AITA Wife wants 100% in case of untimely end?

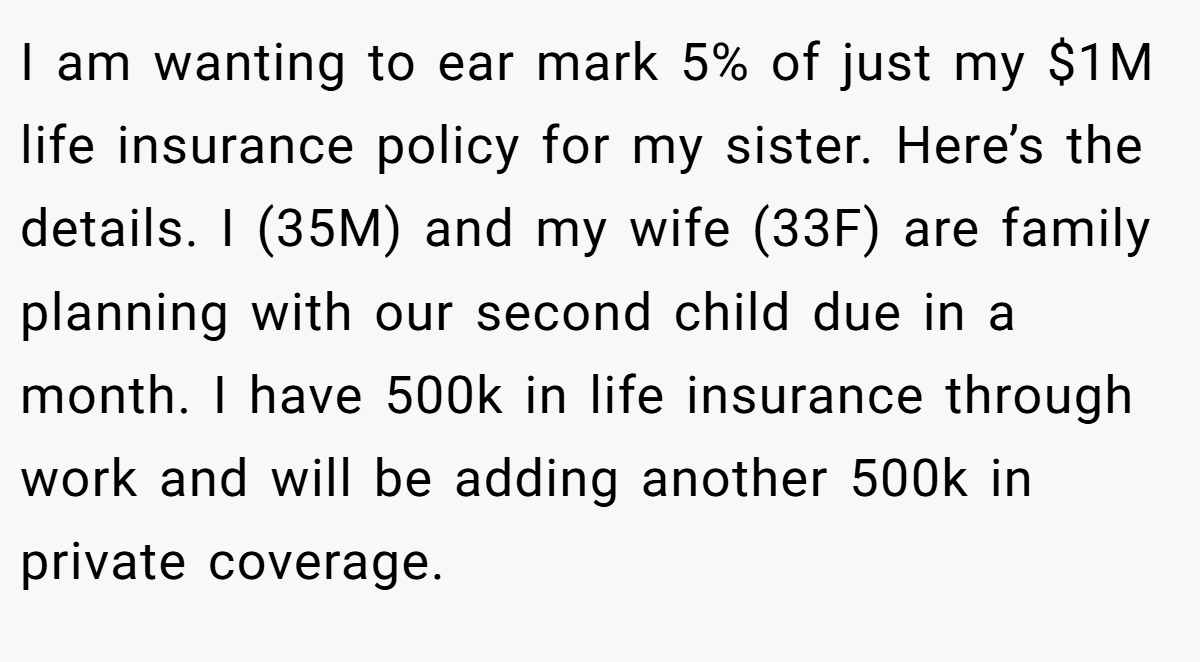

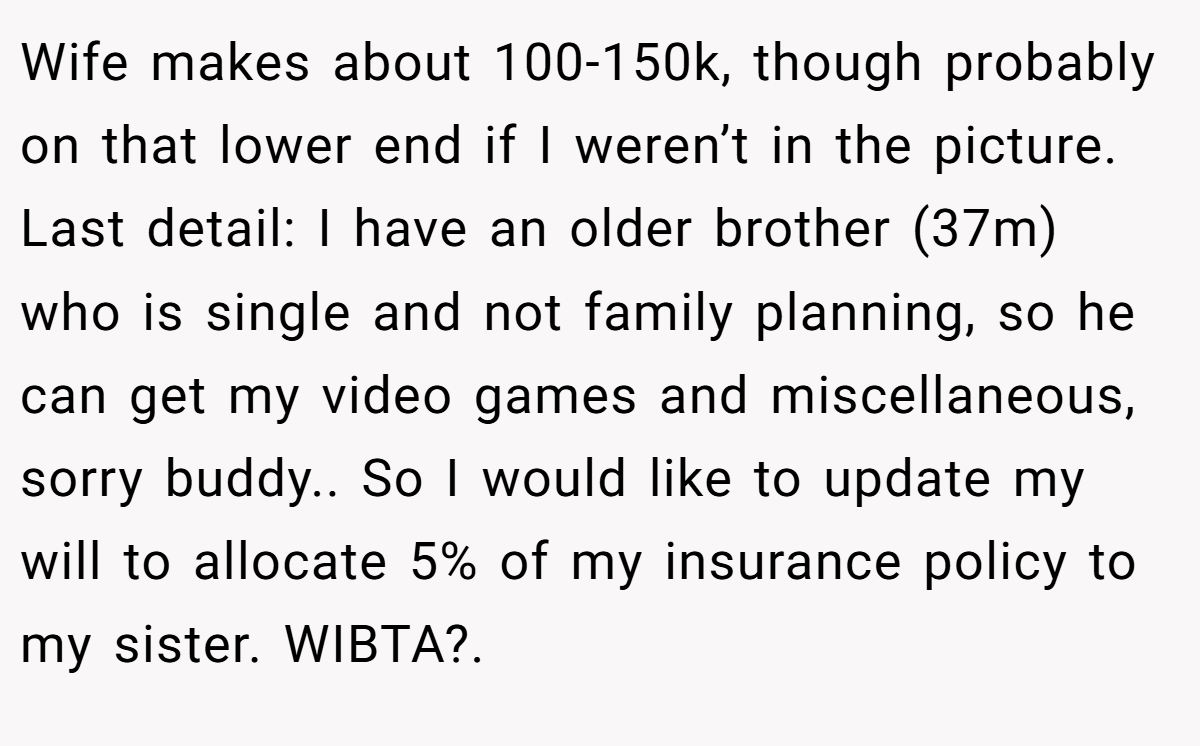

In the realm of financial planning and family dynamics, one man’s decision about his life insurance policy has sparked a heated debate. Faced with a $1M policy and the responsibility of safeguarding his family’s future, he now finds himself torn between his wife’s demand for full protection for their children and his desire to help his sister with a modest allocation.

The delicate balance of love, duty, and financial security hangs in the balance. Amid the excitement of planning for a new child and a future built on shared dreams, the tension of conflicting priorities casts a shadow. While his wife argues that every dollar should secure their immediate family’s well-being.

He sees a chance to offer a helping hand to his sister—a gesture he believes could materially change her circumstances. This conundrum sets the stage for an in-depth discussion about personal responsibility, familial obligations, and the often-complicated decisions that come with planning for the unforeseen.

‘AITA Wife wants 100% in case of untimely end?’

