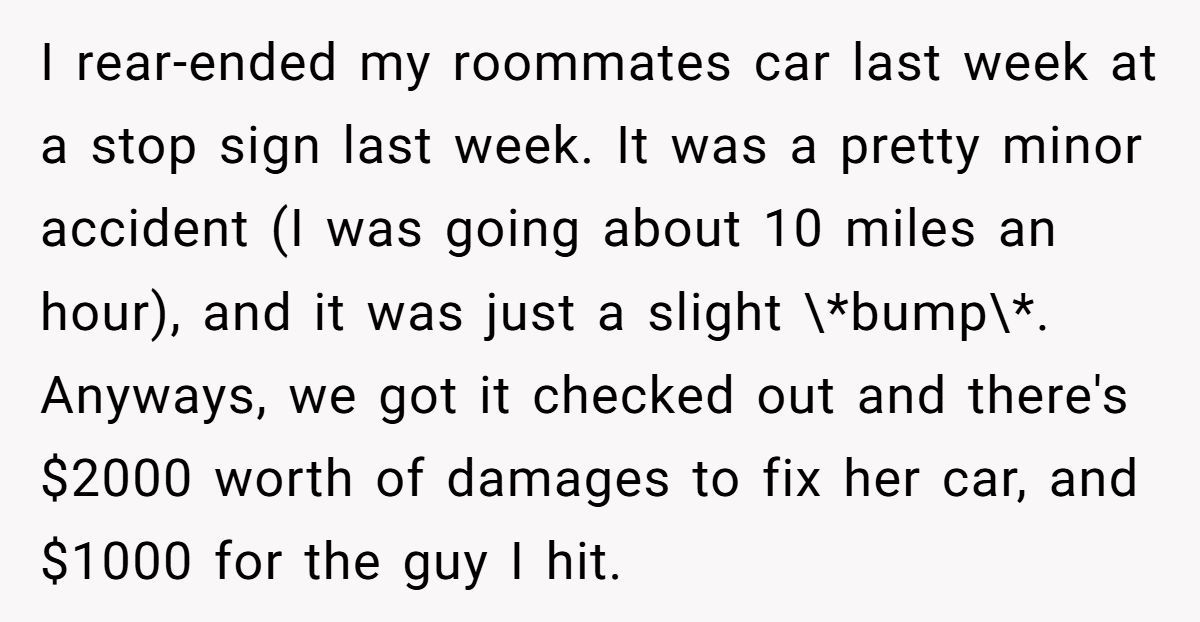

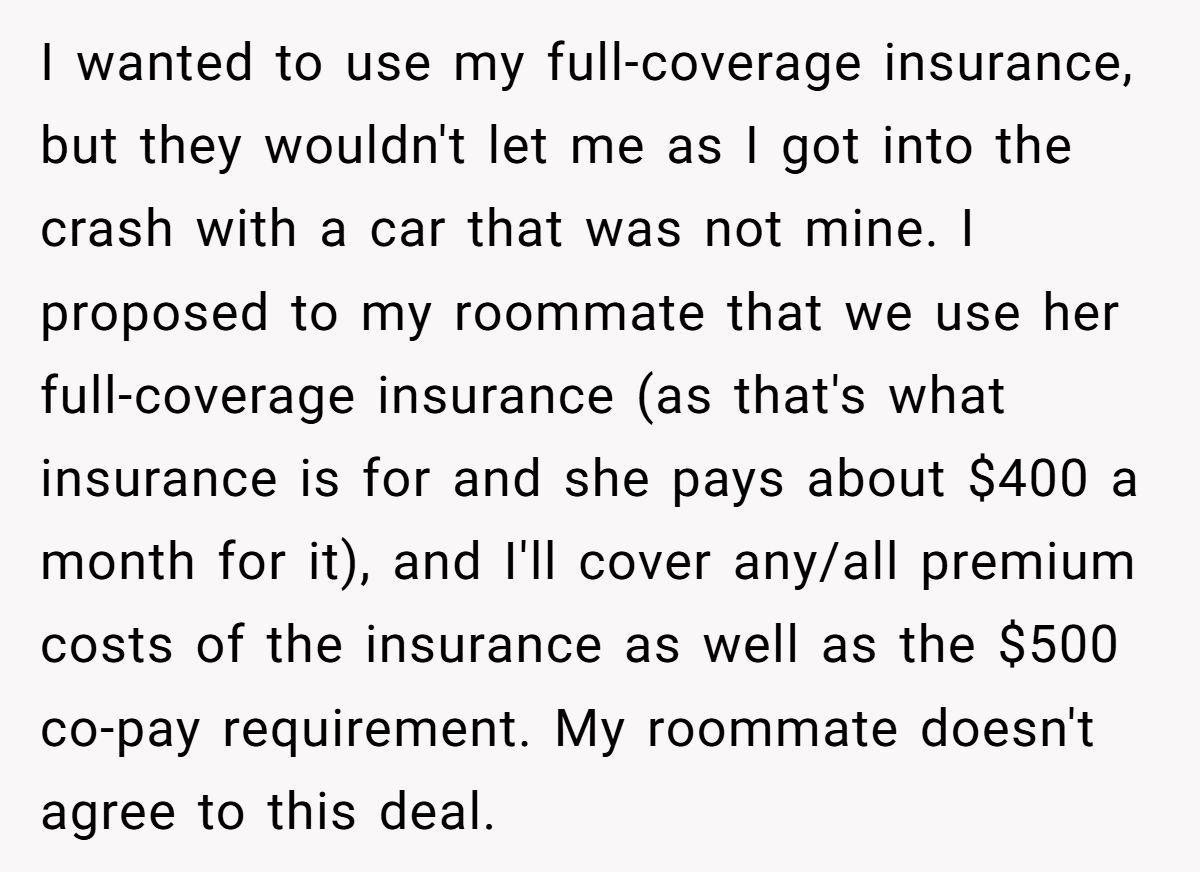

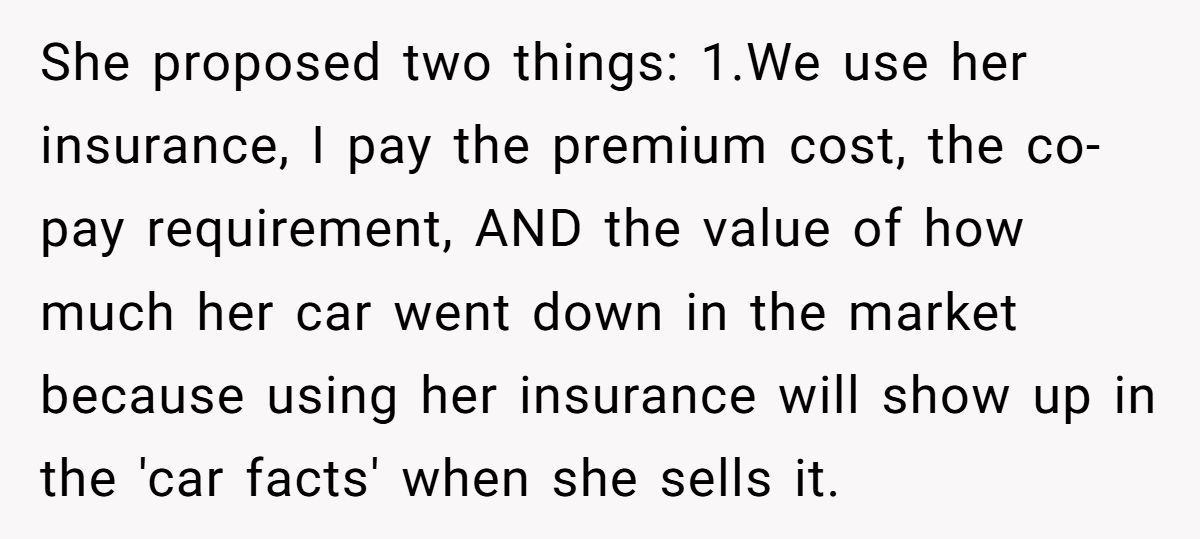

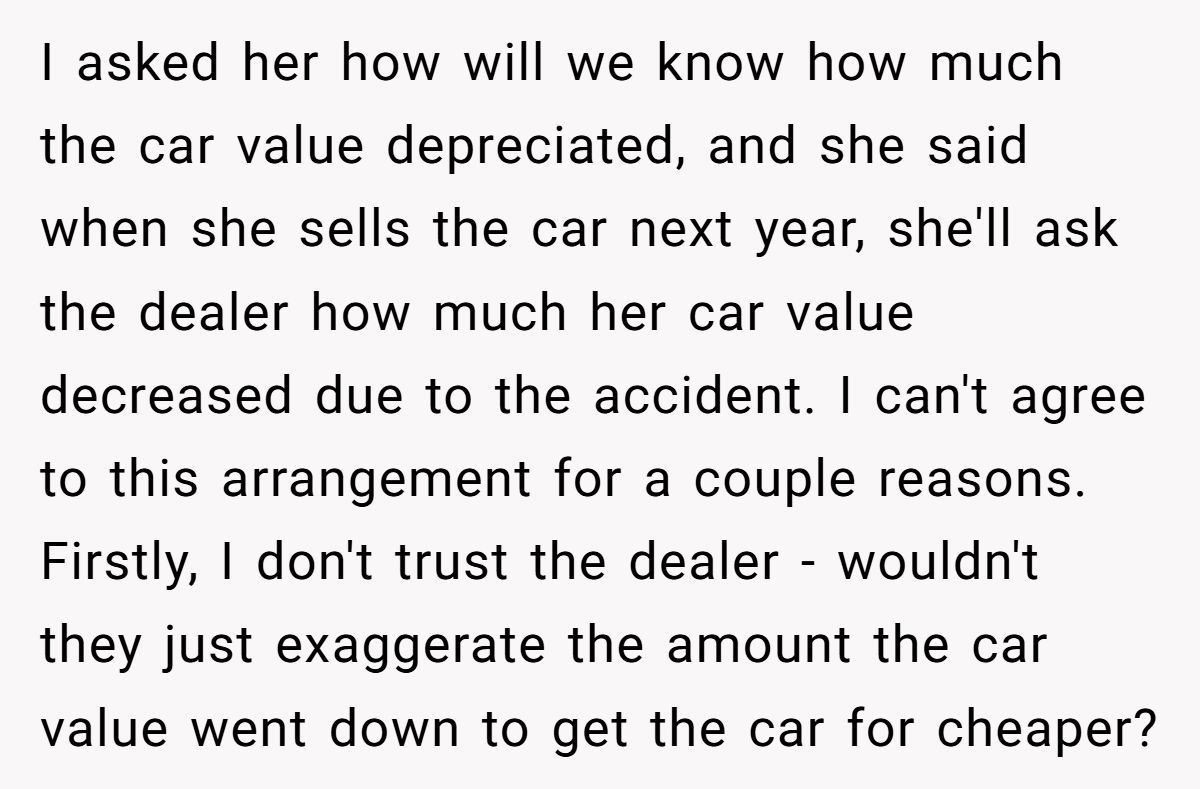

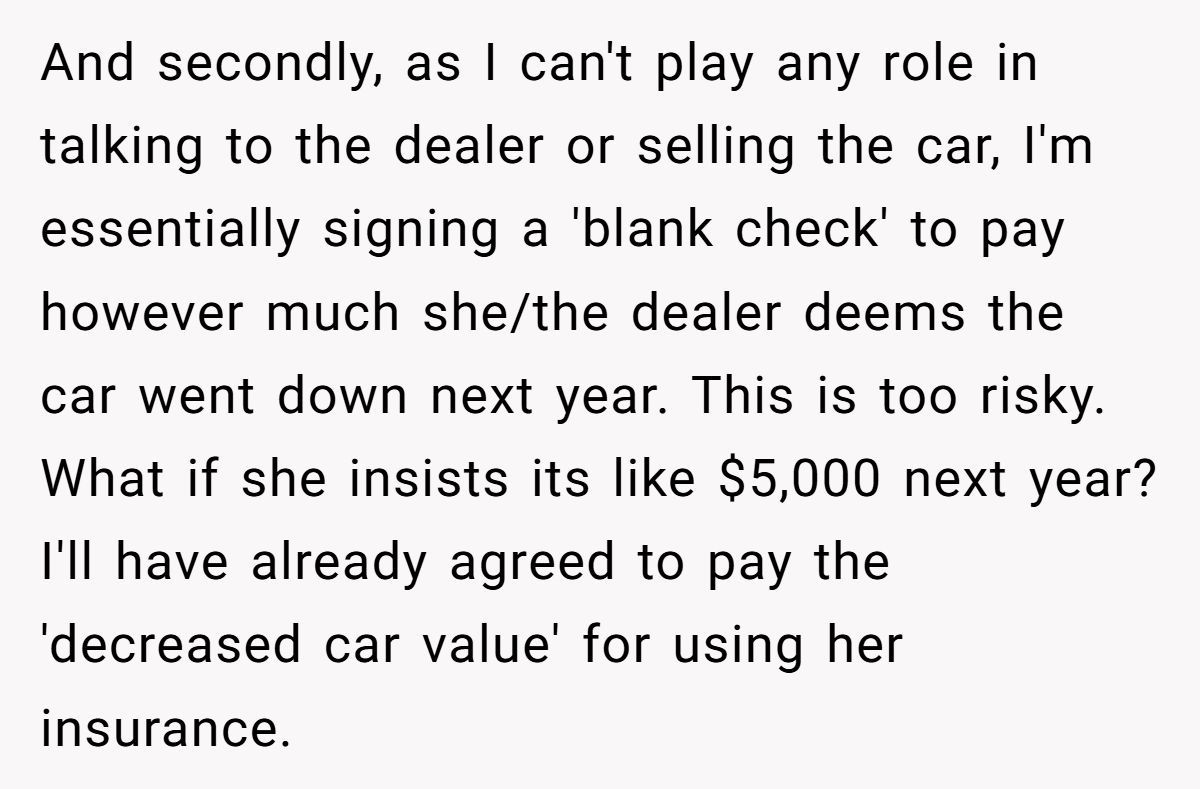

AITA for crashing my roommates car, and then wanting to use her insurance instead of paying out of pocket?

Picture a quiet suburban street, where a stop sign stands sentinel—until a distracted driver delivers a fateful bump. In a flash, a minor fender-bender turns a roommate’s car into a battleground of budgets and blame. The culprit, a 23-year-old borrowing their roommate’s ride, now faces a $3,000 repair bill and a roommate who’s less than thrilled about footing the insurance fallout. What seemed like a small mistake snowballed into a heated debate over dollars, depreciation, and decency.

The driver’s plea to use their roommate’s insurance, paired with a refusal to cover potential car value loss, has sparked a feud that’s less about dents and more about trust. With emotions running high and wallets on the line, readers are left wondering: who’s really in the wrong when a favor turns into a financial fiasco?

‘AITA for crashing my roommates car, and then wanting to use her insurance instead of paying out of pocket?’

This car crash kerfuffle is more than a dented bumper—it’s a lesson in responsibility and roommate dynamics. The OP’s insistence on using their roommate’s insurance, while offering to cover premiums and co-pay, seems reasonable at first glance. However, the roommate’s concern about car value depreciation is valid. According to Kelley Blue Book, a vehicle’s history of accidents, even minor ones, can reduce its resale value by 5-15%, depending on the car’s make and market.

