Her Fiancé Lives With His Parents, But Demands She Sell Her Paid-Off Home to Fund His Lifestyle

We all know that moment when a partner’s casual suggestion suddenly feels like a massive red flag. For one 46-year-old woman, a conversation about future living arrangements quickly morphed into a demand that threatened her entire financial safety net. She holds the deed to a fully paid-off home, a precious asset inherited from her late mother. Her 45-year-old fiancé, however, has a completely different vision for their future.

Despite still living with his parents and working a retail job, he is pushing her to liquidate her inheritance so they can rent a costly apartment instead. As the pressure mounts and their conflicting backgrounds clash, she finds herself questioning his logic—and perhaps his motives. Curious how this relationship drama unfolded? The full story is right below.

Setting the stage, the relationship already navigates the complex realities of neurodivergence and career instability.

The irony is sharp—delaying marriage for financial stability, yet proposing a plan that actively destroys it.

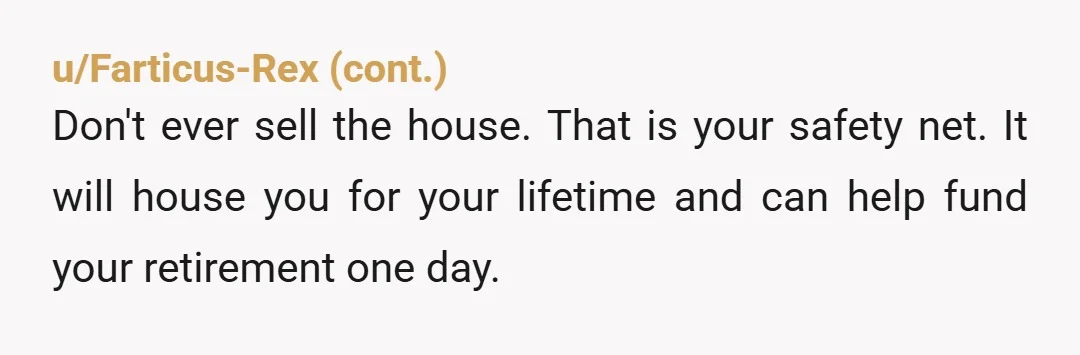

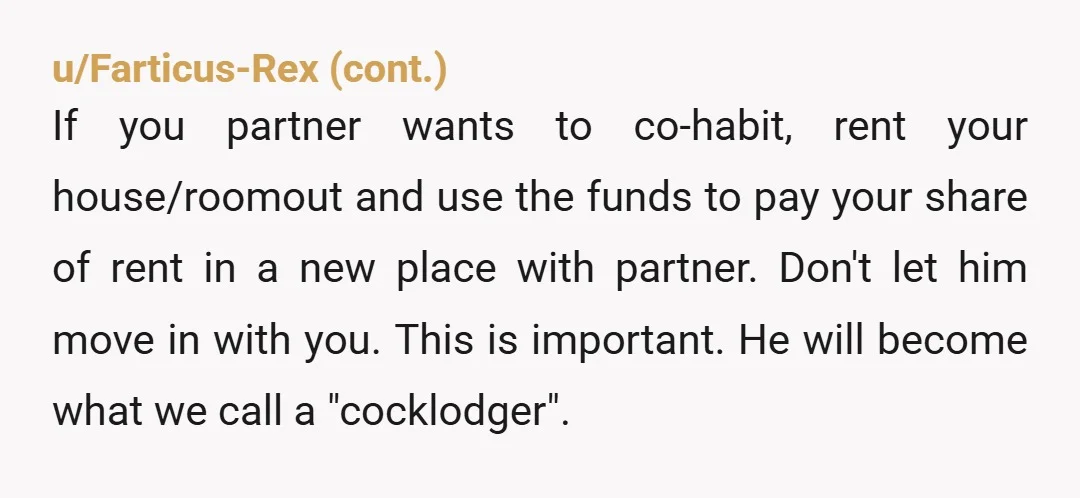

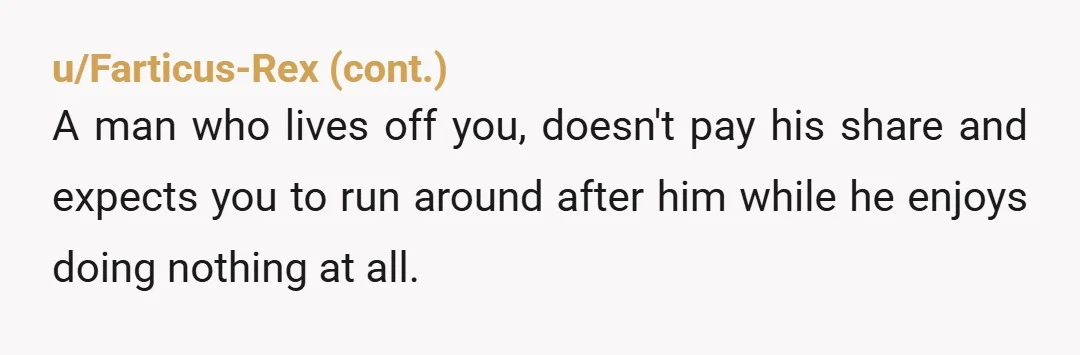

This clash over real estate reveals a fundamental mismatch in how each partner views security and independence. For the original poster, a fully paid-off home represents a permanent safety net, especially given her background of financial struggle. Conversely, her fiancé’s push to sell the house and rent an expensive apartment suggests a desire to perform a certain standard of living, even if it defies mathematical logic.

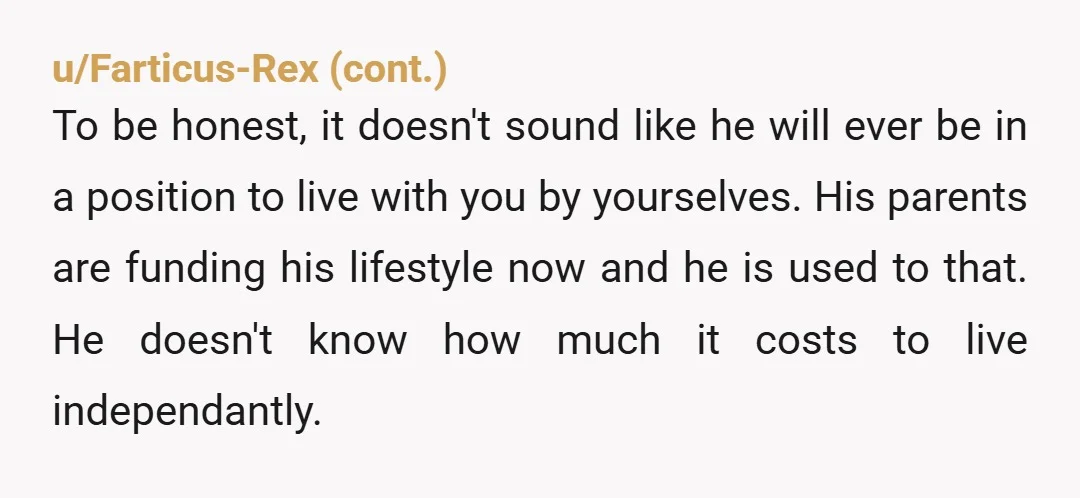

From an analytical perspective, the fiancé—having never lived entirely independently—may romanticize the idea of a fresh start in a leased space, completely underestimating the relentless drain of monthly rent. According to general consensus among financial therapists and wealth advisors, liquidating a secure pre-marital asset to fund temporary living expenses is universally discouraged. This is especially true when co-owning the property with a sibling, which adds complex legal barriers to any potential sale.