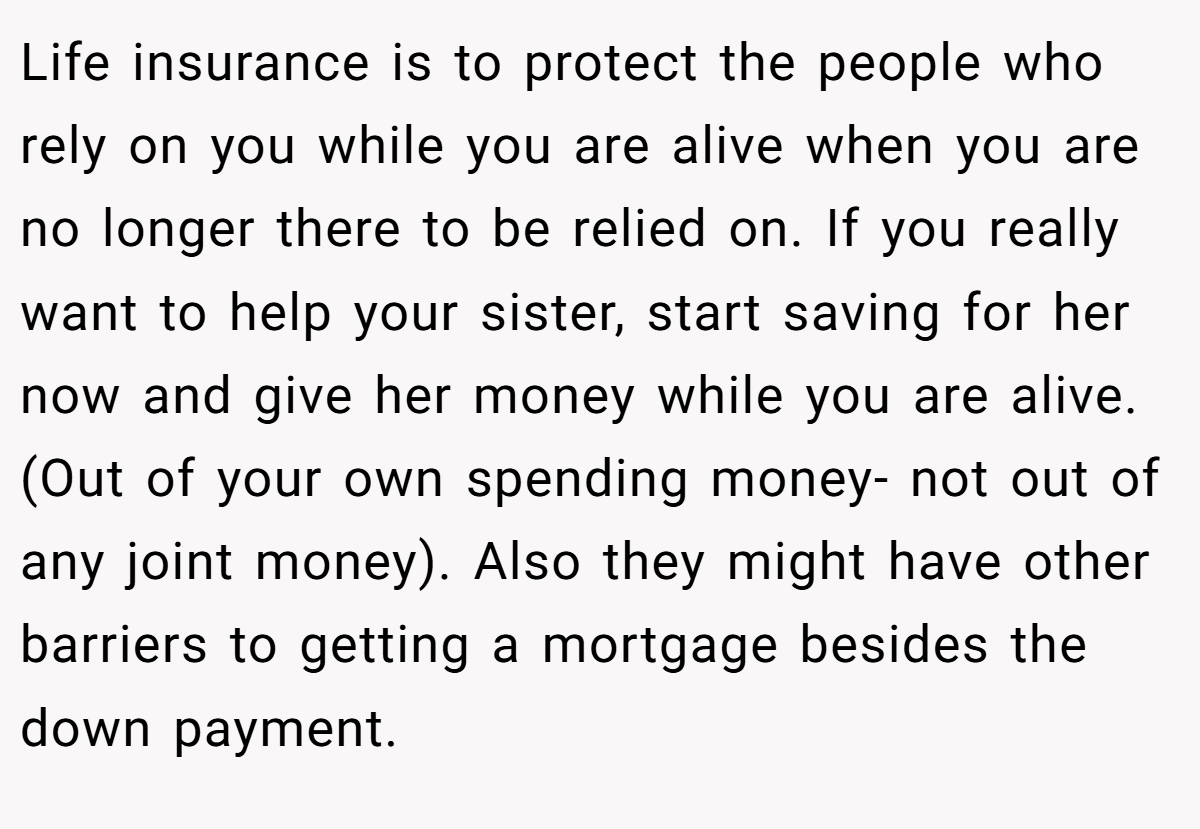

Navigating the allocation of life insurance benefits is no simple task. In this case, the author faces a dilemma that pits immediate family security against a desire to assist extended family in need. Life insurance is traditionally viewed as a means to ensure financial stability for those who rely on your income after you’re gone. However, personal values and family dynamics often complicate that straightforward approach.

