AITA for getting angry at my husband after he refused to contribute to our child’s education savings plan?

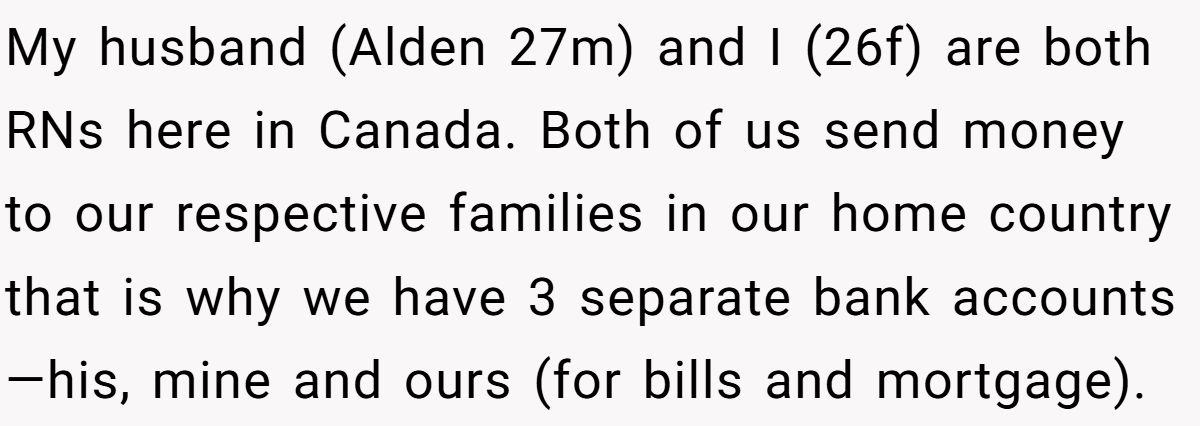

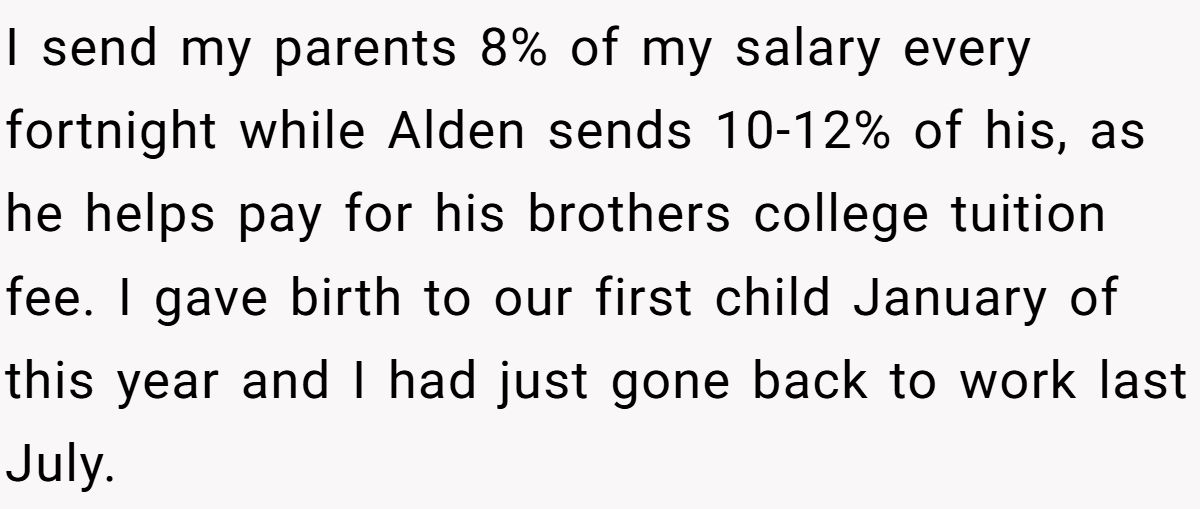

In a cozy Canadian home, two young RNs juggle love, work, and family ties across continents. The original poster (OP), a 26-year-old new mom, and her husband Alden, 27, balance separate finances to support their families abroad. But when OP suggests starting a college savings plan for their newborn son, Alden’s refusal—citing his brother’s tuition and family pressures—ignites a fiery clash. His rejection of even a small contribution, paired with accusations of stripping his stress relievers like Netflix, sends OP storming out, nearly hurling her phone.