Dr. Jane Greer, a relationship expert quoted in a Bustle article, says, “When borrowing someone’s property, you’re borrowing their trust—breaking it comes with consequences.” The OP’s refusal to consider the roommate’s terms, especially the murky “depreciation” clause, ignores the roommate’s financial stake. The roommate, meanwhile, risks seeming inflexible by demanding an open-ended payment based on a future dealer’s estimate, which can indeed be subjective.

This situation reflects a broader issue: 60% of roommate disputes involve financial misunderstandings, per a Roommate Nation survey. The OP should propose a compromise—perhaps paying the full $3,000 out of pocket in installments to avoid insurance hikes. Open communication, maybe over a pizza to ease tensions, could rebuild trust.

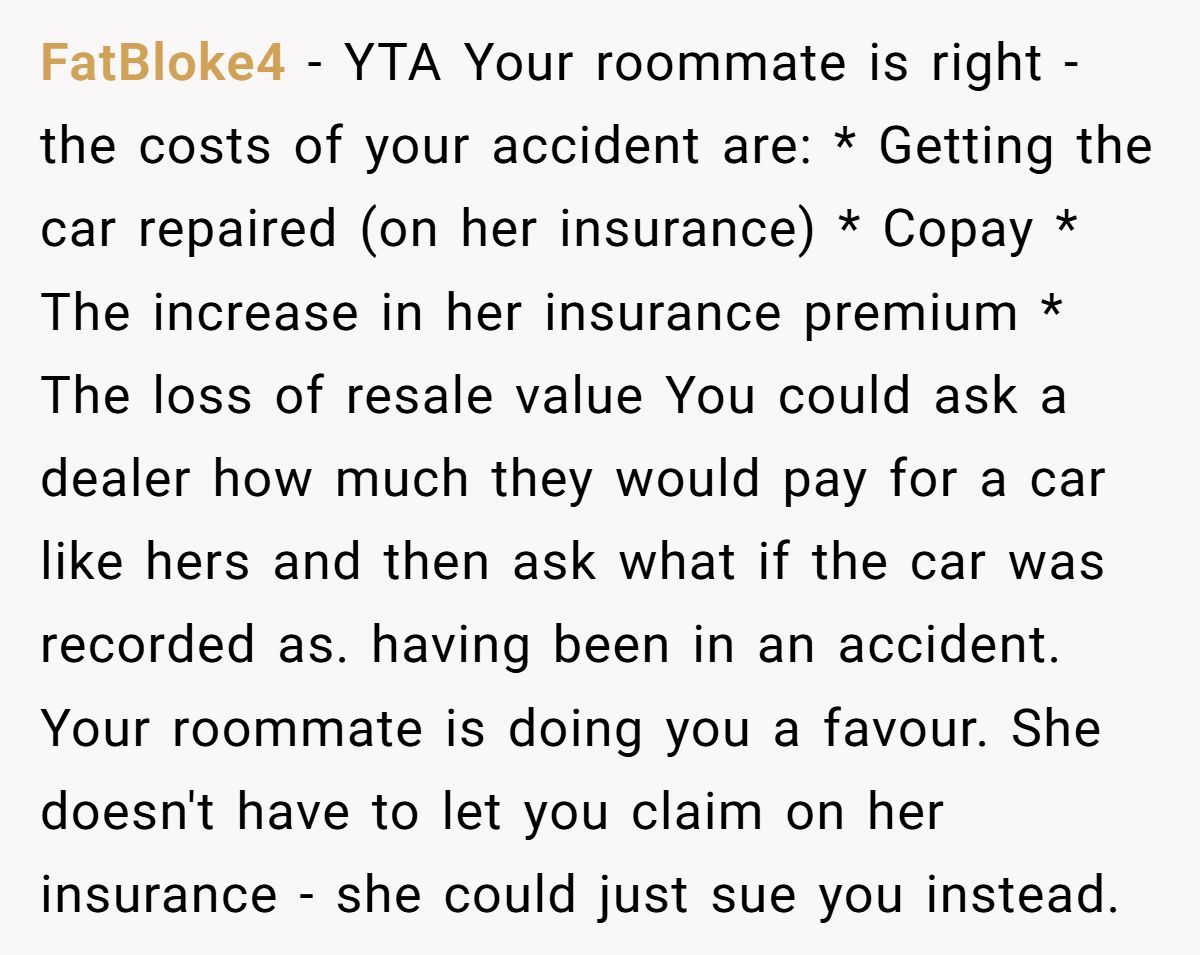

Check out how the community responded:

The Reddit squad rolled up with a mix of shade and wisdom, dishing out opinions like a potluck of tough love. From calling out the OP’s entitlement to debating insurance logistics, the comments were a lively mix of eye-rolls and reality checks. Here’s the raw scoop from the crowd:

