AITA for telling my husband he doesn’t need to know the ins and outs of my debt if he isn’t helping me pay it off?

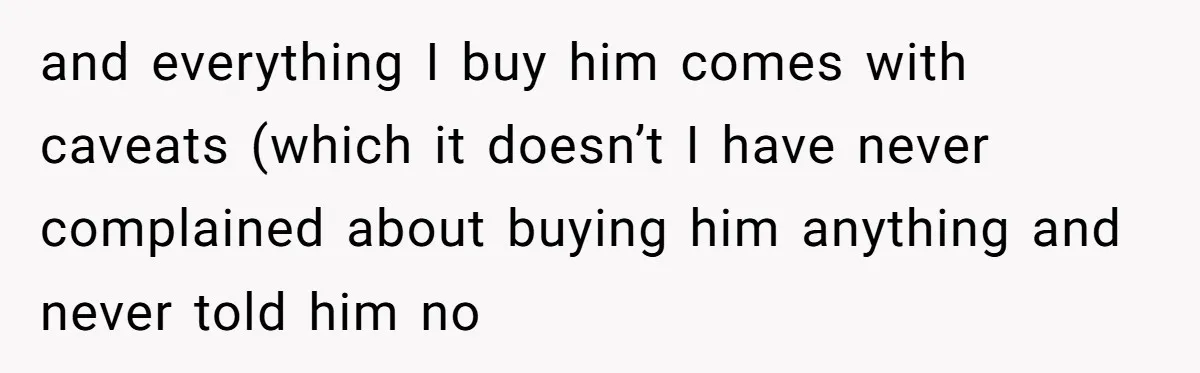

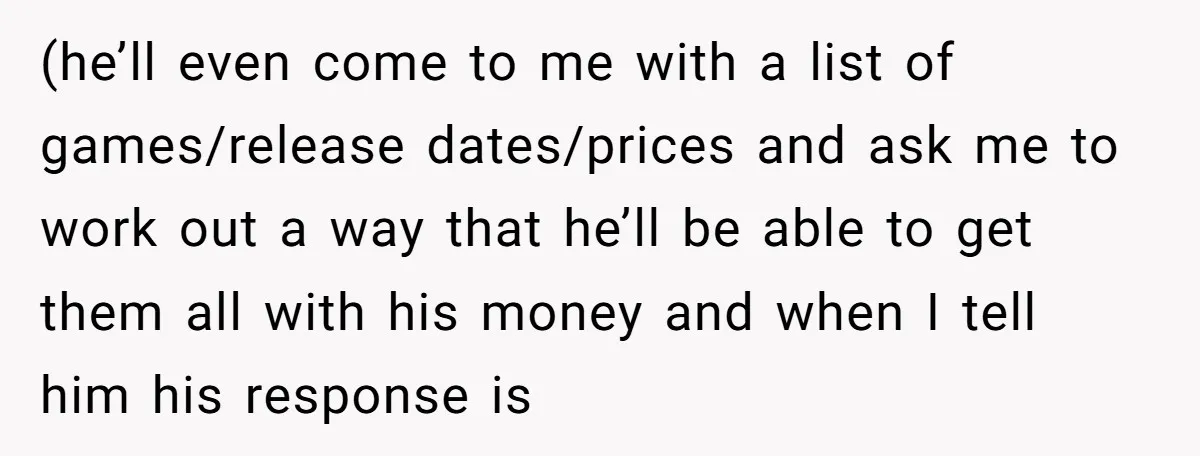

A 29-year-old working mom recently hit her limit with her 32-year-old stay-at-home husband over money. She handles full-time remote work while he cares for their 23-month-old son, but the financial dynamic has turned toxic. He demands a fixed £200 monthly “fun money” for games, constantly guilts her into extras like PSN cards, toy collections, and takeout—often putting the overflow on her credit card. After bills, she has less leftover than his allowance to chip away at her debt.

