AITA for not wanting to share my college fund with my little brother?

A 17-year-old girl spent years watching her college fund grow, keeping spreadsheets tracking every dollar for in-state schools and saving most of her paycheck—until her parents informed her that half the money now belonged to her toddler brother. They wanted to retire early and have more time for their new baby; she wanted the debt-free future they had promised. The change happened fifteen months before the application deadline.

What made the story more complicated was the math: the same amount, invested for sixteen more years, could have quadrupled for the boy while leaving her scrambling. Her parents called it their money, their rules; she called it a broken promise that punished planning. The internet came quickly: she wasn’t an asshole for expecting what she’d been led to believe was hers.

‘AITA for not wanting to share my college fund with my little brother?’

The college fund was always presented as hers alone.

The baby brother changed the equation overnight.

The numbers—and the retirement excuse—didn’t add up.

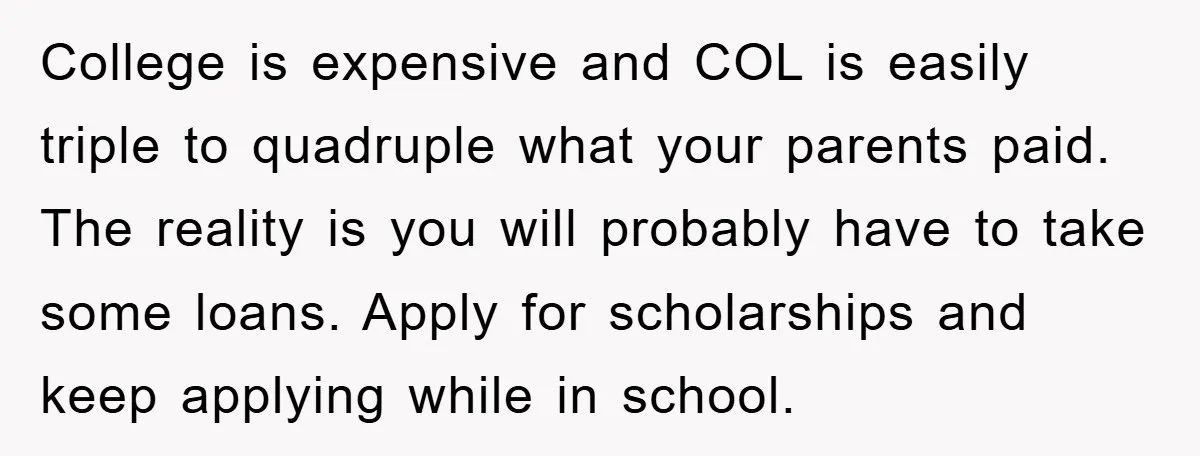

College money is a long-term promise built into the family budget from the day a child is born. While parents repeatedly refer to it as “your college savings,” the young woman sees it as a fixed variable in life’s grandest equation. Withdrawing half the money fifteen months before moving in is not redistribution; it’s a scam, punishing planning and rewarding parental whim. The toddler brother doesn’t need a dime today, but the sister’s spreadsheet is red with five-figure debt.