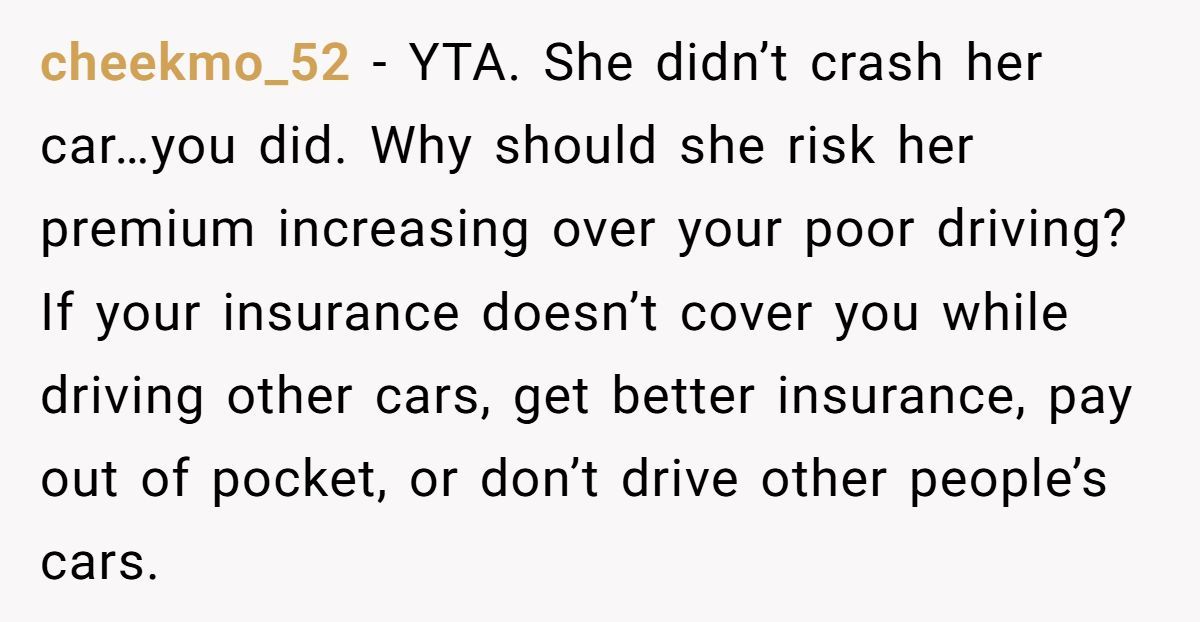

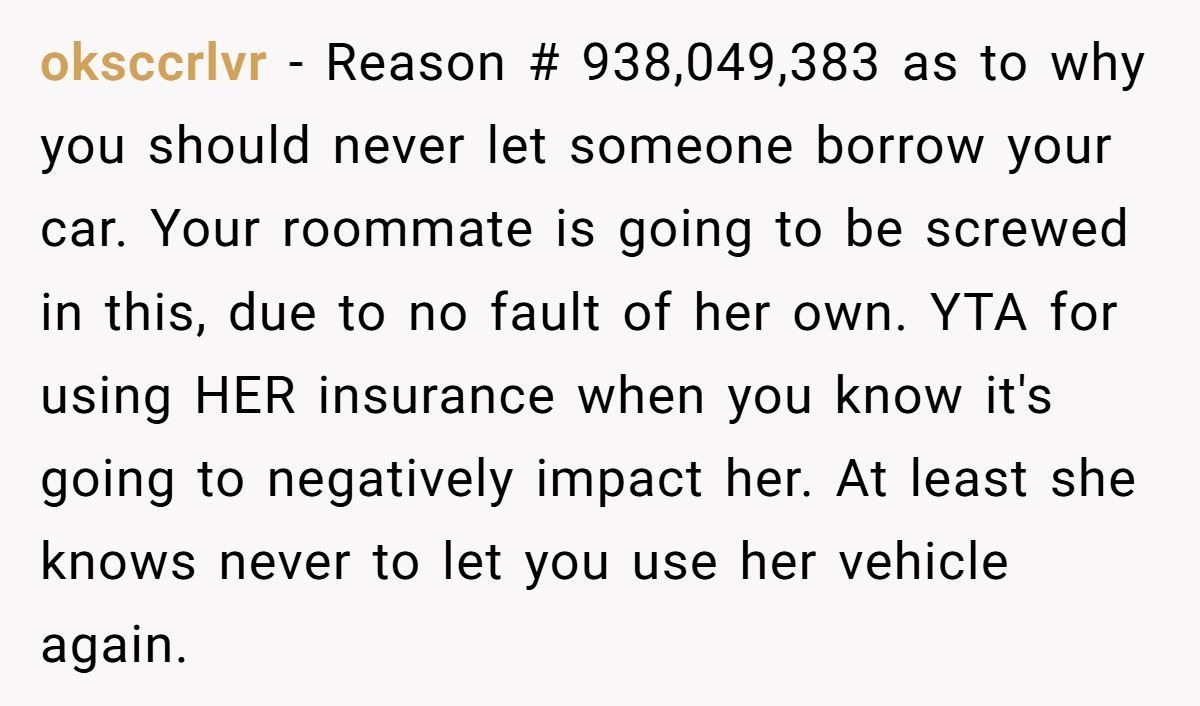

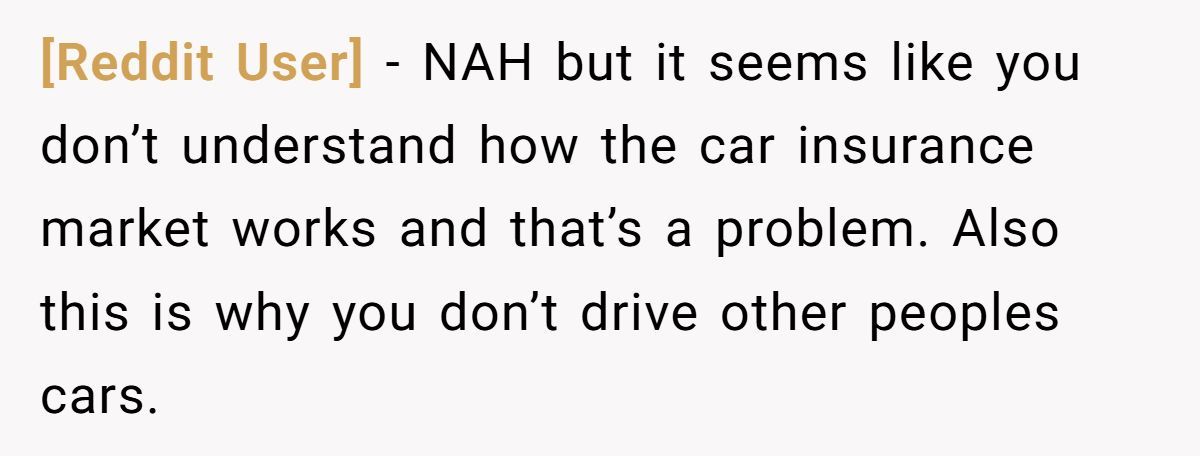

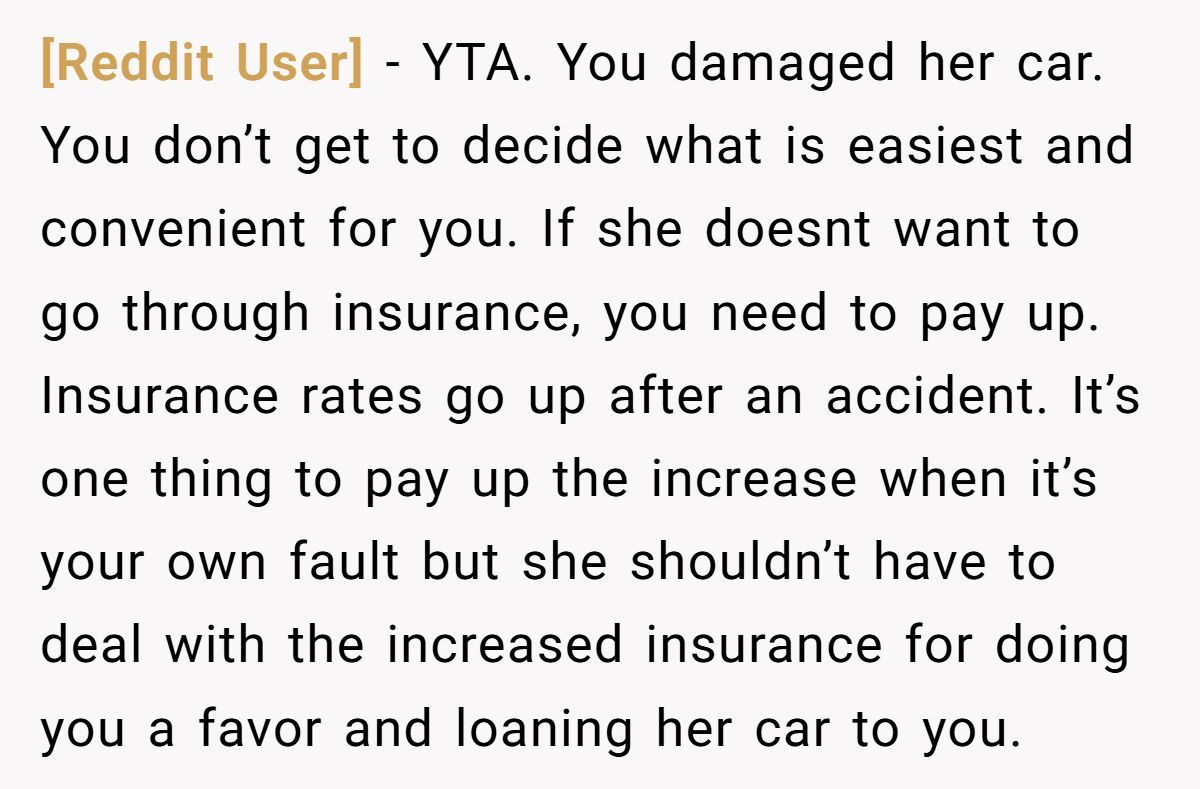

These Redditors leaned hard into accountability, with most siding against the OP for expecting the roommate to bear the insurance burden. Some questioned the crash’s severity, while others urged the OP to own the mistake. But do these spicy takes capture the full story, or are they just revving up the drama?

This tale of a fender-bender gone wrong highlights the messy intersection of favors, finances, and friendship. The OP’s push to use their roommate’s insurance, while dodging long-term costs, clashed with the roommate’s need to protect her asset. It’s a reminder that borrowing comes with responsibility—and sometimes a hefty price tag. How would you handle a roommate dispute over a damaged car? Share your thoughts—what’s the fairest way to settle this crash course in accountability?