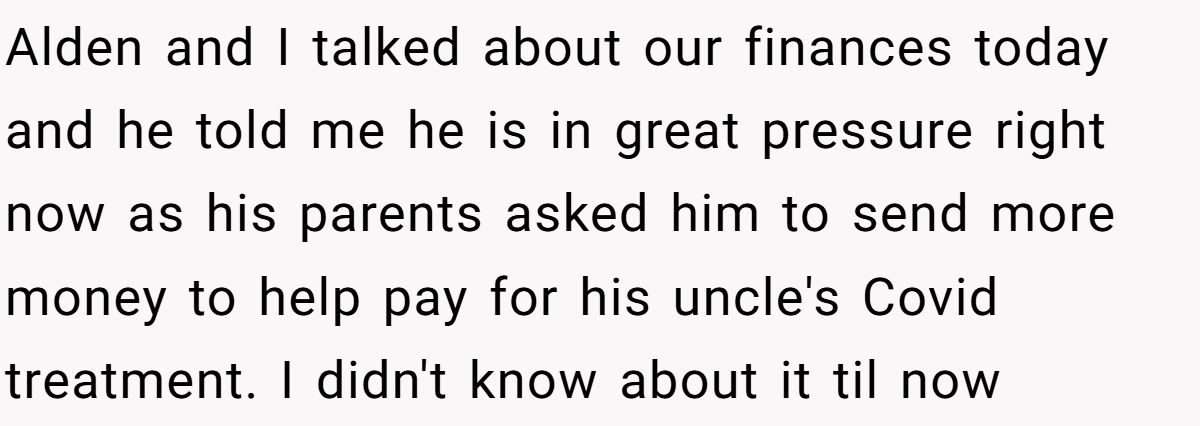

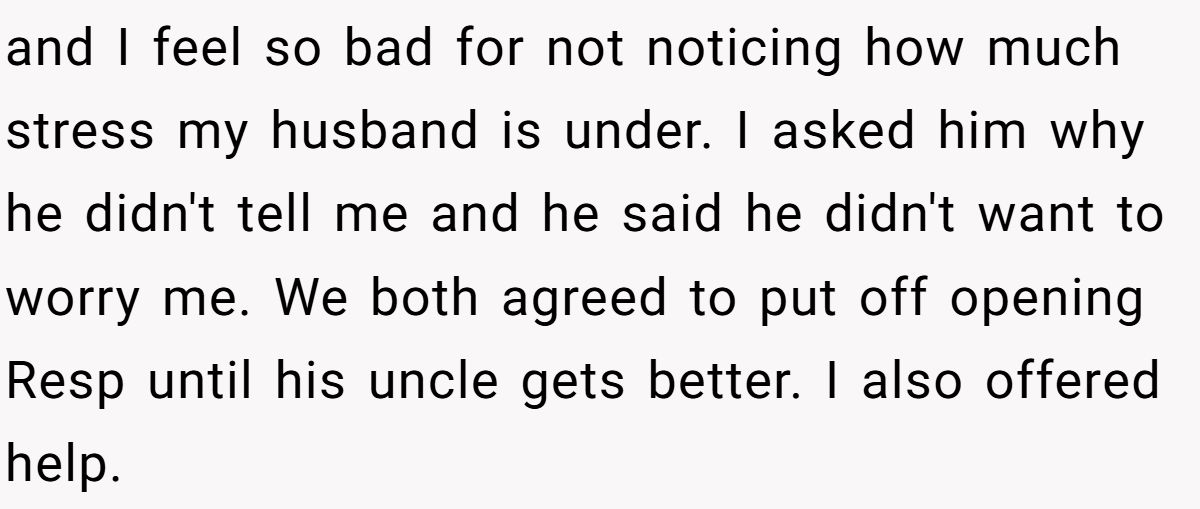

The couple’s silence lingers until a heartfelt talk reveals Alden’s hidden stress over his uncle’s medical bills, pausing their savings plan. Was OP’s anger justified, or did she overlook her husband’s burdens? This tale dives into the messy intersection of marital finances, family duties, and new parenthood, where good intentions spark heated fights.