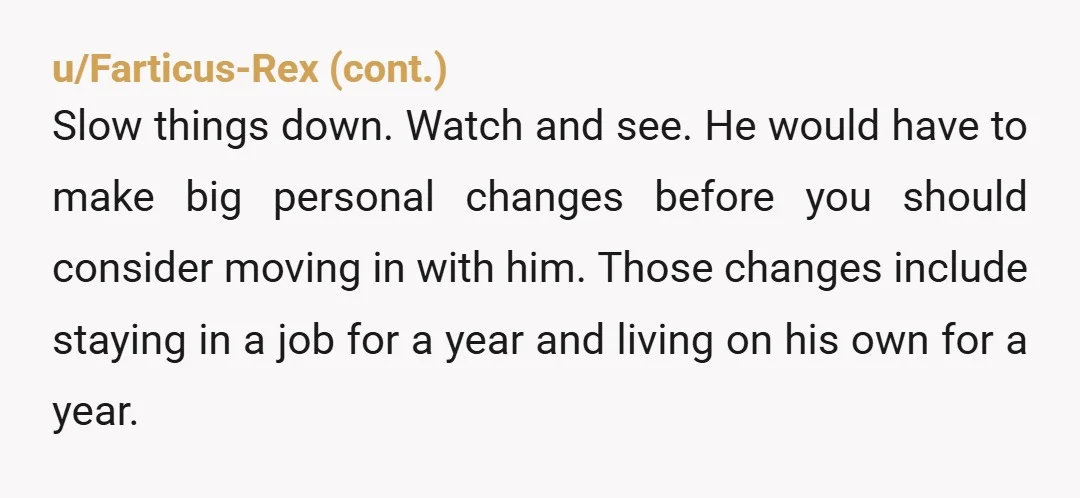

To navigate this impasse, the original poster should firmly establish her home as a non-negotiable asset. Instead of arguing about the sale, they could concretely test their compatibility by having the fiancé live independently and manage his own lease for a year. This practical step would bridge the gap between his expensive tastes and the reality of their current personal finance situation.

Navigating financial disparities before marriage requires careful consideration of both partners’ needs and realities. While one envisions a fresh start in a modern apartment, the other prioritizes the stability of a fully paid-off family inheritance. Do you think she should hold firm on keeping her property, or is there a compromise that satisfies his desire for a different lifestyle? And how should they address the underlying career issues before tying the knot? Share your thoughts below!

