WIBTA if I refused to help my mom pay for a $6,000 dental procedure?

Helping family financially often feels like the right thing to do, until trust starts to crack. One woman thought she was doing exactly that when she gave her mother thousands of dollars to pay off credit card debt. Instead, she discovered the money quietly disappeared into more spending, leaving her feeling misled and deeply used.

Now, years later, her mother is back with another request, this time for a $6,000 to $7,000 dental procedure. The stakes feel higher because it involves health, yet the fear of repeating the same mistake won’t go away. Caught between compassion and self-preservation, she turned to social media asking whether refusing outright, or insisting on strict conditions, would make her heartless. The responses were intense, emotional, and surprisingly blunt, revealing how complicated money becomes when family history is involved.

The situation began with what sounded like a straightforward request for help

What initially looked like progress quickly started to feel wrong

The realization was devastating once the numbers were added up

Now, facing another request, the emotional conflict feels impossible to ignore

This dilemma sits at the intersection of financial trauma and family obligation. The daughter isn’t reacting only to a new request; she’s reacting to unresolved hurt from the last one. Being financially betrayed by a parent can leave long-lasting scars, especially when the betrayal involved deliberate concealment rather than a one-time mistake. From the mother’s side, chronic overspending and reliance on credit often stem from deeper issues such as avoidance, emotional spending, or a lack of financial literacy.

Still, intention doesn’t erase impact. When someone repeatedly demonstrates they cannot manage borrowed money responsibly, trust becomes a rational boundary, not a punishment. Dr. Brad Klontz, a psychologist and financial behavior expert, has said that “money scripts formed in childhood can drive destructive financial behaviors well into adulthood.” That applies here on both sides: the mother’s spending habits and the daughter’s growing fear of becoming a permanent safety net.

Practically speaking, there are ways to help without exposing oneself to the same risk. If assistance is offered, paying the medical provider directly and treating the money as a gift rather than a loan can prevent future resentment. Clear limits, written agreements, or simply saying no are all valid responses depending on one’s emotional capacity. What matters most is recognizing that health emergencies don’t erase past patterns. Compassion does not require self-sacrifice to the point of harm, and helping once does not obligate someone to help forever.

Take a look at the comments from fellow users:

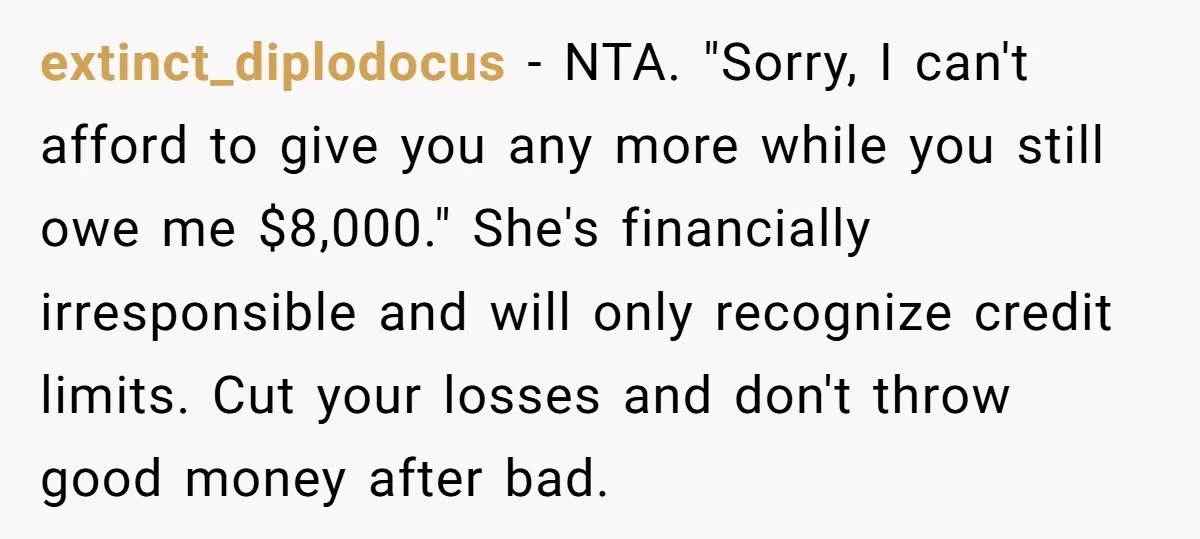

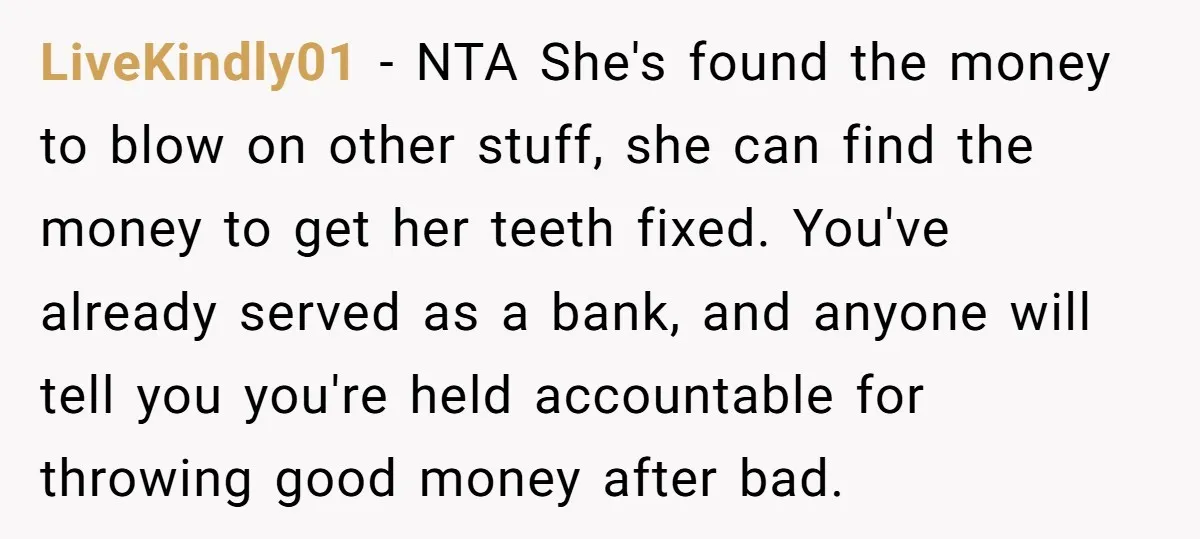

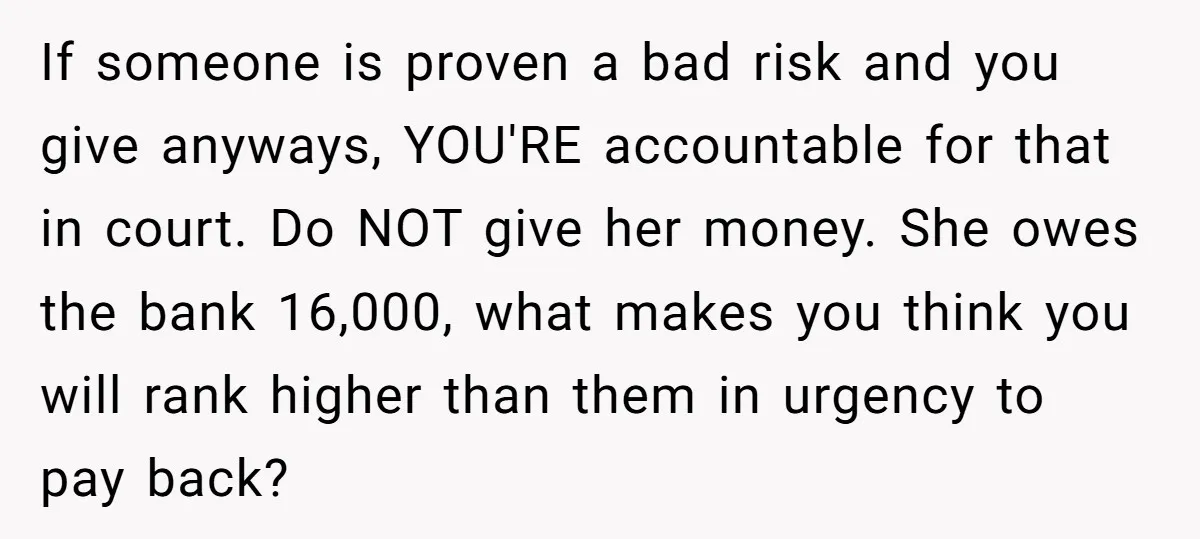

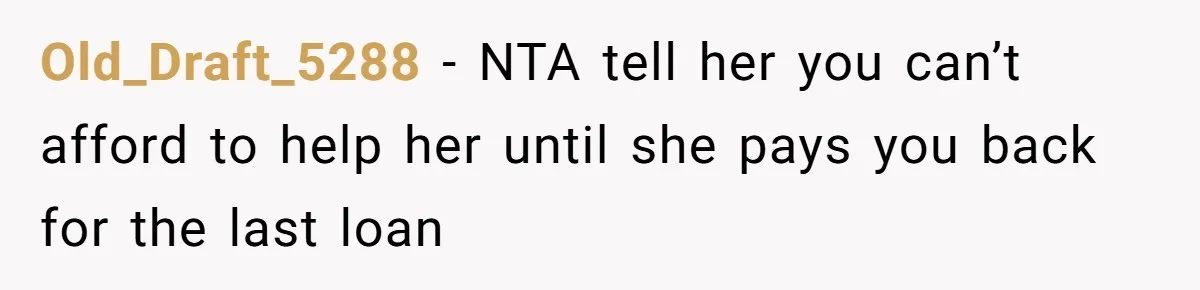

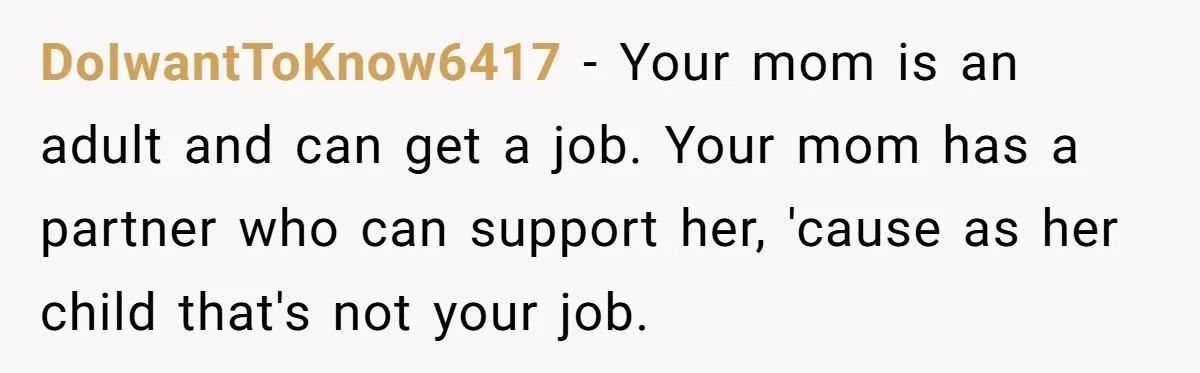

