AITA for giving my son’s college fund to my daughter?

A father reallocates his middle son’s untouched college fund to his ambitious daughter pursuing medical school, igniting fury from the 29-year-old who skipped higher education. The parents saved generously for each child to attend any college debt-free, yet the son opted for minimum-wage jobs without trade skills or further training. Now demanding the cash for personal use, he clashes with his dad’s refusal to fund “beers and video games.”

The daughter, eager to avoid crushing debt in her doctor path, accepts the boost. The son labels his father cruel for withholding “his” money. What makes the story more complicated is the fund’s original education-only intent versus adult entitlement claims.

‘AITA for giving my son’s college fund to my daughter?’

Equal college savings were set aside for all children to ensure debt-free futures.

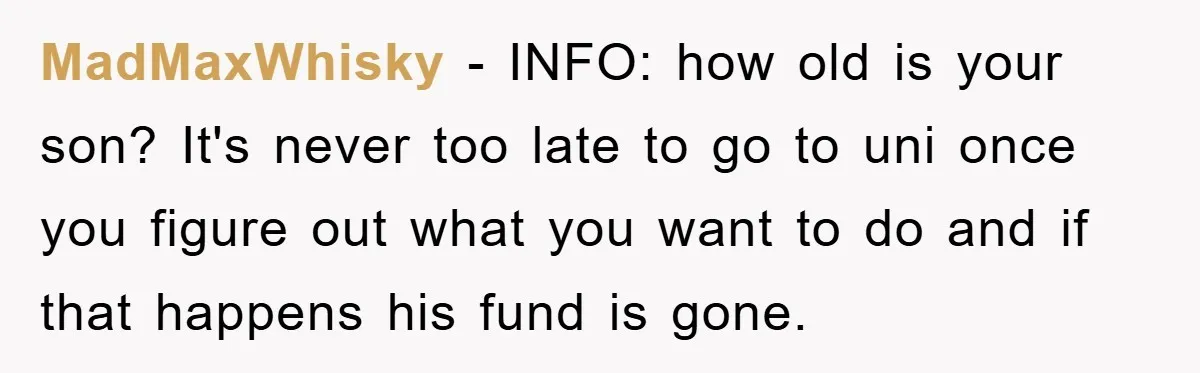

The middle son’s choices bypassed education, despite parental concerns over limited prospects.

Redirection of funds to the pursuing sibling sparked demands and accusations.

Parental savings tied to specific goals like education retain donor control, not automatic child ownership upon adulthood. The father’s conditional approach—funds activate for college or trades—aligns with intent to launch responsible futures, not handouts. Redirecting to the daughter honors productivity while the son’s demands treat the pot as inheritance, ignoring its purpose. At 29, his minimum-wage path reflects choices, not barriers, making cash release risky for squandering.

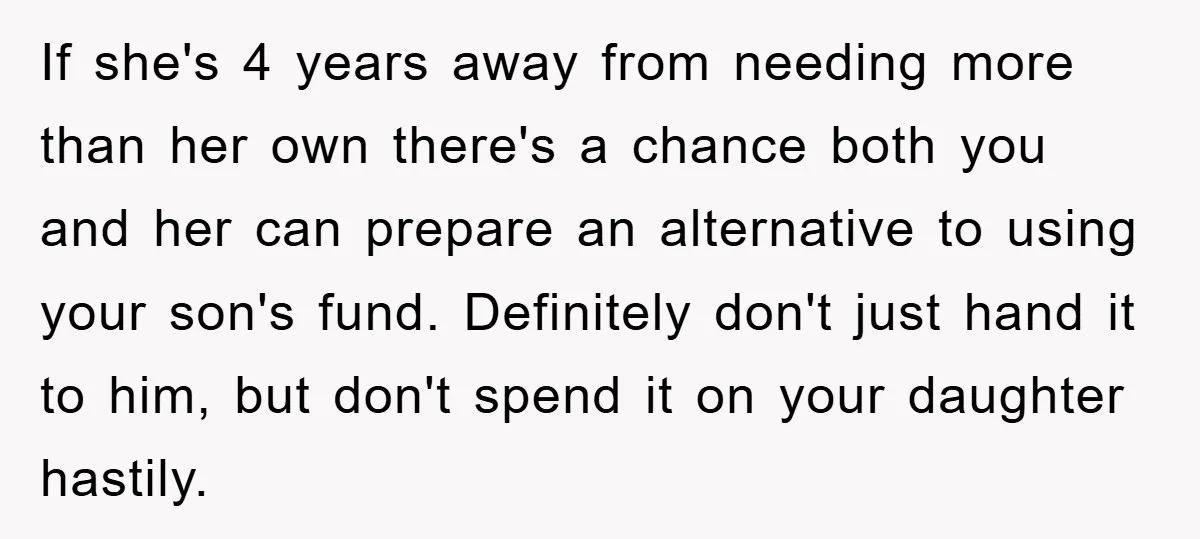

Opposing angles stress potential resentment or late-blooming education needs; holding a portion could bridge gaps. Yet haste in spending ignores medical school timelines. Critics note early fund disclosure breeds entitlement. What makes the story more complicated is balancing autonomy with accountability—freedom means self-funding non-educational lives.