‘AITA for getting angry at my husband after he refused to contribute to our child’s education savings plan?’

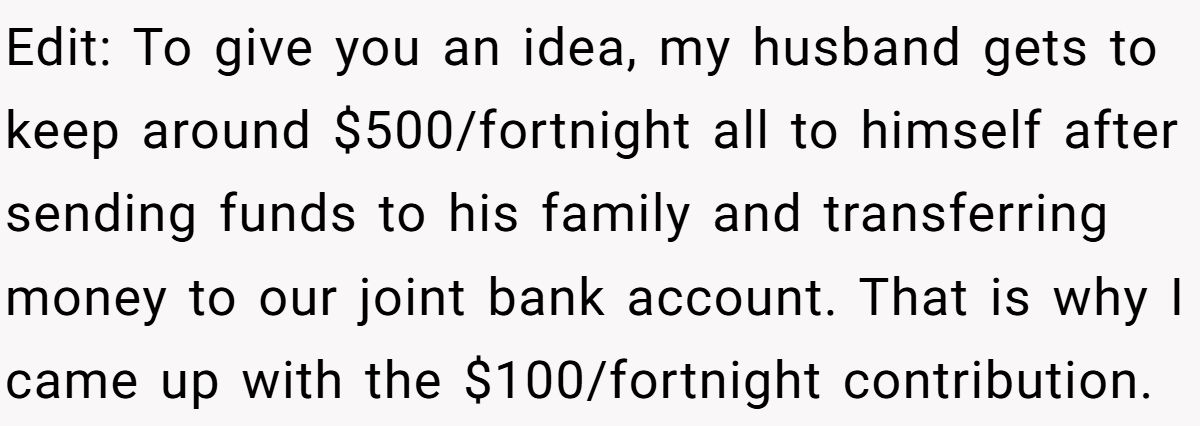

Money talks can turn marriages into battlegrounds, and OP’s push for a college savings plan hit a nerve with Alden’s existing obligations. Her proposal for a $100/fortnight RESP contribution is practical, leveraging Canada’s tax-advantaged plan to secure their son’s future. Dr. David de Rosenroll, a financial therapist, notes, “Couples must align on financial priorities to avoid resentment” (Money and Marriage, 2018). OP’s anger stems from Alden’s refusal to prioritize their child, especially with $500/fortnight in discretionary funds, though his family’s medical crisis explains his stress.