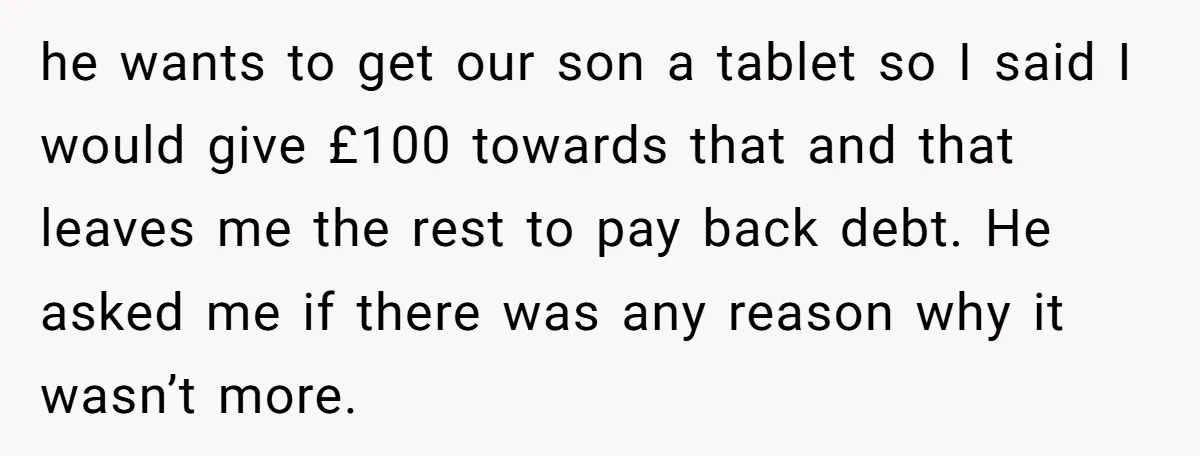

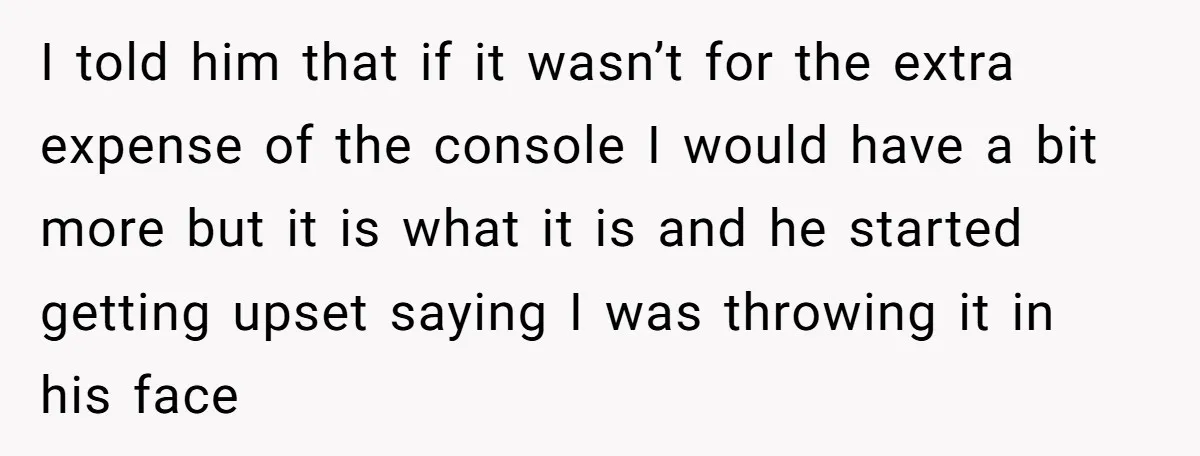

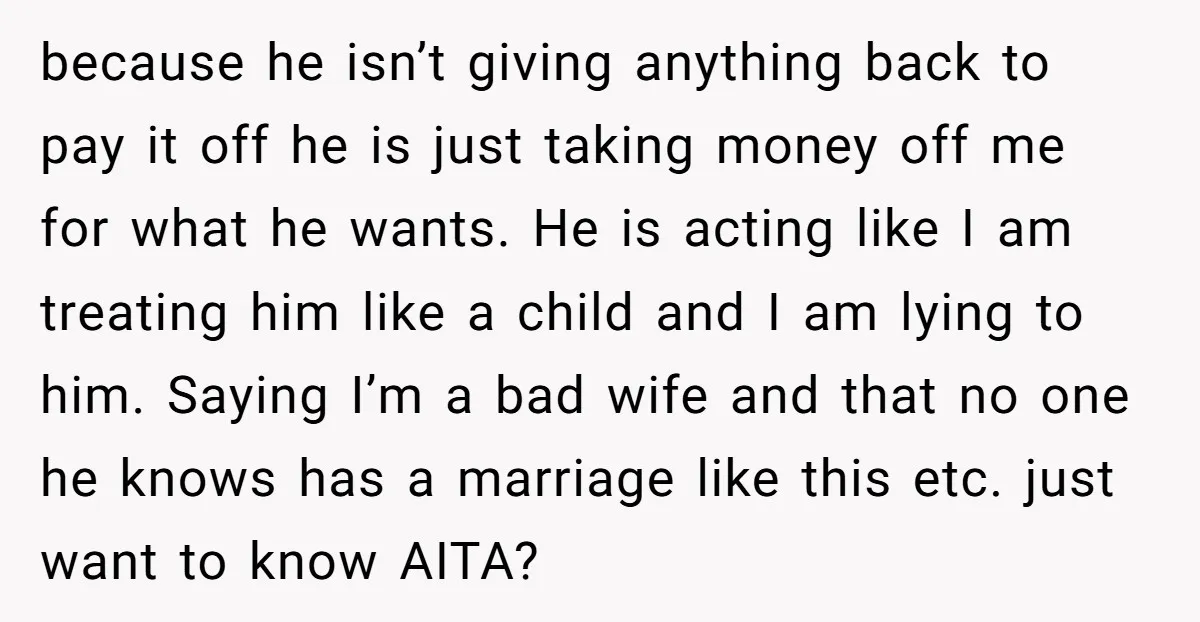

When a £1600 after-tax bonus arrived, she allocated £900 to him (£600 for a PS5 Pro, £300 for a collector’s edition game), £100 toward a tablet for their toddler, and the rest to debt. He questioned why it wasn’t more, accused her of throwing expenses in his face, then demanded full debt details. She shared the amount but said he doesn’t need the “ins and outs” since he