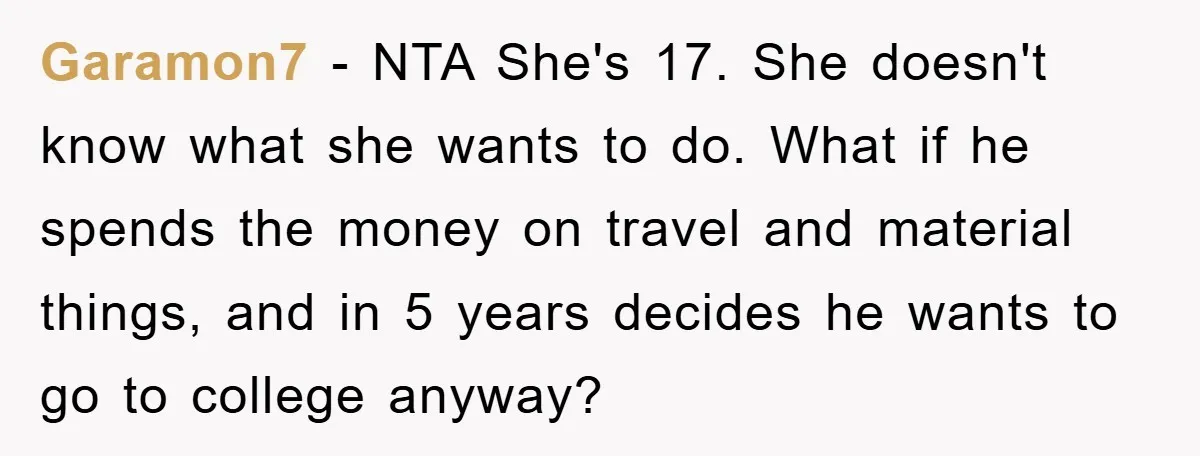

Social media users jumped into the debate, offering varied perspectives: Many backed the parents, stressing the fund’s specific purpose:

Others highlighted practical and legal considerations:

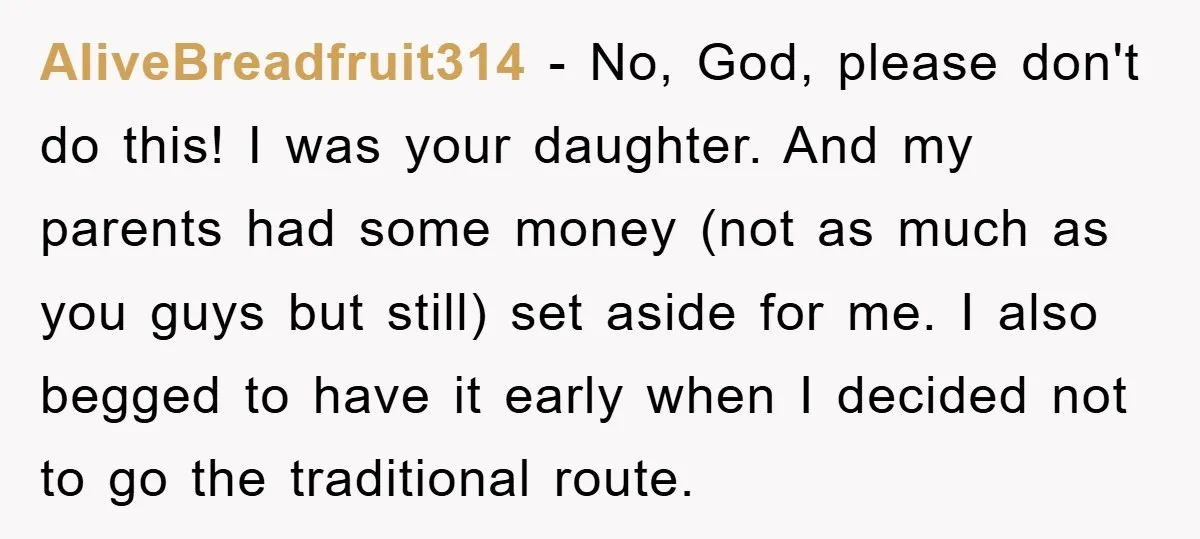

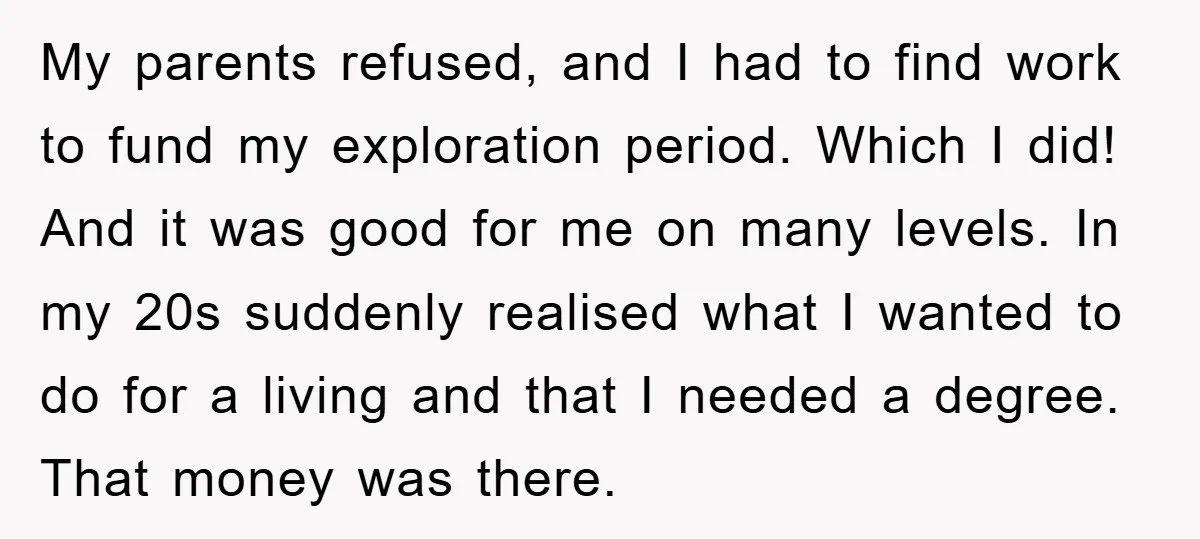

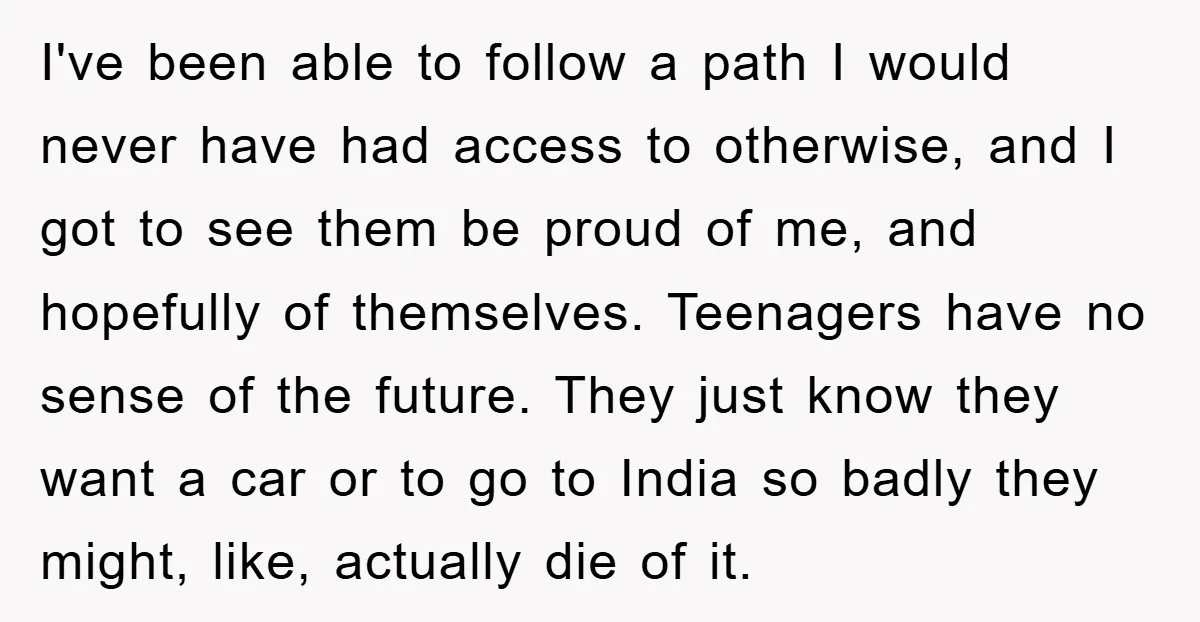

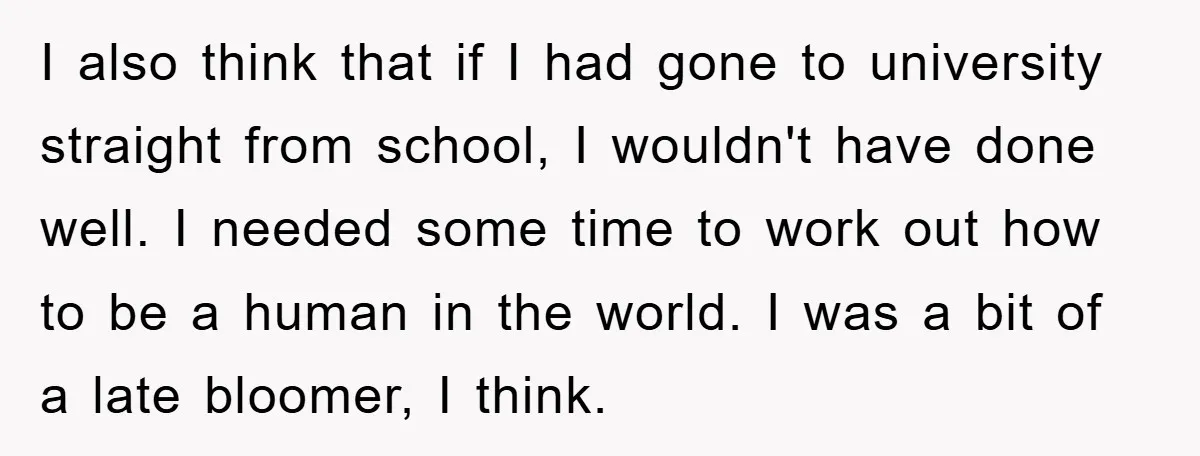

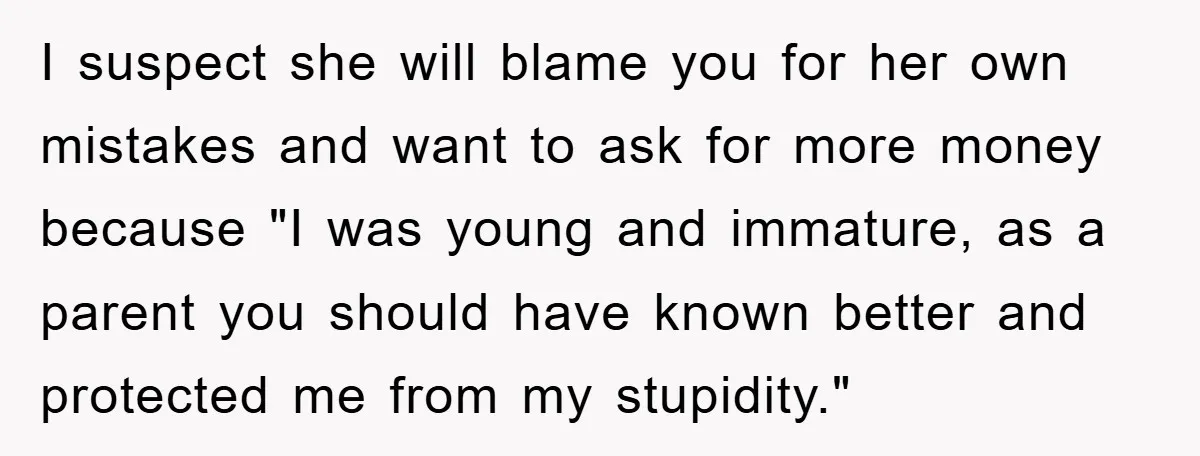

Some shared personal stories, relating to both sides:

![[Reddit User] - You are not the a__hole, and one day your daughter will realize that too. I think it’s hard to see the bigger picture when you’re young, and...](https://en.aubtu.biz/wp-content/uploads/2025/11/wp-editor-1762479027899-6.webp)

![[Reddit User] - i’m 20 taking a gap year. i have a 529 that will cover the remainder of my college and i would never dream of asking for access...](https://en.aubtu.biz/wp-content/uploads/2025/11/wp-editor-1762479030223-8.webp)

The parents chose to protect the $200,000 college fund for its intended purpose—education—despite their daughter’s objections. They support her non-traditional path but want to ensure her future isn’t compromised by impulsive choices at 17. Their stance reflects care, though the family tension highlights a need for better communication to address her feelings.

Should the daughter have a say in how the fund is used, or are the parents right to hold firm? What would you do in their shoes? Share your thoughts below!