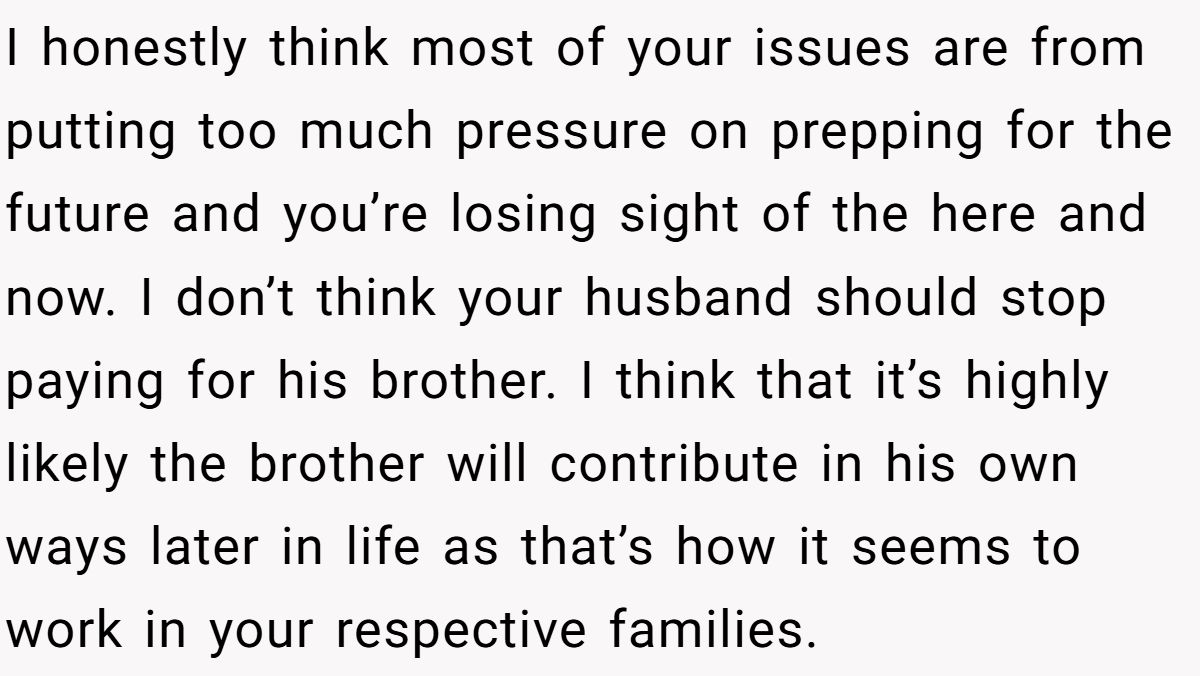

Alden’s perspective reveals a cultural and familial bind. Supporting his brother’s education and now his uncle’s treatment reflects a common collectivist duty, but his defensive reaction—escalating over Netflix and Xbox—signals poor communication. His failure to share the uncle’s situation earlier left OP blindsided, fueling her frustration. A 2023 Journal of Family and Economic Issues study found 65% of couples face financial disputes when external family demands clash with household goals, often due to unspoken pressures.