isn’t contributing to repayment—he just spends. Now he calls her a bad wife, claims she treats him like a child, and says no one else has a marriage like this. Is she wrong for keeping financial details private?

‘AITA for telling my husband he doesn’t need to know the ins and outs of my debt if he isn’t helping me pay it off?’

The imbalance has been building for months with constant requests that exceed budgets:

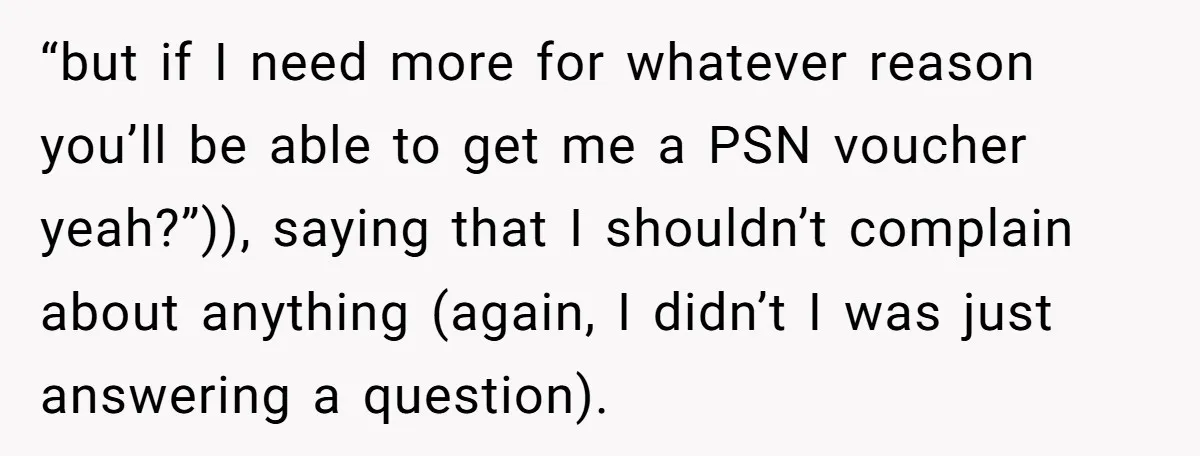

The bonus sparked the latest blow-up:

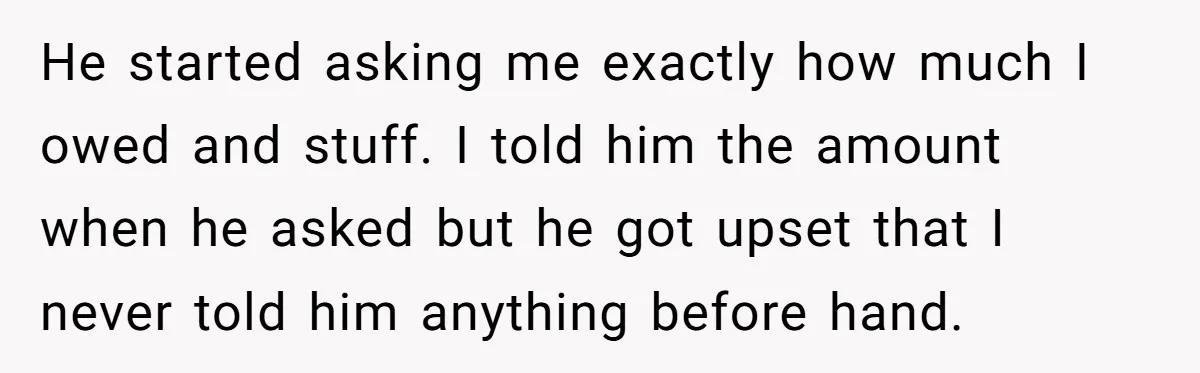

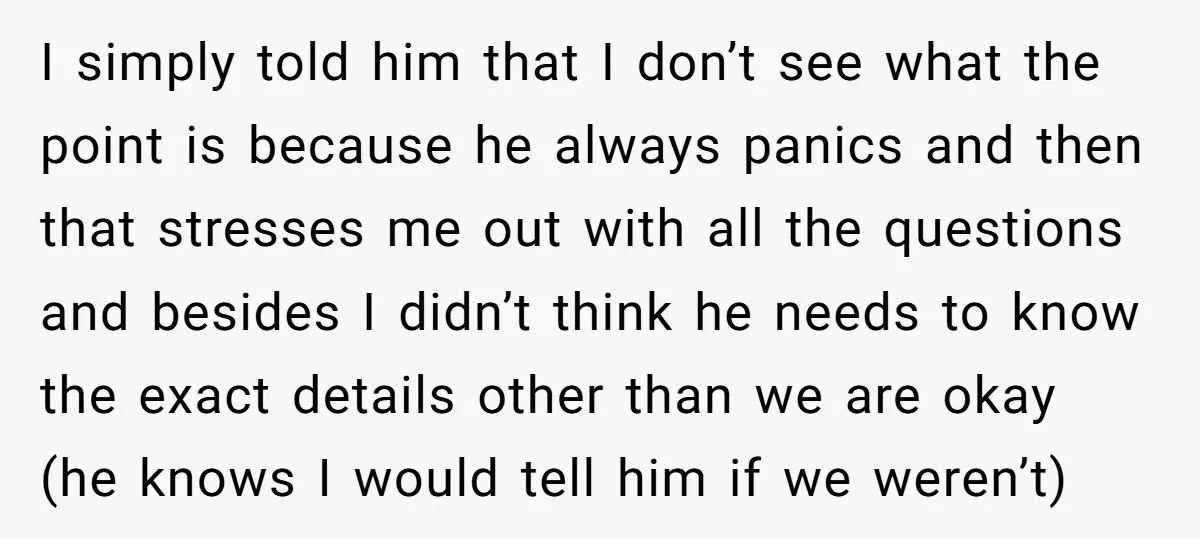

He pressed for full transparency, but she pushed back:

This dynamic has shifted from partnership to something closer to parent-child, where one spouse controls spending while the other demands extras without accountability. The husband’s repeated guilt-tripping and overspending—pushing extras onto credit cards—creates unsustainable debt pressure, especially when he refuses deeper financial involvement despite regular offers to share info.

From his perspective, being kept in the dark about exact debt figures can feel infantilizing or secretive, particularly in marriage where finances are joint. However, his panic reactions and refusal to engage in budgeting undermine any claim to full transparency. Healthy couples discuss numbers openly to build trust, not weaponize ignorance or demands.