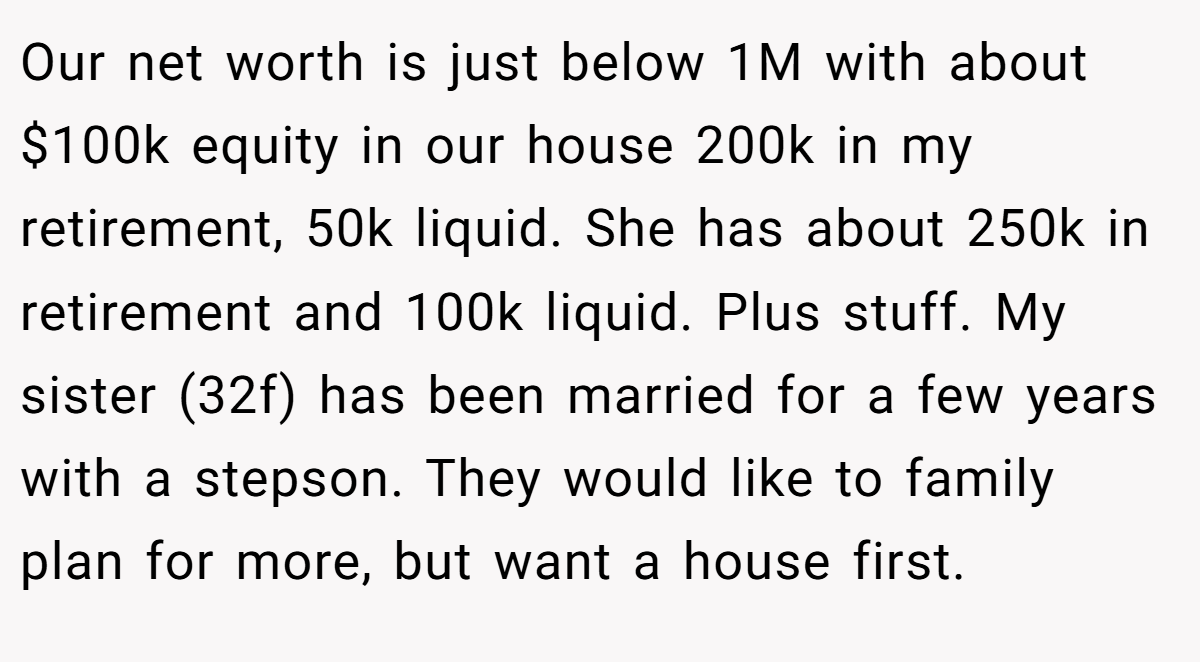

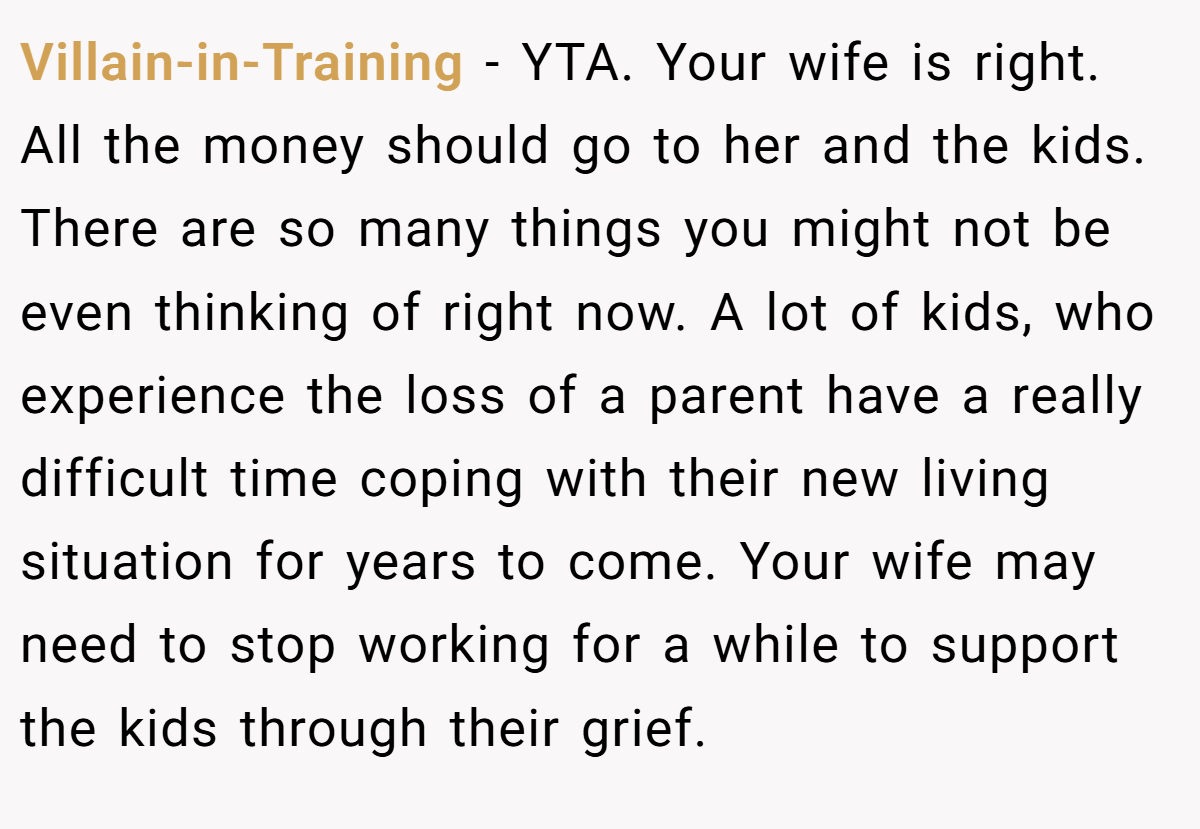

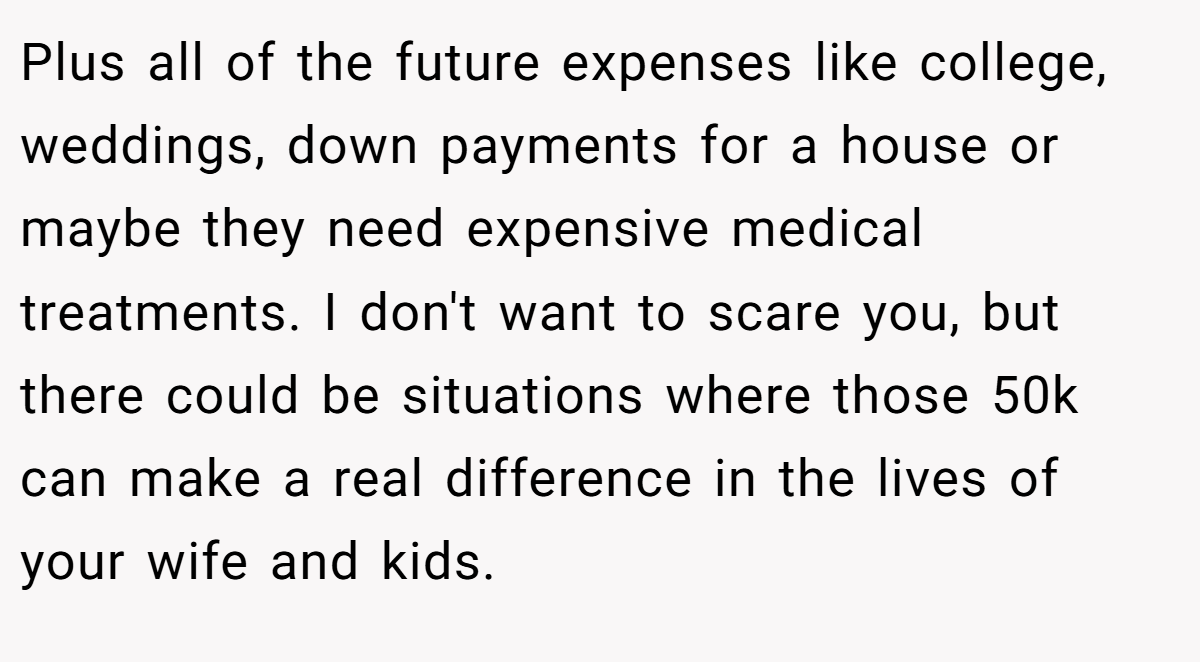

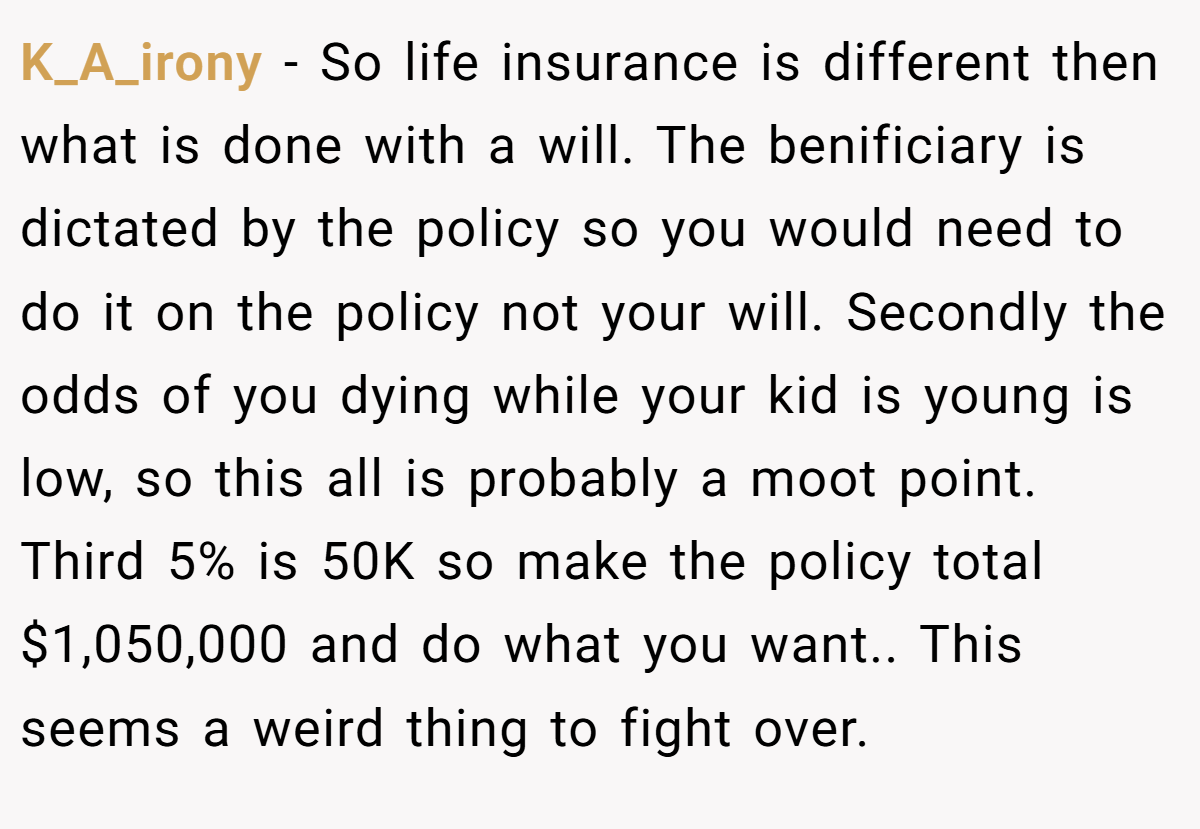