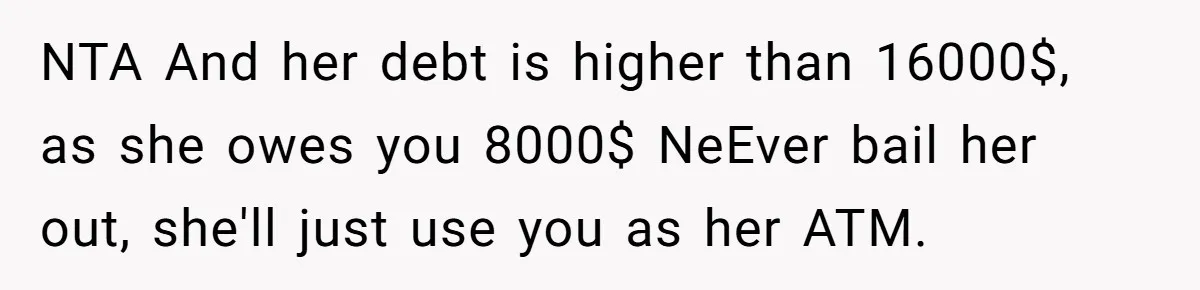

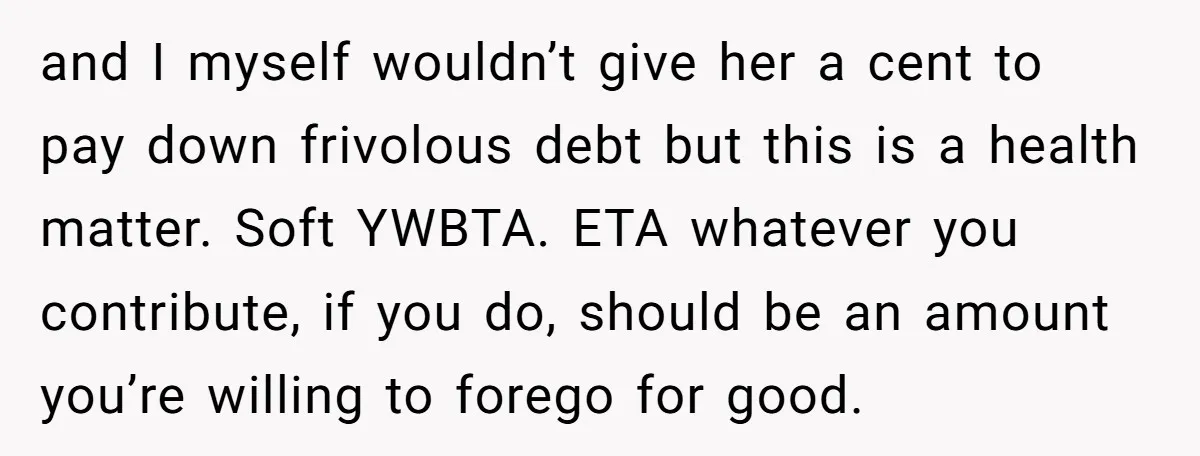

Many users firmly supported the daughter, urging her to protect herself financially