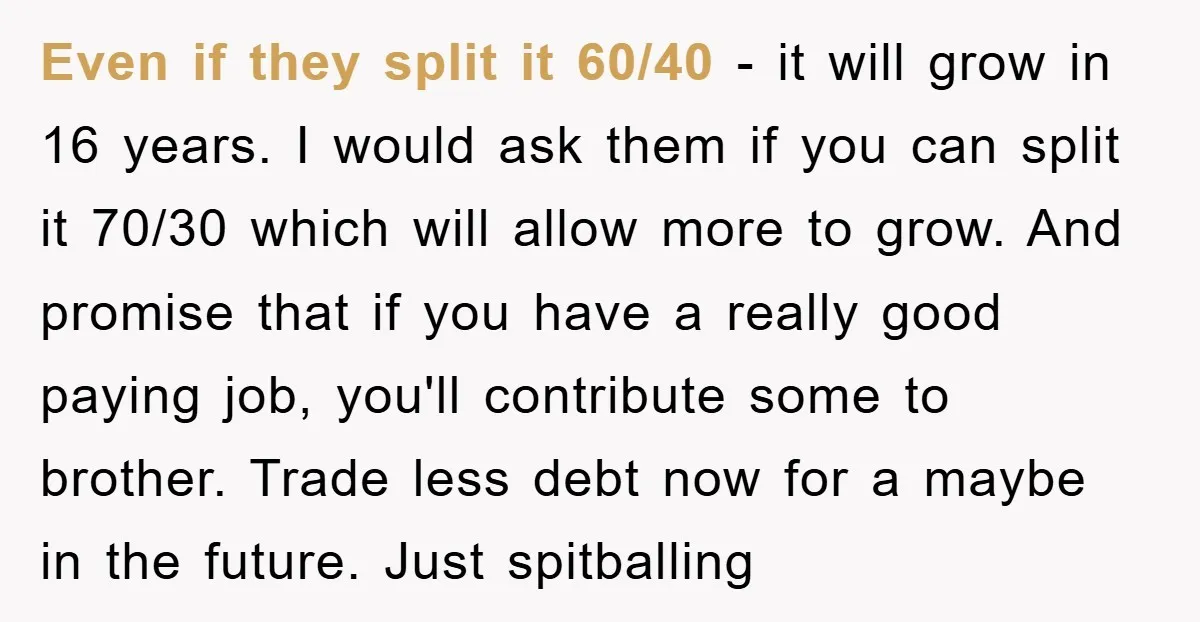

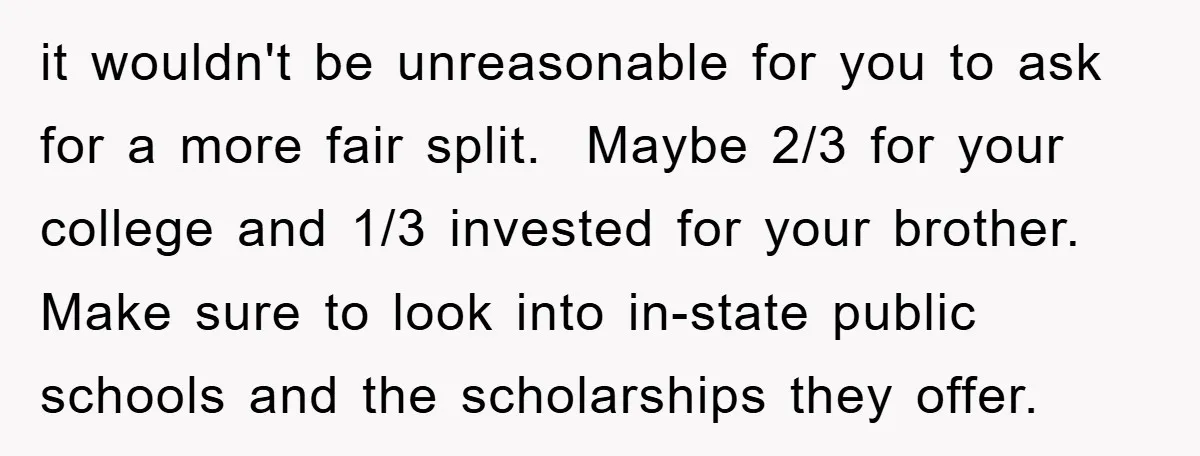

Legally, the money belongs to the parents, but morality doesn’t operate on paper ownership. The rationale for retirement boils down to simple compound interest: any money given to the son now grows 7% annually for sixteen years, potentially quadrupling, while the sister’s half stays the same. A balanced approach—split 70/30, continue to send money monthly, or work part-time—could cover both futures without forcing her into high-interest debt.

Instead, they prioritize beach sunsets over photos of her in a cape and hat. Personal finance author Suze Orman underscored this point in The Money Class: “When parents undercut one child to prioritize another—or their own time—they sow resentment that lasts longer than every penny.” The calculus is brutal: working parents in their mid-forties can delay retirement by twelve months and still be able to quit at fifty-five, easily funding their youngest sibling’s college education. They choose not to expose the true budget divide: convenience over equity, newborn over firstborn.

Let’s dive into the reactions from Reddit:

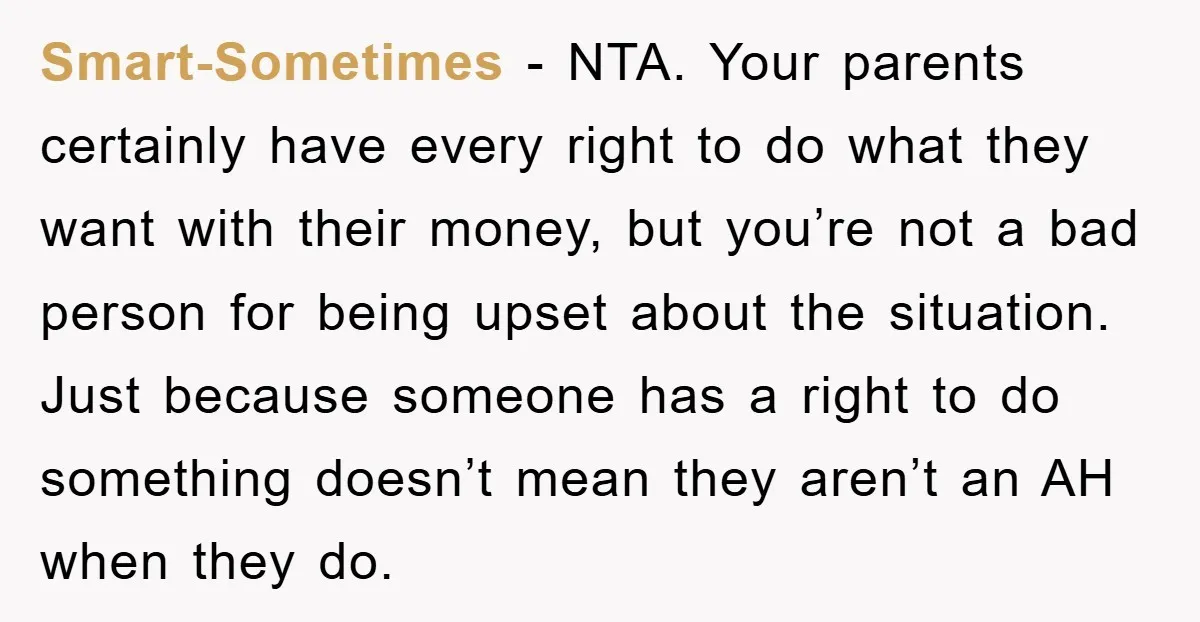

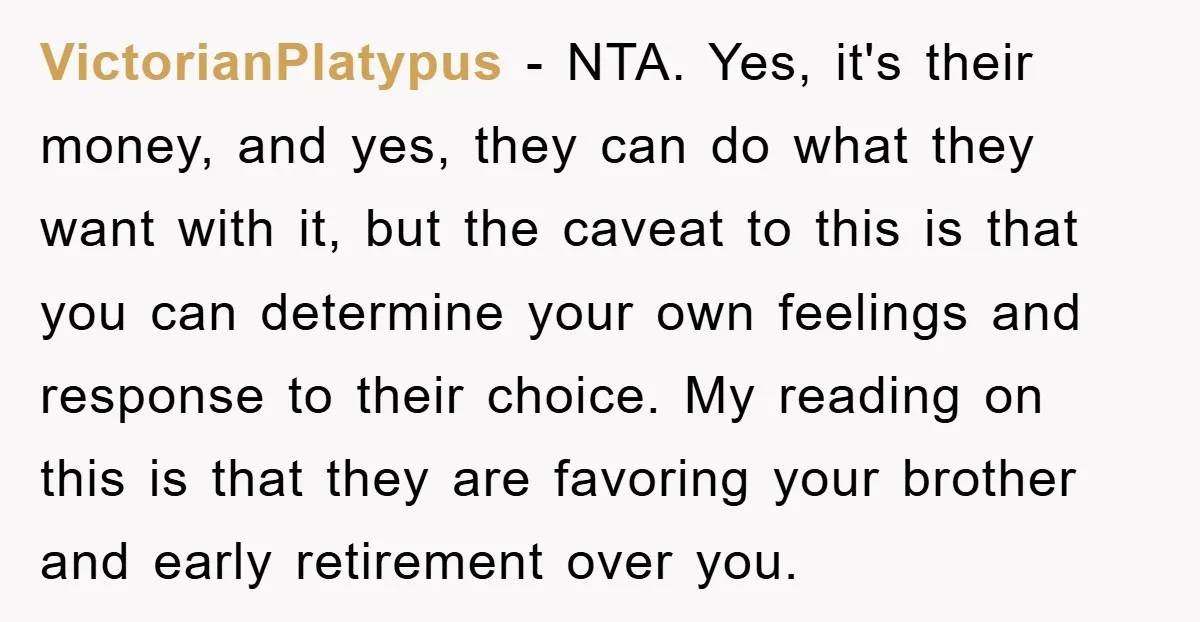

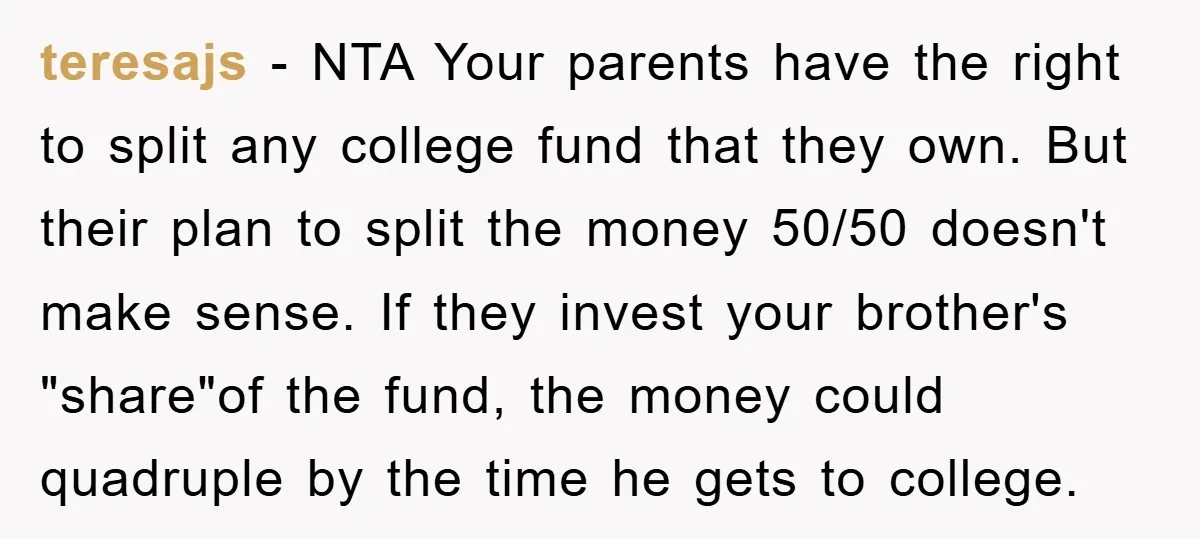

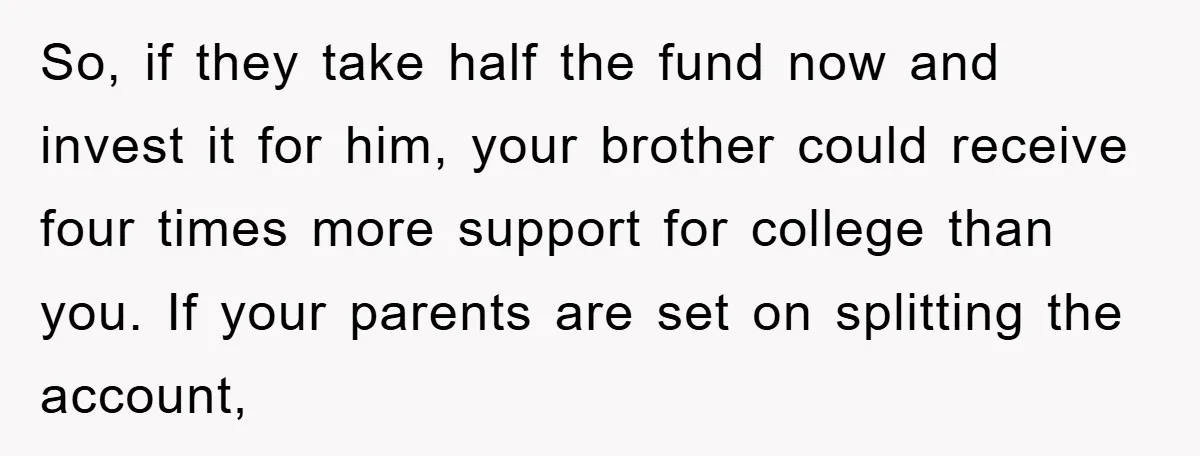

