AITA For Denying Financial Help to My NEET Father-In-Law?

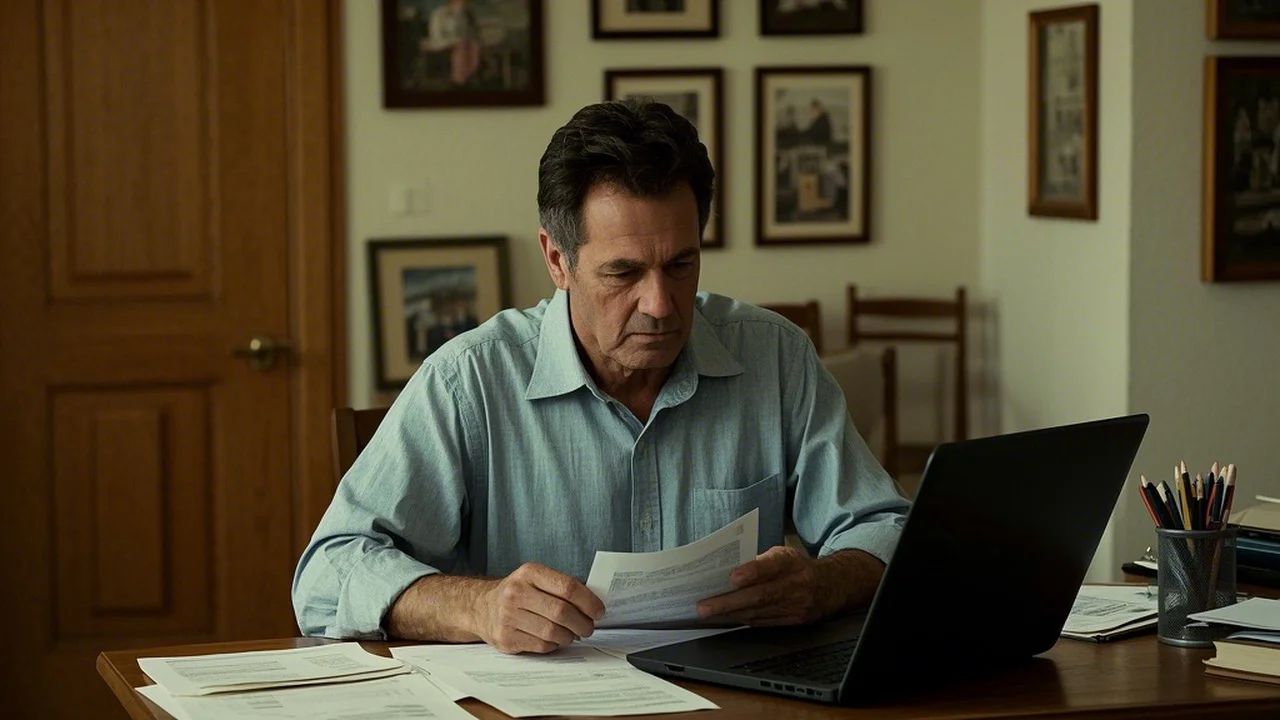

Family financial boundaries are one of the most sensitive topics that can lead to heated debates. In this case, a man finds himself in a challenging position when his 66-year-old father-in-law, who has long depended on his mother’s pension and has never been self-sufficient, asks for US$2000. Despite knowing his father-in-law’s history of poor money management and irresponsibility, he’s now under pressure from other family members—especially his wife’s side—to offer help.

The request comes at a time when the man is focused on safeguarding his own finances for his family’s future. With limited disposable income and savings earmarked for his son’s education, he has set strict conditions for any financial assistance. These include full transparency of his father-in-law’s finances and a concrete plan to establish a sustainable income. This firm stance has sparked controversy within the family, leaving everyone to wonder: should family ties override personal financial security?

‘AITA for not giving NEET father-in-law money?’

Financial boundaries with family members, especially those with a history of irresponsibility, are essential for protecting your future. Suze Orman, a well-known personal finance expert, once said, “Establishing clear financial boundaries with family is crucial—you must protect your own financial future before you try to fix someone else’s problems.” This advice is particularly relevant when a family member, like a NEET father-in-law, repeatedly demonstrates poor money management.

In situations where an individual repeatedly fails to provide for themselves, offering unregulated financial support can lead to a cycle of dependency. OP’s approach—demanding a full disclosure of his father-in-law’s financial situation and a viable plan for income—is a method endorsed by many financial advisors.

By setting these conditions, he is not only safeguarding his own financial stability but also encouraging personal responsibility. This strategy can be seen as a way to prevent enabling behavior, which, as experts warn, often results in long-term financial loss for the helper.

Moreover, financial experts stress that any monetary support given without proper accountability may eventually divert funds meant for essential family needs—like saving for a child’s education or securing a stable future. When one family member is chronically irresponsible, a single one-time payment rarely resolves the underlying issues.

Instead, it tends to establish a precedent where the individual expects ongoing help. Legal advisors often recommend that any financial support to family members in such circumstances be structured as a conditional loan or as assistance directed toward specific expenses (such as paying utility bills or rent) rather than a lump sum cash gift.

Additionally, it’s important to note that your father-in-law’s request is part of a broader pattern of behavior, including his reliance on his late mother’s savings and his refusal to work or apply for disability benefits he might be entitled to.

This pattern reinforces the need for strict financial boundaries. By refusing to give money without clear, accountable conditions, you are sending a message that while you care about your family, you cannot compromise your own financial security or the well-being of your child.

Ultimately, while it’s natural to want to help family in times of crisis, financial experts agree that such help must be balanced with protecting your own future. If the support is not structured with accountability, you risk becoming the default financial safety net for someone who has repeatedly failed to manage their own affairs responsibly.

Here’s the feedback from the Reddit community:

Here are some candid reactions from the Reddit community – a mix of strong support and practical caution. Many commenters applaud the decision not to give money without strict conditions, noting that enabling irresponsible behavior often leads to further dependency. Others remind OP that family members should not dictate financial choices, emphasizing that safeguarding one’s own future, especially for one’s children, is paramount.

In conclusion, the dilemma of whether to financially support a family member with a long history of poor money management is never simple. While compassion for a struggling loved one is natural, protecting your financial security and that of your children must come first.

Would structuring the support as a conditional agreement—perhaps even tying it to a specific plan—be a workable compromise, or is it better to say no outright? What do you think is the best way to balance family obligations with personal financial responsibility? Share your thoughts and experiences below and join the discussion.

Tell him he has 2 sources of income 1. He can get a job and work for it & 2. Disability payments both of which he’s choosing not to do. Your hard earned cash is not his 3rd option. Email him ads for jobs and the disability payment form for him to fill in then leave him to it.