Community Opinions

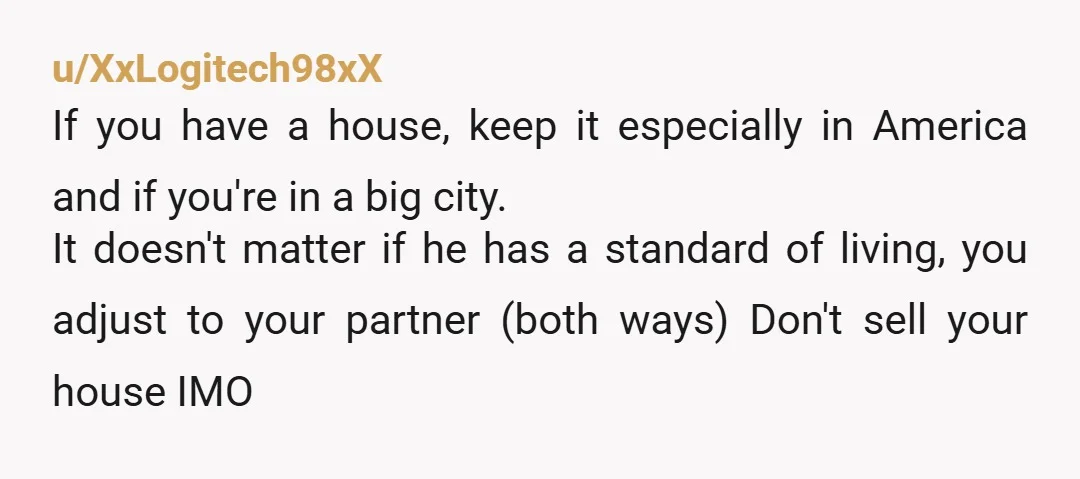

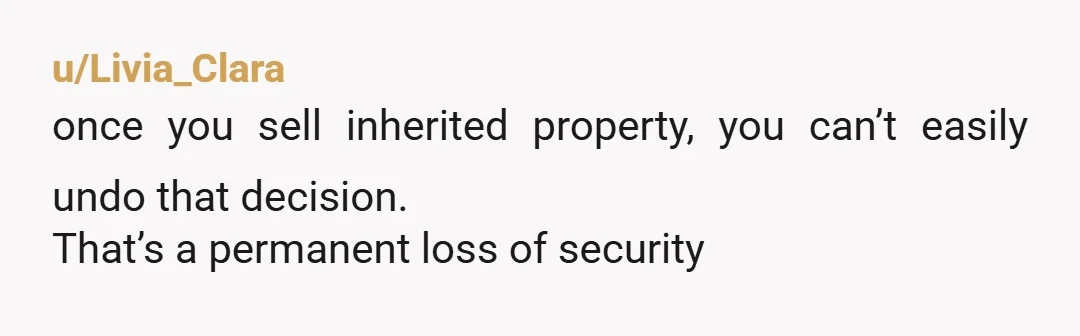

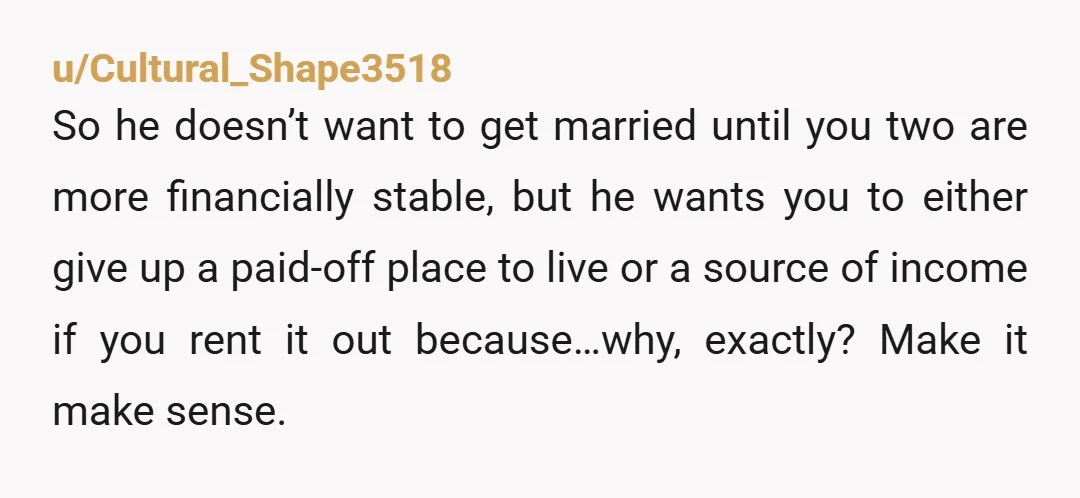

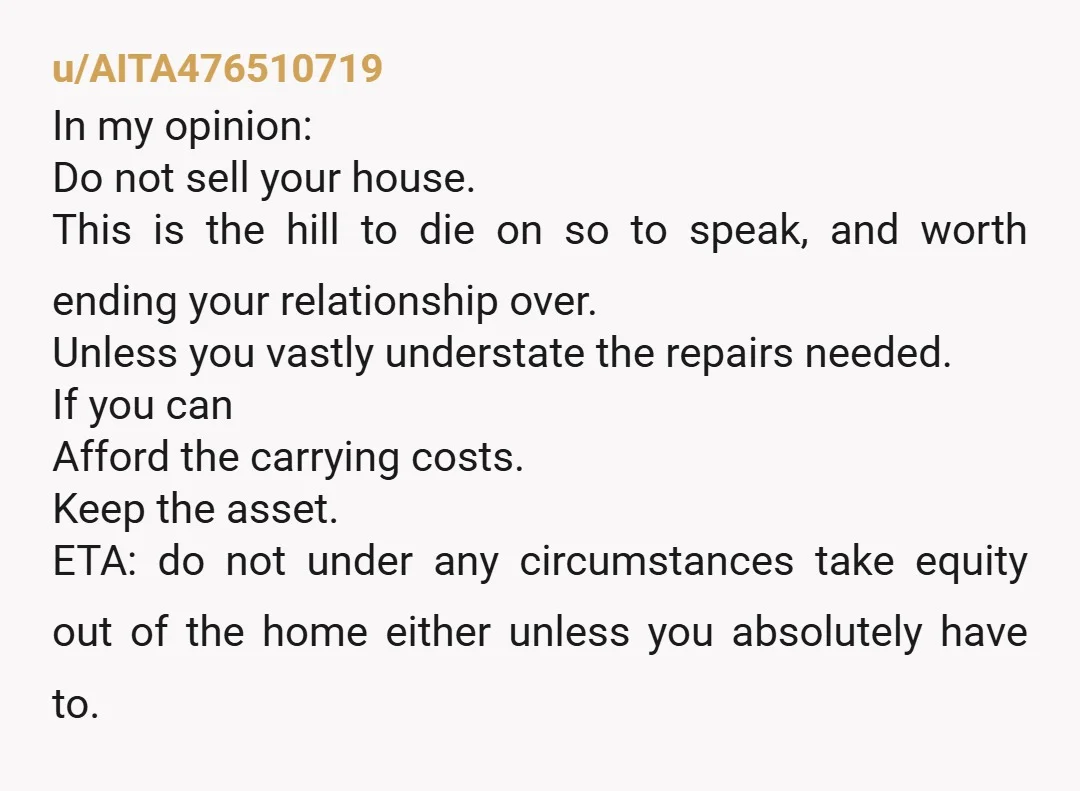

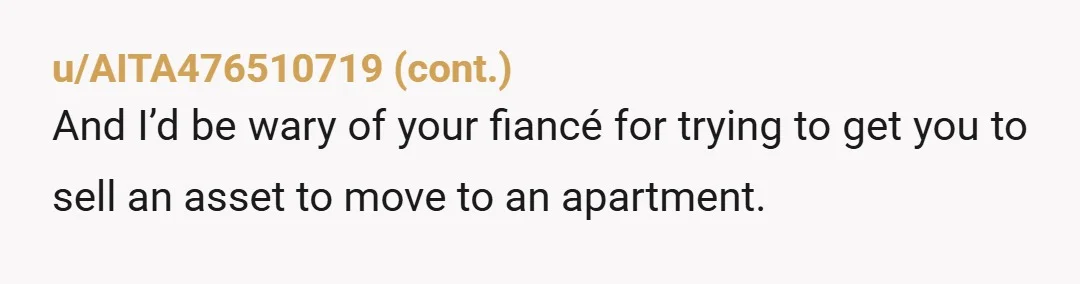

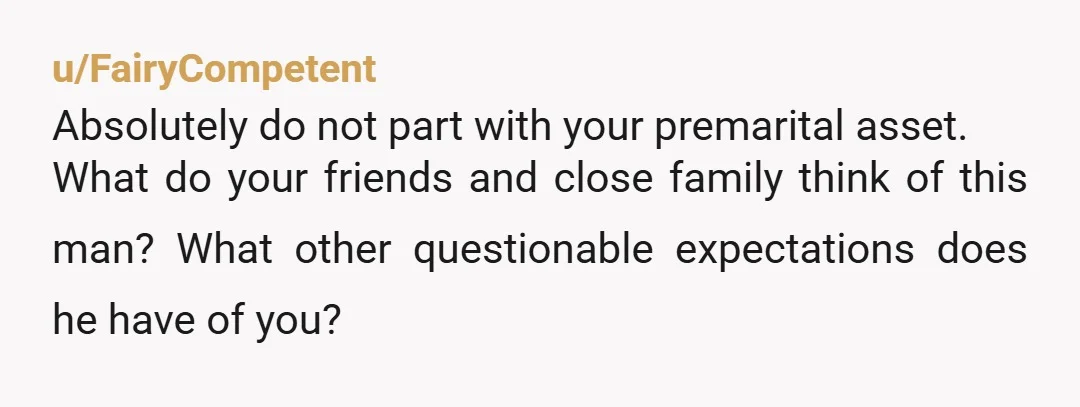

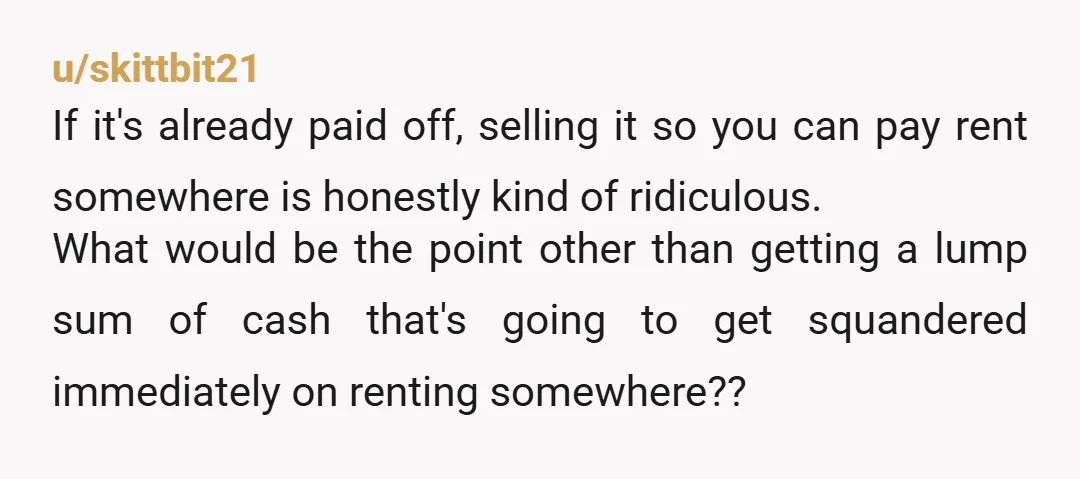

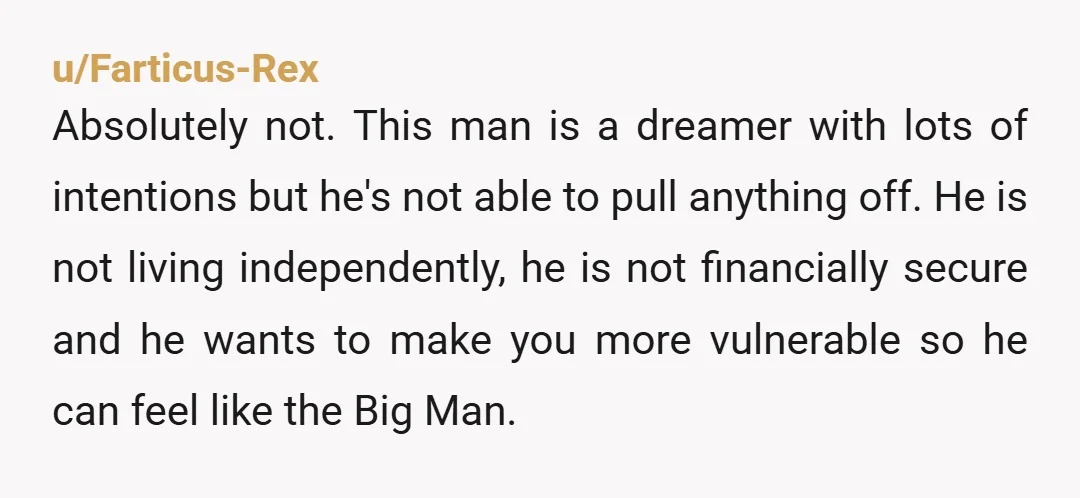

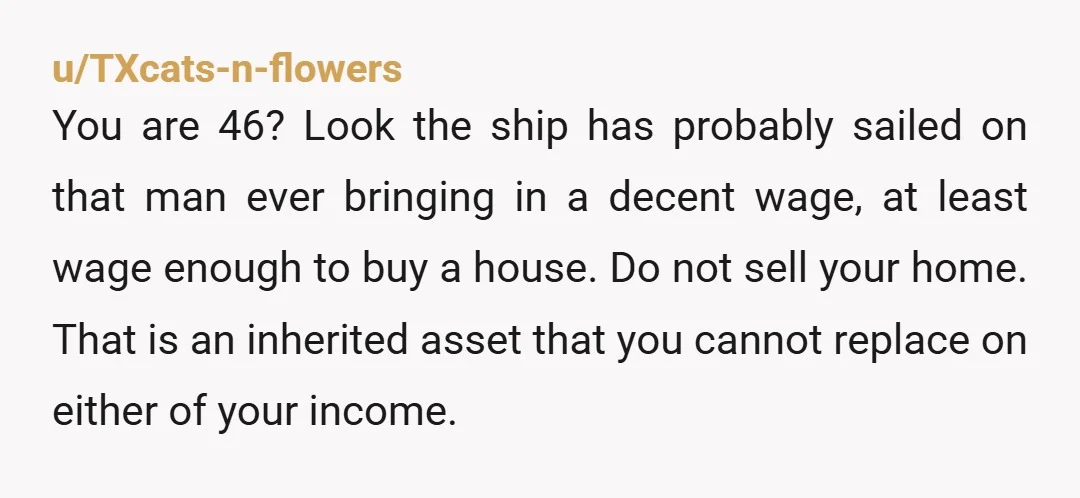

Reddit came in hot—nearly unanimous in their outrage, with a vocal majority begging the original poster to protect her assets at all costs.

A few seasoned commentators even warned that this financial red flag might signal deeper compatibility issues down the line.

Ultimately, navigating shared finances requires both partners to be grounded in reality, rather than just lofty aspirations. Tensions often peak when one person’s desire for a specific lifestyle threatens the other’s hard-won stability. Do you think the fiancé is just incredibly naive about the cost of living, or did he have an ulterior motive for wanting her to sell? And how would you handle a partner demanding you give up your financial safety net? Drop your thoughts in the comments!