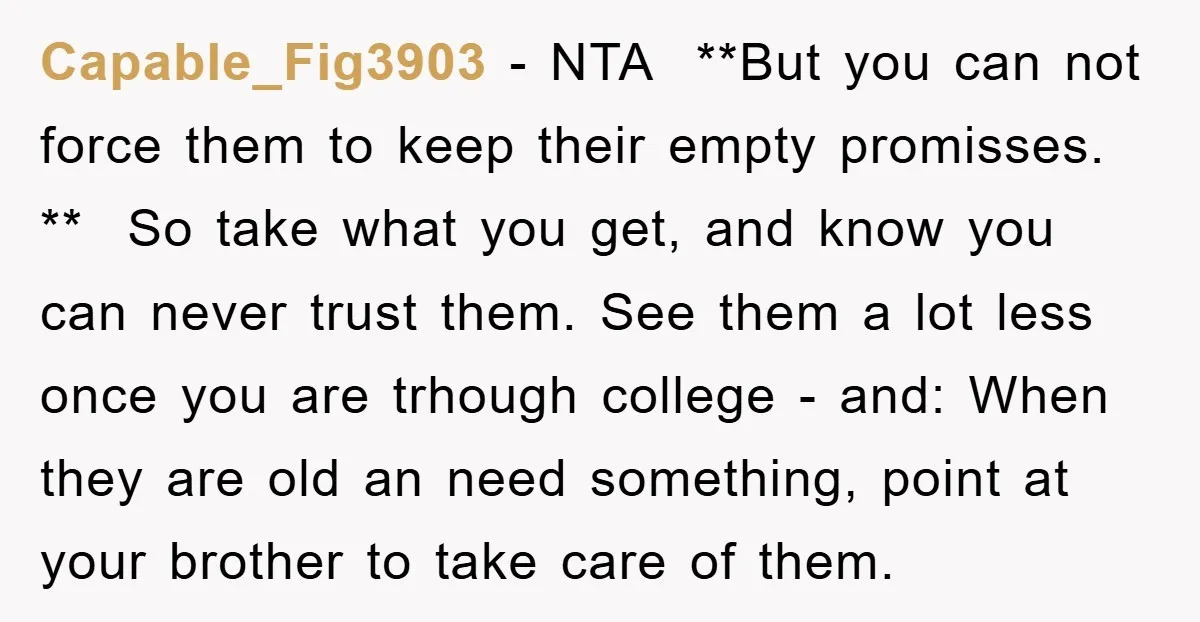

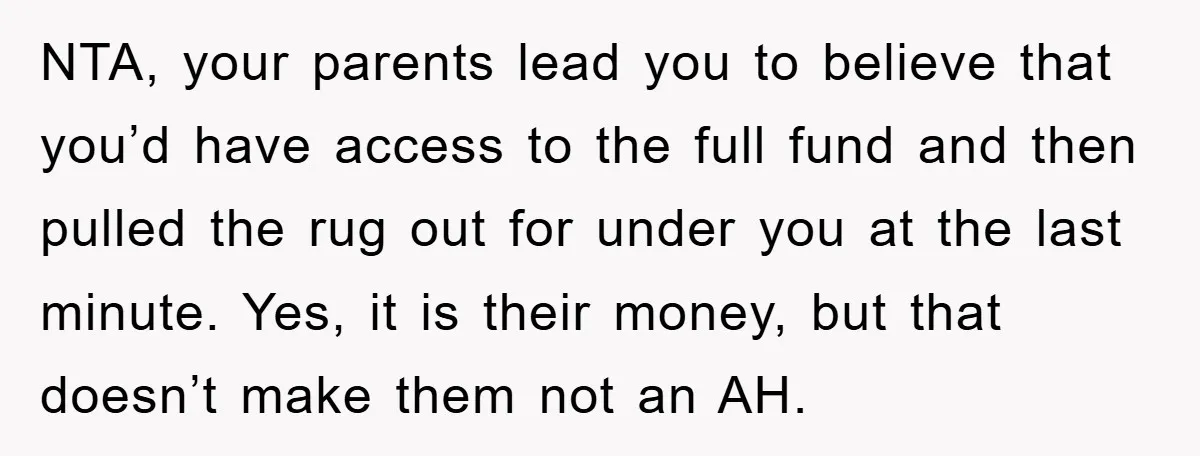

Users slammed the parents for moving the goalposts at the worst possible moment.

