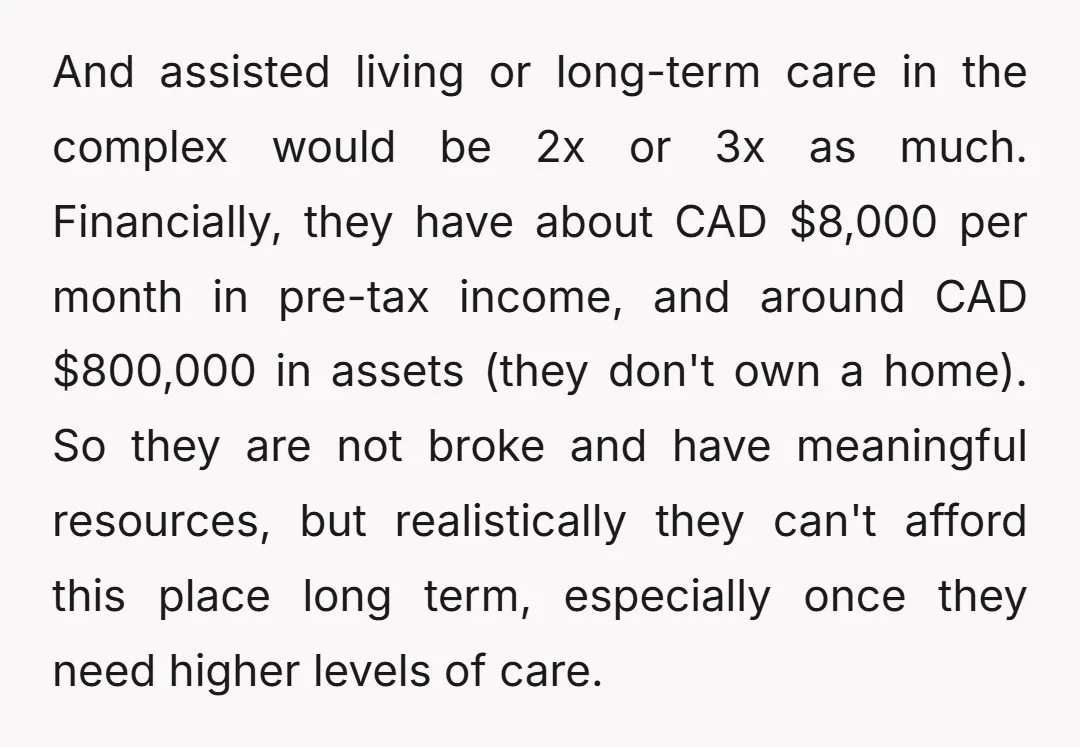

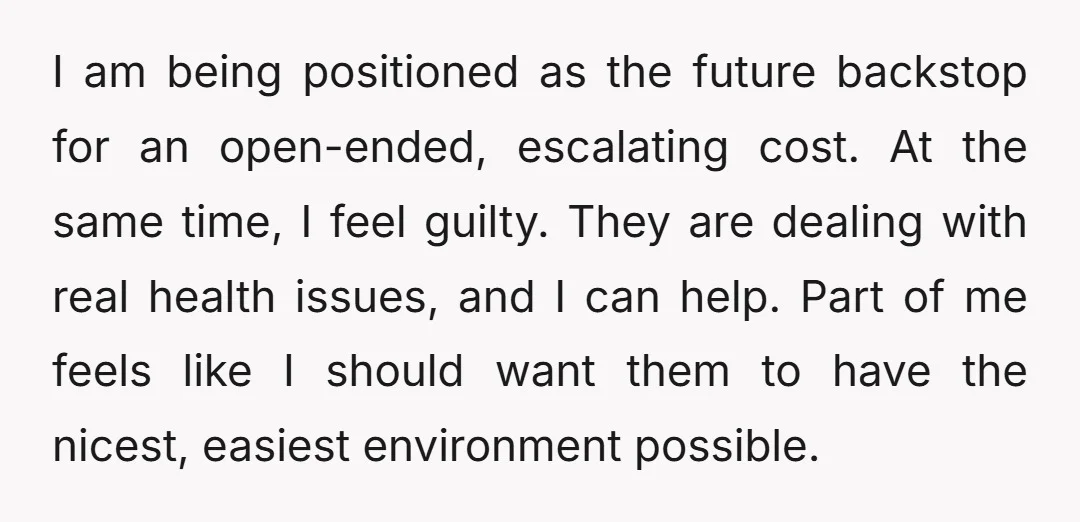

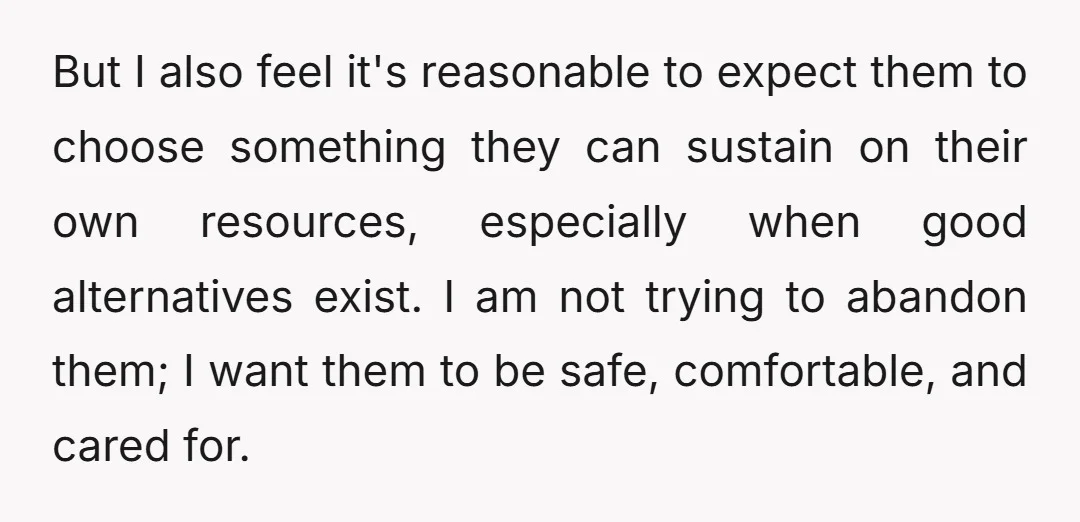

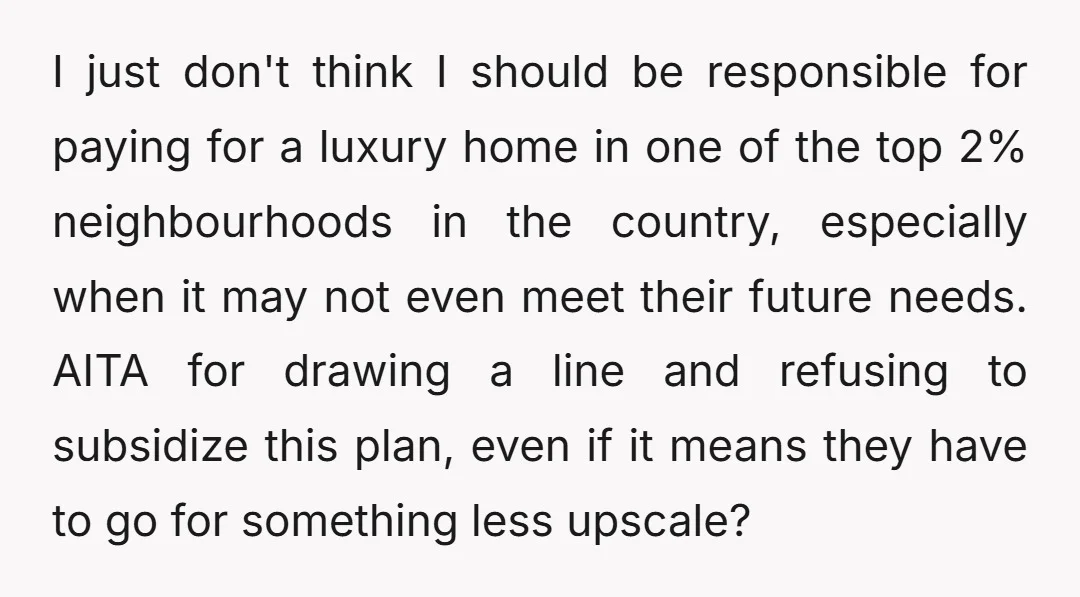

This Doctor Refused to Subsidize His Parents’ $11,000-a-Month Senior Home, Now He’s Questioning Everything

We all know that moment when the reality of aging parents hits hard, bringing tough choices we never wanted to make. For one 34-year-old physician, this emotional milestone quickly spiraled into a massive financial dilemma. His parents, dealing with serious health issues including early-stage Alzheimer’s and cancer, decided it was time to plan for their transition into assisted living.