Financially, earmarked gifts avoid entitlement traps. As estate planner Suze Orman states in The Money Book for the Young, Fabulous & Broke, “Money given with strings is a loan; without, a gift—but parents set the terms.”

Here’s the comments of Reddit users:

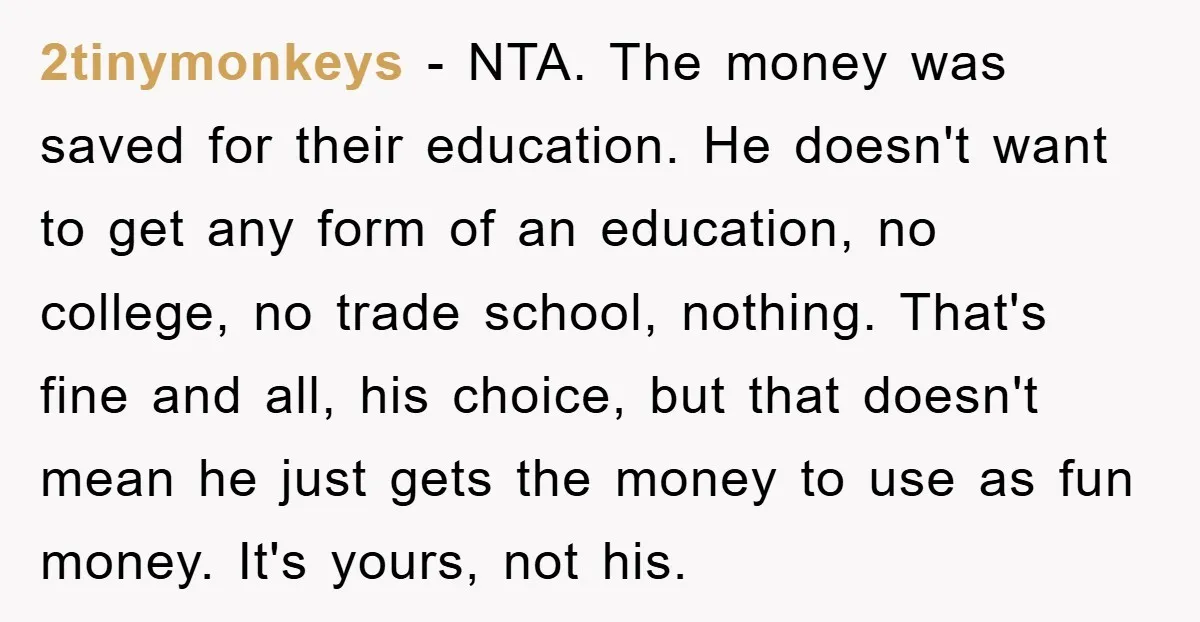

Many users defend the father, insisting funds stay education-bound without handouts.