Marriage and financial therapists often stress that debt incurred during marriage is typically “marital debt,” regardless of whose name is on it. When one partner overspends while the other shoulders repayment, resentment builds fast. According to financial psychologist Dr. Brad Klontz (co-founder of Your Mental Wealth Advisors), unequal financial power dynamics—like one spouse treating allowances as entitlement while ignoring debt—frequently signal deeper control or avoidance issues that benefit from couples counseling focused on shared responsibility (source: Klontz’s work on money disorders in relationships).

Practical steps include creating a joint monthly budget meeting where both review income, bills, debt payments, and discretionary spending—no exceptions. Set hard limits on “fun money” and stick to them; anything extra requires mutual agreement. If guilt-tripping continues, individual therapy can help the working partner build boundary skills, while couples counseling addresses why one partner avoids financial adulthood. Debt repayment should take priority over luxury purchases until the balance drops significantly.

Here’s the comments of Reddit users:

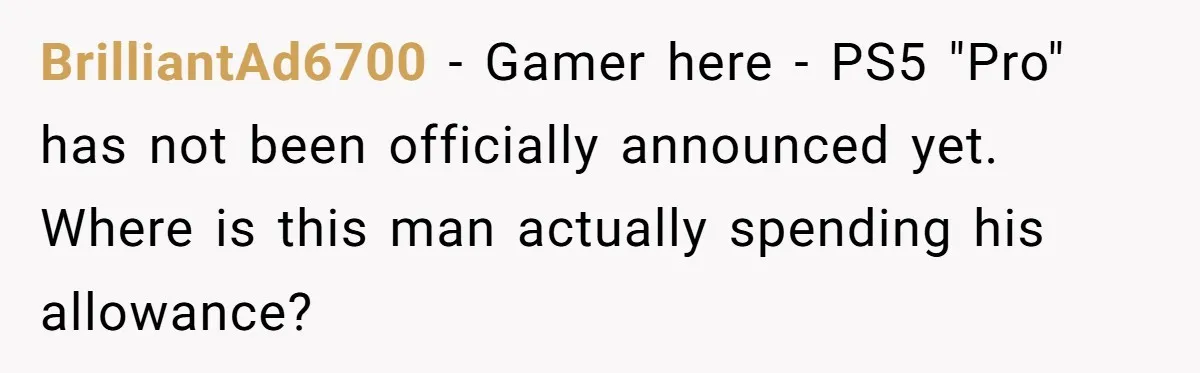

The community largely sided with NTA, slamming the husband’s entitlement, gaming obsession, and lack of contribution while urging OP to stop enabling the behavior:

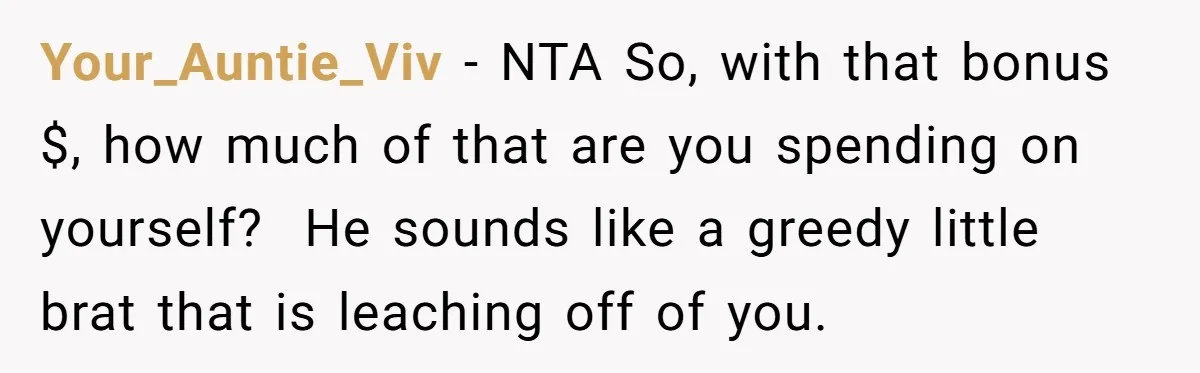

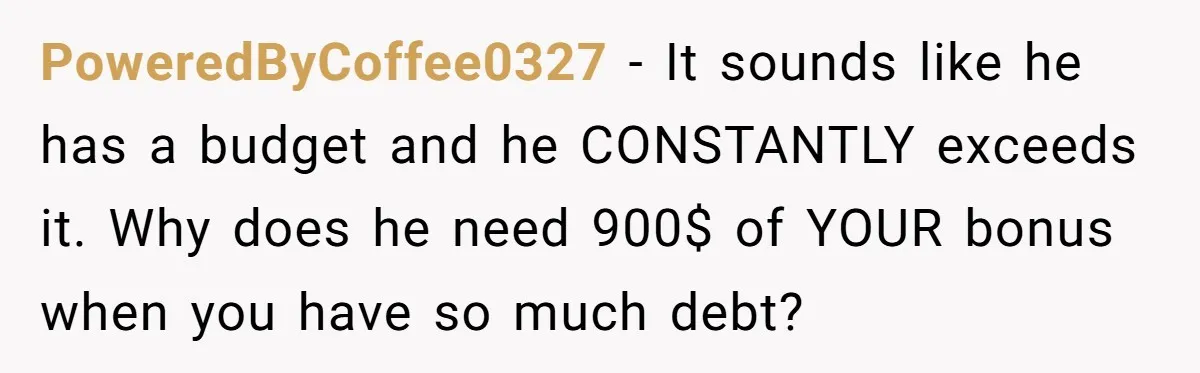

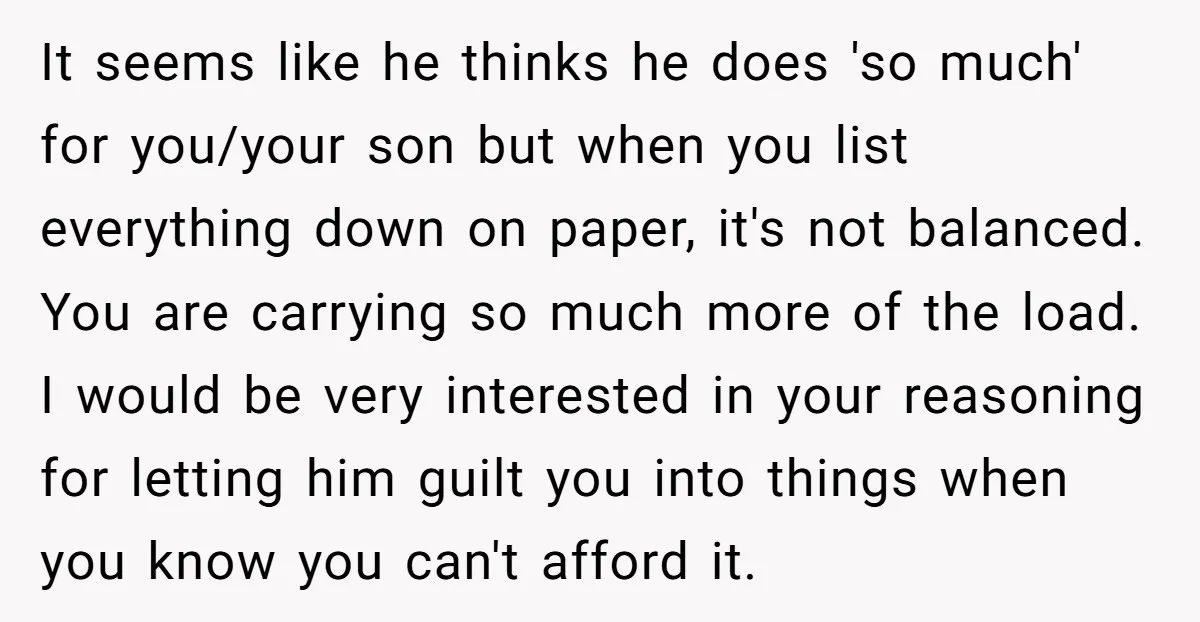

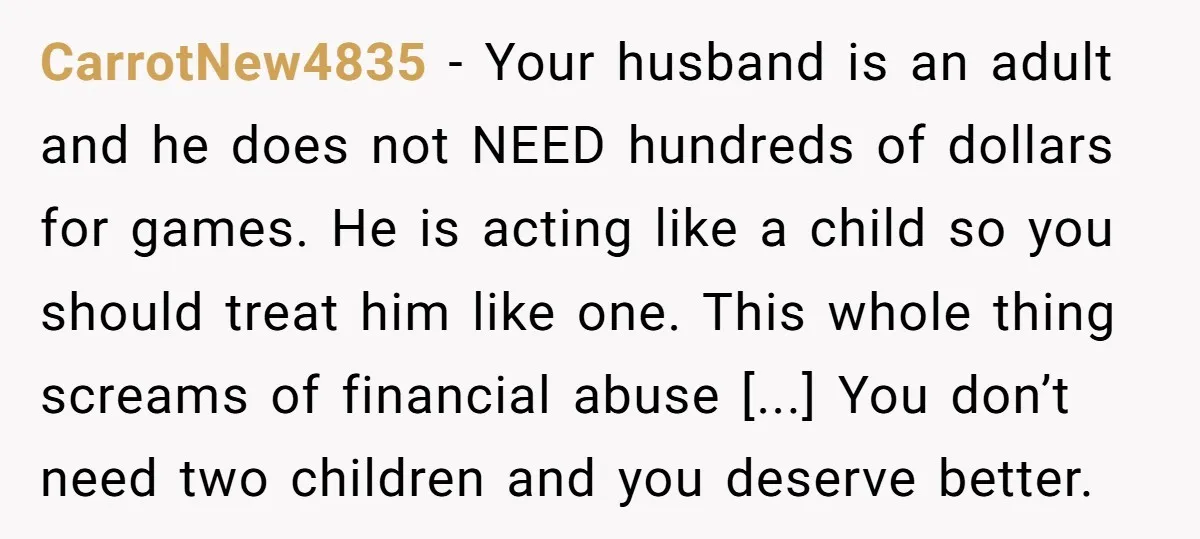

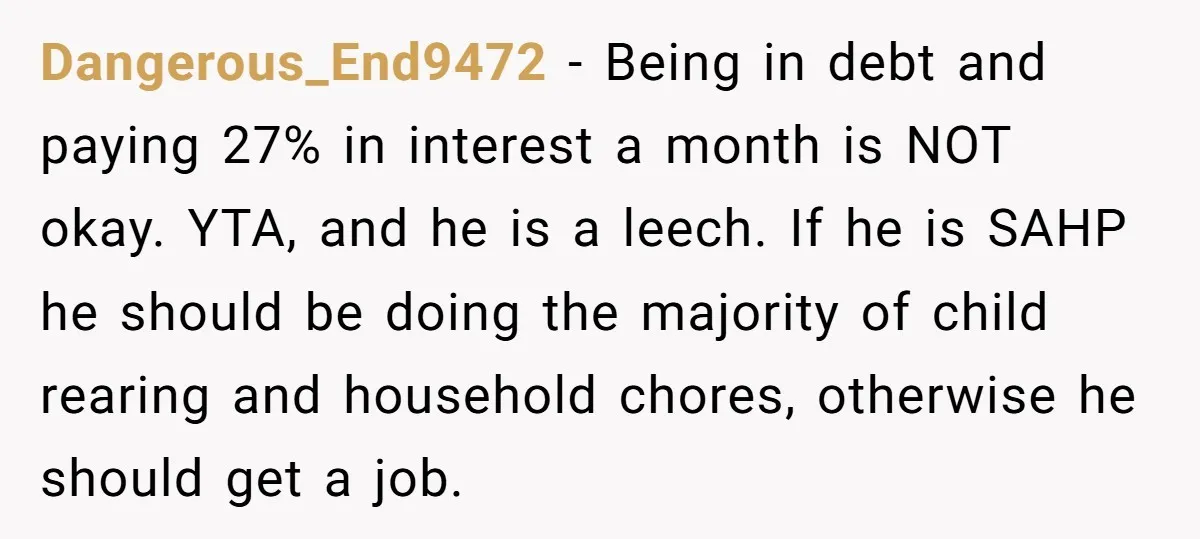

Many commenters called out financial abuse and unequal load-bearing:

![Ornery-Process - NTA- [...] I think you really need to take a good hard look at why you’re with someone who treats you so poorly. It doesn’t seem like your...](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1768440749765-6.webp)