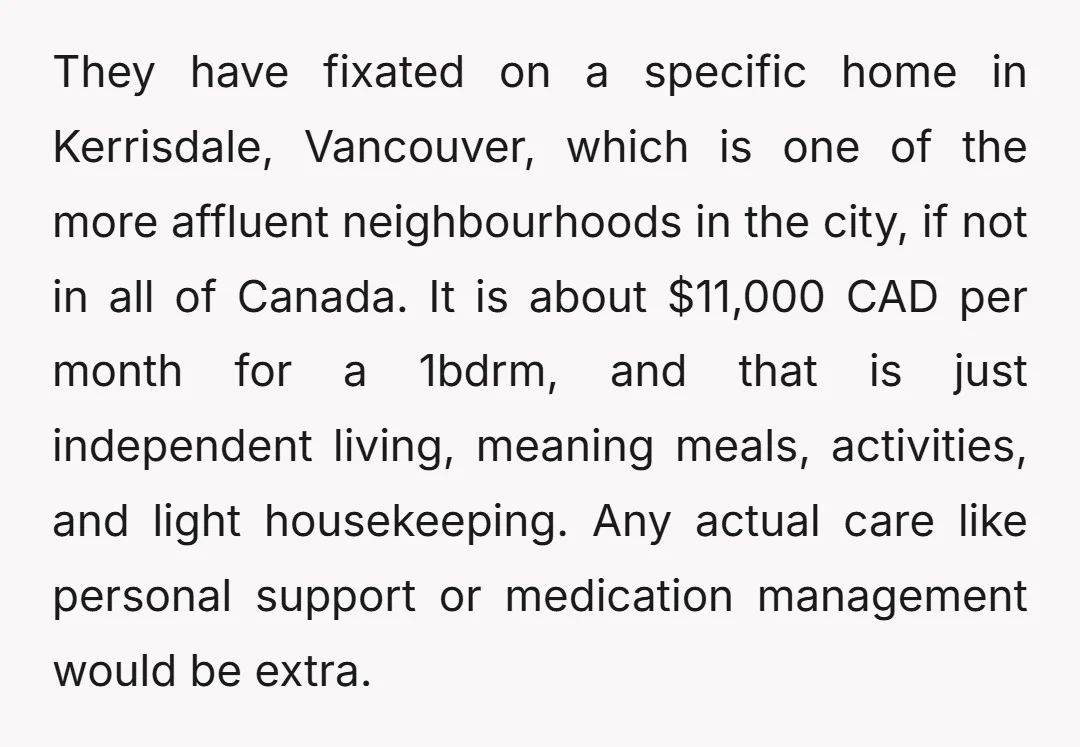

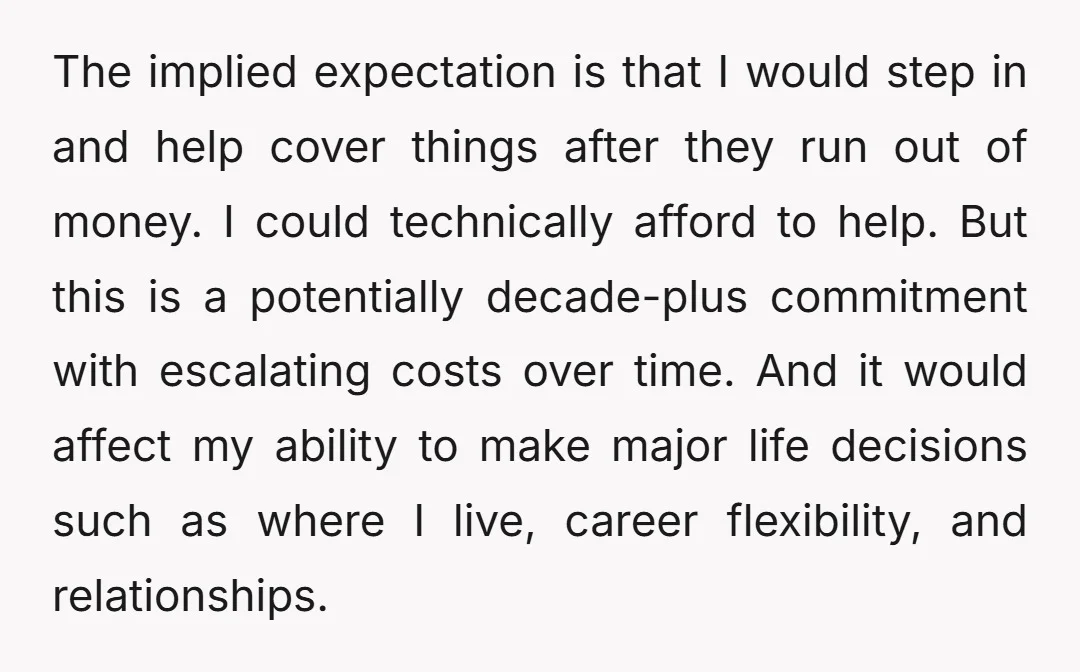

But instead of choosing a sustainable option, they set their sights on an ultra-premium luxury facility in Vancouver’s affluent Kerrisdale neighborhood. The price tag? A staggering $11,000 CAD per month just for independent living. Facing an open-ended expectation to bankroll their elder care costs once their savings run dry, he had to draw a hard boundary. Curious how this family financial conflict unfolded? The full story is right below.

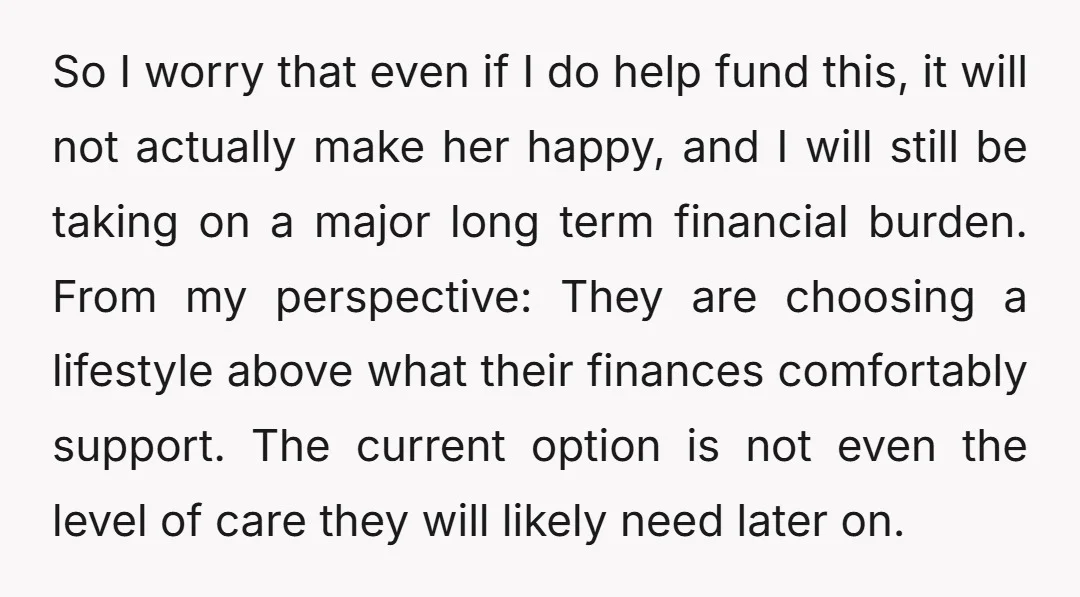

Setting the scene, the stark reality of dual diagnoses casts a long shadow over the family’s future planning.