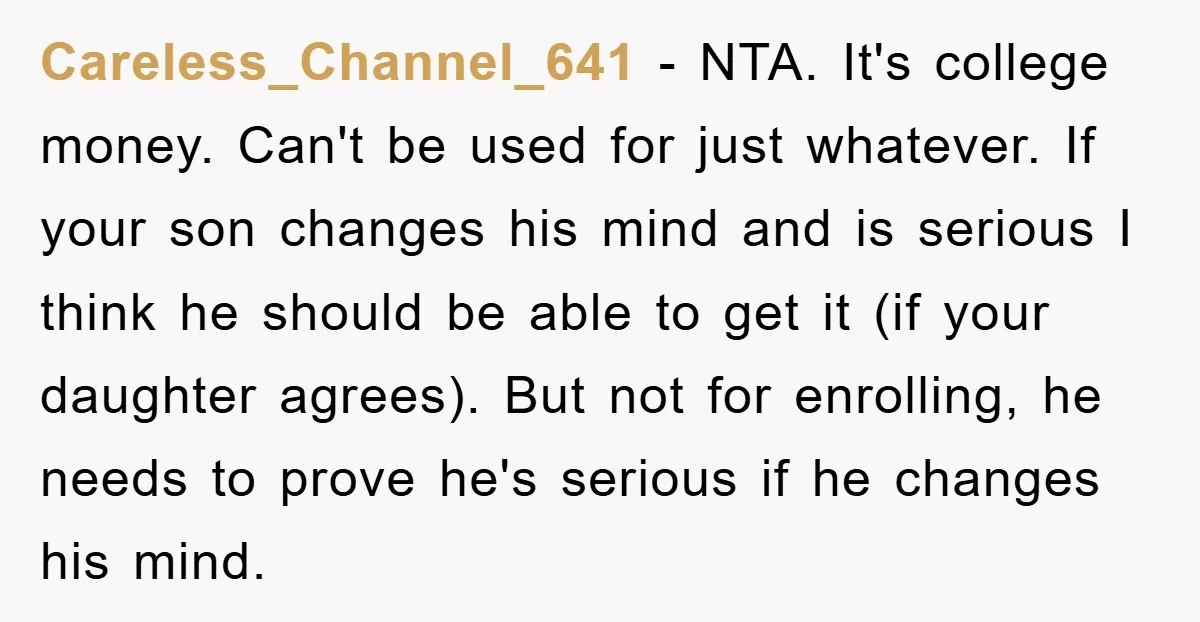

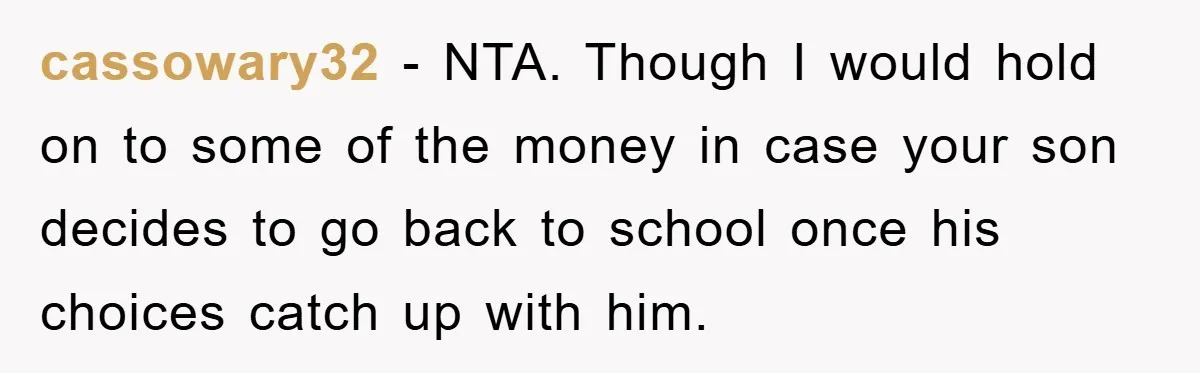

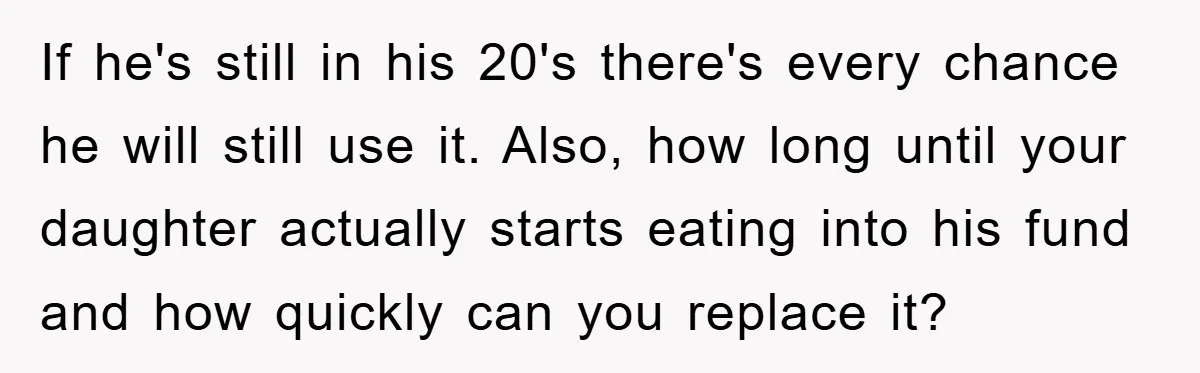

Some commenters propose safeguards, like reserves for future shifts while prioritizing current use.

Light-hearted voices jest about late realizations, easing family fund drama.

The father steadfastly guards the fund’s original mission—fueling education—by channeling it toward his daughter’s medical dreams, refusing to let it vanish into non-educational pursuits despite his 29-year-old son’s heated objections. This choice underscores that parental support, while generous, remains tethered to shared goals of growth and responsibility, not blind equality in distribution.

Should unused college funds vanish after a certain age, or stay open indefinitely for potential late starters? How can parents craft savings plans that motivate ambition without breeding resentment among siblings on different paths?