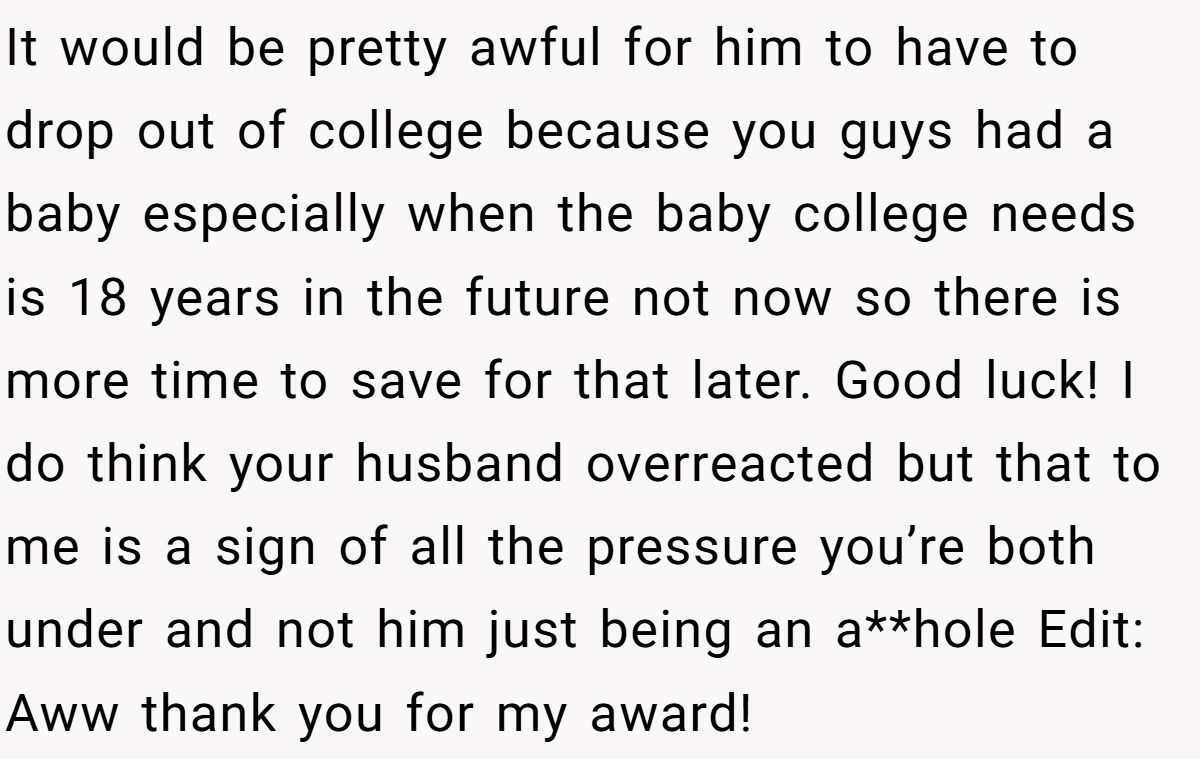

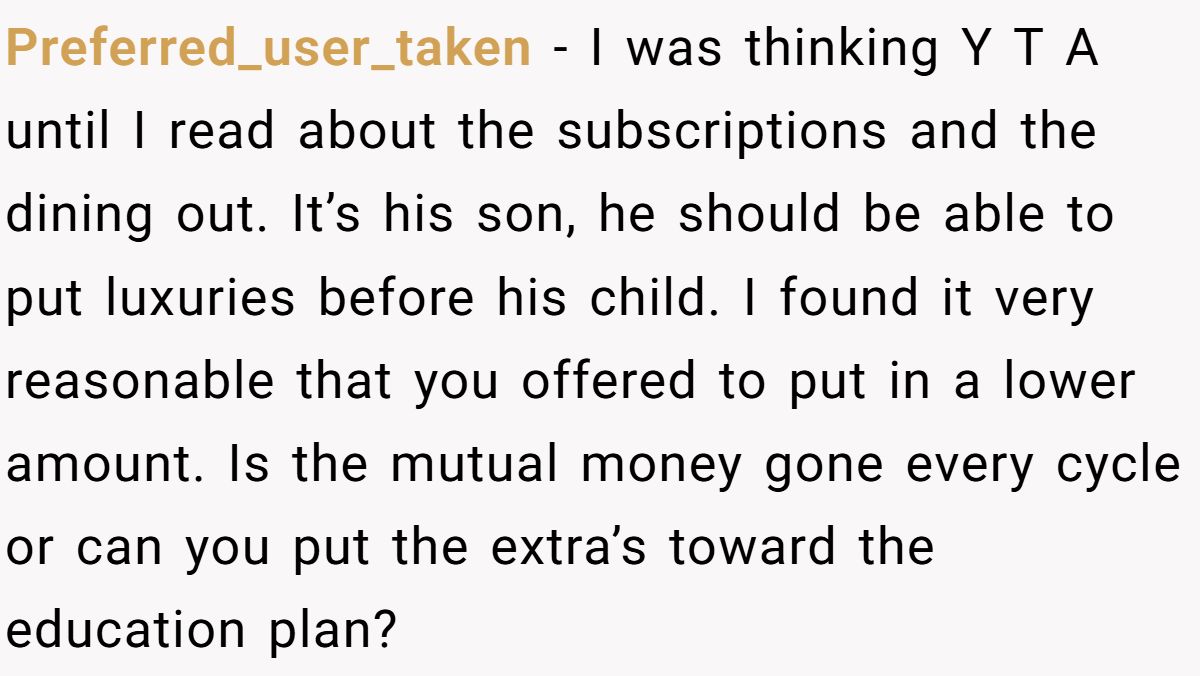

OP’s willingness to compromise ($20-$50/fortnight) shows flexibility, but Alden’s outright refusal shut down dialogue. Their eventual talk and decision to pause the RESP is a step forward, but long-term harmony requires transparency. A joint budget review, possibly with a financial planner, could balance family support with their son’s future. Cutting small luxuries, like dining out, could free up funds without stripping stress relievers, fostering teamwork over tension.