The gap between their current physical needs and the exorbitant luxury price tag creates an immediate, glaring point of tension.

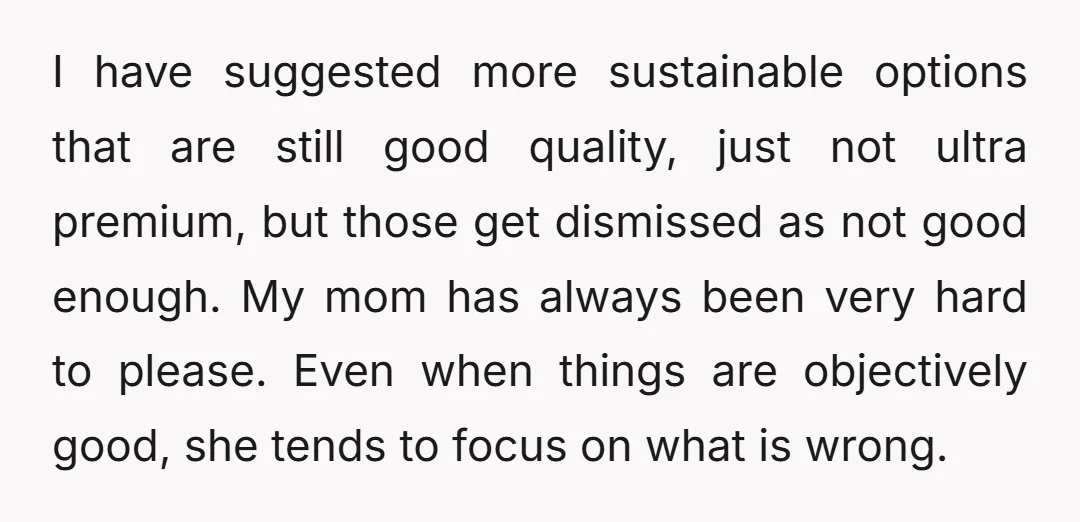

It is a classic clash: practical logic meeting emotional resistance from a parent who historically struggles to find satisfaction.

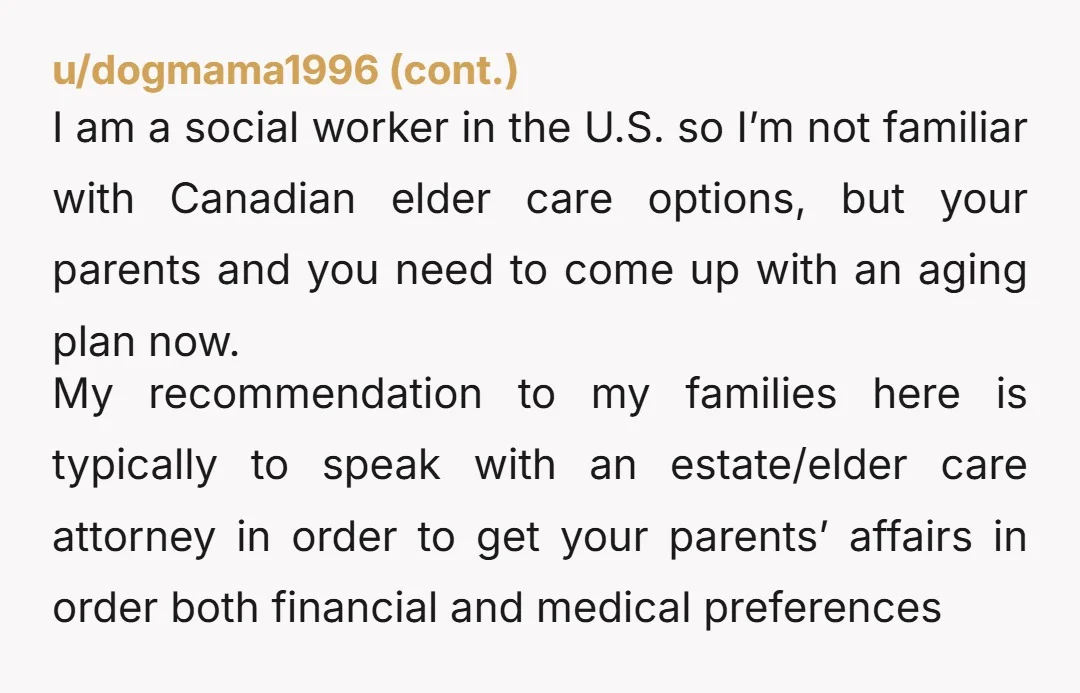

Navigating the financial logistics of aging parents requires setting clear boundaries before a crisis hits. Practically speaking, this physician and his parents need to shift from emotional wishes to a concrete, long-term caregiving strategy. According to family caregiving experts at AARP, adult children must be transparent about what they can actually afford without compromising their own financial security.