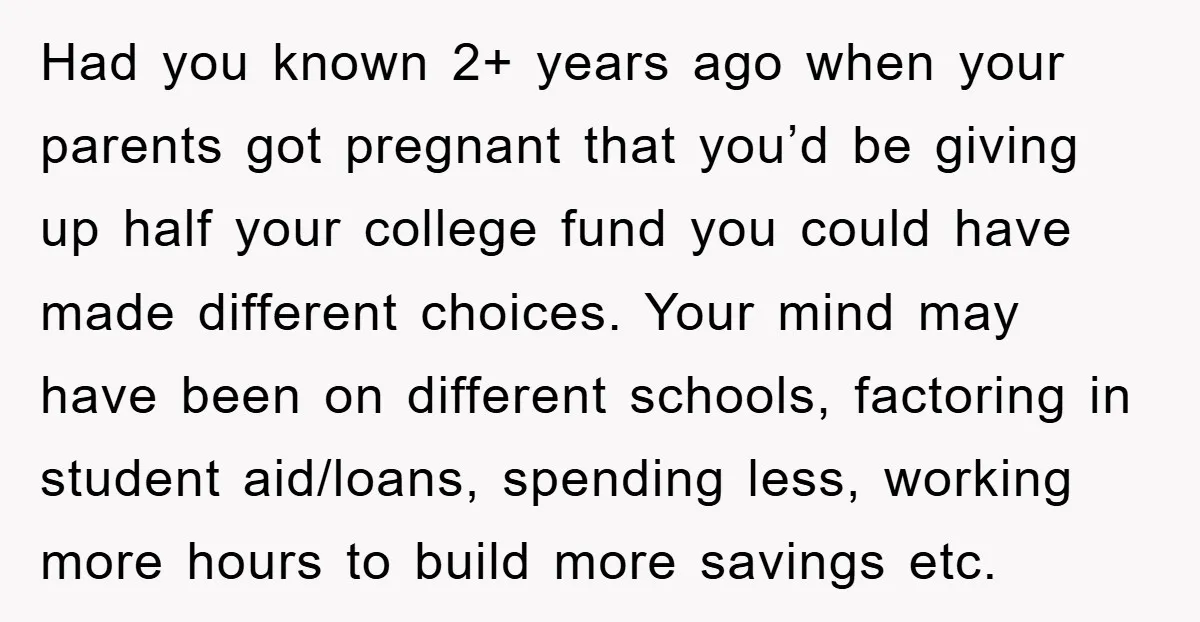

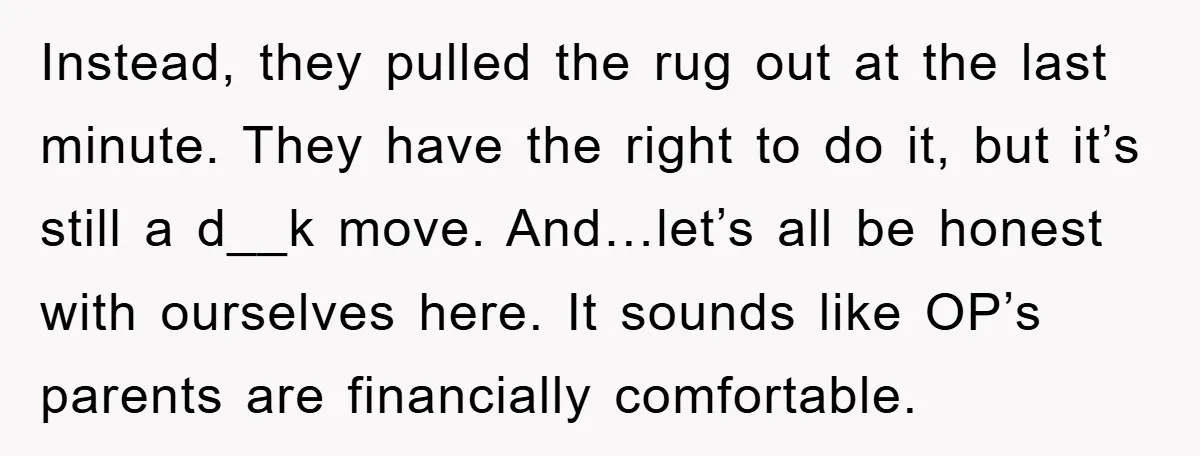

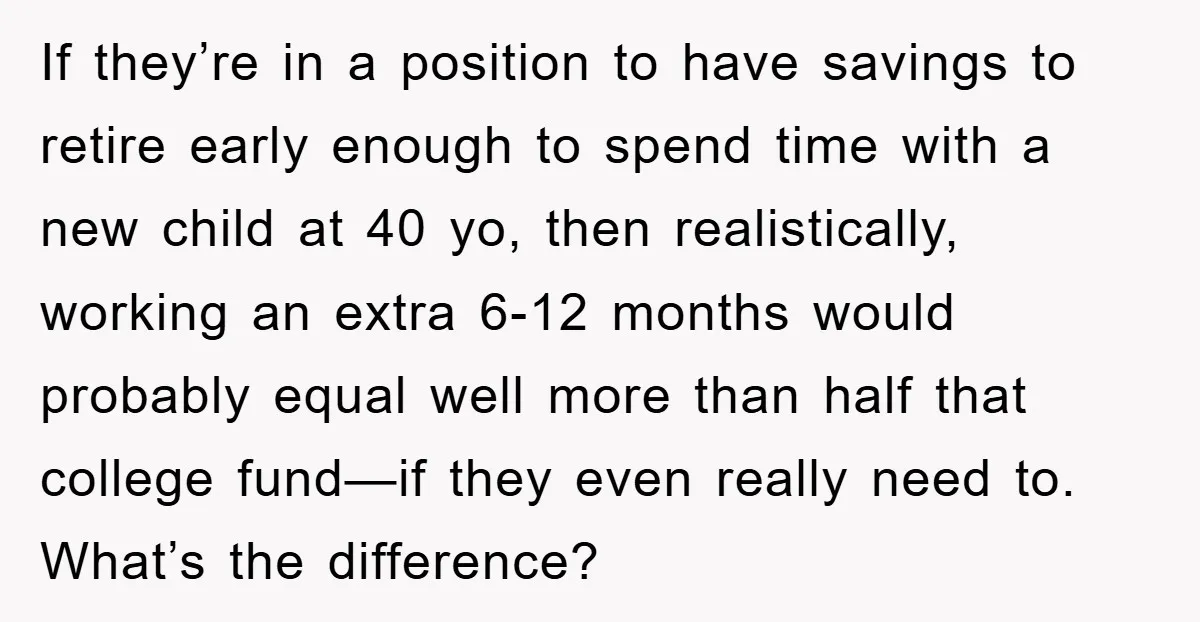

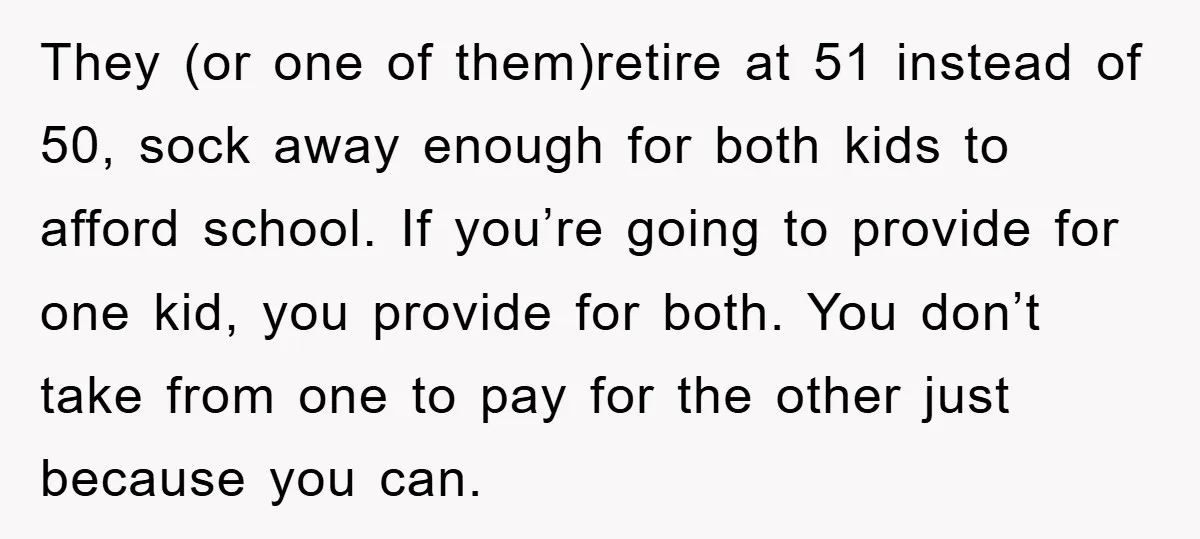

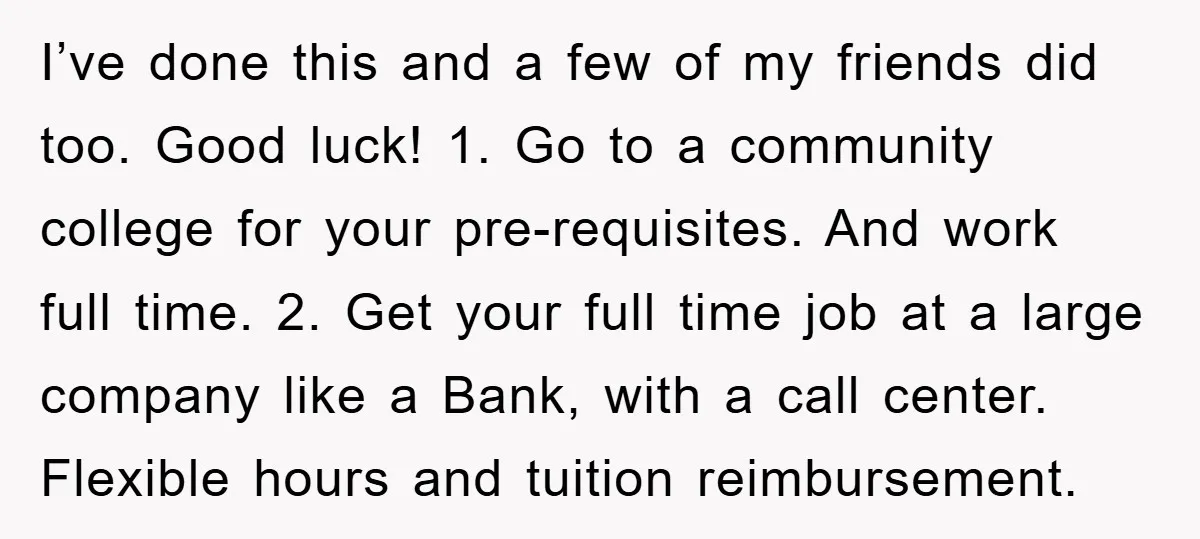

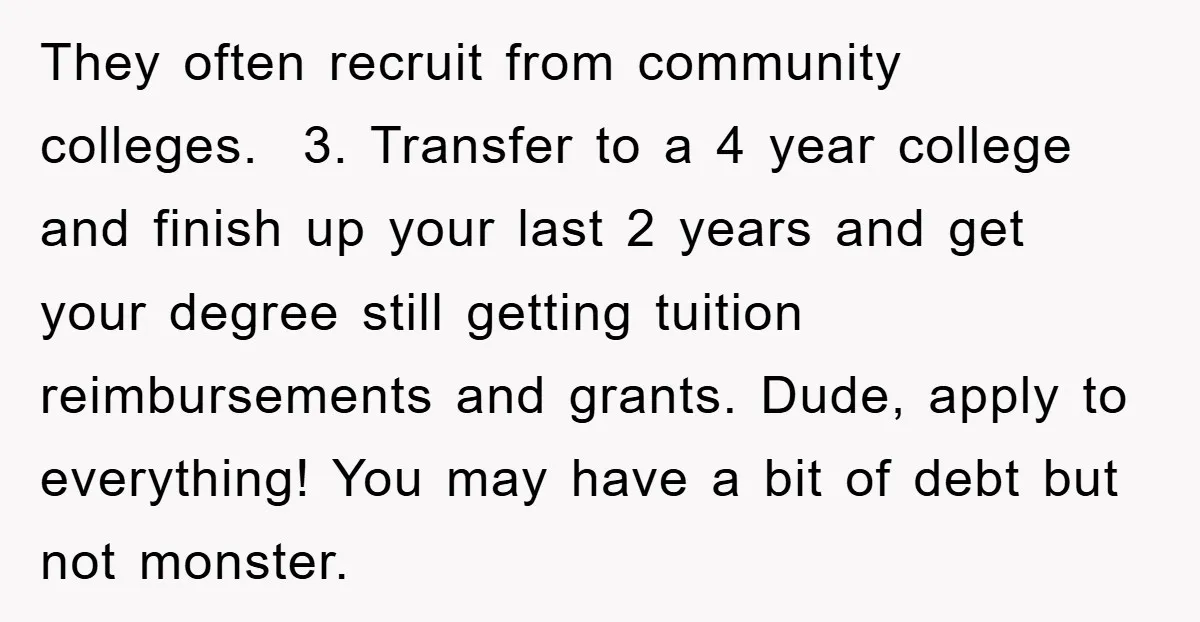

Practical voices offered work-arounds without excusing the betrayal.

![[Reddit User] − It is kind of unfair that your parents led you to believe you would have the entire amount, and then changed their minds right before you needed...](https://en.aubtu.biz/wp-content/uploads/2025/11/wp-editor-1762400147843-1.webp)

![[Reddit User] − NTA. And it is their money. But your parents clearly let you and your brother down. To be frank, you don’t retire early by having a second...](https://en.aubtu.biz/wp-content/uploads/2025/11/wp-editor-1762400158592-7.webp)