Here’s what people had to say to OP:

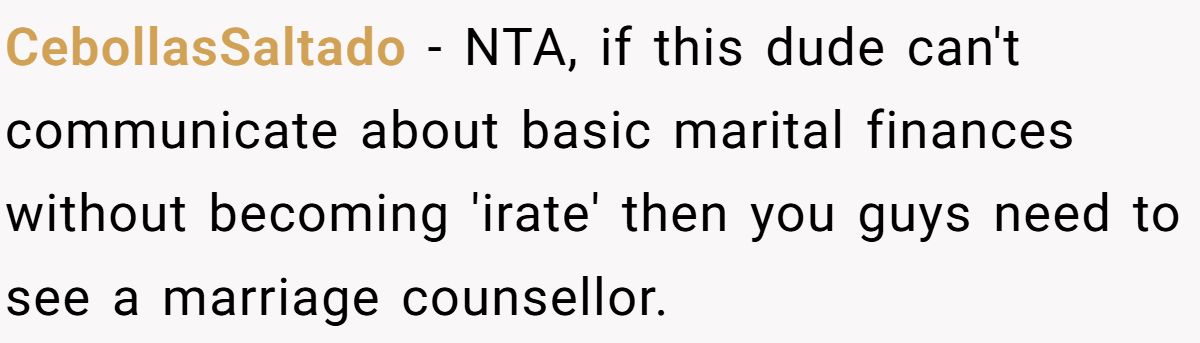

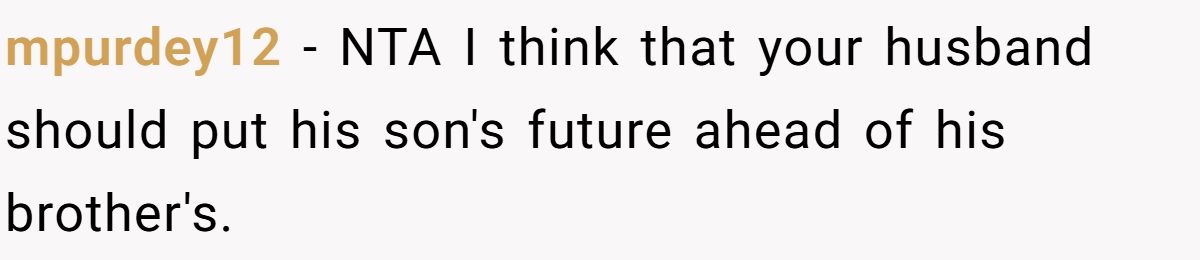

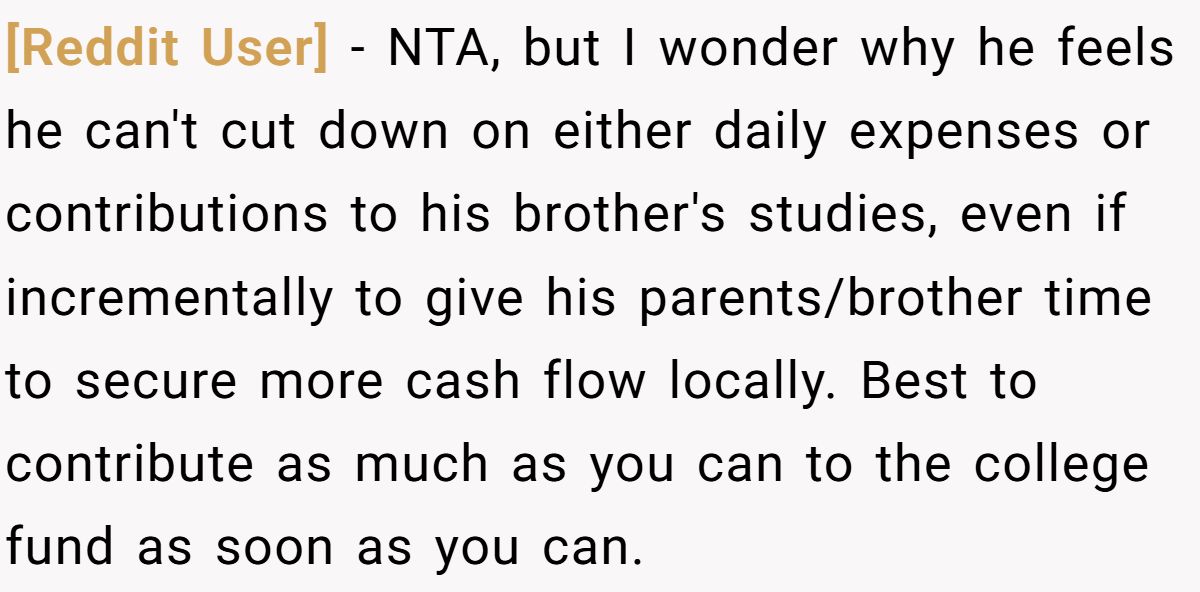

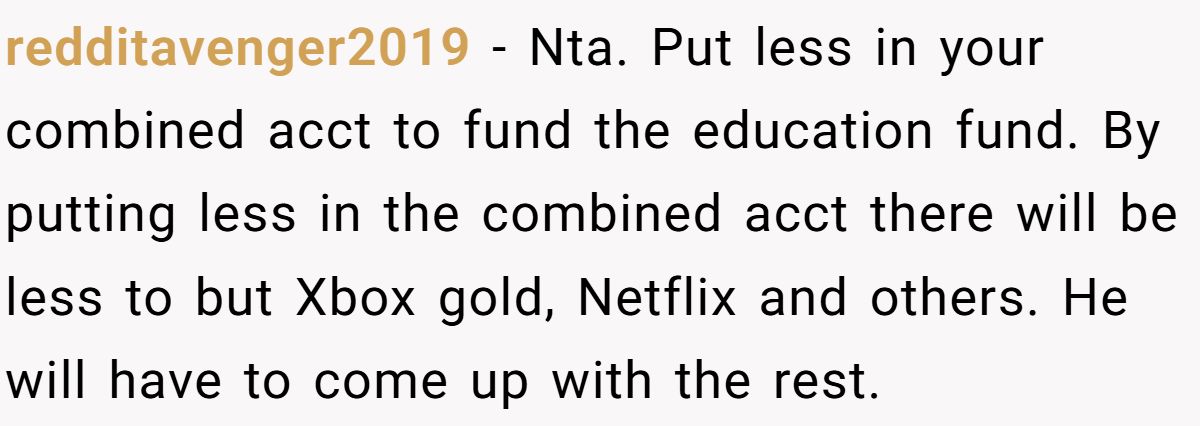

Reddit mostly backs OP, arguing Alden should prioritize their son over extended family, especially with disposable income. Users criticize his “irate” reaction and dismissal of compromises, seeing it as dodging responsibility. Some suggest redirecting joint account funds to force shared sacrifices, while others note his family pressures but stress communication failures.

A few see no assholes, citing the couple’s mutual stress—new parenthood for OP, family burdens for Alden. Humor surfaces with jabs at Alden’s “stress reliever” excuses, but practical advice includes marriage counseling or financial planning. Reddit’s mix of support and wit leans toward OP, urging Alden to step up for their child while acknowledging his family’s pull.

This financial feud highlights how family obligations can strain a marriage. OP’s anger was fueled by Alden’s refusal to budge, but his hidden pressures reveal a communication gap. Their pause on the RESP shows progress, but transparency is key. Ever clashed with a partner over money priorities? Share your stories below—how do you balance family duties with your own household’s needs?