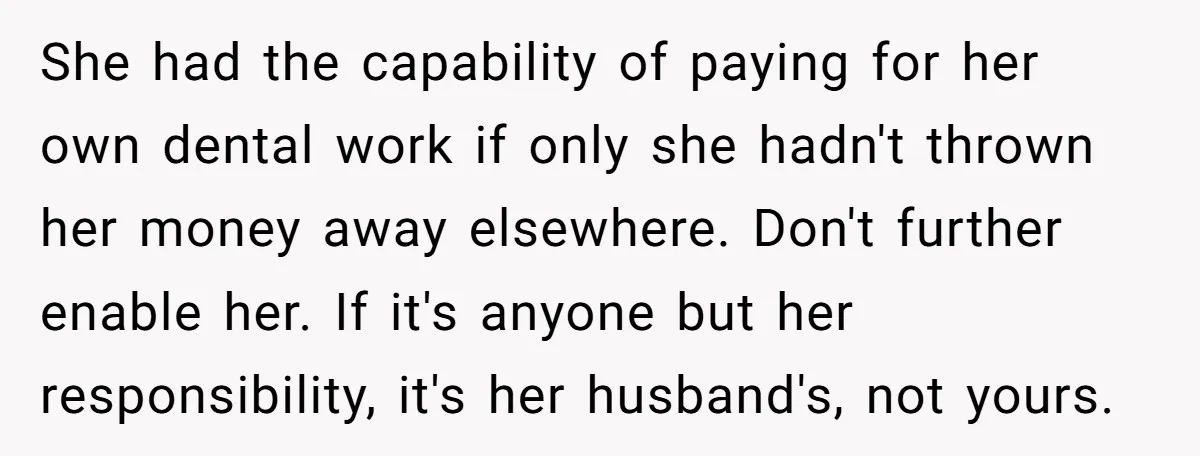

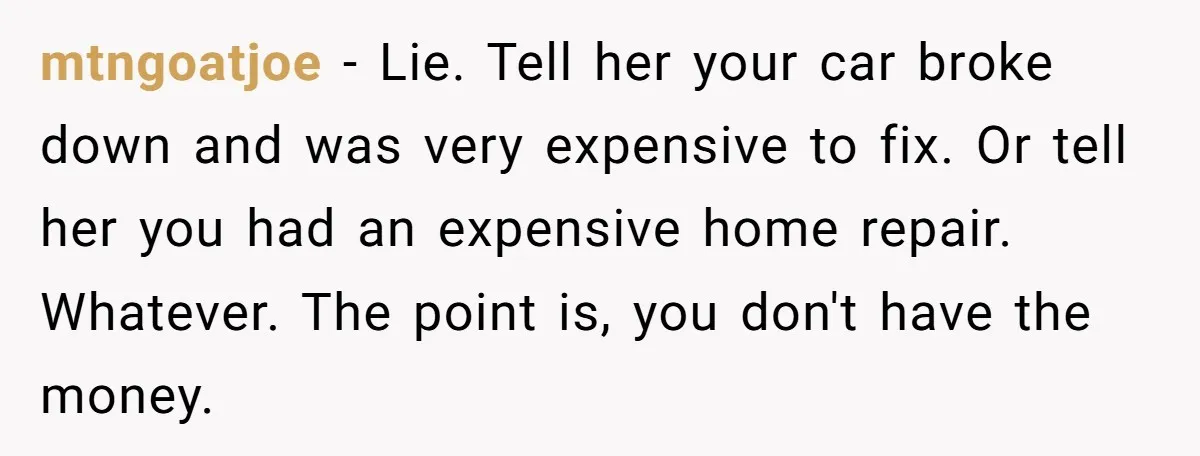

Others shared more conditional advice, focusing on minimizing risk if help was given

A smaller group leaned toward compassion, while still acknowledging the risk

This situation highlights how financial trust, once broken, can permanently change family dynamics. The daughter isn’t questioning whether her mother deserves care; she’s questioning whether she can survive another betrayal. Health concerns complicate the decision, but they don’t erase years of irresponsible behavior. Whether she chooses to say no, offer limited help, or step back entirely, the real issue is self-protection versus guilt. In this position, what would you do: help despite the risk, or finally draw a hard line?