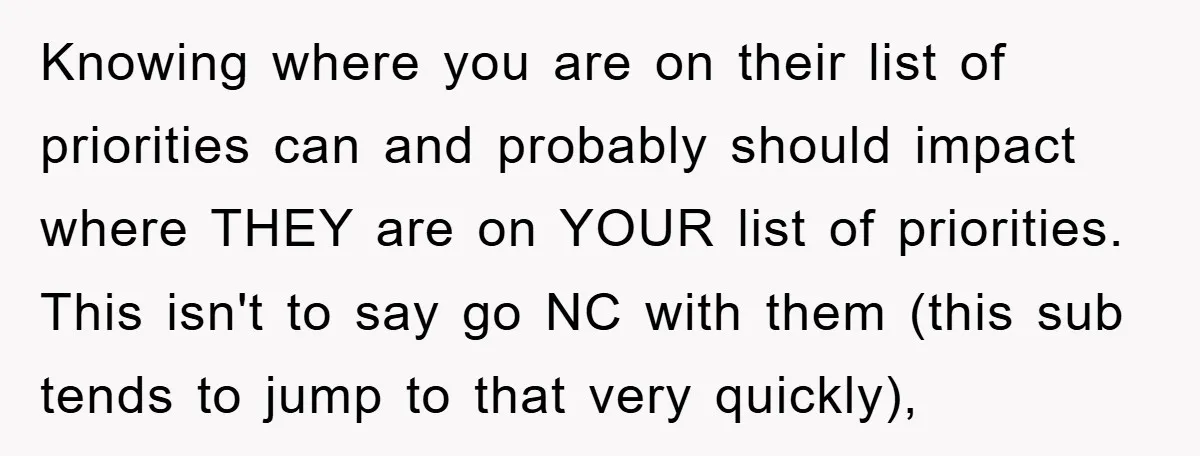

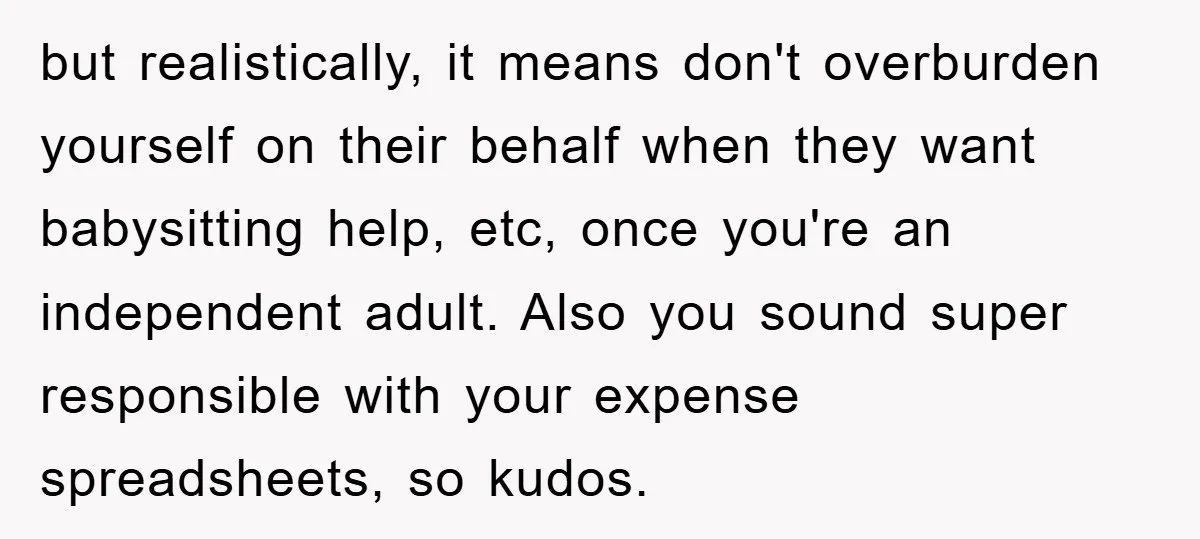

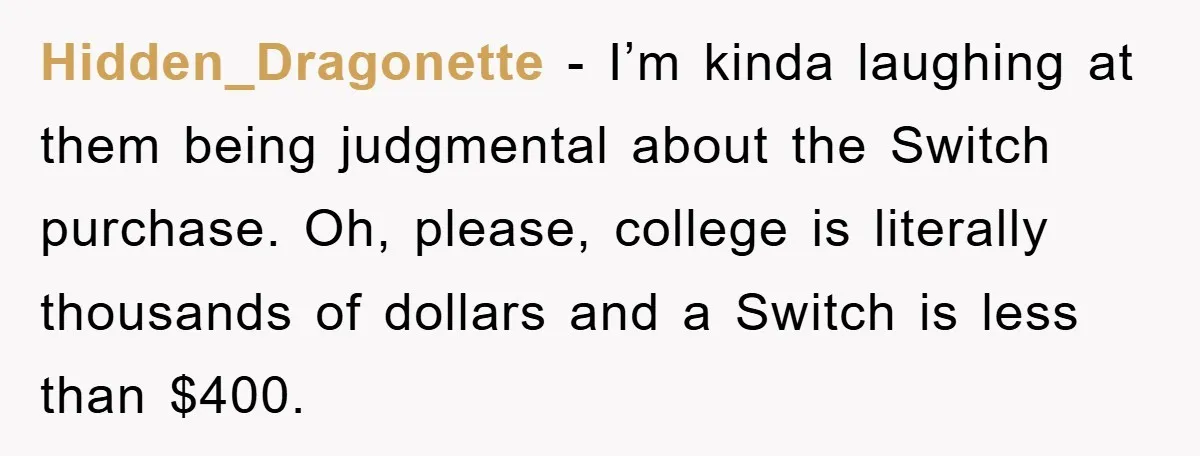

Two replies kept it spicy with zero sympathy for the parents.

She’s not entitled to the money, but she’s entitled to the truth—and the truth is her parents changed the deal after she built her future around it. A fair split would account for time value; instead, they chose convenience and called it parenting. She’ll survive with scholarships, community college, or loans, but the trust fund that broke wasn’t financial.

Have your parents ever moved financial goalposts on you? What creative side hustles got you through college when the safety net vanished? Drop your survival stories below—your spreadsheet hack might save the next senior’s sanity.