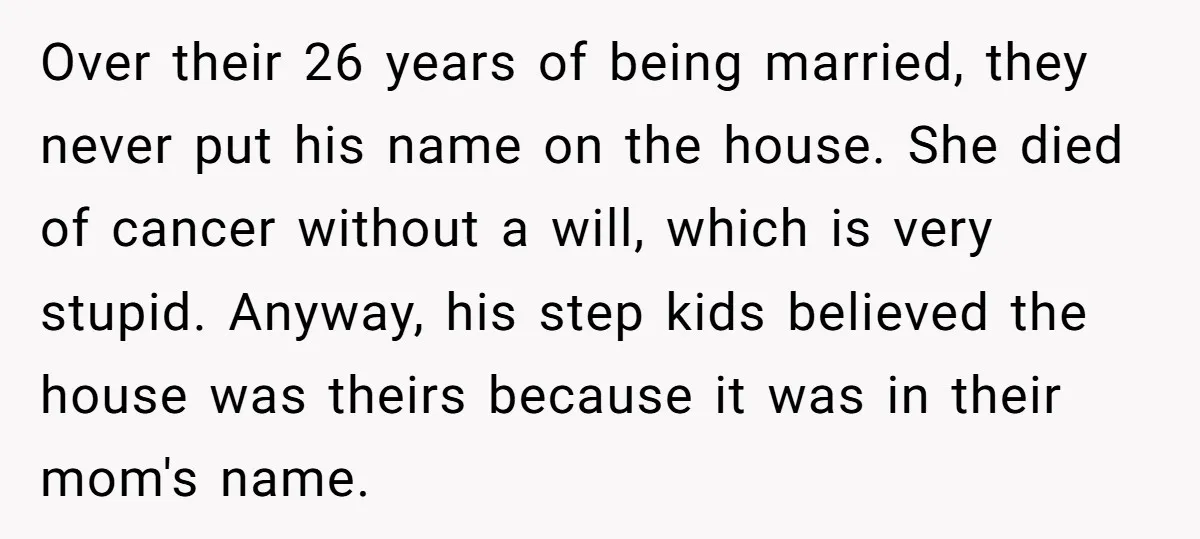

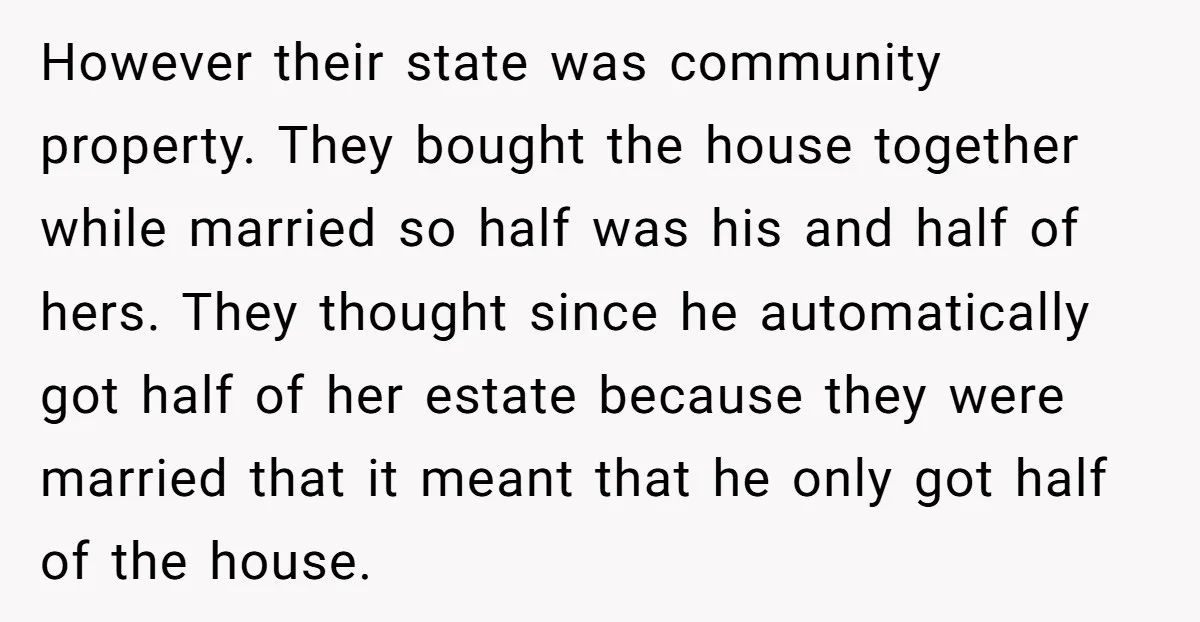

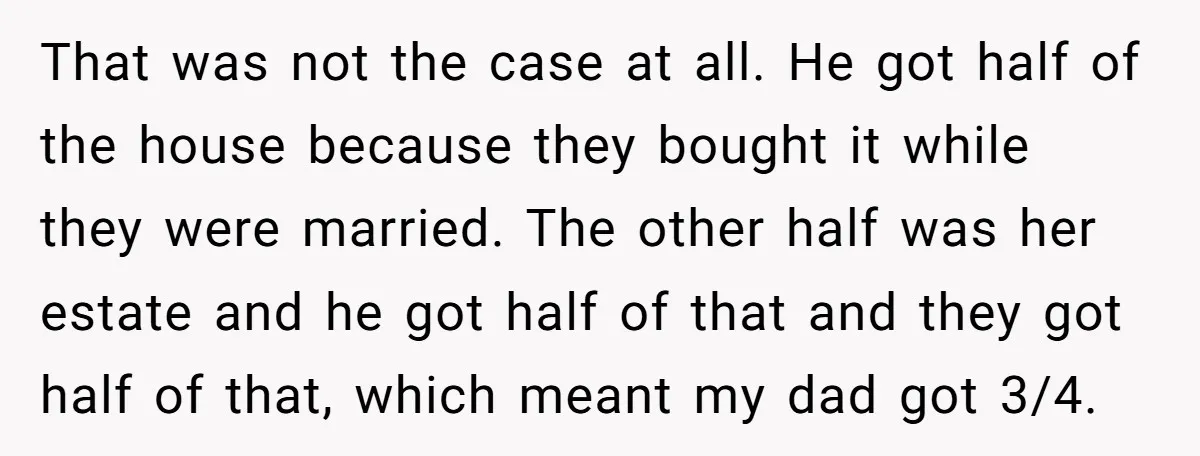

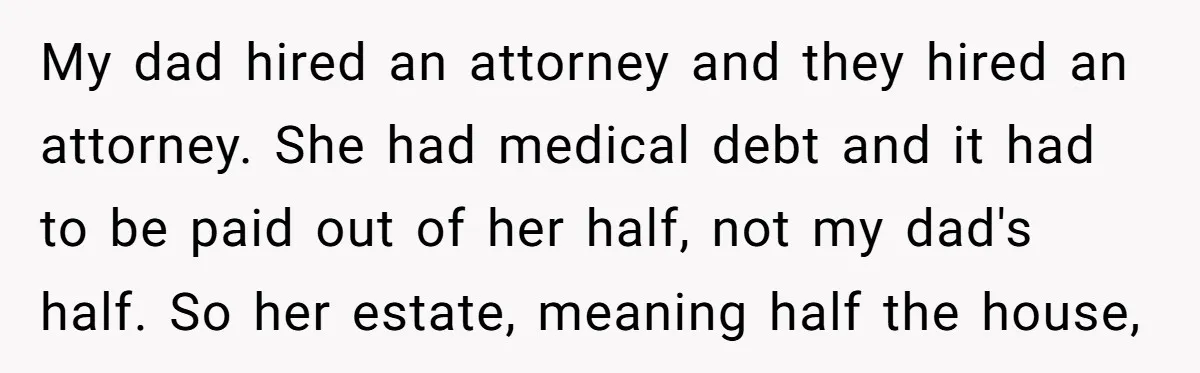

AITAH for keeping my moms small life ins that was left to me?

A 59-year-old single woman is standing firm after her mother’s passing, refusing to share the $5,000 life insurance policy that was left solely to her. For 13 years she was her mom’s full-time caregiver—providing round-the-clock care even though she was only paid for 40 hours a week—while her four siblings offered zero help despite repeated pleas.

When mom passed, she left the policy to her daughter as “starting over money,” knowing how much sacrifice had been made. But the siblings, who are financially comfortable, exploded in anger, demanding a share and even insisting she cover final expenses. With no home, no job, a broken Jeep, and grief hitting hard, she used the money to fix her car, secure a place to live, and buy groceries. Now the family is trashing her—leaving her wondering if she’s the asshole for putting herself first for once.

‘AITAH for keeping my moms small life ins that was left to me?’

The full situation unfolded after years of one-sided caregiving:

The daughter gave 13 years of her life—far beyond the paid 40 hours—providing 24/7 care without meaningful support from siblings. It’s common in elder care dynamics for the primary caregiver to sacrifice career, housing stability, and personal life, only to face resentment when inheritance decisions reflect that reality. The mother clearly intended the policy as a small but deliberate thank-you and safety net—designating her daughter as the sole beneficiary was not accidental.

From a legal and ethical standpoint, life insurance proceeds paid directly to a named beneficiary are not part of the estate. They bypass probate and are not subject to claims from other heirs or even final expenses unless the policy specifies otherwise. Experts in estate planning (such as those from the American Bar Association and Nolo) emphasize that the deceased’s choice of beneficiary should be honored without guilt. Siblings demanding a share—especially when financially secure—are often driven by entitlement rather than fairness.