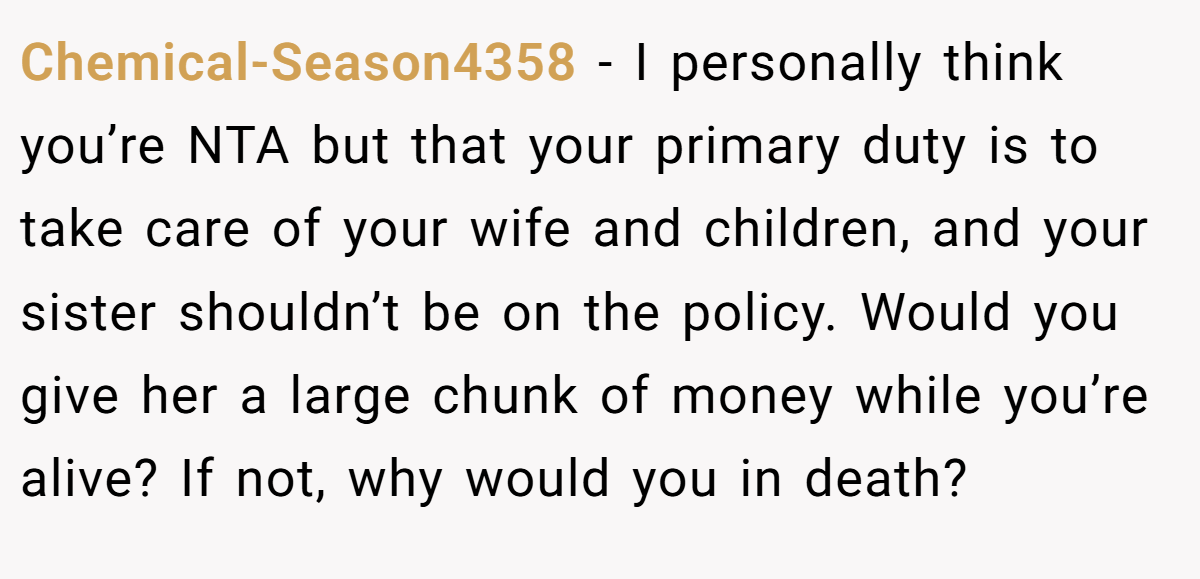

The core of this debate is the balance between protecting one’s immediate family and extending help to relatives who are struggling financially. On one hand, the wife insists that every penny of the $1M policy should benefit their children and secure the family’s future.