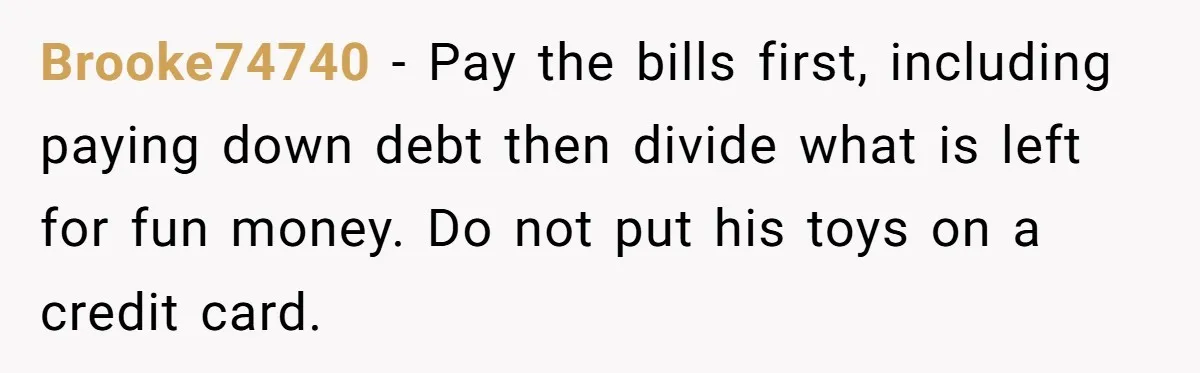

Practical advice focused on boundaries, budgeting, and reevaluation:

![SoMuchMoreEagle - ESH This arrangement does seem to be more of a parent-child one than equal partners. [...] Panic is not good [...] But that doesn't mean you should just...](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1768440739156-3.webp)

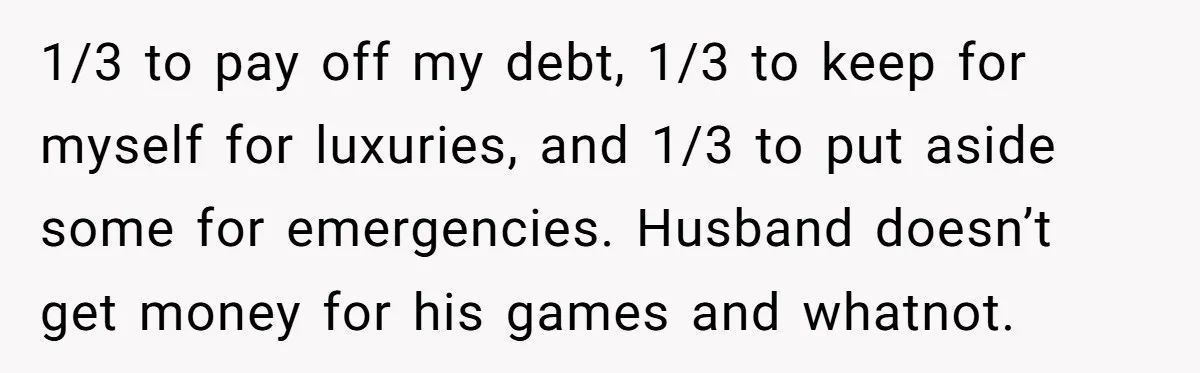

![Mundane-Scarcity-219 - If I were OP, I would never tell husband that I even got a bonus/raise [...] Then divide the windfall into thirds:](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1768440740111-4.webp)

Some questioned his actual SAHP role and suggested drastic steps:

![bestbobever - INFO - You say he is a stay at home parent. How much does he actually contribute to the overall managing of the household? [...]](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1768440731418-1.webp)

![NTA - or maybe ESH your husband isn’t a stay at home parent, he just stays at home. [...] In 20 years would you be happy if their future long...](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1768440732371-2.webp)

Sarcasm and direct calls to action rounded it out:

![[Reddit User] - Tell him to get a job](https://en.aubtu.biz/wp-content/uploads/2026/01/wp-editor-1768440700700-3.webp)

This situation highlights how quickly “fun money” can become one-sided entitlement when debt looms and contributions feel unbalanced. OP isn’t wrong for protecting her peace around finances, but long-term, transparency and mutual budgeting might prevent bigger blow-ups—or reveal if the partnership is truly equal.

What would you do here? Force a full budget sit-down? Stop extras completely? Or is it time to rethink the whole setup? Drop your thoughts below.