Families must map out a realistic timeline of care progression, especially with an Alzheimer’s diagnosis, where memory care expenses will inevitably skyrocket. The son could concretely help by hiring an elder care financial planner or geriatric care manager. A neutral third party can objectively assess the parents’ $800,000 nest egg and demonstrate exactly how fast an $11,000-a-month facility will deplete it.

By redirecting the conversation away from a blunt refusal to a professional review, he can preserve the relationship while firmly protecting his own future. Try setting up a family meeting with a certified advisor to review the numbers objectively. You could also research three sustainable alternatives to present alongside the financial reality check.

Setting financial boundaries with aging parents is incredibly challenging, especially when health crises are looming. This physician’s dilemma highlights the delicate balance between honoring our parents’ wishes and protecting our own long-term stability.

Do you think he is justified in refusing to fund their luxury lifestyle, or should he compromise to give them peace of mind? And how would you handle the escalating costs of memory care in this situation? Share your thoughts below!

Community Opinions

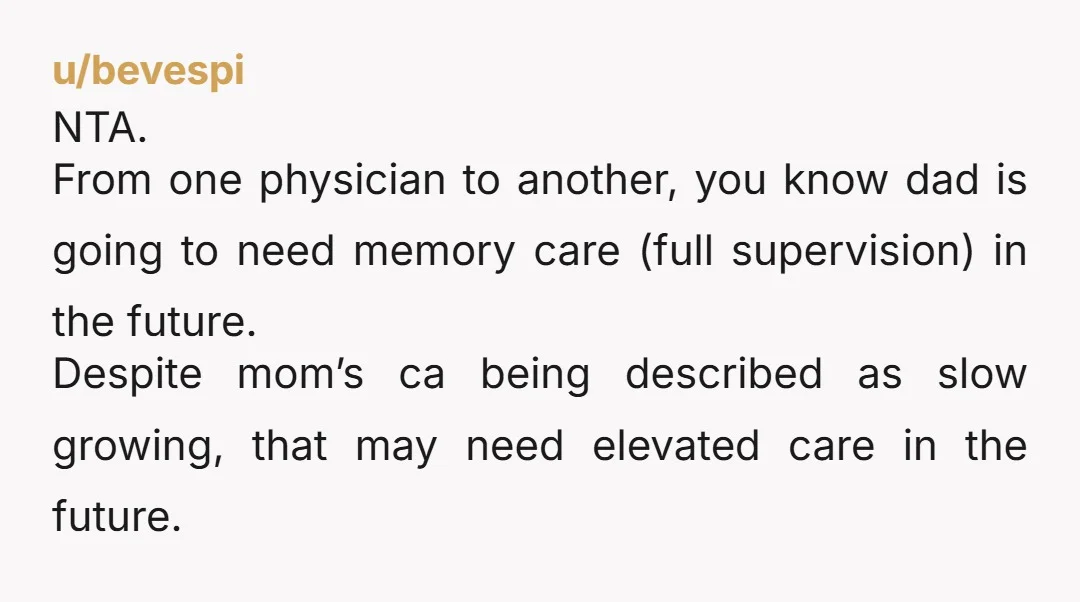

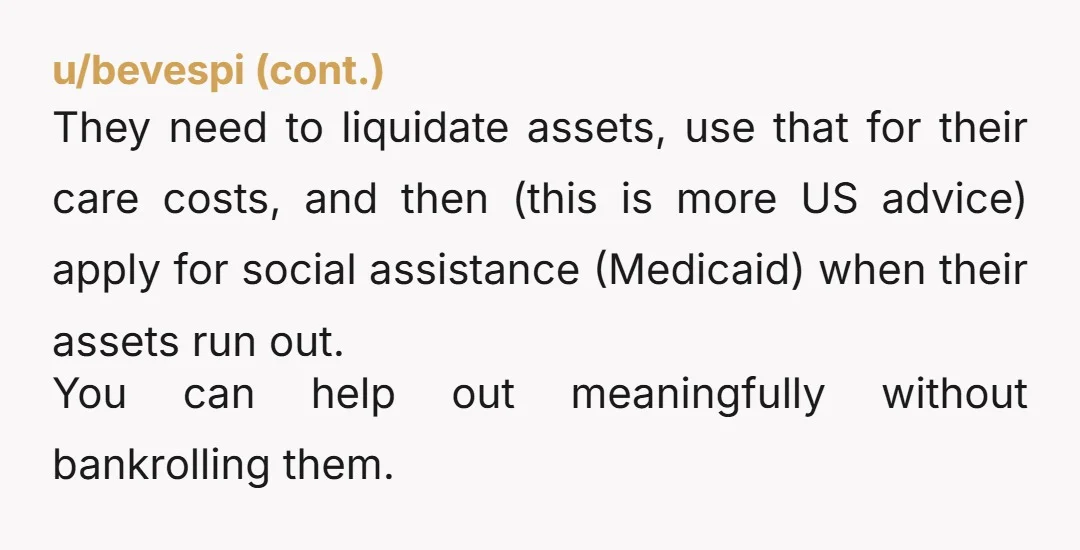

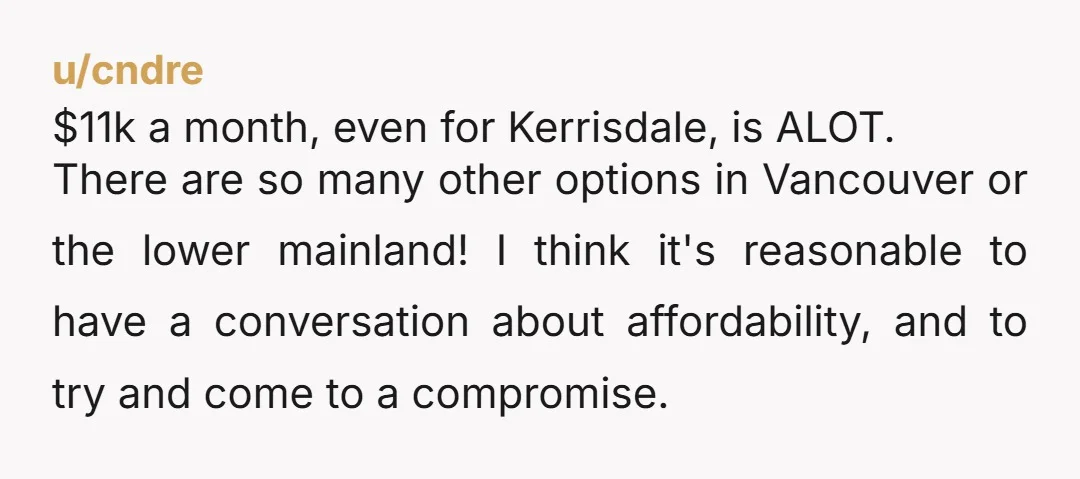

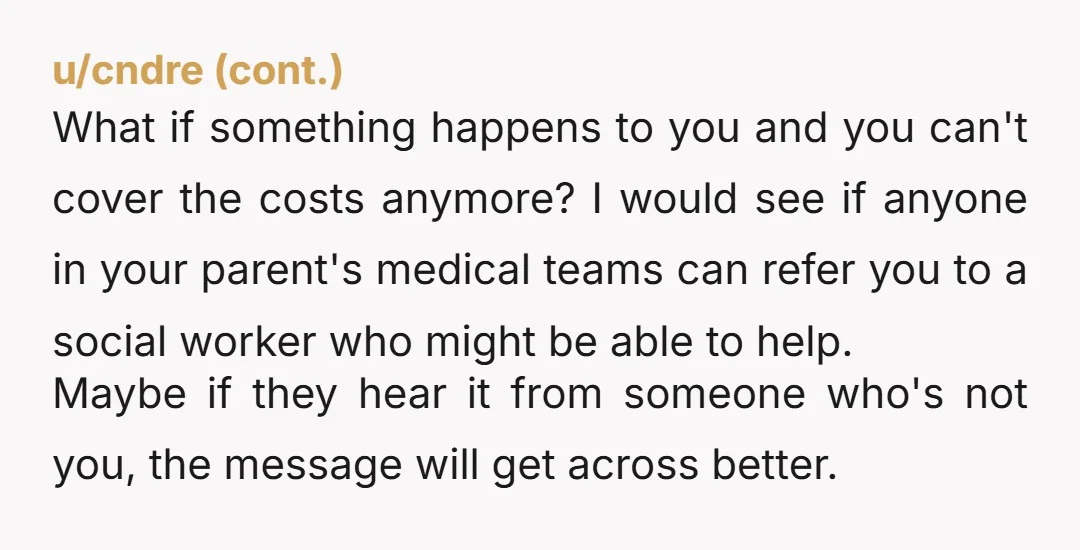

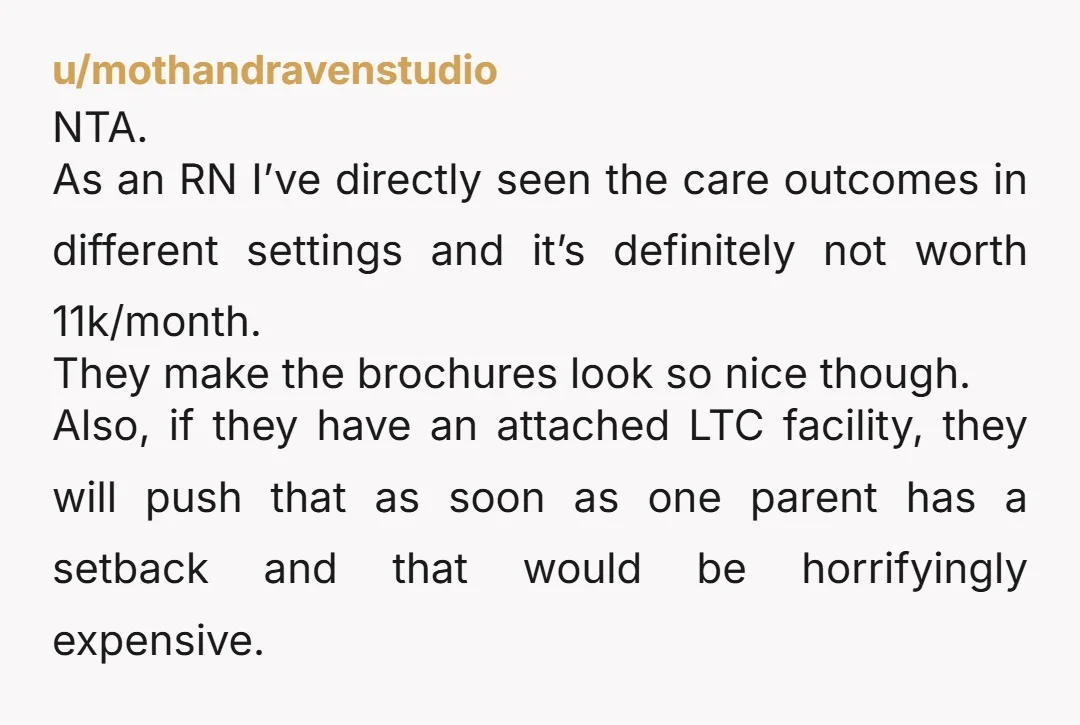

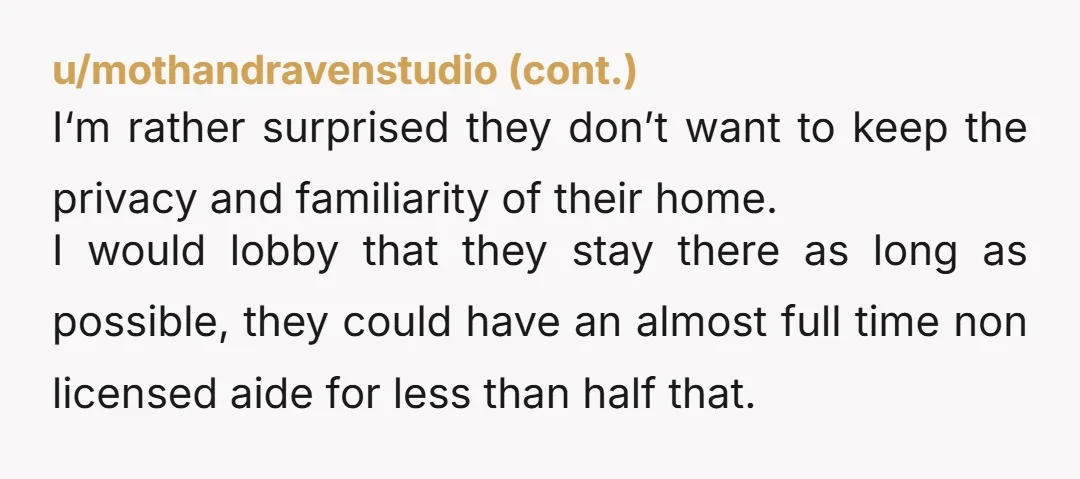

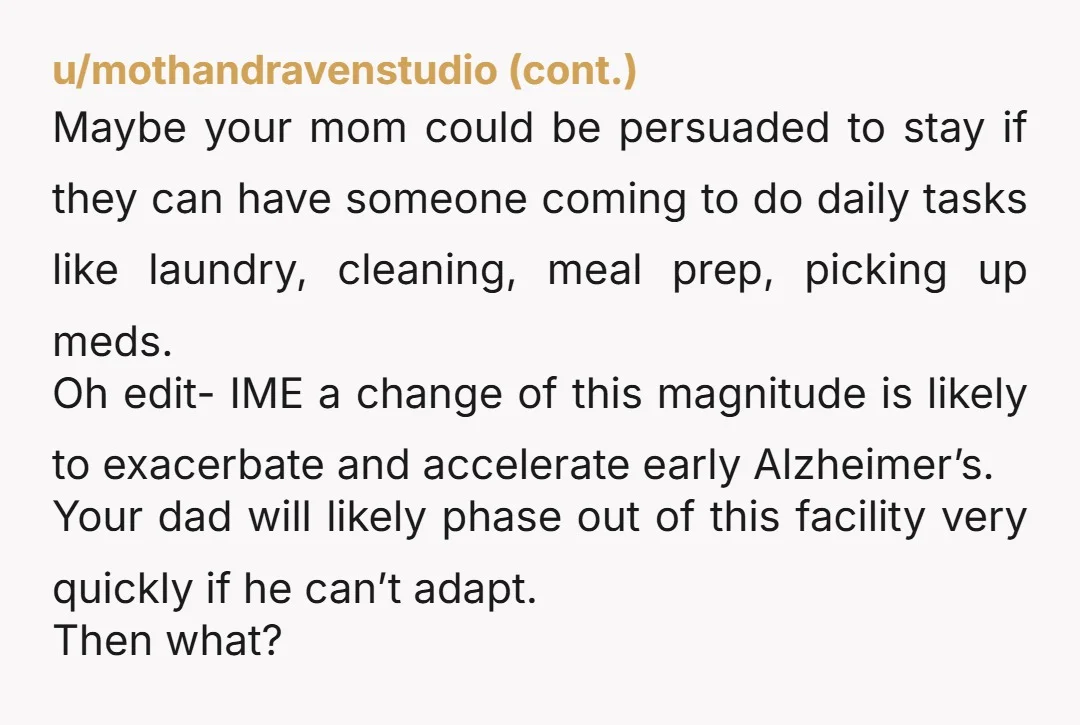

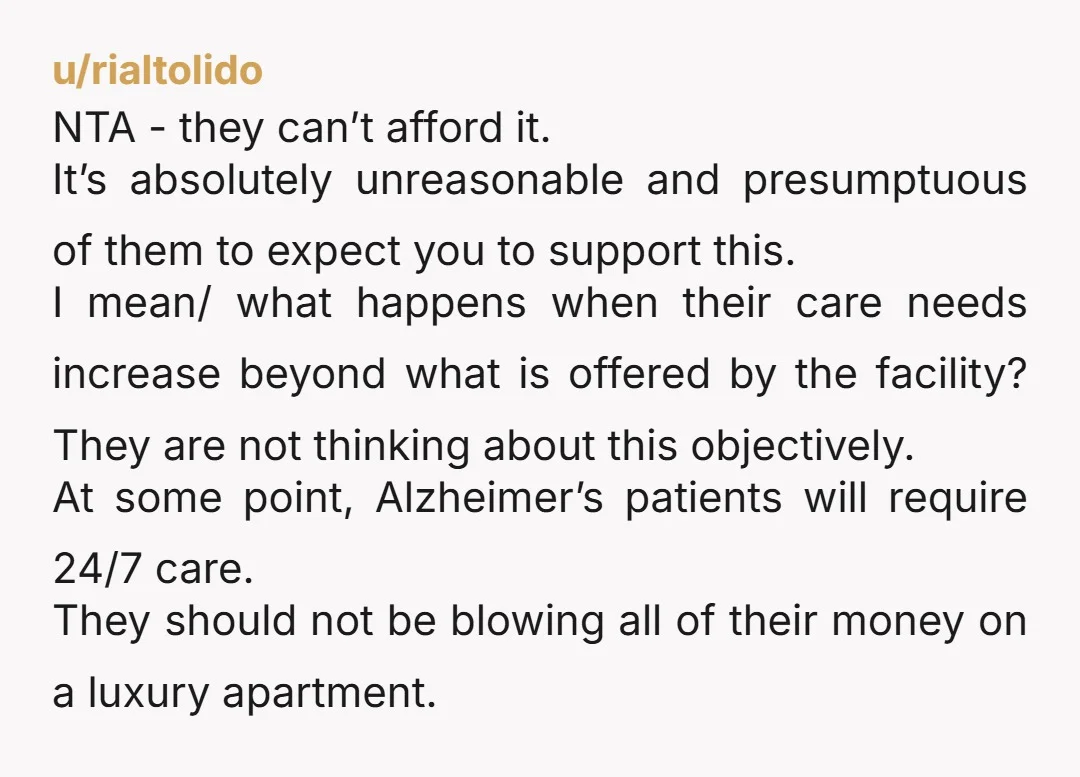

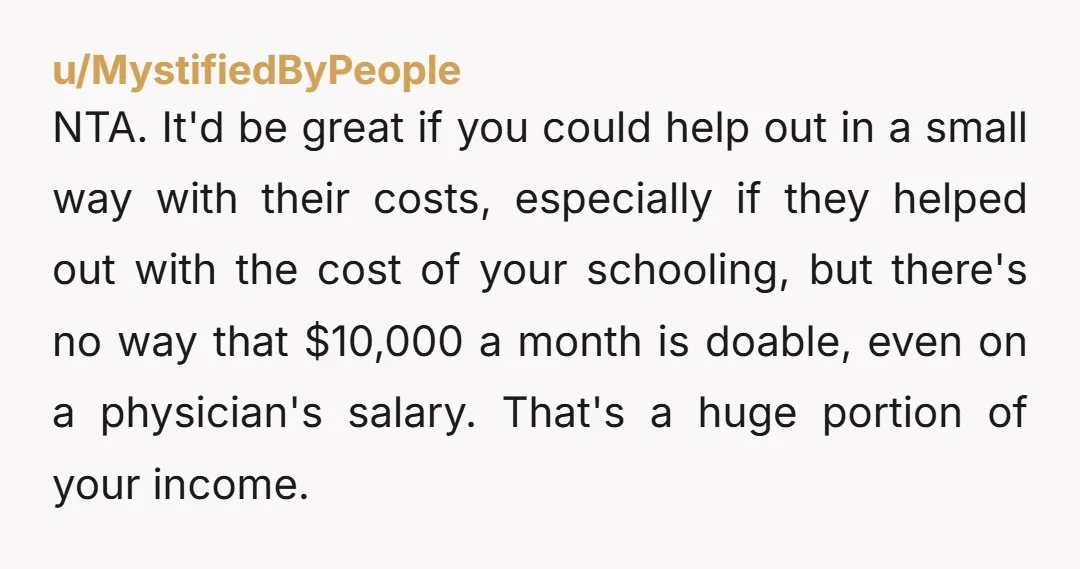

Reddit came in hot—nearly unanimous in defending the son, with many medical professionals chiming in to warn about the escalating realities of memory care.

A few voices gently reminded him to frame his refusal out of love and concern for their long-term security rather than just a flat denial.

Navigating the intersection of family obligations and personal financial health is incredibly tricky. Do you think the parents are being unreasonable with their luxury expectations, or did the son dismiss their final comforts too quickly? And how would you handle setting firm financial boundaries with parents facing serious health declines? Drop your thoughts in the comments.