Psychologically, this can feel like a final invalidation of the caregiver’s sacrifice. Grief counselors note that absent siblings frequently project guilt onto the caregiver through accusations of greed, when in truth they’re avoiding accountability for their own neglect. The daughter is not obligated to redistribute the funds, particularly when she was left homeless and jobless overnight.

Practical steps forward: Keep records of the beneficiary designation and any communications showing mom’s intent. If siblings escalate (threatening legal action), a quick consultation with an estate attorney can confirm the money is hers alone—most would back off once informed. Long-term, consider low-contact or no-contact if the toxicity continues; protecting mental health after such a long caregiving role is essential. This small sum isn’t about wealth—it’s about honoring a mother’s final wish and allowing the daughter to finally rebuild. She deserves that peace.

Check out how the community responded:

The online community overwhelmingly supported the woman, blasting the siblings as greedy and selfish while praising her for finally putting herself first:

Almost everyone agreed the money is rightfully hers—mom made her choice for good reason:

Many shared empathy and called out the siblings’ entitlement:

Honoring a loved one’s final wishes is one of the last ways we can show respect, especially after years of selfless caregiving. The $5,000 isn’t just money—it’s a mother’s quiet acknowledgment of her daughter’s extraordinary sacrifice, and keeping it is not selfish; it’s rightful.

You’re not the villain here—the siblings’ anger says more about their guilt than your actions. Be gentle with yourself during this grief. You’ve earned the chance to rebuild. Have you faced similar family pressure after a loss? How did you handle it? Share below—we’re here for you.

![[UPDATE] My (26M) brother (29M) is married to, and cheating on my best friend (26F) and I’m conflicted if I should say anything.](https://en.aubtu.biz/wp-content/uploads/2025/05/87654-768x403.jpg)