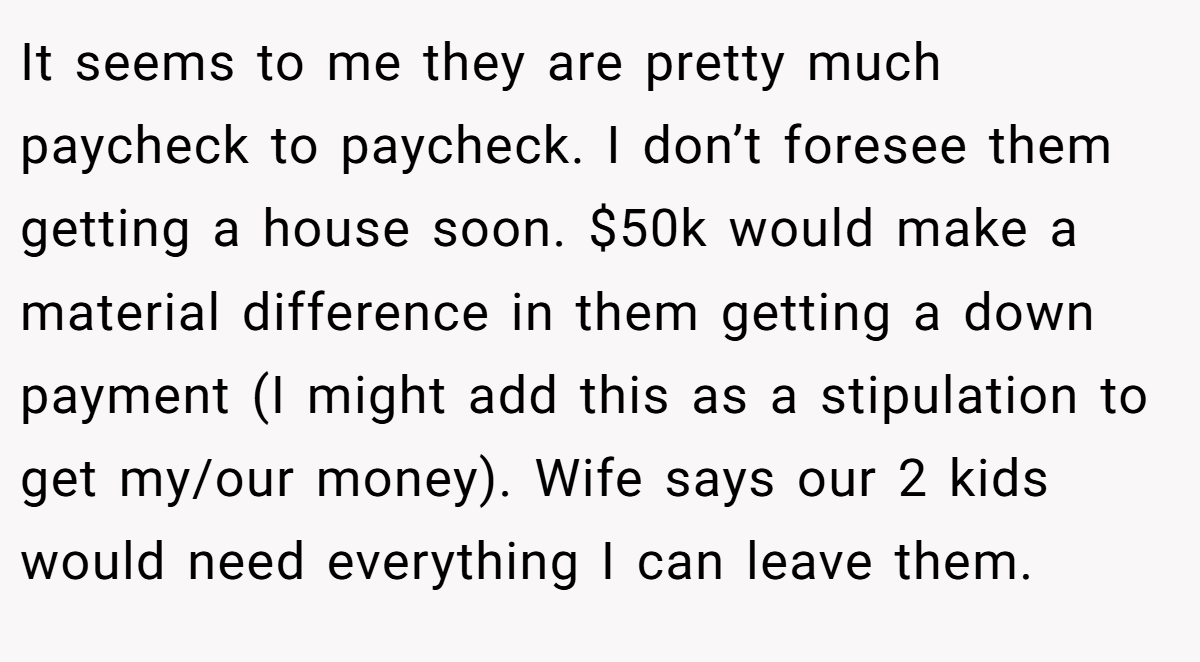

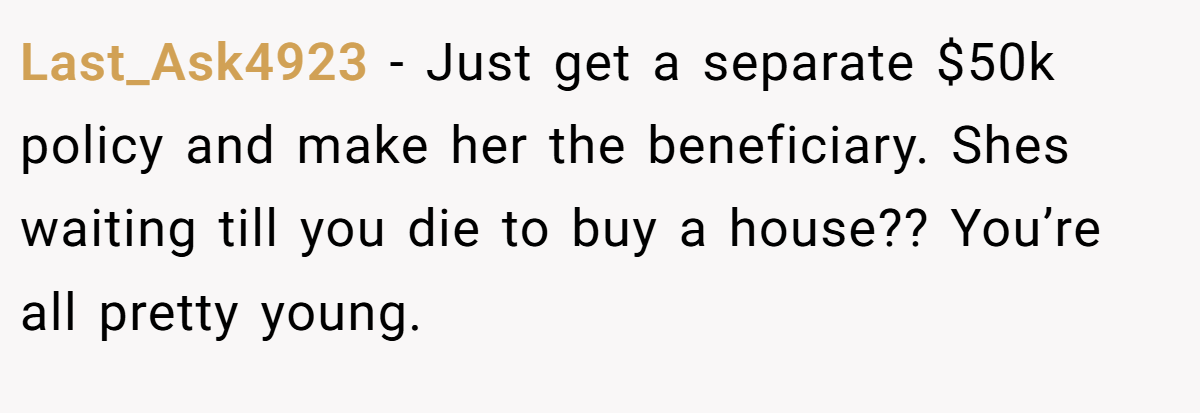

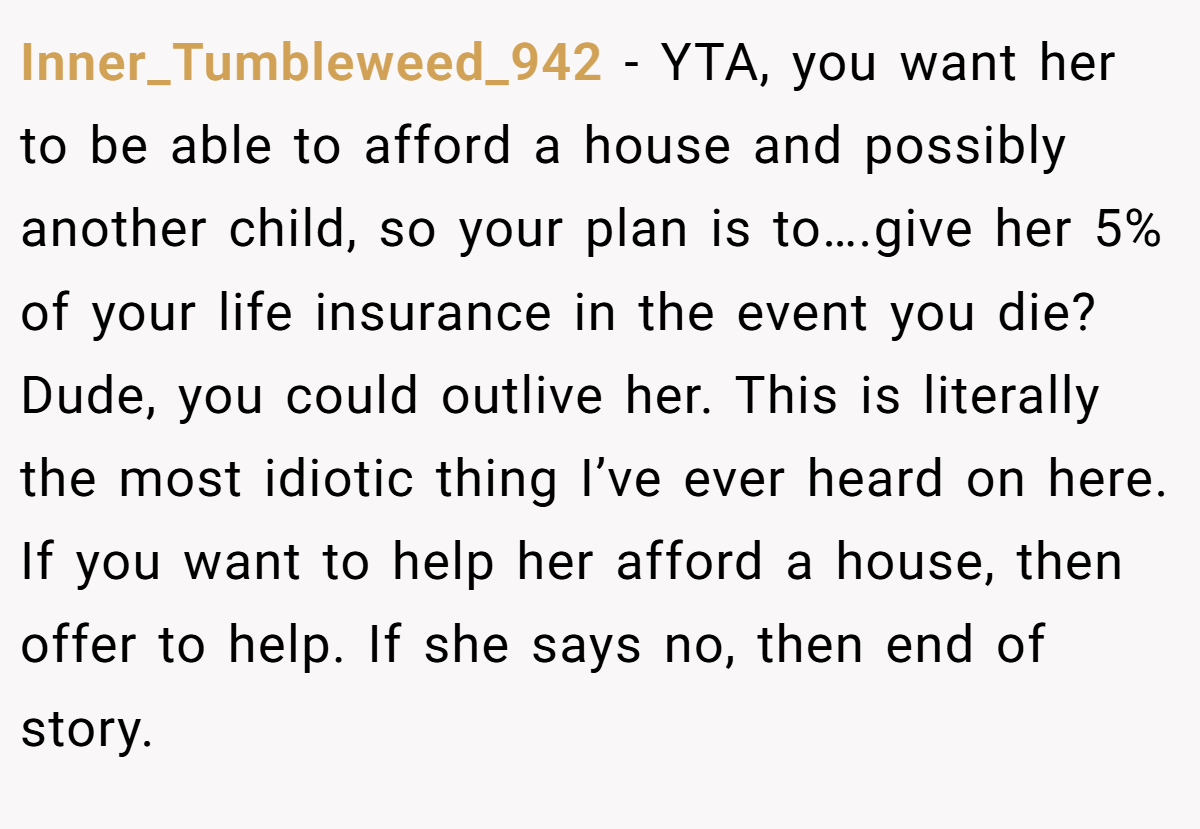

On the other hand, the author believes that earmarking 5%—or $50K—could provide crucial assistance for his sister to make a down payment on a home, thereby potentially improving her long-term financial outlook. This conflict brings to light the broader issue of how to best distribute resources in anticipation of unforeseen events.

According to Suze Orman, a renowned personal finance expert, “Life insurance should be designed primarily to protect those who depend on you financially, ensuring they have the resources to navigate a difficult transition.” This perspective underscores the traditional view: that your primary beneficiaries should be those most vulnerable to the loss of your income.

Nonetheless, it also invites a discussion about whether and how to address the needs of extended family, especially when they are in a precarious financial situation. Balancing these competing interests requires careful thought and open communication among all involved.

Another layer to this issue is the unpredictable nature of life. While the chance of an untimely death may be statistically low, the impact on a family without proper financial support can be devastating. The author’s proposal to allocate a modest portion of his policy reflects a proactive attempt to address a potential future need, albeit one that his wife finds too risky.

This scenario raises questions about priorities: Should financial decisions focus solely on the immediate family, or is there room to extend a safety net to others in need? Ultimately, those facing similar dilemmas might benefit from exploring alternative financial strategies. For instance, purchasing a separate policy for extended family support or creating a living trust could be considered.

Open dialogue, transparent planning, and expert consultation are crucial in ensuring that all parties’ needs are addressed without compromising the financial security of those who rely most on your income.

Here’s the input from the Reddit crowd:

Overall, the community expressed mixed but common sentiments. Many agree that life insurance is primarily meant to protect one’s immediate family, emphasizing that the funds should secure the future of one’s spouse and children.

Yet, a few voices recognize the merit in offering some assistance to extended family members, arguing that helping a sibling during tough times is a noble gesture. Despite differing opinions, the shared consensus underscores the importance of prioritizing those who depend most on you.

In conclusion, this debate highlights the complex interplay between financial security, family obligations, and personal values. The author’s proposal to allocate 5% of his life insurance to help his sister, while his wife advocates for full protection of their immediate family, reflects a broader challenge faced by many in planning for an uncertain future.

What would you do if faced with a similar decision? Share your thoughts, experiences, and advice in the comments below, and join the conversation on how best to navigate such delicate financial and familial choices.